Credit Corp’s share price has spent four months in a hole of its own market’s making. Management has twice pointed to record earnings ahead, and the stock has stayed roughly 18% below where it traded before the first-half FY26 result landed on 3 February 2026. That result delivered a 10% net profit miss against consensus despite a 2% revenue beat, triggering a 16.7% single-day fall. A May trading update reaffirming guidance and upgrading the lending outlook produced a 7.9% bounce that still failed to close the gap. The persistent discount is not a technical anomaly. It reflects a specific market argument about execution risk, credit quality, and the credibility of a very large second-half earnings step-up. What follows is a dissection of that disconnect: what the numbers actually showed, why management’s reaffirmation deepened rather than resolved investor anxiety, what brokers are saying versus what the market is pricing, and what specific evidence would need to emerge for the stock to rerate.

What the first-half result actually showed

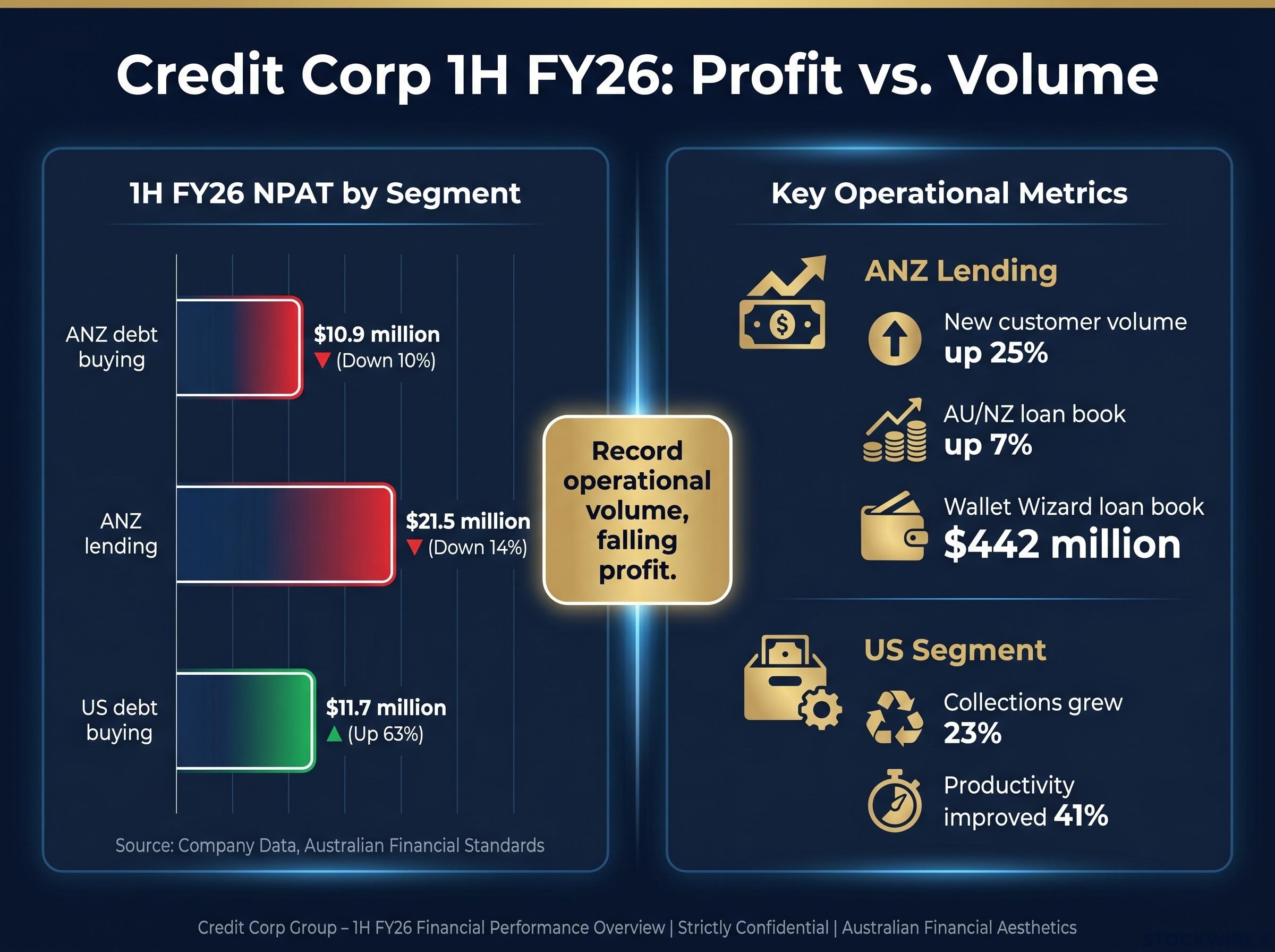

The headline numbers pulled in opposite directions. Revenue of $283.6 million beat analyst estimates of $277.5 million by 2%, yet net profit after tax of $44.1 million fell roughly 10% short of the consensus expectation of approximately $48.9 million. The interim dividend was held flat at 32 cents per share, a decision that carried its own signal alongside management’s confident language about full-year guidance.

The divergence sharpened at the segmental level.

| Segment | 1H FY26 NPAT | Change on pcp |

|---|---|---|

| ANZ debt buying | $10.9 million | Down 10% |

| ANZ lending | $21.5 million | Down 14% |

| US debt buying | $11.7 million | Up 63% |

The US segment delivered genuine improvement: collections grew 23%, and productivity improved 41% year-on-year. Both ANZ segments disappointed on profit, even as lending volumes told a different story entirely:

- New customer volume growth of 25% year-on-year

- AU/NZ loan book up 7%

- Wallet Wizard loan book reaching $442 million

Record operational volume, falling profit. That combination, more than any single headline number, is the tension sitting beneath the share price.

When big ASX news breaks, our subscribers know first

The arithmetic problem management created by reaffirming guidance

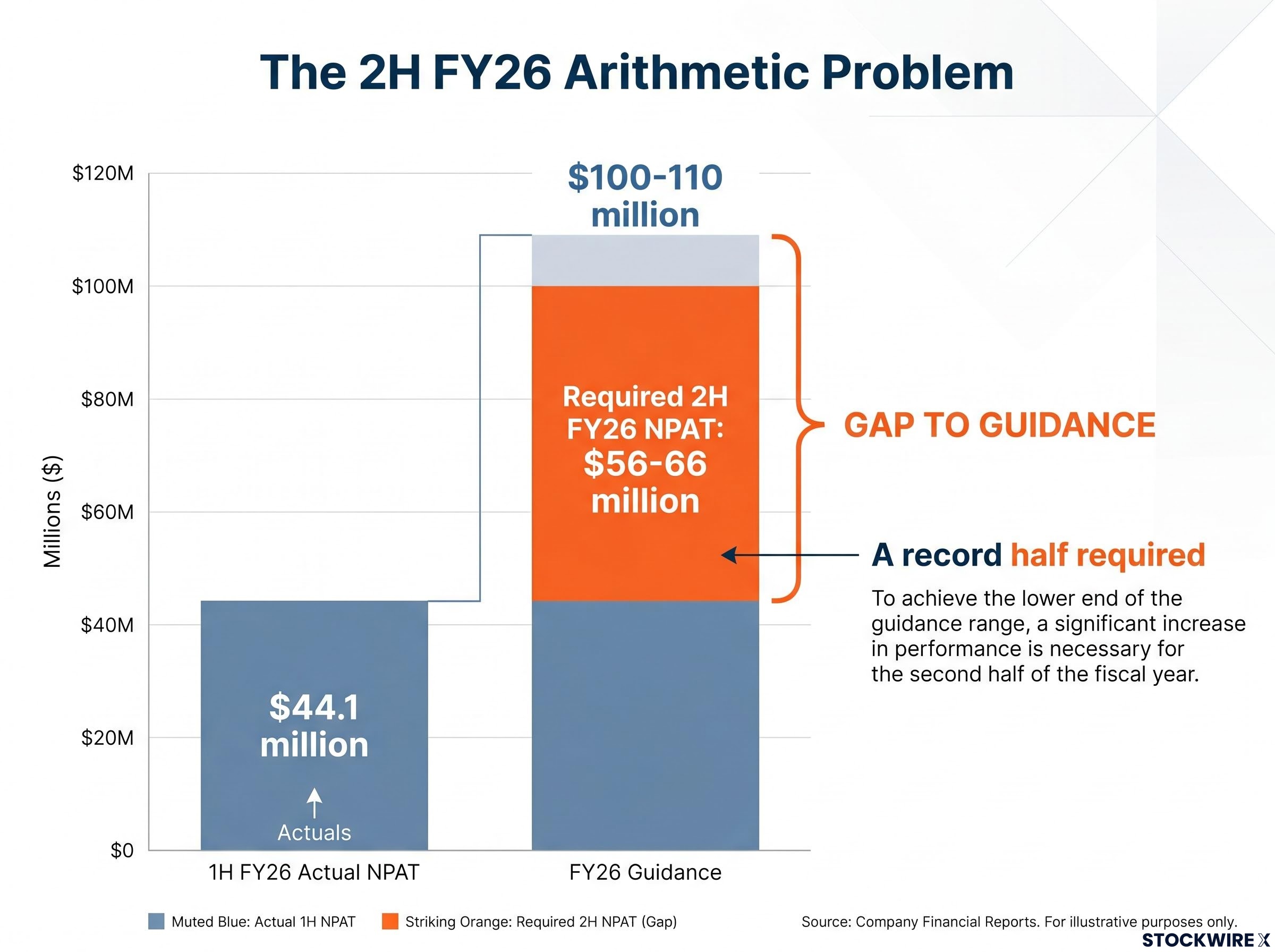

Credit Corp reaffirmed full-year FY26 NPAT guidance of $100-110 million, characterising the outcome as a record. With first-half NPAT of $44.1 million, the arithmetic is unavoidable.

The second half must deliver roughly $56-66 million in NPAT to meet even the bottom of guidance, a record half by a meaningful margin.

In a different context, reaffirmed guidance might have steadied sentiment. Here, it amplified anxiety, because it raised the bar without providing additional evidence the bar could be cleared. Four structural factors explain why the market remained unconvinced:

- The arithmetic itself: A required second-half NPAT of approximately $56-66 million would represent a record performance. In cyclical, capital-intensive businesses like debt purchasing and non-prime lending, markets apply heavy discounts to back-end-loaded earnings profiles.

- Execution risk already materialised: ANZ forward-flow purchasing disruptions and a US forward-flow contract loss both occurred during the first half, demonstrating that the variables management cannot fully control had already moved against the company.

- Volume growth without profit follow-through: ANZ lending volumes hit records, yet segmental NPAT fell 14%. That sequence raises questions about credit quality, provisioning adequacy, and whether front-loaded costs will produce clean earnings leverage or higher arrears and write-offs.

- A flat dividend that contradicts confident guidance: Holding the interim payout steady at 32 cents while projecting record full-year earnings creates an internal tension. If management truly expected a record second half, the dividend would be an obvious place to signal that conviction.

The question for investors shifted from “did Credit Corp have a bad half?” to “can Credit Corp have a record half in a historically difficult environment?”

Credit Corp’s capital allocation story carries an additional layer of complexity that the first-half result does not fully capture: the Humm acquisition proposal, which has advanced to due diligence despite Humm’s Independent Board Committee formally labelling the $0.77 per share offer ‘not compelling,’ adds meaningful execution and balance sheet uncertainty to a business already navigating a demanding second-half earnings task.

How the debt-purchasing model creates earnings volatility (and why it matters here)

How the PDL model generates earnings

Credit Corp’s debt-purchasing business operates by acquiring portfolios of charged-off consumer debt at a discount to face value, then collecting on those debts over time. Returns depend on three variables: the purchase price paid, the collection rate achieved, and the volume of portfolios available to buy. The internal rate of return on each portfolio is locked in at acquisition, meaning pricing discipline at the point of purchase is where the economics are won or lost.

Forward-flow contracts sit at the centre of this model. These are ongoing agreements with creditors (typically banks and other financial institutions) to purchase debt as it is charged off, providing a predictable supply of portfolios for the buyer. They are competitively priced against other debt buyers, and retention depends on offering creditors a combination of competitive pricing and compliance quality.

ASIC’s debt collection regulatory guide sets out the compliance standards that apply to creditors and third-party collectors operating in the Australian market, meaning forward-flow contract pricing decisions made by Credit Corp and its competitors sit within a regulatory environment that constrains how aggressively collection strategies can be pursued to recover margin.

Where the model ran into trouble in HY26

Both regions experienced supply or competition disruptions during the first half. In ANZ, several issuers temporarily suspended debt sales, reducing the volume of portfolios available for purchase. In the US, Credit Corp lost a forward-flow contract to a competitor offering more aggressive pricing.

These disruptions illustrate the structural choice facing any debt buyer when supply is constrained: pay more for available portfolios (compressing returns) or deploy less capital (slowing growth). Either path undermines the record-earnings scenario. The US segment’s 63% NPAT growth despite the contract loss demonstrates that collection efficiency improvements can partially offset supply disruptions, but the question is whether that offset can scale to the level required in the second half.

Brokers say “buy”; the market says “prove it”

Three brokers maintained positive ratings on Credit Corp following the February result, though all adjusted price targets to reflect the new risk profile.

| Broker | Rating | Previous target | Revised target | Key rerating condition |

|---|---|---|---|---|

| Morgans | Buy | $21.50 | $19.35 | US competitive dynamics stabilising |

| E&P | Positive | $26.35 | $22.88 | Share price reaction viewed as excessive |

| JPMorgan | Overweight | $19.60 | $19.60 | US segment execution |

E&P offered the sharpest expression of the divergence, describing the share price reaction as excessive relative to the actual risk profile. JPMorgan kept its target unchanged but conditioned rerating potential on successful US execution. Rask characterised the implied price-to-earnings ratio at guided earnings as high single-digit, a level it described as low if profit grows from the current base.

The broker community, after detailed work and management engagement, broadly accepted the guidance as a credible base case with some risk discounting. The broader market is pricing a probability-weighted scenario where guidance is cut, returns on growth investments prove weaker than assumed, or the credit cycle turns more sharply against non-prime borrowers. Both readings carry analytical weight; the divergence itself is the signal.

The pattern of a stock trading at a deep discount to intrinsic value despite management repeatedly reaffirming guidance is not unique to Credit Corp; CAR Group experienced a structurally similar persistent re-rating gap after its H1 FY26 result, where 16% profit growth and reaffirmed guidance still could not close a 33% share price decline, illustrating how back-half earnings reliance and macro headwinds can keep markets in a ‘show me’ posture even when fundamentals appear supportive.

Four conditions that would close the valuation gap

The stock will not rerate on narrative alone. Four categories of evidence would directly address the market’s stated concerns:

- PDL deployment at acceptable returns: Visible replacement of disrupted forward-flow volumes in ANZ or the US, with disclosed return metrics in line with historical targets. Commentary that portfolio pricing has normalised and competition is rational would speak directly to the market’s core fear.

- Clean delivery of FY26 guidance: Actual FY26 NPAT at or above the guided $100-110 million range, without reliance on one-off gains, directly undermines the “they’ll have to cut” thesis. Hitting the midpoint would require second-half NPAT of approximately $61 million.

- Evidence that lending growth is high-quality: Stable arrears, controlled write-offs, and provisioning that does not require material upward revision despite strong loan growth. This would demonstrate that front-loaded marketing and provisioning are setting up profitable loan books, not merely larger ones.

- More constructive sector and macro signals: Signs that consumer credit stress is not worsening materially and that competition in debt purchasing is stabilising would lower the risk premium applied across both operating segments.

The RBA’s March 2026 Financial Stability Review documented rising mortgage arrears and cash flow pressures among lower-income borrower segments, providing the macroeconomic backdrop against which Credit Corp’s ANZ lending provisioning decisions and arrears trajectory need to be assessed.

An 18% discount to the pre-result price and a single-digit P/E on record earnings guidance represent the market saying: “show me, don’t tell me.”

Until at least some of these boxes are ticked, that posture is unlikely to shift.

The case for the market and the case for the stock

The case for the stock

- US NPAT grew 63%, with collections up 23% and productivity up 41% year-on-year

- ANZ new customer volumes rose 25%, indicating demand for the lending product

- Revenue beat consensus by 2%, demonstrating top-line execution

- Management had sufficient visibility to reaffirm full-year guidance after a volatile half, then reaffirmed again in May with an upgraded lending outlook

- E&P characterised the market reaction as disproportionate to the actual risk

- The implied P/E at guided earnings sits in the high single digits

The case for the market’s caution

- NPAT missed consensus by approximately 10% despite strong top-line and volume growth

- Forward-flow disruptions materialised in both regions during the first half: ANZ issuer suspensions and a US contract loss

- The earnings trajectory relies on a record second half in businesses exposed to the credit cycle and competitor behaviour

- Rapid volume growth combined with falling segmental NPAT in ANZ lending raises genuine questions about credit quality and future provisioning requirements

- A flat dividend sits uneasily alongside a record-earnings narrative

The 7.9% single-day gain on the May trading update demonstrated that the market will reward positive news. It has simply not yet been given enough to rerate fully. Whether the current discount is excessive depends on an investor’s assessment of the base rate at which a debt-purchasing and non-prime lender can deliver record guidance after a first-half miss, and their confidence in Credit Corp’s specific management and underwriting track record.

The verdict the market is waiting to write

The 18% discount is not irrational noise. It is a legible and specific market argument about execution risk, back-half arithmetic, and credit quality in a cyclical business. The upcoming full-year result is the moment that argument either collapses or proves prescient: either management delivers record earnings and the “show me” posture becomes untenable, or guidance disappoints and the current pricing looks measured rather than punitive.

The question for investors is not whether Credit Corp is a good business. Its US turnaround, lending scale, and collections infrastructure all point to genuine operational capability. The question is whether the current share price already compensates for the specific risks the market has identified, or whether it is pricing in a scenario that management’s track record suggests may not arrive.

For investors working through their own assessment of whether the current discount compensates for the identified risks, our comprehensive walkthrough of ASX stock evaluation covers the full framework used by professional fund managers, including how to distinguish a genuine earnings downgrade cycle from a temporary miss, how to assess management credibility against disclosed guidance, and how to apply valuation discipline when markets and brokers disagree.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.