How a Jury Conviction Redraws Director Disqualification Risk

47 mins ago

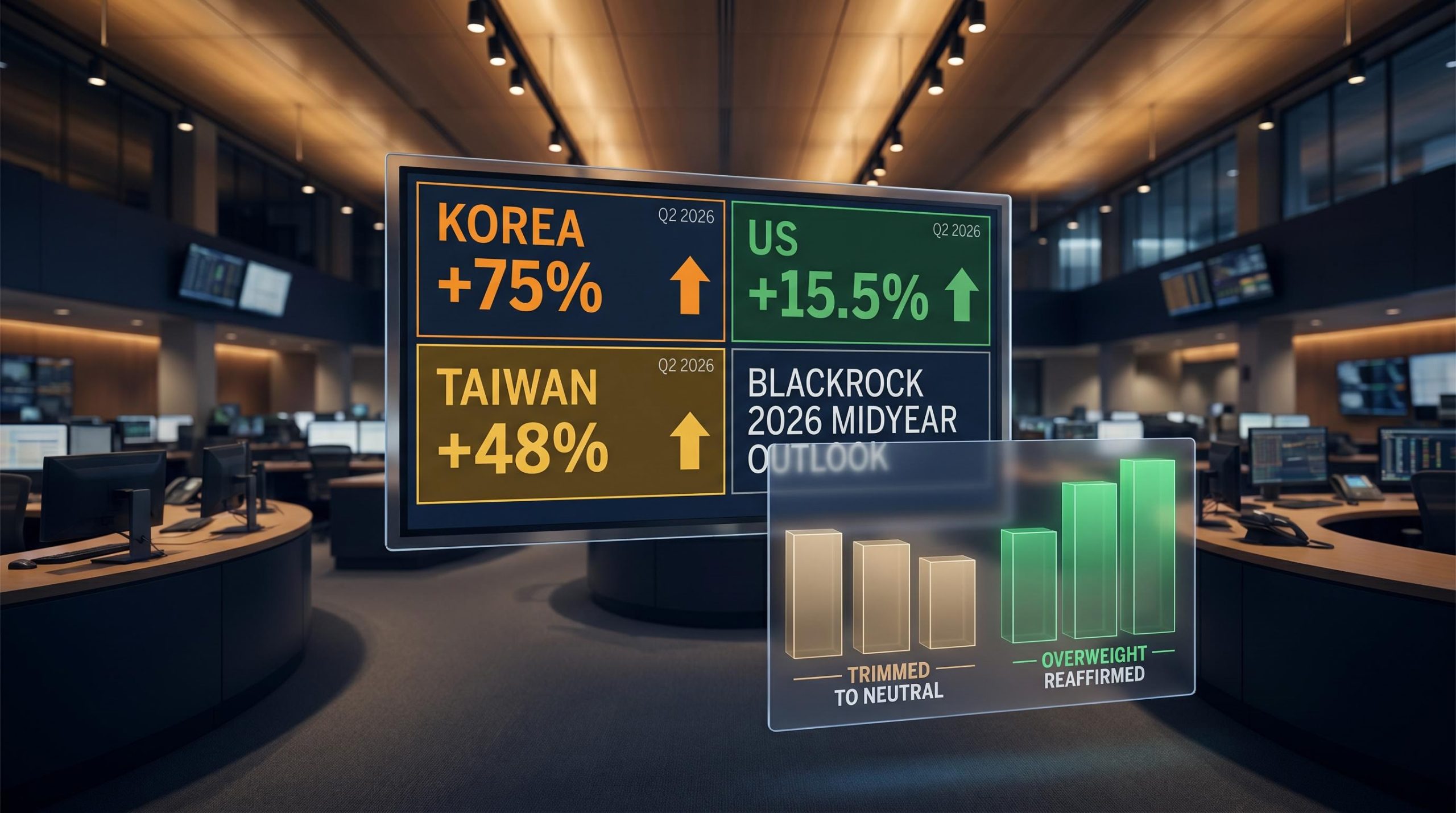

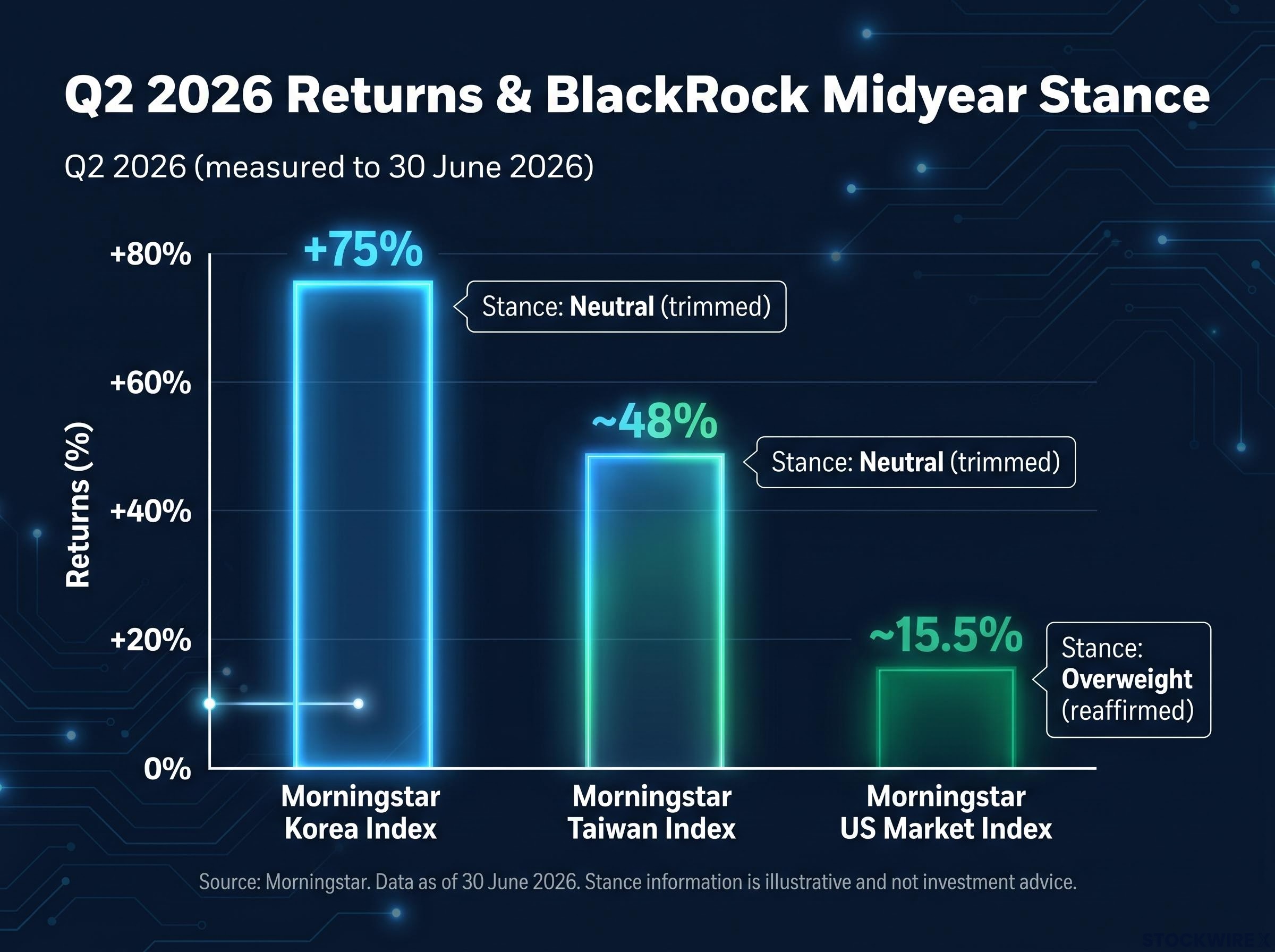

BlackRock’s midyear move is not the story most investors assume when they see “reduced emerging markets exposure.” After Korean equities surged more than 75% and Taiwanese equities climbed roughly 48% in a single quarter, BlackRock did not cut because it lost faith in AI. It cut because the positions had grown too large relative to what the risk warranted.

BlackRock’s 2026 Midyear Global Investment Outlook, published in early July 2026, lays out a world the firm describes as defined by scarcity: energy, infrastructure, labour, capital, and materials all facing demand that exceeds available capacity as the AI buildout accelerates. That framing shapes every allocation decision in the report, from staying overweight U.S. equities to trimming positions that have already delivered and now carry disproportionate risk.

Here is the internal logic connecting both moves, what the scarcity framework actually implies for sector exposure beyond technology, and where BlackRock sees the least-crowded AI opportunities heading into the second half of the year. These are the three things that matter most when evaluating whether BlackRock’s positioning makes sense for your own portfolio.

Start with the numbers, because they explain the decision before any commentary does:

Those are extraordinary single-quarter moves. When a position delivers that kind of gain, its share of total portfolio risk can exceed its share of portfolio weight by a wide margin. A 5% allocation that triples in value does not just become a 15% allocation; it becomes the single largest contributor to portfolio volatility, regardless of where conviction sits.

That is precisely the reasoning Wei Li, Global Chief Investment Strategist at the BlackRock Investment Institute, gave for the shift from overweight to neutral on Asian emerging market equities. According to Li, the move had nothing to do with valuation concerns. It was driven by elevated volatility in both markets and the risk contribution those positions had accumulated after their surge.

Wei Li, BlackRock Investment Institute: “Hold steady and reduce concentrated exposure at this stage.”

The distinction matters. A valuation-driven cut implies the thesis has changed. A volatility-driven trim implies the thesis is intact but the position has outgrown its risk budget. For your own AI-linked holdings that have run hard this quarter, the question BlackRock is answering here is not “do I still believe?” but “has the position gotten too big for what the risk warrants?”

The practical mechanism for applying this logic to your own holdings is beta-weighted position sizing, which converts each position into market-risk equivalent dollars and reveals whether your AI-linked names are contributing risk proportional to their portfolio weight or are quietly dominating your volatility profile.

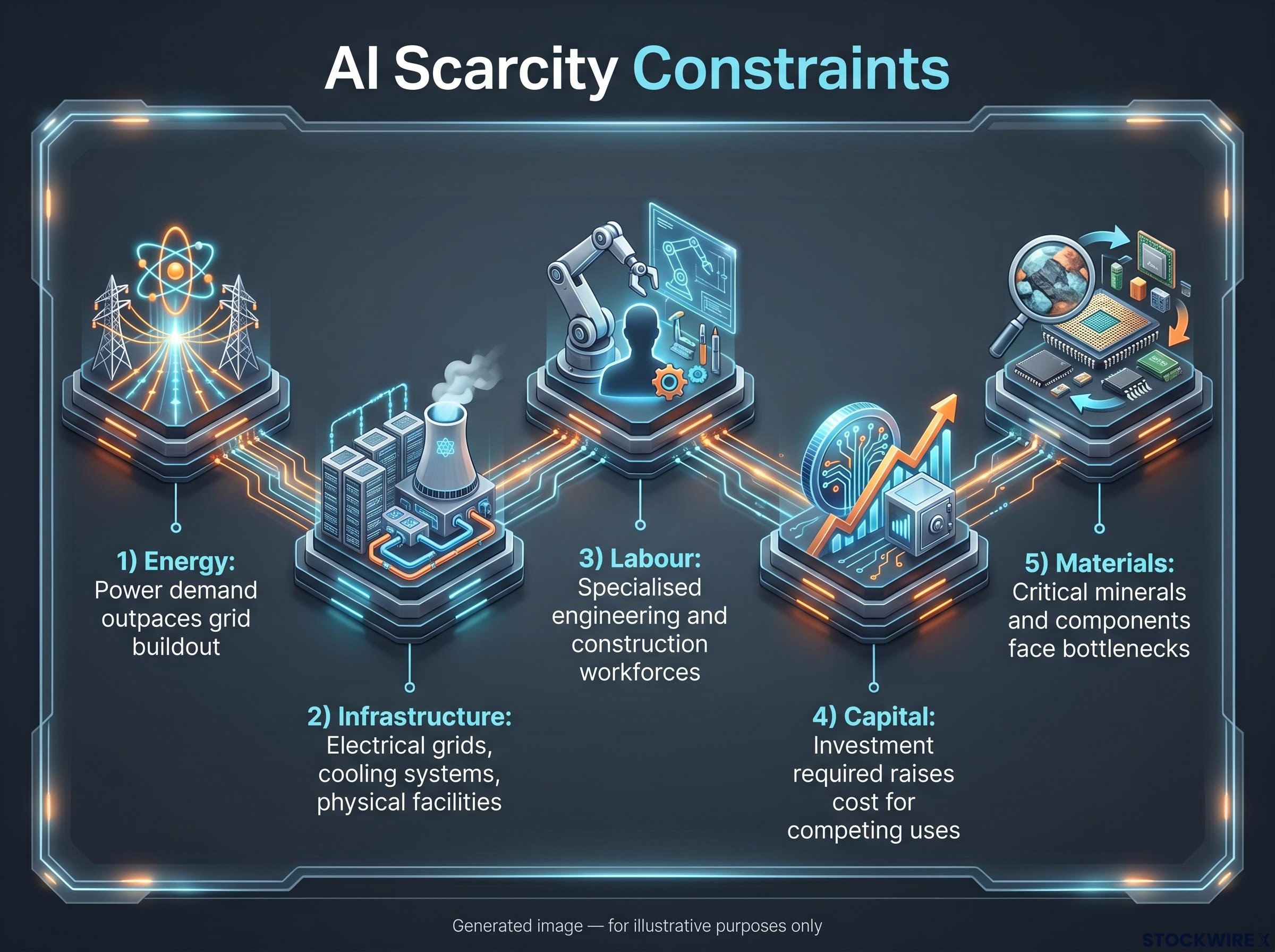

Scarcity is one of those words that gets used so often in market commentary it risks meaning nothing. BlackRock is specific about what it means: the condition where AI-driven demand outstrips available capacity across multiple input categories, not just semiconductors.

The midyear outlook names five explicit constraint categories:

The breadth of that list is the point. If you are positioned purely in AI software or chip names, you are capturing only part of the opportunity BlackRock is describing. Bottleneck pressures are most acute across the infrastructure and energy segments, with the tightest constraints found in power generation, grid buildout, semiconductor supply chains, and physical AI systems.

BlackRock describes this environment as “ripe for active investing,” with concentrated gains and “more room for alpha and the need for big calls.” The AI infrastructure opportunity is sector-agnostic in origin but highly concentrated at specific bottleneck nodes. That distinction is what separates the scarcity framework from a generic “buy AI” thesis.

The five constraint categories BlackRock names are not equally tight: AI infrastructure bottlenecks in power generation and grid interconnection carry multi-year resolution timelines that semiconductor supply chains do not, which is why the scarcity premium is concentrating at specific nodes rather than spreading evenly across the AI investment universe.

BlackRock reaffirmed its overweight on U.S. equities in the midyear outlook, and the reasoning is structural rather than momentum-driven. Wei Li pointed to four structural strengths that give the U.S. a durable edge in the AI buildout:

The Q2 performance data makes the cost of underweighting the U.S. visible:

| Market | Index | Q2 2026 Return | BlackRock Stance as of Midyear |

|---|---|---|---|

| United States | Morningstar US Market Index | ~15.5% | Overweight (reaffirmed) |

| South Korea | Morningstar Korea Index | +75% | Neutral (trimmed from overweight) |

| Taiwan | Morningstar Taiwan Index | ~48% | Neutral (trimmed from overweight) |

Morningstar data shows that the U.S. market’s Q2 gain of approximately 15.5% represented the best single quarter for U.S. equities in six years. Market-cap-weighted U.S. indexes, which overweight the largest AI beneficiaries, have significantly outperformed equal-weighted versions over the same period.

BlackRock Investment Institute: Avoiding U.S. AI exposure is “not a neutral stance” but a deliberate underweight to the key return driver, and one that has so far been unrewarded.

BlackRock frames these advantages as durable rather than cyclical. If your portfolio has tilted away from market-cap-weighted U.S. exposure over the past two quarters, through equal-weighting or regional diversification, the data suggests you have likely paid a material performance cost. The question is whether your diversification rationale is strong enough to justify continuing that bet against the structural case BlackRock is making.

Most investors assume AI is a mega-cap story. The largest positions in the largest indexes hold the largest AI beneficiaries, and that is where the theme lives. Wei Li disagrees, at least partially.

Li pointed to small-cap equities as a segment the market has largely overlooked when scanning for AI-related return potential, arguing that active mandates are better positioned to find AI exposure in less obvious corners of the market, including small-cap value. Within that universe, memory stocks stand out: despite accounting for a relatively small slice of the small-cap index by number of constituents, they have generated a share of returns far exceeding their weight.

Wei Li, BlackRock Investment Institute: Small-cap equities offer an area where active strategies can uncover AI exposure in less conventional areas, with memory stocks driving a significant share of returns despite modest universe representation.

The implication connects directly to how you think about portfolio construction:

For an investor who assumes their AI exposure is adequate because they hold a broad U.S. equity index, this surfaces a genuine gap. The fastest-moving pockets of AI returns may be concentrated in segments where passive vehicles carry thin weights, and where BlackRock’s “more room for alpha” framing has the most practical application.

Every individual allocation decision in the midyear outlook flows from a single structural observation: the macro environment has changed, and portfolio construction has to change with it.

BlackRock describes a more levered financial system with heightened vulnerability to bond yield spikes and a structurally higher cost of capital than the prior cycle. That is the backdrop against which every position must justify its place.

Higher capital costs are not an abstraction in mid-2026: the 10-year TIPS real yield reached 2.22%, its highest level in over 12 months under new Fed Chair Kevin Warsh, establishing a materially different hurdle rate than the sub-1% real rate environment in which most portfolio valuation models were originally calibrated.

| Approach | Characteristics | BlackRock’s Midyear Assessment |

|---|---|---|

| Prior cycle: spreading risk indiscriminately | Broad diversification across regions and asset classes; risk allocation by convention rather than conviction | Less effective in a concentrated-return environment with higher capital costs |

| Current approach: owning risk deliberately | Scenario-based construction; each position justified by its specific risk-return contribution; concentration where conviction is highest | Recommended; aligned with scarcity-driven dispersion and shock-prone system |

This is the connective tissue that makes sense of seemingly contradictory moves. Cutting Asian EM while adding U.S. concentration is not inconsistent when both decisions flow from the same framework: calibrated risk ownership in a shock-prone system. The Asian positions had accumulated outsized risk contribution after their Q2 surge. The U.S. positions carry structural advantages that justify concentration.

In a higher capital cost environment, the opportunity cost of holding positions that are merely diversifying rather than deliberate has risen. BlackRock’s framework asks you to assess whether each position in your portfolio is there by active choice or by default inertia.

Four actionable takeaways emerge from BlackRock’s midyear positioning, each translatable beyond the firm’s specific trades:

The tension BlackRock is navigating, a pro-risk stance within a shock-prone, higher capital cost system, is the same tension in most investor portfolios right now. The most important question to take from this outlook is whether your AI exposure is deliberate and calibrated, or the product of passive allocation choices made in a different market environment.

Investors exploring how to offset crowded AI positioning with a structural hedge will find our full explainer on European equities as an AI hedge, which covers the Barclays analysis of extreme hedge fund short positioning in European small caps and the mechanical snap-back dynamic that activates when AI momentum unwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The BlackRock 2026 Midyear Global Investment Outlook, published in early July 2026, sets out BlackRock's view that AI-driven demand is creating scarcity across energy, infrastructure, labour, capital, and materials, and uses that framework to justify staying overweight U.S. equities while trimming concentrated Asian emerging market positions that surged in Q2.

BlackRock moved from overweight to neutral on Asian emerging market equities because the positions had accumulated outsized risk contribution after extraordinary Q2 gains, not because the AI thesis had changed; the Morningstar Korea Index surged more than 75% and the Morningstar Taiwan Index climbed roughly 48% in a single quarter, making the positions too large relative to what the risk warranted.

BlackRock's scarcity framework identifies five input categories where AI-driven demand is outstripping available capacity: energy, infrastructure, labour, capital, and materials; the practical implication is that the AI investment opportunity extends well beyond chip and software names into power generation, grid buildout, and critical minerals.

BlackRock cites four structural advantages that give the U.S. a durable edge in the AI buildout: leadership in chip design and AI model development, energy independence, and deep capital markets; the firm also frames any move away from U.S. market-cap-weighted exposure as a deliberate underweight to the key return driver, one that cost material performance in Q2 2026.

The core question BlackRock's framework asks is whether a position has grown too large for the risk it contributes, not whether the underlying thesis still holds; beta-weighted position sizing is the practical tool for converting each holding into market-risk equivalent dollars and revealing whether AI-linked names are quietly dominating your volatility profile after a strong run.