AI Stocks Split in Two as CoreWeave Falls 14% and Meta Surges 9%

1 hr ago

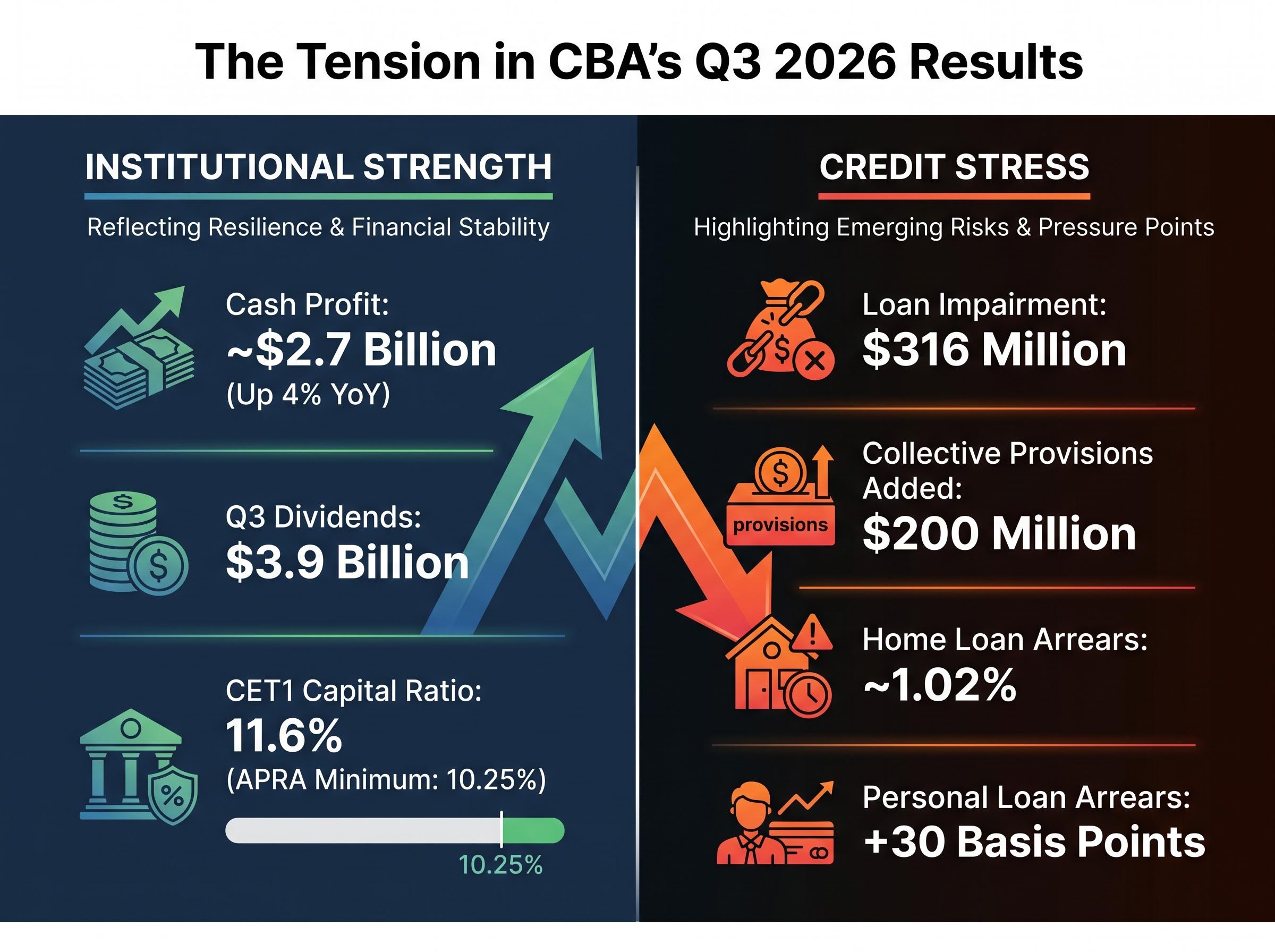

Commonwealth Bank of Australia reported headline cash profit of approximately $2.7 billion for Q3 2026, a figure that looked steady enough on the surface. The market read something else entirely. CBA shares fell approximately 5.7% on 13 May 2026, dropping from $172.90 to $163.00 in a single session, and the selling pointed squarely at one thing: the credit quality numbers beneath the headline. Rising arrears across home loans, credit cards, and personal loans; a $200 million top-up to collective provisions; and an explicit shift toward downside economic scenario weighting are not the language of a bank that sees smooth conditions ahead. This analysis unpacks what CBA’s Q3 2026 credit data reveals about Australian borrowers, how it aligns with the Reserve Bank of Australia’s (RBA) own forecasts, what the bank’s balance sheet strength can and cannot offset, and what the picture means for households and investors right now.

The loan impairment expense tells the first part of the story. CBA recorded $316 million in loan impairments for the quarter, a figure Macquarie analysts described as approximately 4% above consensus expectations. The miss was not dramatic in isolation, but it arrived alongside deterioration across every major consumer lending category, and it is the breadth of that deterioration that warrants attention.

Loan impairment expense: $316 million for Q3 2026, approximately 4% above analyst consensus (Macquarie).

The arrears movements across CBA’s lending book during Q3 2026:

Personal loan arrears deserve particular scrutiny. A 30 basis point rise in a single quarter signals borrowers under acute short-term cash flow pressure, the kind of stress that tends to show up in unsecured lending before it migrates into mortgage books. CBA management cited seasonality as a partial factor but also pointed to elevated energy prices, interest rates, and supply chain disruptions as structural headwinds. The combination of those acknowledgements, spread across multiple loan types, builds a picture of broad-based borrower stress rather than isolated pockets of weakness.

The personal loan arrears spike sits within a broader pattern of household deterioration that aggregate GDP figures obscure: Australia has been in a per capita recession for the better part of 2025, with real wages falling roughly 0.3% even as nominal Wage Price Index growth of 3.4% appeared healthy, and corporate insolvencies reaching their highest level since the 1990-91 recession.

The $200 million increase in collective provisions during Q3 2026 is, in many respects, the most telling number in the entire quarterly disclosure. It requires a different kind of reading than the arrears data because it is not a record of what has already gone wrong. It is a statement about what CBA’s risk team expects to go wrong next.

Collective provisions are funds a bank sets aside based on forward-looking economic models. They are not triggered by specific loans that have already defaulted. Instead, they reflect management’s assessment of the probability and severity of future credit deterioration across the entire lending portfolio. When a bank increases collective provisions, it is telling shareholders and regulators that its internal models now assign higher probability to adverse outcomes.

Collective provisions reflect anticipated future conditions, not past losses. A $200 million single-quarter increase is a real-time signal of institutional economic sentiment.

CBA’s management stated that the increase was driven by revised macroeconomic forecasts and greater weighting assigned to downside economic scenarios. This language matters. It means the bank’s economists have adjusted their base-case assumptions, and the adjustment was large enough to require a material provisioning response. Actual credit losses during the quarter remained low, and provision coverage was described as adequate, which sharpens the point further: CBA is not responding to a crisis that has already arrived. It is preparing for conditions it believes are coming.

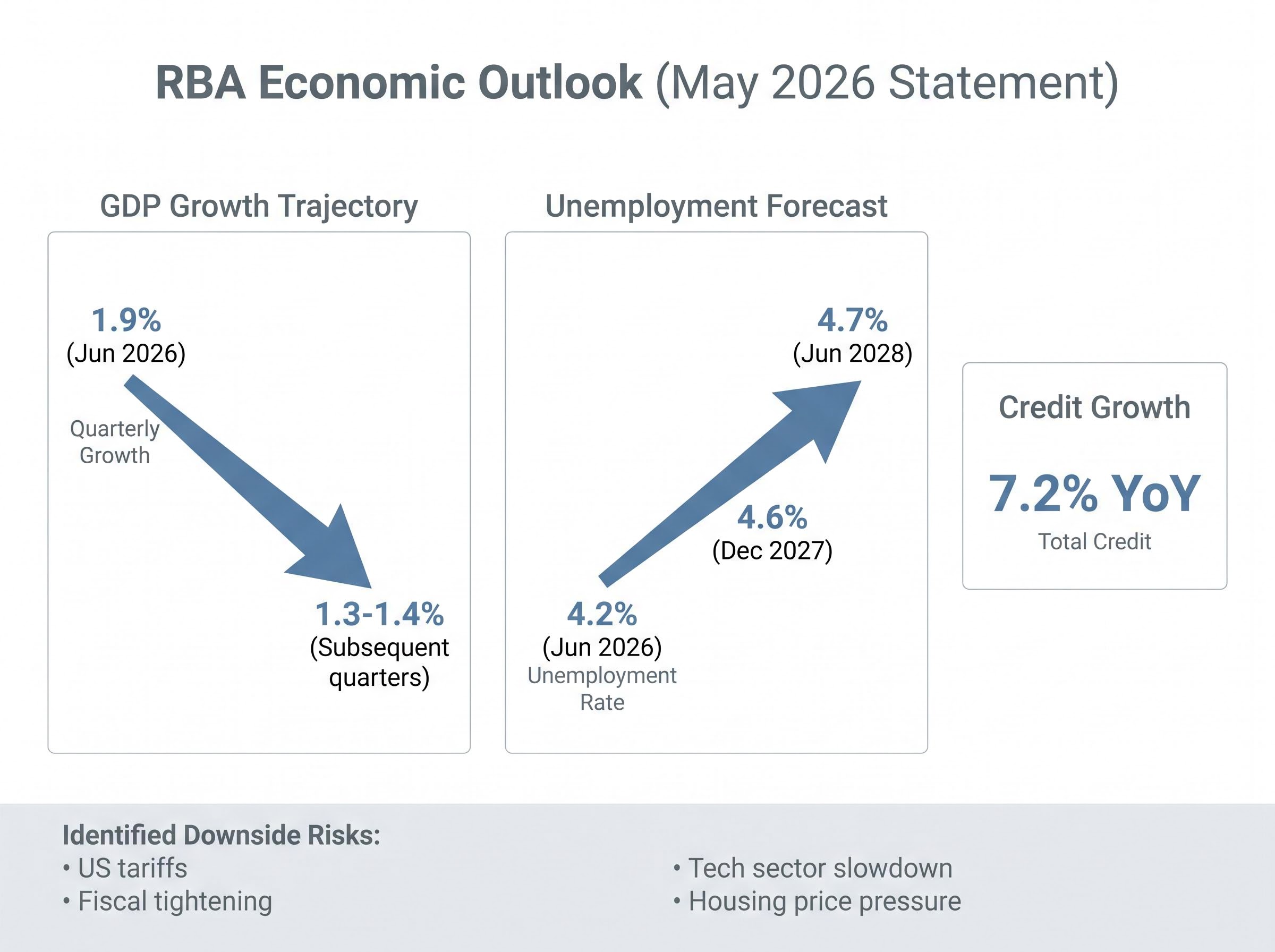

The RBA’s May 2026 Statement on Monetary Policy flagged US tariffs, fiscal tightening, a tech sector slowdown, and housing price pressure as downside risks to the Australian economy. CBA’s provisioning decision aligns directly with that risk catalogue.

CBA’s defensive positioning does not exist in isolation. The central bank’s own published outlook paints a strikingly similar picture, and the convergence between the two makes the combined signal harder to set aside.

The RBA’s May 2026 Statement on Monetary Policy, published 7 May 2026, projects GDP growth of 1.9% for the June 2026 quarter, declining to 1.3-1.4% in subsequent quarters. Unemployment, currently at 4.2%, is forecast to rise to 4.6% by December 2027 and 4.7% by June 2028. Credit growth is running at 7.2% year-on-year, meaning Australians continue to take on debt even as the economic outlook softens.

The RBA’s May 2026 Statement on Monetary Policy projects GDP growth slowing from 1.9% in the June 2026 quarter to 1.3-1.4% in subsequent quarters, with unemployment rising from 4.2% to 4.6% by December 2027, a trajectory that maps directly onto the household income and loan serviceability pressures showing up in CBA’s arrears data.

| Indicator | Current reading | RBA forecast (near term) | RBA forecast (medium term) | Relevance to CBA provisioning |

|---|---|---|---|---|

| GDP growth | 1.9% (Jun 2026 qtr) | 1.3-1.4% (subsequent qtrs) | Slowing trajectory | Weaker growth pressures household income and loan serviceability |

| Unemployment | 4.2% (Jun 2026) | 4.6% (Dec 2027) | 4.7% (Jun 2028) | Rising joblessness is the primary driver of mortgage default risk |

| Credit growth | 7.2% YoY | Elevated | No material slowdown flagged | Growing debt stock meets a deteriorating income environment |

The unemployment trajectory is the single most important variable connecting the RBA’s outlook to CBA’s provisioning decision. Rising unemployment reduces household income, which directly affects loan serviceability across mortgages, credit cards, and personal loans. The RBA has confirmed that household arrears are rising across major banks due to persistent cost-of-living pressures, while noting they remain below Global Financial Crisis (GFC) peaks. Directionally, peer banks including NAB, ANZ, and Westpac appear to be recording similar trends, though specific peer figures have not been independently verified.

The alignment between CBA’s internal risk modelling and the RBA’s published forecasts tells a consistent story: what looks like one bank’s caution is the Australian financial system’s collective reading of where household credit stress is heading.

The RBA rate hike to 4.35% on 5 May 2026 made Australia’s central bank the most aggressive in the developed world, with the Fed, ECB, and Bank of England all holding steady in the same week, a divergence that amplifies the debt serviceability pressure CBA’s arrears data captures.

Before treating the credit data as an unqualified warning, the balance sheet deserves its full weight. CBA’s capital and liquidity position is genuinely strong, and the strength is material to assessing how much risk the bank can absorb.

The headline metrics:

CBA distributed $3.9 billion in dividends during Q3 2026, reaching more than 800,000 direct shareholders and over 14 million Australians through superannuation holdings. The 11.6% CET1 ratio exceeds APRA’s minimum by 135 basis points, providing a buffer against unexpected losses that would need to be substantial before threatening institutional stability or dividend capacity.

The distinction matters. APRA-compliant capital buffers are designed to absorb institutional losses, ensuring the bank can continue operating and paying dividends even if credit conditions worsen materially. They do not ease the household debt serviceability pressures that are driving arrears higher in the first place.

For readers holding CBA shares through superannuation, this creates a dual signal. The dividend is supported by the balance sheet. The arrears trajectory, however, is a separate signal about the economic environment that their other assets, including property and employment income, are exposed to. Conflating institutional resilience with borrower relief would be a misreading of what the numbers say.

For investors wanting to model what CBA’s arrears trajectory and provisioning increase mean for their own portfolio positioning, our dedicated guide to ASX bank stock valuation walks through five qualitative dimensions, including RBA rates, employment, and property, that drive the $19.00 to $85.50 per share valuation range a single NAB model can produce under different macroeconomic assumptions.

The institutional framing is useful, but the arrears percentages represent something more immediate than bank accounting. They represent households choosing between mortgage repayments, energy bills, and basic expenditure.

CBA management identified three structural pressure factors weighing on Australian households and businesses:

These are not transient shocks. The RBA’s May 2026 Statement on Monetary Policy characterises the cost-of-living pressures as persistent, and the unemployment forecast, rising from 4.2% to 4.6-4.7% through 2027 and 2028, suggests the pressure will intensify before it eases.

The RBA has confirmed that household arrears are rising across major banks due to persistent cost-of-living pressures, while remaining below GFC peaks.

The provisioning increase is a bank-level confirmation of that trajectory. CBA’s own economists have modelled the forward path and concluded that $200 million in additional buffer is warranted. For Australian households with mortgages, credit cards, or personal loans, CBA’s Q3 data is the most current large-scale reading of where real financial stress sits in the economy. The combination of rising arrears, increased provisions, and a rising unemployment forecast paints a picture of sustained rather than temporary pressure.

The Q3 2026 result, taken as a whole, is best understood not as a scorecard of recent performance but as a forward-looking act of institutional positioning. The provisioning increase, the downside scenario weighting, and the arrears trajectory are collectively a forecast embedded in a balance sheet.

The $200 million provisioning increase is a forecast embedded in a balance sheet, not merely a historical record.

The share price reaction reinforces this reading. The approximately 5.7% decline on 13 May 2026 reflects investors pricing in a less favourable credit environment ahead, not simply reacting to one quarter’s figures. Broader market weakness and Federal Budget discussions were also in play on that date, meaning the full decline cannot be attributed solely to the credit disclosure, but the direction of the market’s verdict was clear.

Morgans issued sell ratings on all four major ASX banks simultaneously ahead of the May 2026 reporting season, with CBA facing the steepest implied downside at approximately 29% to Morgans’ price target of $124.26, a call grounded in a provisioning forecast that sees total Big Four provisions rising from roughly $2.4 billion in FY25 to approximately $5.5 billion by FY27.

Three forward signals from Q3 2026 that warrant monitoring:

Profit still grew 4% year-on-year (Q3 2026 versus Q3 2025), and cash NPAT came in at approximately $2.7 billion. CBA remains a profitable institution with a strong balance sheet. The tension between that strength and the credit deterioration is the defining feature of this result, and it is a tension that the next several quarters will resolve.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

CBA’s Q3 2026 credit disclosure is most usefully read as an institutional forward signal rather than a verdict on recent performance. The balance sheet strength and the credit stress signals are both real, and they must be held together rather than used to cancel each other out. The bank is not in distress; it is preparing for conditions that its own risk team, and the RBA, believe are coming.

The variables that will confirm or complicate this picture in coming quarters are the unemployment trajectory, RBA rate decisions, and whether arrears continue to rise or plateau. CBA’s next quarterly update and the RBA’s August 2026 Statement on Monetary Policy are the two most important data points for resolving the tension this result leaves open.

Collective provisions are funds a bank sets aside based on forward-looking economic models to cover anticipated future credit losses, not past defaults. CBA added $200 million to its collective provisions in Q3 2026 because its internal risk models assigned greater probability to adverse economic outcomes, driven by revised macroeconomic forecasts aligned with RBA projections.

CBA's Q3 2026 results showed rising arrears across home loans, credit cards, and personal loans, with personal loan arrears jumping 30 basis points in a single quarter, indicating broad-based household financial stress rather than isolated pockets of weakness.

CBA shares dropped approximately 5.7% from $172.90 to $163.00 on 13 May 2026, as investors reacted to deteriorating credit quality data beneath the headline $2.7 billion cash profit, including rising arrears across all major lending categories and a $200 million increase in collective provisions.

CBA's CET1 capital ratio of 11.6% exceeds APRA's minimum requirement of 10.25% by 135 basis points, providing a substantial buffer against unexpected losses and supporting its capacity to continue paying dividends even if credit conditions deteriorate materially.

The RBA's May 2026 Statement on Monetary Policy projects unemployment rising from 4.2% to 4.6-4.7% through 2027-2028 and GDP growth slowing to 1.3-1.4%, conditions that directly reduce household income and loan serviceability, which is precisely the stress pattern visible in CBA's rising arrears data.