Credit Corp’s Share Price Gap: a Record Half or a Guidance Cut?

1 hr ago

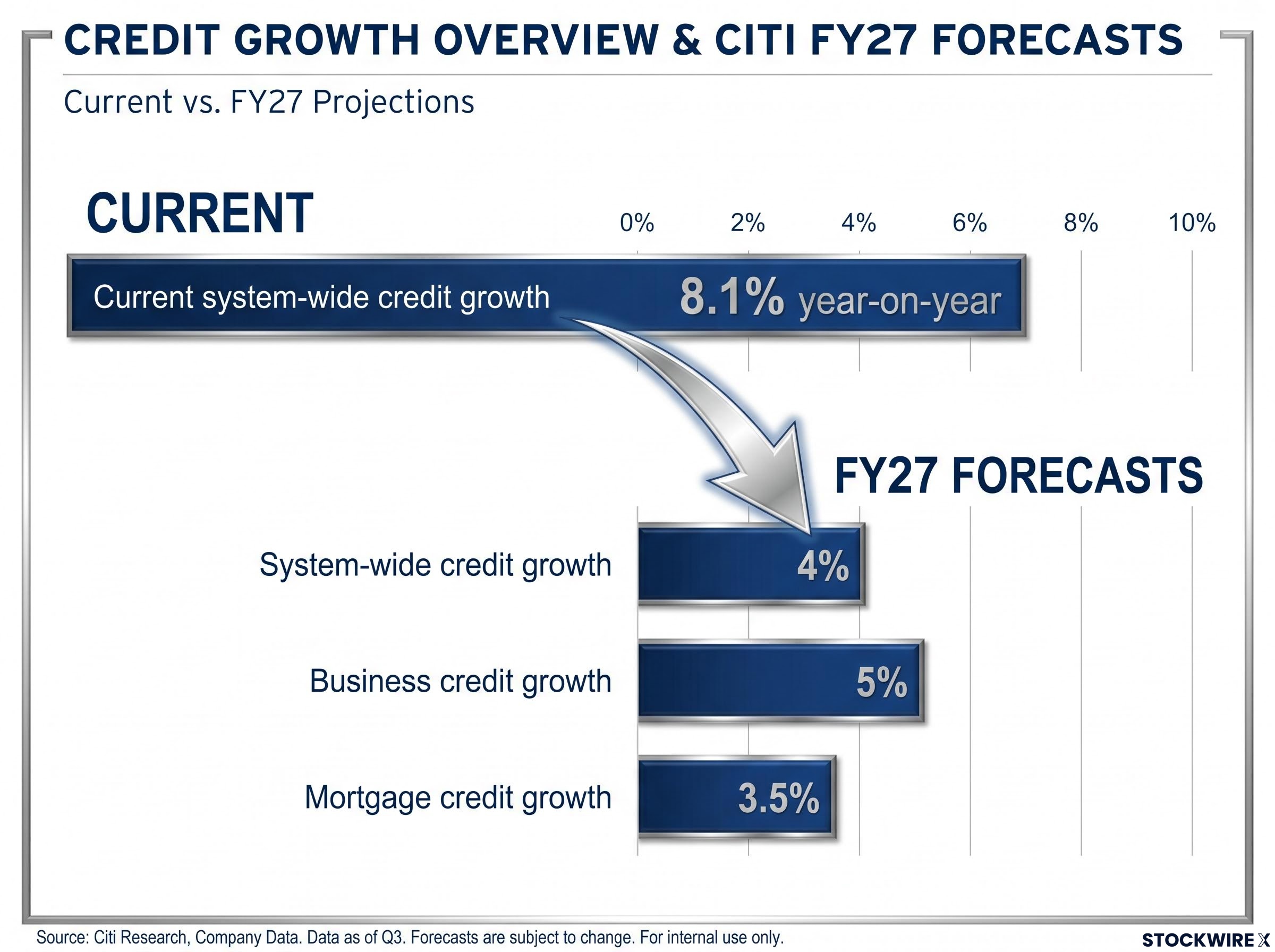

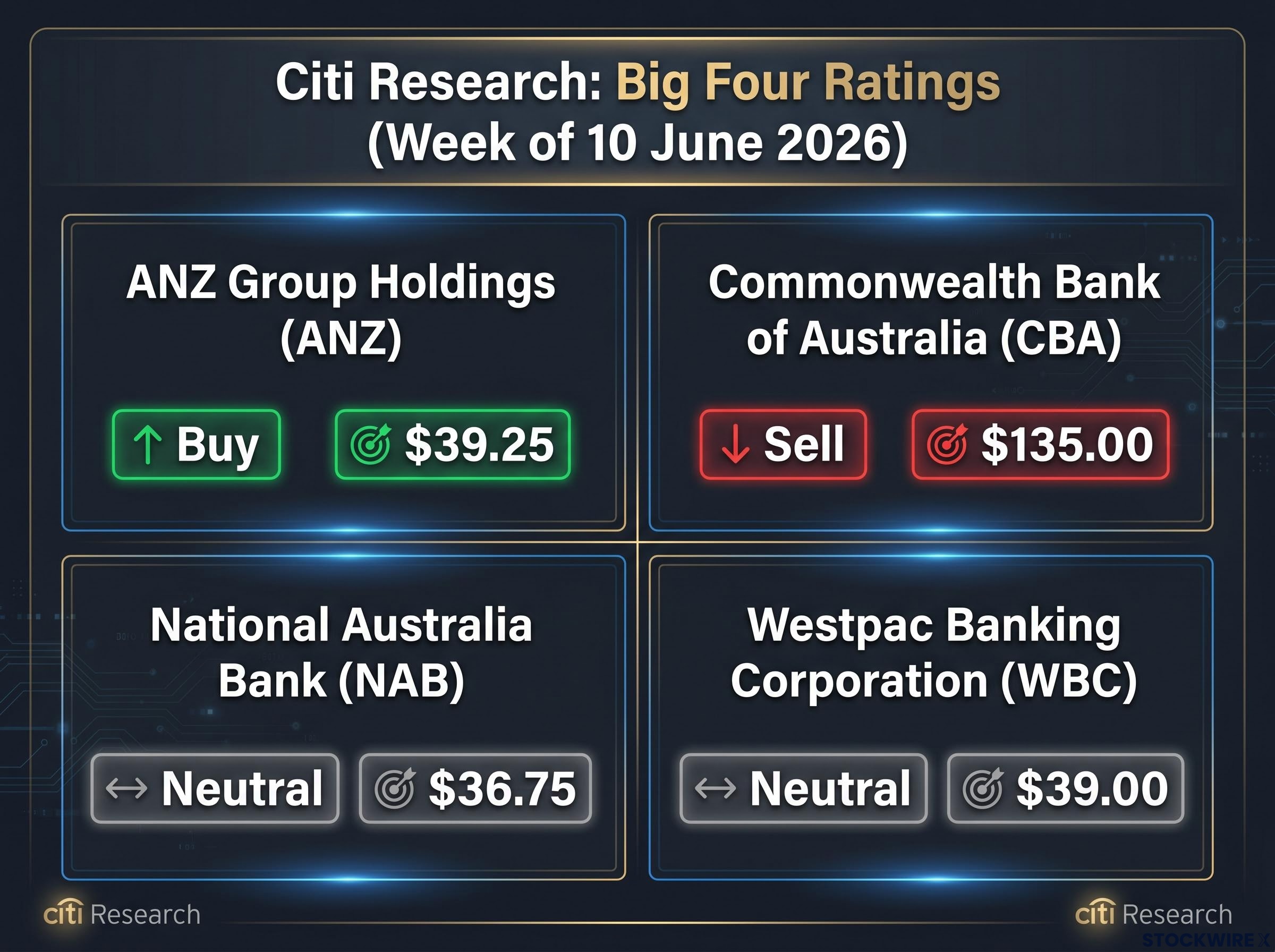

Citi Research has downgraded its outlook on Australia’s banking sector and issued a split verdict across the big four: a Buy on ANZ Group Holdings and a Sell on Commonwealth Bank of Australia, with National Australia Bank and Westpac Banking Corporation sitting in between at Neutral. The divergence captures the tension now running through the Australian bank outlook, where a single deteriorating macro backdrop is producing materially different risk profiles depending on where each stock’s valuation starts. The catalyst is a research note published the week of 10 June 2026, driven by two converging forces: announced changes to the 50% capital gains tax (CGT) discount for property investors, effective 1 July 2027, and a revised system-wide credit growth forecast cut to 4% by FY27. Total private sector credit is still running at 8.1% year-on-year, which makes the gap between where credit growth is today and where Citi expects it to land unusually wide. What follows unpacks the mechanics behind the downgrade, walks through what two prior regulatory tightening cycles suggest about the likely trajectory, and explains what the revised price targets mean for investors weighing their bank exposure.

The first trigger is the announced adjustment to the 50% CGT discount for residential property investors. The change, effective 1 July 2027, directly reduces the after-tax return on investment property sales and is expected to dampen investor housing demand at the margin. That demand has been a meaningful driver of mortgage book growth across the major banks, which means any pullback feeds straight into credit volumes.

The CGT reform mechanics extend well beyond the property investor mortgage channel: a business founder selling a $1 million company could lose more than $225,000 in after-tax proceeds under the new regime, and a lock-in effect that discourages asset sales could undermine the broader capital reallocation the Government intends.

The second trigger compounds the first. Regulators have tightened macroprudential settings on high debt-to-income (DTI) loans, removing additional capacity from the investor lending pipeline beyond what the CGT change alone would produce. Together, the two measures arrive at a moment when the cash rate sits at 4.35% following successive 25 basis point increases through May 2026, squeezing borrower serviceability from the interest-rate side simultaneously.

APRA’s DTI lending limits for residential mortgages, activated effective 1 February 2026, cap new investment and owner-occupied loans at 20% of total new lending where the borrower’s debt exceeds six times income, directly constraining the high-DTI segment of the investor pipeline that the CGT changes are also targeting.

Citi Research, week of 10 June 2026: The broader environment for Australian banks represents an “unfavourable stagflation backdrop,” where slower economic growth reduces credit demand while elevated rates maintain pressure on borrower serviceability.

In practical terms, that phrase means banks face the worst of both sides: weaker demand for new lending and rising risk on the loans already on the books. Citi’s revised forecasts quantify the expected impact:

Against current system credit running at an annualised 7.7% in the three months to February 2026, the deceleration implied by those forecasts is large enough to matter for earnings across all four major banks.

Australia has been through this before. Two prior episodes of regulatory intervention aimed at cooling investor housing activity offer a useful anchor for sizing the credit impact, though with a critical qualification.

When the Australian Prudential Regulation Authority (APRA) imposed restrictions on investor lending in the mid-2010s, investor credit growth fell sharply, from approximately 11% to roughly 2% over 15 months. Investor lending commitments declined by an estimated 30-40% during the period.

The total housing credit damage, however, was contained to roughly 1%. Owner-occupier borrowing accelerated from approximately 5% to roughly 9%, absorbing much of the gap left by retreating investors.

The second episode played out during the Royal Commission into financial services. Tighter serviceability standards drove investor credit from around 4% down to approximately 0% over 18 months. Investor lending commitments again fell an estimated 30-40%, but the offsetting dynamics were less pronounced.

| Episode | Investor credit movement | Owner-occupier response | Duration |

|---|---|---|---|

| Mid-2010s APRA tightening | ~11% to ~2% | ~5% to ~9% (strong offset) | ~15 months |

| Royal Commission period | ~4% to ~0% | Limited offset | ~18 months |

The mid-2010s offset required a specific enabling condition: falling interest rates. Lower rates expanded owner-occupier borrowing capacity, giving that segment room to grow into the space vacated by investors.

That condition is absent today. With the cash rate at 4.35%, borrower serviceability is already stretched. The historical pattern where owner-occupier demand cushioned total housing credit may not repeat in the current cycle, which means investors should treat the precedent as instructive rather than predictive.

For investors who have not previously tracked how mortgage book composition affects bank profitability, the transmission chain from slower credit to lower share prices runs through four sequential links:

Investor loans grew 9.2% over the 12 months to February 2026, compared to 6.1% for owner-occupier loans (indicative figures). That gap illustrates why a CGT-driven pullback in investor demand hits a disproportionately active part of the mortgage book.

The owner-occupier offset, where first-home buyers and upgraders fill the gap left by retreating investors, remains a possibility but not a base-case guarantee. High rates and tight serviceability make the required acceleration in owner-occupier borrowing uncertain.

With mortgage credit growth projected at 3.5% by FY27 under Citi’s updated model, the earnings implications are material across the sector. The question is which banks carry more or less risk given their starting valuations, a question the price targets address directly.

The bank earnings transmission channel from the CGT and negative gearing reforms runs through mortgage book concentration and starting valuation multiples, a combination that explains why CBA fell approximately 10% on 13 May 2026 while the other three major banks absorbed the same sector headwind from lower starting multiples.

Citi’s updated ratings and price targets, published the week of 10 June 2026, produce a clear hierarchy within the big four:

| Bank | ASX code | Citi rating | Price target |

|---|---|---|---|

| ANZ Group Holdings | ANZ | Buy | $39.25 |

| Commonwealth Bank of Australia | CBA | Sell | $135.00 |

| National Australia Bank | NAB | Neutral | $36.75 |

| Westpac Banking Corporation | WBC | Neutral | $39.00 |

Citi’s preferred holding: ANZ is rated Buy among the four major banks, reflecting a valuation starting point that Citi views as offering the most relative protection in a decelerating credit environment.

The logic behind the bookends is valuation-driven. ANZ’s lower starting multiple means less compression risk if earnings come under pressure. Modest delivery on earnings can still support total returns, because the stock is not priced for strong growth. The margin of safety is wider.

CBA sits at the opposite end. Its premium multiple, built on years of superior returns and franchise strength, creates a double-risk scenario in a slowdown: earnings revisions push the numerator lower while the market simultaneously questions whether the elevated multiple is justified, pushing the denominator lower too.

CBA’s deteriorating credit quality was already visible before Citi’s June downgrade: the bank added $200 million to collective provisions in Q3 2026 and reported rising arrears across every major consumer lending category, including a 30 basis point spike in personal loan arrears in a single quarter.

When earnings are being revised down, the multiple a stock trades on determines whether the share price impact is absorbed or amplified. A stock on 15x earnings that misses expectations by 5% has a different magnitude of price risk than a stock on 25x earnings facing the same miss. CBA’s premium multiple means every percentage point of earnings disappointment translates into a larger share price adjustment than the same miss would produce for ANZ.

NAB and Westpac, both rated Neutral, sit in the middle ground. Neither carries CBA’s premium valuation risk nor offers ANZ’s relative discount. For investors, the two Neutral-rated banks represent a position where the risk-reward is more balanced, but neither stock stands out as a clear opportunity or a clear risk within Citi’s framework.

Citi’s forecast is a base case, not a certainty. Three variables will determine whether the scenario is better, worse, or broadly in line with the downgraded outlook:

Monthly RBA credit aggregates are the primary tracking data point. These releases will show in near-real time whether the deceleration Citi anticipates is materialising or whether credit growth is proving stickier than forecast.

Legislative progress on the CGT changes will be visible through parliamentary sitting schedules and budget update materials. Any modifications to the announced design, in either direction, would shift the base-case assumptions.

Perhaps most consequentially, any shift in RBA cash rate guidance would directly affect the owner-occupier offset probability. A rate-cutting cycle would expand borrowing capacity for owner-occupiers and improve the odds of the mid-2010s offset pattern repeating. Sustained elevated rates would remove that possibility.

The same macro headwinds, CGT changes, macroprudential tightening, elevated rates, and a softening economic outlook, affect all four major banks. The stock-level implications, however, vary materially based on valuation starting point.

CBA at a Sell with a $135.00 price target carries the most asymmetric downside, because its premium multiple amplifies earnings risk in both directions. ANZ at a Buy with a $39.25 target carries the most relative protection, because its lower multiple requires less to go right for the investment case to hold. The gap between those two positions is where the actionable insight sits.

Citi’s system credit forecast of 4% by FY27 is the base-case anchor, not a certainty. The three swing factors identified, CGT policy design, the pace of credit deceleration, and the strength of any owner-occupier offset, each have genuine potential to shift the outcome in either direction. The 1 July 2027 CGT effective date gives investors a visible policy milestone against which to calibrate.

For investors holding undifferentiated exposure across the big four, the implication is worth stating directly: the four banks are not a single trade. Sector-level analysis provides the context, but the premium-versus-discount question within the sector is where the positioning work needs to happen.

For investors who want to apply the premium-versus-discount framework to their own holdings, our dedicated guide to stress-testing ASX bank valuations walks through dividend discount model inputs, CET1 capital ratios, and 90-day arrears thresholds with a structured qualitative checklist designed specifically for the major ASX banks.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Citi Research describes the Australian bank outlook as an unfavourable stagflation backdrop, where slower economic growth reduces credit demand while elevated interest rates maintain pressure on borrower serviceability, prompting a sector-wide downgrade and revised credit growth forecasts of 4% by FY27.

The split rating is driven by valuation starting points: ANZ's lower price-to-earnings multiple offers more protection if earnings disappoint, while CBA's premium multiple creates a double-risk scenario where both the earnings estimate and the multiple itself can compress simultaneously in a credit slowdown.

The reduction in the 50% capital gains tax discount for property investors, effective 1 July 2027, is expected to dampen investor housing demand, which has been a key driver of mortgage book growth across the major banks, feeding directly into slower credit volumes and lower net interest income.

Citi's updated price targets as of the week of 10 June 2026 are: ANZ at $39.25 (Buy), CBA at $135.00 (Sell), NAB at $36.75 (Neutral), and Westpac at $39.00 (Neutral).

Two prior episodes are relevant: the mid-2010s APRA tightening, which saw investor credit fall from roughly 11% to 2% over 15 months before being partially offset by owner-occupier lending, and the Royal Commission period, where investor credit fell from around 4% to near 0% over 18 months with a more limited offset from owner-occupier borrowers.