A stock trading 65% below its 12-month high, sitting just 6.8% above its 52-week low, with a price-to-sales ratio that has collapsed from 9.18x to 2.77x. That is the quantitative picture confronting anyone evaluating Cochlear Limited (ASX: COH) in May 2026.

A single ASX announcement on 22 April 2026 triggered an approximately 39% single-day share price fall, sending the stock to levels not seen since 2016. What followed was a rapid reassessment by growth investors across the Australian market, as one of the ASX’s most reliably premium-rated healthcare names repriced in a matter of hours. This analysis examines what the price-to-sales compression actually means for Cochlear’s stock, whether the drivers of the de-rating are cyclical or structural, and what the valuation data signals for growth-focused ASX investors evaluating the company at current levels.

What Cochlear actually is and why it commands premium valuations

Cochlear was founded in Sydney in 1981 and has evolved into the world’s largest cochlear implant manufacturer. The company operates across more than 180 countries, employs more than 5,000 staff, and has distributed over 750,000 implantable devices across its operating history. That installed base is not just a historical statistic; it is the foundation of a recurring revenue model, because each implant recipient becomes a long-term customer for sound processor upgrades.

The business spans three product categories:

- Cochlear implants: Surgically implanted devices that bypass damaged parts of the inner ear to directly stimulate the auditory nerve, providing hearing to individuals with severe-to-profound hearing loss.

- Bone conduction systems (including the Osia System): Devices that transmit sound through the bone to the inner ear, suited for patients with conductive hearing loss or single-sided deafness.

- Acoustic implants: Partially implantable devices designed for patients with mixed or moderate hearing loss who may not benefit from conventional hearing aids.

This product architecture, combined with the largest global market share in cochlear implants as of 2023, has historically justified premium valuation multiples. When earnings are predictable and the competitive moat is deep, markets pay up.

A structural growth market, not a cyclical one

Three independent market research firms converge on the same conclusion about the global cochlear implant market. Fortune Business Insights sized it at US$1.69 billion in 2023 with a 9.2% compound annual growth rate (CAGR) through 2032. Grand View Research estimated US$1.67 billion with a 7.4% CAGR through 2030. MarketsandMarkets placed it at US$1.8 billion in 2024 with an 8.5% CAGR through 2029.

The convergence matters: regardless of methodology, the addressable pool of untreated hearing loss remains vast, providing long-run runway independent of near-term surgical capacity constraints.

When big ASX news breaks, our subscribers know first

The April 2026 earnings shock and what caused it

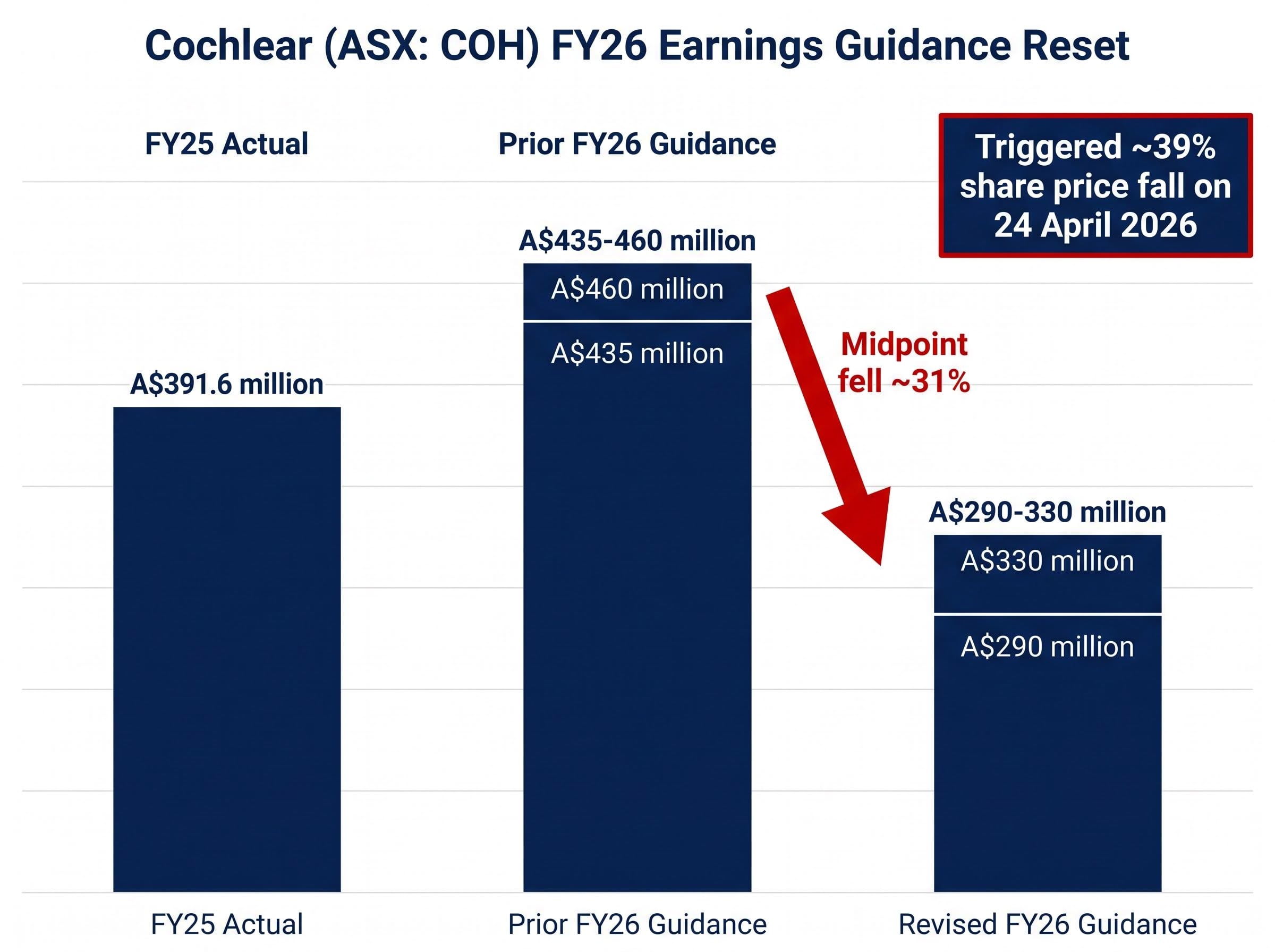

The sequence began on 22 April 2026, when Cochlear issued an ASX announcement titled “Trading update and reduction to FY26 earnings guidance.” The numbers told the story before the commentary did.

Guidance reset: FY26 underlying net profit after tax (NPAT) was revised to A$290-330 million, down from prior guidance of A$435-460 million. The midpoint fell approximately 31%.

The market’s response was immediate. On 24 April 2026, Cochlear shares fell approximately 39% in a single session, closing around A$101.76 after touching an intraday low of A$97.88.

| Metric | FY25 Actual | Prior FY26 Guidance | Revised FY26 Guidance |

|---|---|---|---|

| Revenue | A$2,355.8 million (up 4%) | Not separately guided | Not separately guided |

| Underlying NPAT | A$391.6 million (up 1%) | A$435-460 million | A$290-330 million |

| Cochlear Implant Units | 46,800 (up 11%) | Not disclosed | Not disclosed |

Three specific operational drivers underpinned the cut. TheBull and Kalkine, both reporting on 24 April 2026, identified softer-than-expected demand in the United States and Europe, hospital staffing and capacity constraints limiting surgery volumes, and delays in public tender decisions and reimbursement approvals across select markets.

The analytical question this raises is direct: are these drivers cyclical, meaning capacity backlogs and policy timelines that will normalise, or structural, reflecting a genuine loss of competitive position? The distinction shapes every valuation conclusion that follows.

Cochlear’s April selloff was amplified well beyond the arithmetic of the earnings cut itself, with four simultaneous geographic headwinds, forced institutional selling, and a collapse in guidance credibility all compressing the share price in ways that a simple 31% profit downgrade would not have produced on its own.

How price-to-sales fits Cochlear’s investment profile

When a company’s near-term earnings have just been reset by 31% at the midpoint, the price-to-earnings (P/E) ratio becomes a less reliable valuation tool. Three characteristics of the current situation explain why price-to-sales (P/S) provides a clearer lens:

- P/E ratios are distorted by earnings volatility. One-off items, margin swings, and guidance resets can produce P/E readings that overstate or understate the market’s true assessment of the business. When earnings are in flux, the ratio becomes noisy.

- Revenue is more stable than profit. Price-to-sales strips out margin variability and measures what the market is paying for the underlying revenue base, a figure less susceptible to temporary cost pressures or demand timing.

- For growth companies, P/S relative to historical averages captures the growth premium. Comparing the current P/S to its long-run average reveals how much future growth the market is currently willing to pay for, or how much it has stopped paying for.

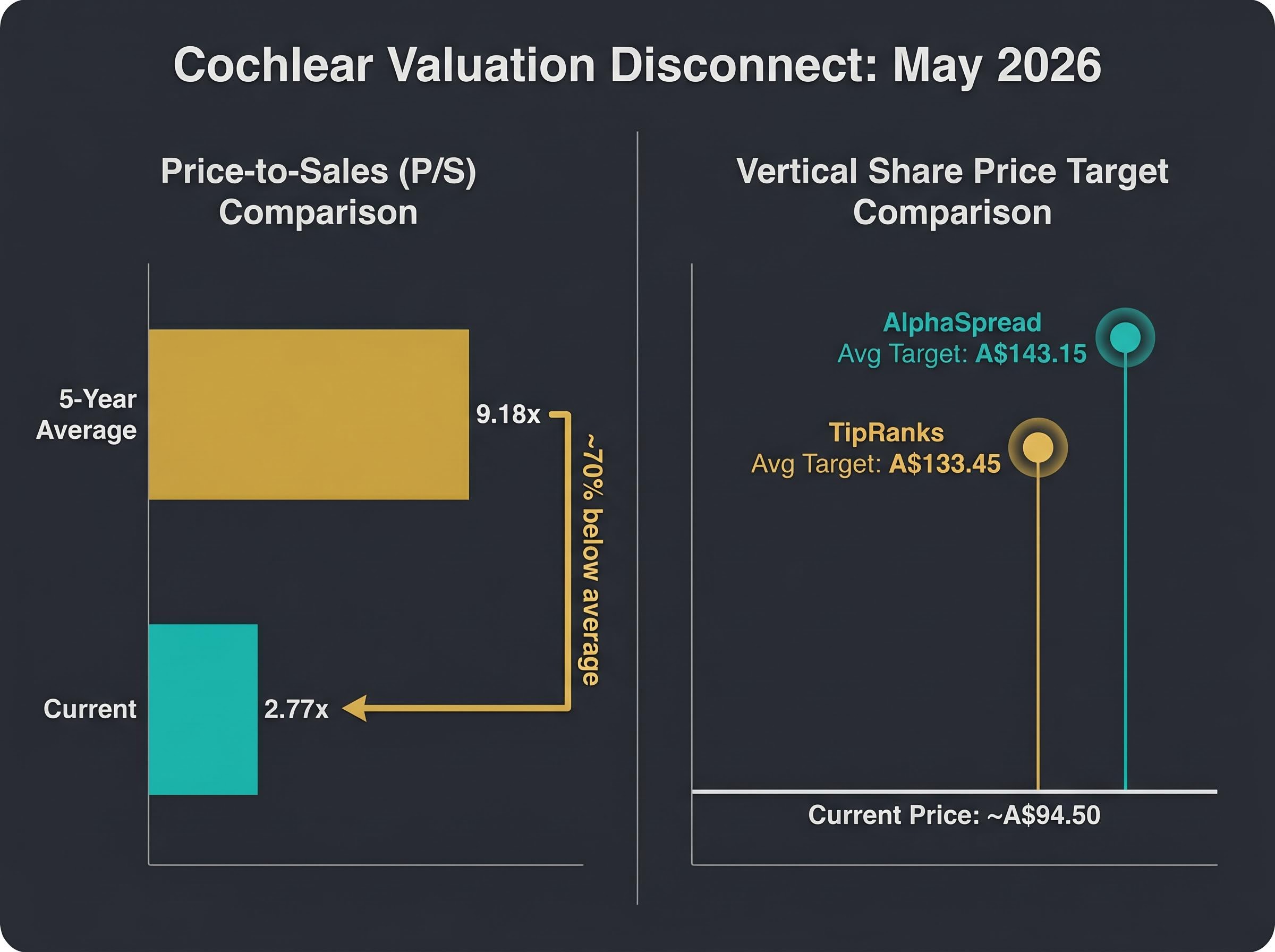

Cochlear’s FY25 revenue of A$2,355.8 million provides the denominator. The current P/S ratio of 2.77x sits against a five-year historical average of 9.18x.

GuruFocus data as at 16 June 2025 showed Cochlear’s P/E was already near its two-year low, with the stock trading at A$286.24 and a trailing P/E of 50.66. Compression had begun well before the April guidance cut.

The broader ASX healthcare de-rating as context

Cochlear’s multiple compression did not occur in isolation. Livewire Markets and the Australian Financial Review documented through 2024 and 2025 how rising interest rates drove 30-50% multiple compression across premium ASX healthcare names including CSL, ResMed, and Cochlear itself.

The April 2026 guidance cut accelerated a process already underway. That context matters for interpreting where “normal” multiples might eventually settle: a return to 9.18x P/S may require both earnings recovery and a broader re-rating of the ASX healthcare sector.

The ASX healthcare sector de-rating that compressed Cochlear’s multiple alongside CSL and ResMed was not a uniform event: bond-proxy unwinding, GLP-1 sentiment in the case of ResMed, and dual earnings-and-multiple compression at CSL each operated through different mechanisms, with RBA rate direction, CSL EPS trajectory, and domestic margin stabilisation at Ramsay and Sonic now identified as the four observable catalysts for any eventual re-rating.

What the 2.77x P/S ratio actually signals

The gap between 2.77x and 9.18x is not incremental. It represents approximately 70% compression from the five-year average, a magnitude the market has not assigned to this stock in recent memory outside the current drawdown.

A 70% compression in price-to-sales ratio is historically unusual for Cochlear and reflects a genuine repricing of earnings risk, not a routine sector rotation.

Simply Wall St’s discounted cash flow (DCF) model, a method that estimates a company’s value by projecting future cash flows and discounting them to present value, places Cochlear 50.3% below estimated fair value. That estimate embeds assumptions about earnings recovering at approximately 8.07% per year and revenue growing at 8.2% per annum beyond the FY26 reset.

Analyst consensus offers another reference point. AlphaSpread reports an average 12-month price target of A$143.15 (range: A$95.95 to A$326.14). TipRanks places the 12-month average at A$133.45. Against a current share price of approximately A$94.50-95.37, those averages imply 40-51% upside if consensus proves correct.

| Valuation Metric | Current Level | Reference Point | Implied Gap |

|---|---|---|---|

| Price-to-Sales | 2.77x | 9.18x (5-year average) | ~70% below average |

| Share Price vs Fair Value (Simply Wall St DCF) | ~A$94.50 | Estimated fair value | 50.3% below |

| Share Price vs Analyst Target (AlphaSpread) | ~A$94.50 | A$143.15 (average) | ~51% upside |

| Share Price vs Analyst Target (TipRanks) | ~A$94.50 | A$133.45 (average) | ~41% upside |

The low-end analyst target of A$95.95 sits near current trading levels. That detail warrants attention: it suggests at least some analysts see limited near-term upside even if the business stabilises at revised guidance levels.

The recovery case and the risks that complicate it

Recovery drivers:

- Cochlear implant unit growth of 11% in FY25 (to 46,800 units) demonstrates that underlying demand exists and is growing

- Structural hearing loss trends, including ageing populations and expanded clinical indications such as bilateral implants in children and single-sided deafness, remain intact across developed and developing markets

- R&D investment of approximately 12% of sales supports the medium-term product roadmap, including the Nucleus 8 sound processor rollout and Osia System approvals

- FY25 full-year dividend of A$4.90 per share (up 8%) signals board confidence in the long-term earnings trajectory even as near-term profit resets

Risk factors:

- The FY26 guidance range of A$290-330 million represents a genuine earnings reset, not merely a timing delay; the midpoint sits 21% below FY25 actual NPAT

- Hospital capacity constraints and reimbursement approval timelines are external variables Cochlear cannot control or accelerate

- The Oticon Medical acquisition, agreed in 2022, has faced regulatory complexity across multiple jurisdictions, delaying expected integration synergies and incremental revenue

- Earnings predictability, the quality that historically justified premium multiples, has been materially impaired

Stocks Down Under noted on 24 April 2026 that prior consensus FY27 earnings per share (EPS) estimates sat at approximately A$7.54, representing roughly A$543 million in profit. The credibility of a recovery to those levels now depends entirely on execution through FY26.

Short interest in COH has tracked between 4% and 5.7% of shares on issue, a level that signals active professional scepticism about the pace and reliability of the earnings recovery, even as the company’s 19.9% return on equity and the recurring revenue floor from its 750,000-strong installed base argue that the underlying franchise remains structurally sound.

What needs to happen for the multiple to re-rate

Three observable triggers would signal a turning point: evidence of US and European surgical volume recovery in half-year trading updates, public tender decisions resolving in Cochlear’s favour across key reimbursement markets, and the FY26 result tracking toward the upper end of the A$290-330 million guidance range. These represent an investor’s watchlist, not a prediction.

Beyond the numbers: what Cochlear’s valuation implies for investors

A P/S ratio 70% below its five-year average is historically unusual for Cochlear. It reflects a genuine repricing of earnings risk: the market is no longer willing to pay a premium multiple against uncertain near-term profit delivery. At the same time, the business model, global market leadership, and long-run demand drivers have not changed.

The current P/S compression is historically unusual for Cochlear, but it is not independently sufficient as a signal to act on. It is a starting point for deeper analysis, not a conclusion.

Kalkine, TheBull, and Simply Wall St all frame the stock as trading at a discount to historical valuations and to estimated fair value. Each cautions that the timing and pace of recovery depends on variables that remain unresolved as of May 2026, including surgical volumes, reimbursement decisions, and FY26 earnings execution.

Simply Wall St forecasts revenue growth of 8.2% per annum and earnings growth of 8.07% per year beyond the reset. Both AlphaSpread and TipRanks consensus targets imply 40-51% upside, though the low-end target of A$95.95 sits near current trading levels, a reminder that not all analysts share the same recovery timeline.

The appropriate response to this data is further due diligence: DCF modelling against multiple earnings scenarios, monitoring FY26 trading updates as they are released, and assessing surgical volume data as it becomes available. The valuation compression provides a framework for analysis. The investment decision requires more.

For investors ready to move beyond the P/S ratio and build the complete picture, our comprehensive walkthrough of ASX share valuation methods covers the five-step sequence of P/S screening, EV/EBITDA benchmarking, DCF modelling, and DDM where applicable, including worked examples that show how each method corrects the blind spots of the previous one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.