Cochlear’s share price has fallen 62.63% year-to-date, erasing more than AU$10 billion in market capitalisation from a company that still earns a 74.9% gross margin and holds more cash than debt. The collapse crystallised on 22 April 2026, when a single-day fall of 35-40% followed a formal FY26 earnings guidance cut of approximately 30% at the midpoint. That event was itself the second profit warning Cochlear had issued in 2026, with the first preceding it and the second explicitly tied to war-related earnings disruptions. For ASX investors, the question is now sharply binary: does AU$97.53 reflect a permanently impaired business, or a quality medical device company repriced to levels it has not seen in years? This analysis works through the catalysts for the sell-off, the underlying fundamentals that remain intact, the valuation picture as it stands, and what investors need to weigh before drawing a conclusion.

What triggered a 35% single-day collapse in April

On 22 April 2026, Cochlear filed a formal guidance revision with the ASX, cutting its FY26 earnings outlook by approximately 30% at the midpoint of prior guidance. The share price fell between 35% and 40% in a single trading session, according to reports from Stocks Down Under and Rask Media. For a company that had spent years trading at a premium growth multiple, the speed of the repricing was severe.

Market Index reporting on Cochlear’s April 2026 selloff, published on the day the event occurred, characterised the move as the company’s worst one-day decline on record, with the share price falling approximately 40% as the market processed a guidance cut of roughly 30% at the midpoint of prior FY26 net profit expectations.

The ASX Listing Rule 3.1 continuous disclosure obligations require listed entities to immediately notify the exchange of any information a reasonable person would expect to have a material effect on share price, which is why Cochlear’s April 2026 guidance revision took the form of a formal ASX filing rather than a broader investor communication.

What made the April event analytically significant was not the size of the cut alone. It was the fact that this was Cochlear’s second profit warning of the year.

- First warning (earlier in 2026): The precise date and numeric detail of the initial guidance revision are not publicly available, but its existence is confirmed by subsequent reporting. It marked the first signal that management’s visibility into forward earnings was deteriorating.

- Second warning (22 April 2026): Explicitly tied to war-related impacts on earnings and broader risk-off sentiment across equity markets. The guidance cut of approximately 30% at the midpoint accompanied a 35-40% single-day share price fall.

“Cochlear has issued its second profit warning of the year as the war impacts earnings and sends the broader sharemarket lower.” — Ausbiz, April 2026

Two downward revisions in a single year carry a different signal from one. A single warning can be absorbed as a discrete event. A second warning tells the market that management’s earnings visibility was materially limited when the first estimate was set, and that further revisions cannot be ruled out. That pattern, more than any individual number, explains why the recovery has been so slow.

The April 2026 selloff was amplified by four geographic headwinds operating simultaneously: cyclical US surgical volume declines, structural European hospital capacity constraints, geopolitical Middle East cancellations, and structural Chinese reimbursement policy changes, a confluence that explains why the share price move exceeded the earnings cut by a wide margin.

When big ASX news breaks, our subscribers know first

The fundamentals that the sell-off has not changed

The share price says one thing. The financial statements say something different, and the dissonance is worth sitting with.

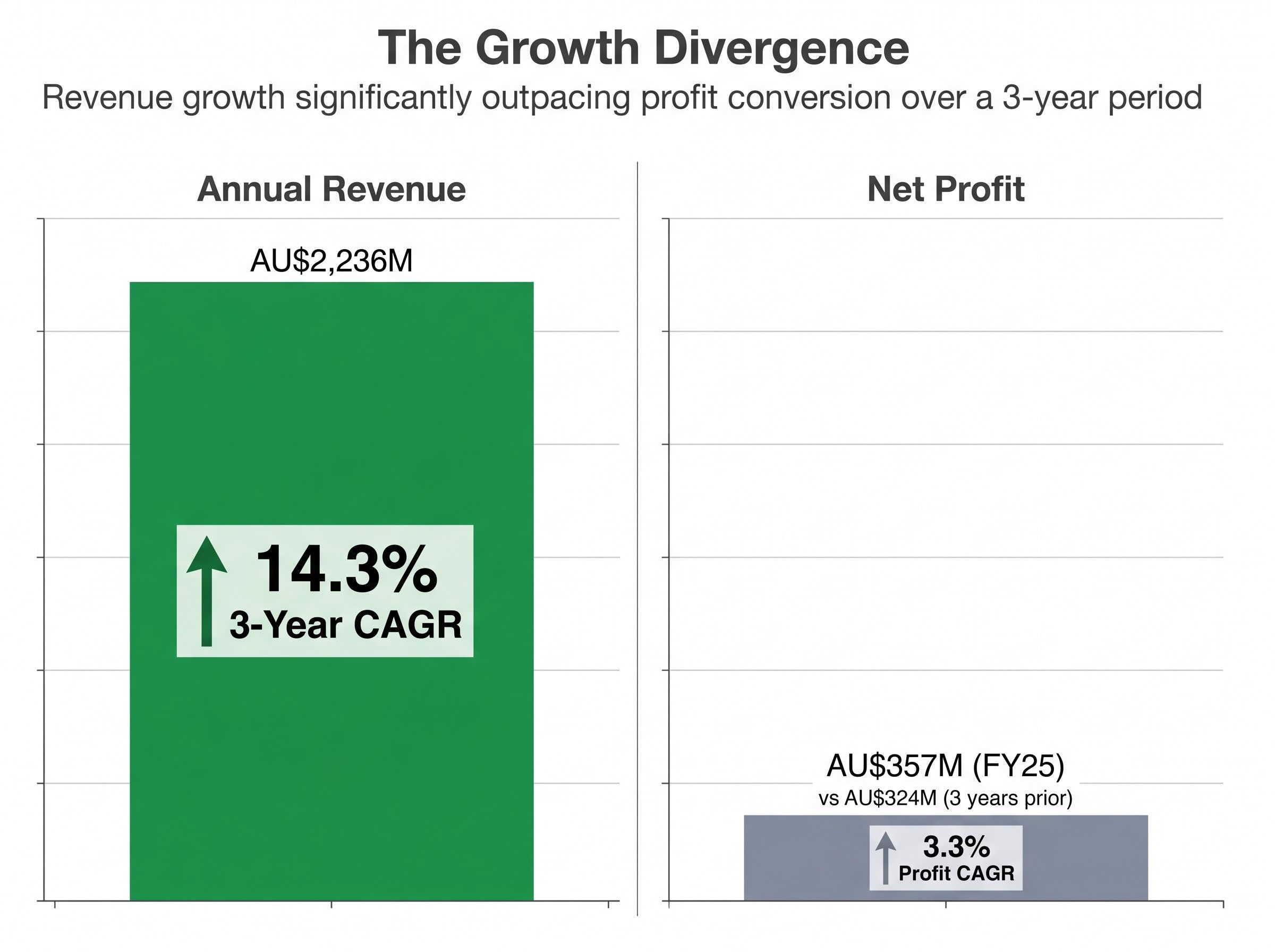

Cochlear reported annual revenue of AU$2,236 million in its most recent fiscal year, reflecting a three-year revenue compound annual growth rate (CAGR) of 14.3%. Gross margin stood at 74.9%, a figure that places the company in rarefied territory across any sector, not just medical devices. The balance sheet carries negative net debt of AU$270 million, meaning Cochlear holds more cash than borrowings.

The profit picture is less straightforward. Net profit of AU$357 million in FY25 compares to AU$324 million three years prior, yielding a profit CAGR of approximately 3.3%. Revenue growing at 14.3% while profit grew at 3.3% is a gap that warrants attention: it suggests operating cost growth or investment spending has absorbed much of the top-line momentum.

| Metric | Most recent figure | Three-year prior / benchmark | What it signals |

|---|---|---|---|

| Annual revenue | AU$2,236M | Three-year CAGR: 14.3% | Strong top-line growth sustained over multiple years |

| Gross margin | 74.9% | Above 70% threshold | Durable pricing power and structural competitive advantage |

| Net profit | AU$357M (FY25) | AU$324M (three years prior); CAGR: 3.3% | Profit conversion lagging revenue growth |

| Net debt | Negative AU$270M (net cash) | N/A | No near-term solvency risk; no reliance on credit markets |

| Debt-to-equity ratio | 13.2% | N/A | Conservative balance sheet structure |

| Return on equity (FY24) | 19.9% | N/A | Capital deployed efficiently relative to shareholder equity |

Gross margins above 70% are rare in any sector and signal pricing power that competitors cannot easily erode. A net cash balance sheet means Cochlear is not dependent on external financing to fund operations during a period of reduced earnings, a buffer that limits downside risk when sentiment is negative.

Why Cochlear commands 60% of the global market and why that matters now

What cochlear implants are and who needs them

A cochlear implant is a surgically placed electronic device that bypasses damaged portions of the inner ear and directly stimulates the auditory nerve, enabling a form of hearing for individuals with severe to profound hearing loss. In developed markets, cochlear implants are considered the standard of care for children diagnosed with this level of hearing loss, not an optional or emerging treatment.

The addressable market is structurally recurring. Each year, a new cohort of children is diagnosed, and population ageing in developed economies continues to expand the adult candidate pool. This is not a market that fluctuates with consumer discretionary spending or commodity cycles.

Why 60% market share is structurally entrenched

Cochlear holds approximately 60% of the global cochlear implant market, according to Morningstar Australia, which classifies the stock as “Defensive” within Healthcare / Medical Devices. Founded in Sydney in 1981, the company has distributed over 750,000 implantable devices to date.

The market share is entrenched for a specific structural reason: once a patient receives a Cochlear implant, processor upgrades over that patient’s lifetime are almost exclusively Cochlear products. This post-implant lock-in creates a recurring revenue stream that competitors cannot easily disrupt.

The company’s three product categories each serve a distinct role in this dynamic:

- Cochlear implants: The primary surgical product, representing the initial device sale and the basis for the lifetime relationship with the patient

- Bone-anchored hearing aids: An alternative for patients whose hearing loss profile does not suit a cochlear implant, expanding the addressable market

- Sound processors: The externally worn component that pairs with the implant, upgraded multiple times over a patient’s life and representing the recurring revenue mechanic

Competitors including MED-EL, Advanced Bionics, and Demant are active in the space, but no 2025-2026 evidence points to a specific competitor move as a driver of Cochlear’s 2026 guidance cuts. The sell-off, based on available reporting, is operationally and geopolitically driven rather than competitively structural.

The valuation picture after a 62% reset

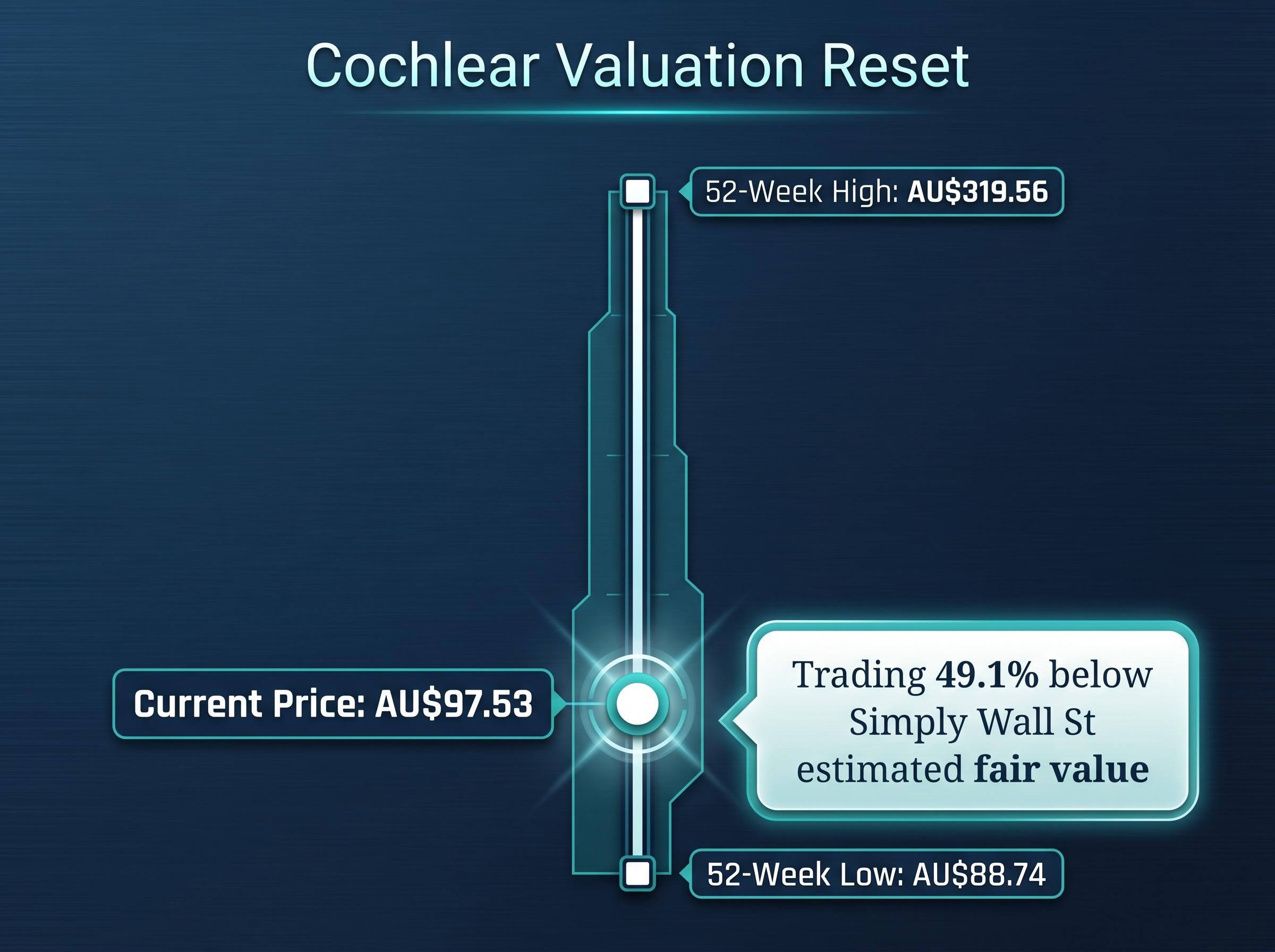

Cochlear traded at a 52-week high of AU$319.56. It now trades at AU$97.53, with a market capitalisation of AU$6.378 billion as at 22 May 2026, according to Intelligent Investor. The 52-week low sits at AU$88.74, meaning the current price is closer to the trough than the peak by a wide margin.

That is a fall of more than 69% from peak to trough, and approximately 62.63% year-to-date. For a company that Morningstar classifies as “Defensive,” the scale of the reset is striking.

Simply Wall St estimates that COH is “trading at 49.1% below our estimate of its fair value” and “trading at good value compared to peers and industry.”

That 49.1% discount to estimated fair value, paired with a forecast earnings growth rate of 8.07% per year, frames the stock as significantly undervalued on one analytical model. Any single valuation model carries limitations, and the Simply Wall St estimate should be treated as a data point rather than a conclusion.

Broker price targets for Cochlear following the guidance cut span a wide range, from A$107.17 at Morgans (Hold) to approximately A$169 at Jarden (Buy), a dispersion that reflects fundamental disagreement not about business quality but about whether the earnings impairment is temporary or permanent.

Intelligent Investor conducted a formal review of Cochlear at a price of AU$99.58 on 23 April 2026, one day after the major guidance downgrade. The timing and structure of that review confirm that at least one credible Australian equity research outlet was reassessing the stock at current price levels.

Key valuation reference points:

- Current price: AU$97.53

- 52-week high: AU$319.56

- 52-week low: AU$88.74

- Simply Wall St fair value discount: 49.1% below estimated fair value

- Forecast earnings growth: 8.07% per year

The distance between the 52-week high and the current price is not the same as a margin of safety. A stock that was previously overvalued and has since been cut in half may still be fully valued. The relevant question is what the current price implies about future earnings, and whether the guidance cuts have already been fully priced in.

What the guidance cuts actually mean for Cochlear’s earnings power

What the warnings appear to reflect

There is an analytical distinction between cyclical earnings disruption and structural impairment. Cyclical disruption includes war-related macro headwinds, risk-off sentiment, and one-time demand dislocations in specific geographies. Structural impairment means loss of market share, product obsolescence, or regulatory reversal.

Based on available evidence, Cochlear’s 2026 warnings sit more consistently in the former category. No reporting attributes the guidance cuts to a loss of competitive position, a regulatory setback, or a technological displacement. The stated drivers are geopolitical disruptions and broader market weakness.

The revenue-to-profit conversion gap, however, is a legitimate pre-existing concern. Revenue growing at 14.3% CAGR while profit grew at only 3.3% is a question investors should have been asking before the guidance cuts. The cuts have made it urgent. If margin pressure persists even after the geopolitical disruptions ease, the profit trajectory may remain muted relative to the top line.

What investors still do not know

Several informational gaps should inform any investment decision made at current prices:

- Precise revised FY26 guidance ranges: The specific NPAT and revenue figures from the April 2026 ASX filing are not publicly available through open web sources. Investors are working with secondary reporting of an approximate 30% midpoint reduction.

- Full scope of geopolitical impact by geography: Cochlear derives an estimated 80% of revenue from developed markets and approximately 20% from emerging markets (note: geographic split is sourced from Morningstar’s profile and has not been independently verified). Which geographies bore the brunt of the disruption remains unclear.

- Whether further guidance revisions are possible: Two warnings in a single year raise the question of whether a third is possible before the 30 June fiscal year end.

- Timing of Cochlear’s next formal market update: The date of the next scheduled ASX disclosure that would provide updated earnings visibility has not been confirmed in available sources.

For readers wanting to understand the precise revised earnings numbers underpinning the current valuation debate, our full explainer on Cochlear’s revised NPAT guidance range covers the A$290-330 million target in detail, compares DCF and AlphaSpread consensus models, and breaks down what the 31% midpoint reduction implies for long-run earnings power at the current share price.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A quality business at a reset price is not the same as a safe investment

The case for Cochlear and the case against it are both grounded in real evidence. The challenge for investors is that neither case invalidates the other at AU$97.53.

What the bulls see:

- A 74.9% gross margin signalling durable pricing power

- A net cash position of AU$270 million removing solvency risk

- 60% global market share with a structurally entrenched upgrade revenue model

- Morningstar’s “Defensive” classification within Healthcare

- Simply Wall St’s estimate of 49.1% below fair value

- Forecast earnings growth of 8.07% per year

What the bears see:

Short interest in COH running at 4-5.7% of float as of May 2026 signals active professional scepticism about a near-term recovery, and supply chain friction from China rare earth export restrictions, which caused approximately 5-7% shipment delays in Q1 2026, adds a dimension to the bear case that the earnings guidance cuts alone do not capture.

- Two profit warnings in a single year, signalling limited management visibility

- An approximately 30% guidance cut at the midpoint, with precise revised figures unavailable

- A three-year revenue-to-profit CAGR divergence (14.3% vs 3.3%) suggesting margin pressure predates the geopolitical disruption

- Incomplete forward guidance visibility, with no confirmed date for the next formal update

- The possibility that further revisions remain on the table before the FY26 close

Investors weighing Cochlear at current levels face three specific next steps: review the company’s next formal ASX market update for revised FY26 guidance ranges; monitor whether the geopolitical disruptions cited are temporary or structurally deepening; and assess whether COH’s “Defensive” classification offers diversification value within their own portfolio positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.