Citi Splits on Big Four: Buy ANZ, Sell CBA in Sector Downgrade

3 hrs ago

Roughly 50 publicly disclosed filing applications for U.S. listings in approximately two years, 56 approvals in 2024 alone, and clearances spanning logistics, clean energy, and enterprise software: the China Securities Regulatory Commission’s overseas listing regime has not closed the door to American capital markets. It has replaced an informal, largely offshore process with a structured, dual-jurisdiction exercise that screens issuers on both sides of the Pacific. Since the Trial Administrative Measures took effect on 31 March 2023, the question facing finance professionals has shifted. It is no longer whether Chinese companies can list in the United States; it is which companies clear both the CSRC’s filing review and the increasingly selective standards imposed by U.S. exchanges. This analysis uses filing and approval data through 22 May 2026, three profiled approved transactions, and Nasdaq’s recent rule changes to provide a grounded assessment of how open, or constrained, this pathway remains in mid-2026.

The Trial Administrative Measures, released in February 2023 and effective 31 March 2023, installed the CSRC as a parallel gatekeeper for every overseas offering by a “domestic company,” whether listed directly from the PRC or indirectly through an offshore holding structure. For deal teams accustomed to treating Chinese regulatory compliance as a background checklist item, the shift is structural: the CSRC now operates on a defined timeline with real rejection authority, and its review runs simultaneously with the SEC or exchange process rather than sequentially after it.

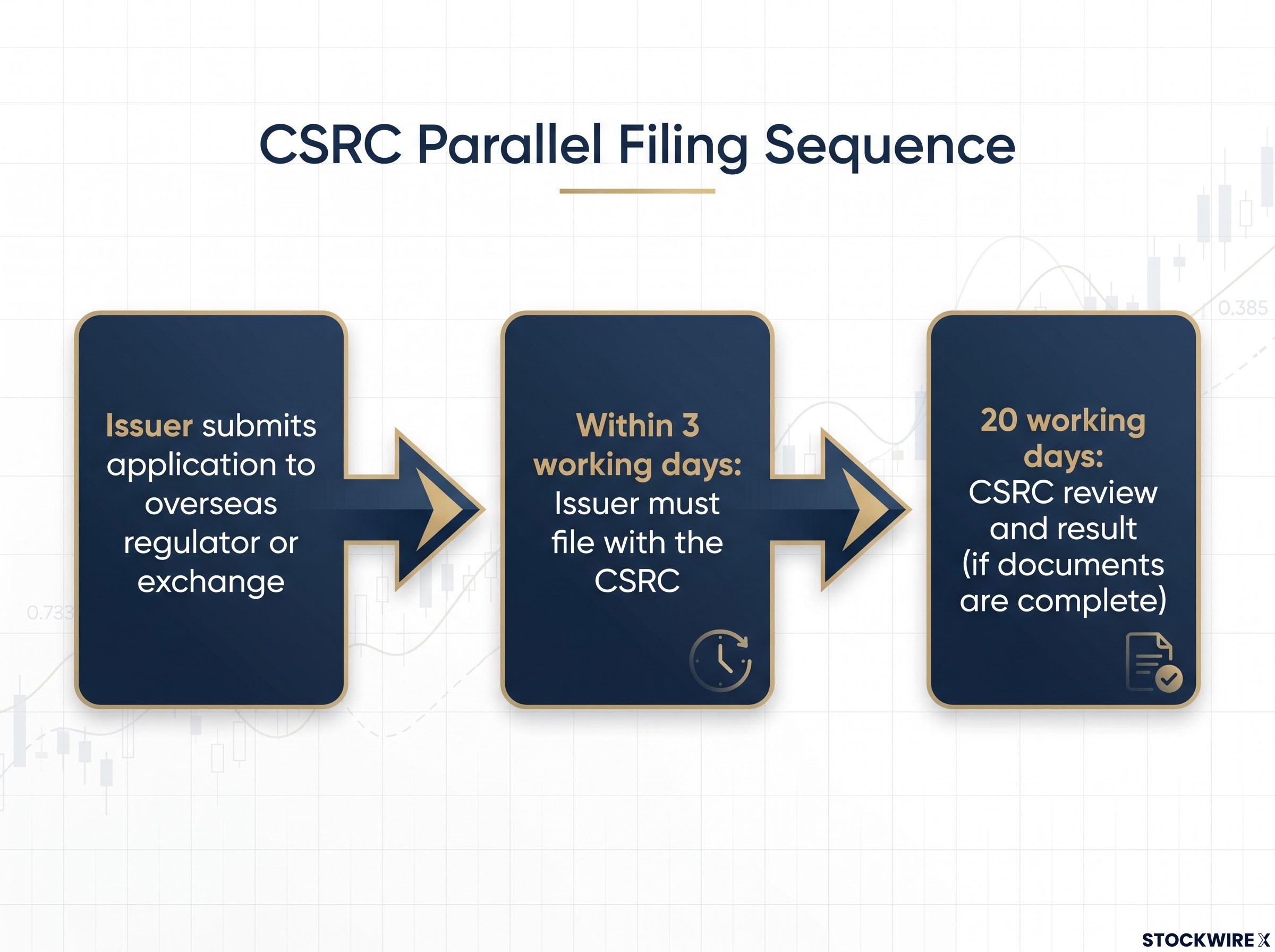

The parallel filing sequence works as follows:

That three-day window is what makes the regime transaction-critical. CSRC review does not wait for the overseas process to conclude. It runs alongside it, meaning a delayed or rejected CSRC filing can derail deal timing just as effectively as an SEC comment letter.

The Trial Administrative Measures of Overseas Securities Offering and Listing, published by the CSRC in February 2023, establishes the three-day submission window, the 20-working-day review timeline, and the quantitative capture criteria that determine whether an offshore holding company qualifies as a domestic company subject to the regime.

The regime captures more than PRC-incorporated entities. Foreign-incorporated issuers, including the Cayman Islands and British Virgin Islands holding companies through which most China-related businesses access U.S. markets, fall within scope if their main business operations, assets, or management are predominantly located in China. The CSRC applies quantitative tests on revenue, assets, and management location to determine whether an offshore entity qualifies.

A data security and national security overlay adds a further requirement: issuers must complete any required security reviews before filing with the CSRC. For companies handling sensitive personal data or operating in sectors with national security implications, this pre-clearance step can add weeks to the preparation timeline.

The numbers tell a specific story when read as an analyst would read them: not as a simple count of approvals, but as evidence of a screened, discretionary process operating at meaningful scale.

As of 22 May 2026, the CSRC had publicly disclosed 50 filing applications relating to U.S. listings, according to ARC Group’s analysis of CSRC disclosures. Against that application base, LLYC’s data reports 56 approvals or filing notices in 2024 and 14 in 2025, with the 2025 figure reflecting an eight-month pause that broke only in December 2025. ARC Group confirms that at least one additional U.S.-related approval was issued in 2026 as of its publication date.

| Year | Approvals / Notices | Notes | Source |

|---|---|---|---|

| 2024 | 56 | Full year | LLYC |

| 2025 | 14 | Pause lifted December 2025 | LLYC |

| 2026 | At least 1 | To May 2026 | ARC Group |

The drop from 56 to 14 and the subsequent December resumption suggest a pipeline that operates on a rolling, discretionary basis rather than through annual approval windows. When clearances stop, they stop because the regulator pauses; when they resume, the pipeline picks up where it left off.

The 50 publicly disclosed U.S.-related filing applications likely understate total pipeline activity. Confidential filing options are permitted under the regime, meaning precise approval-rate calculations are not possible from public data alone. The directional signal, however, is clear: the channel is active, selective, and continuing.

Understanding which issuers are subject to the filing regime requires working through the Measures’ definitional logic. The distinction between direct and indirect listings is where most U.S.-bound transactions sit, and getting the classification wrong can stall a deal before it starts.

A direct listing involves a PRC-incorporated company offering securities overseas. An indirect listing involves a foreign-incorporated entity, typically a Cayman or BVI holding company, whose underlying operations are in China. The CSRC determines indirect listing status through three quantitative capture criteria:

If any combination of these tests establishes that the business is substantially Chinese in character, the offshore holding company is treated as a “domestic company” under the Measures. Clean corporate structure and early regulatory alignment are therefore baseline requirements for any cross-border deal, not optional refinements applied late in the process.

De-SPAC combinations are treated as indirect listings when the post-combination company’s business and management are mainly in China. The CSRC applies the same filing requirements and review standards as for traditional IPOs. SPAC structures attract issuers for pricing, timetable, and valuation flexibility reasons, not because they reduce CSRC filing obligations. Both IPOs and de-SPACs have received approvals under the regime, confirming that neither channel carries lighter scrutiny.

Three recent approvals illustrate the range of businesses, sectors, and deal structures that have passed CSRC scrutiny. Read together, they move the calibrated access interpretation from abstraction to evidence.

The sector diversity across these three approvals, logistics, new energy, and software, signals that the regime’s clearance criteria are compliance- and disclosure-driven rather than industry-specific. The variable that separates cleared transactions from stalled ones appears to be the quality of preparation, not the sector classification.

While the CSRC was refining its filing regime from the Beijing side, Nasdaq independently tightened its own listing standards. The exchange’s recent changes would matter even without the CSRC framework. Combined, they create a genuinely dual-gated environment.

The three changes arrived in quick succession:

Rule IM-5101-3 makes governance quality, advisor reputation, and shareholder structure function as unofficial prerequisites that cannot be reduced to checkable quantitative criteria. A China-related issuer that clears the CSRC, meets Nasdaq’s financial thresholds, and files a complete application can still be denied if the exchange judges the governance structure or intermediary quality to be insufficient. Deal teams must now manage exchange-level qualitative review as a distinct risk alongside CSRC compliance.

For deal teams working through the De-SPAC pathway specifically, our full explainer on Nasdaq’s MVUPHS requirements for De-SPAC transactions covers how high redemption rates compress the qualifying float, why PIPE share registration timing is a critical structuring dependency, and what the separate $25 million threshold for China-based issuers means for transaction design from term sheet onward.

The CSRC filing regime and Nasdaq’s tightened standards now operate as parallel filters on the same pipeline. Each gate is more substantive than its pre-2023 counterpart, and clearing one does not guarantee passage through the other.

Five preparation requirements have shifted from best practice to minimum threshold for viable transactions:

The data supports this reading. Fifty publicly disclosed applications, 56 approvals in 2024, 14 in 2025, and a pipeline continuing into 2026 across multiple sectors confirm that the pathway is being used. Confidential filings mean the market is likely more active than public figures suggest.

Access to U.S. capital markets for China-related issuers is meaningfully open but conditional, and the conditioning is now applied from both sides simultaneously. Transactions designed around both constraint sets can still clear; those that treat either gate as a formality face materially higher execution risk.

The CSRC’s overseas listing regime has restructured access, not eliminated it. Three years of filing data, cross-sector approvals, and a pipeline that resumed after a multi-month pause in late 2025 all point to the same conclusion: the channel is active, selective, and operating within defined parameters.

Three forward indicators will shape the second half of 2026. The first is CSRC approval volumes through the remainder of the year, which will signal whether the pace is stabilising or contracting further from the 2024 peak. The second is whether Nasdaq finalises its proposed $25 million minimum IPO offering size, a rule that would further narrow the viable issuer profile. The third is whether de-SPAC approvals converge with or diverge from traditional IPO clearance rates, a signal of how the CSRC views alternative listing structures going forward.

The SEC disclosure environment that Chinese issuers must navigate is itself shifting: the SEC’s May 2026 proposal to allow eligible domestic public companies to replace quarterly 10-Q filings with a semiannual Form 10-S would, if finalised, alter the ongoing reporting cadence that post-listing Chinese companies must maintain, adding another variable to the post-approval compliance picture.

The US-China bilateral framework that shapes CSRC policy is itself in motion: the May 2026 Beijing summit produced a preliminary consensus on tariffs and procurement commitments, but no formal agreement or implementation timeline, leaving the macro regulatory environment that Chinese issuers navigate as unsettled as the exchange-level rules they must satisfy.

For U.S. finance professionals evaluating China-related issuers, the analytical question has shifted.

The question is no longer “is the pathway open?” It is “does this issuer meet the dual-gate preparation standard?”

Past performance does not guarantee future results. Regulatory frameworks are subject to change based on policy developments in both jurisdictions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The CSRC overseas listing regime, established by the Trial Administrative Measures effective 31 March 2023, requires Chinese companies (including offshore holding companies with predominantly Chinese operations) to file with the China Securities Regulatory Commission within three working days of submitting an application to an overseas exchange, with the CSRC then conducting a parallel 20-working-day review.

According to LLYC data cited in the article, 56 approvals or filing notices were issued in 2024, followed by 14 in 2025 after an eight-month pause that lifted in December 2025, with at least one additional approval confirmed in 2026.

Nasdaq introduced Rule IM-5101-3 in December 2025 granting broad discretionary authority to deny listings based on governance or advisor quality, raised the minimum public float under the net income standard from $5 million to $15 million in January 2026, and is considering a proposed $25 million minimum IPO offering size as of June 2026.

Approvals have spanned multiple sectors including logistics (Smart Logistics Global Limited, April 2025), clean energy (Londian Wason New Energy Tech Inc., December 2025), and enterprise software (DSC Holdings Ltd., April 2026), indicating that clearance criteria are compliance-driven rather than industry-specific.

Deal teams must ensure a clean and transparent offshore corporate structure, begin CSRC filing preparation before submitting the overseas application, complete any required data security reviews in advance, engage credible advisors and auditors, and confirm the issuer meets Nasdaq's $15 million float minimum and proposed offering size thresholds.