The TIPS market posted a real return of 2.22% on the 10-year benchmark, a reading not seen for well over twelve months, and the catalyst was not an inflation shock or a credibility crisis. It was a new Fed Chair deliberately choosing to tighten. Kevin Warsh took the oath as the 17th Federal Reserve Chair on 22 May 2026, and he has wasted no time recentring policy around price stability. The most recent dot plot indicates that approximately half of FOMC members are pencilling in at least one rate increase before the end of the year, with the median 2026 policy rate projection landing near 3.8%. That repricing has overpowered any macro relief the U.S.-Iran interim deal might have delivered, leaving risk assets without the tailwind many anticipated. By the end of this article, you will understand exactly why real yields at this level change the maths for stocks, bonds, credit, and gold, and what that means for how your portfolio is positioned right now.

Warsh’s first major signal: a Fed that wants rates higher

Kevin Warsh succeeded Jerome Powell on 22 May 2026 and immediately began reshaping the committee’s direction. His early public communications have centred on one message: price stability is no longer one priority among several. It is the priority.

Warsh’s confirmation and policy inheritance matter here because the committee he took over was already navigating headline inflation at 3.8% year-over-year and core CPI at 2.8%, both well above the Fed’s 2% target, meaning his hawkish mandate landed into an environment primed for an immediate policy test rather than a gradual handover.

The evidence is already in the numbers. The latest dot plot reveals that the committee’s centre of gravity has shifted, not just its edges:

The FOMC Summary of Economic Projections released on 17 June 2026 shows the committee’s median federal funds rate projection for 2026 sitting near 3.8%, with roughly half of participants pencilling in at least one additional hike before year-end.

- Appointment context: Warsh was confirmed with a mandate to restore inflation credibility, and his earliest statements have leaned explicitly hawkish.

- Dot plot split: Approximately half of FOMC participants now project at least one rate hike before year-end, up from a small minority at the start of 2026.

- Median rate projection: The median 2026 policy rate sits at roughly 3.8%, the concrete anchor markets are now pricing around.

Warsh’s defining policy frame: The new Chair has explicitly recentred Fed policy around price stability, signalling that the committee’s tolerance for above-target inflation has narrowed materially.

This is not one dissenter or a temporary lean. The committee’s centre has moved, and your portfolio’s rate assumptions need to move with it.

When big ASX news breaks, our subscribers know first

What a 2.22% real yield actually means, and why this level is different

The 10-year TIPS yield measures what investors earn from U.S. Treasuries after stripping out expected inflation. It is the true inflation-adjusted cost of capital for the entire economy, the number that sets the hurdle rate every other asset must clear.

After the Fed’s latest decision, that figure settled at 2.22%, marking its most elevated close in over 12 months. Recent readings have held in the 2.21-2.23% range as of mid-to-late June 2026, up approximately 0.21 percentage points year-on-year.

The Fed outlook reversal is striking in its speed: markets moved from pricing 50-75 basis points of cuts to a 65-70% probability of a rate hike by December 2026 in roughly ten weeks, a repricing driven by core PCE data tracking nearly 80 basis points above the Fed’s own year-end projection and reinforced by explicit, quantitative tightening conditions articulated by senior FOMC officials.

| Period | 10-Year Real Yield | What It Means |

|---|---|---|

| Post-2020 baseline | Sub-1% | Treasuries offered little real return; risk assets faced almost no competition for capital |

| One year ago (~June 2025) | ~2.01% | Real rates were rising but still treated as transitional, not structural |

| Current (June 2026) | 2.22% | Treasuries now deliver a genuine inflation-adjusted return; every competing asset must clear a materially higher hurdle |

The new structural baseline

If your valuation models still embed sub-1% real rate assumptions, they are producing systematically optimistic outputs. A real yield of 2.22% means Treasuries now pay you to hold them in inflation-adjusted terms, and every equity, credit instrument, or alternative asset must justify its risk against that benchmark.

Four structural reasons the geopolitical relief trade left risk assets cold

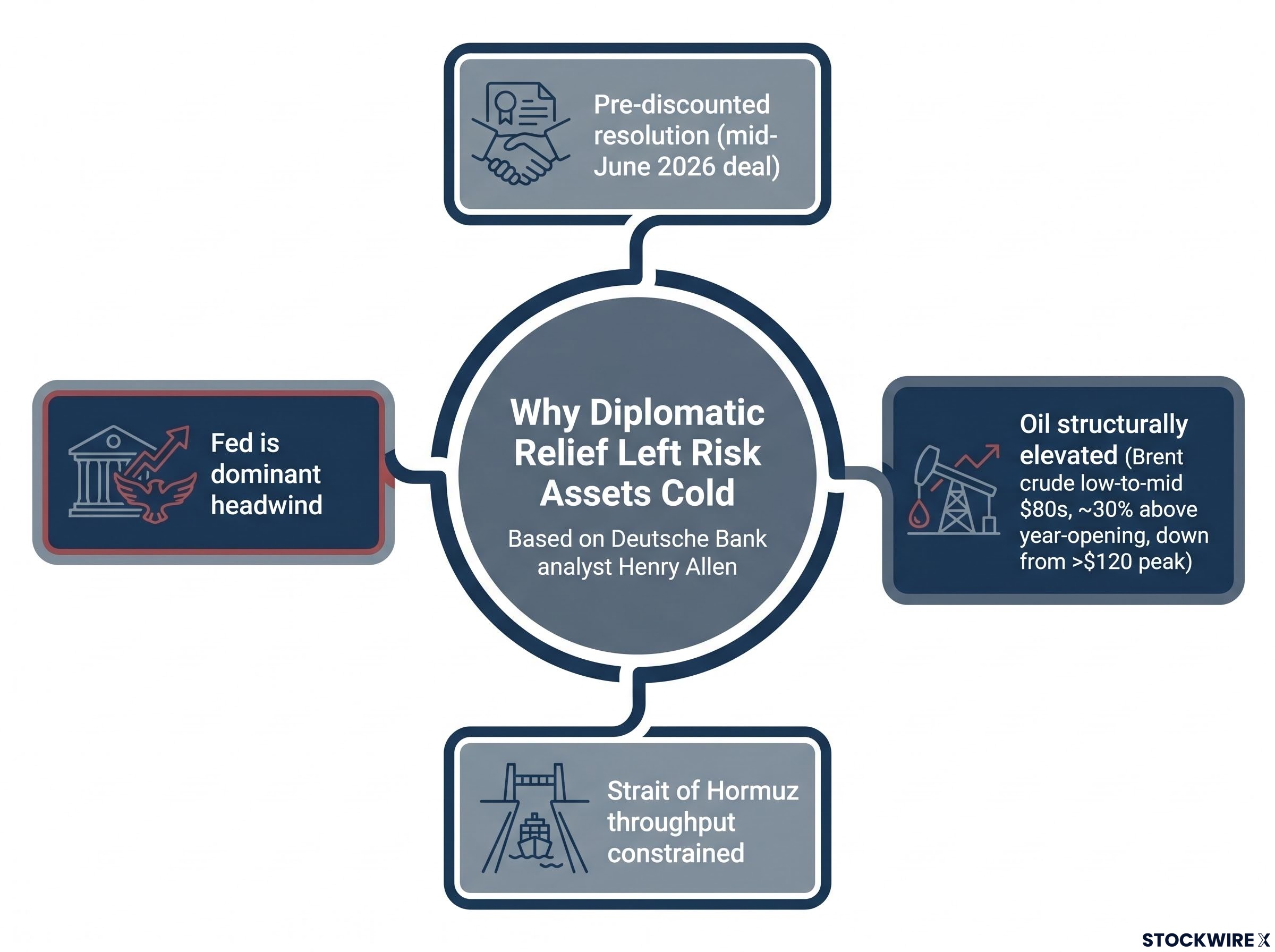

An interim U.S.-Iran deal framework was signed in mid-June 2026. Oil prices pulled back from their conflict-era peaks. And yet broad risk assets barely moved. Deutsche Bank analyst Henry Allen set out four explanations for this, each building on the last to form a picture of a market where diplomatic good news is structurally insufficient, not coincidentally muted.

- Markets had pre-discounted resolution. The geopolitical conflict was widely treated by investors as a temporary disruption from the outset, which placed a firm ceiling on the gains any eventual deal could unlock. The relief was already partially priced in.

- Oil remains structurally elevated. Brent crude still sits roughly 30% above its year-opening level as of 22 June 2026, with recent levels in the low-to-mid $80s after peaking above $120 during the conflict. Energy markets are not back to normal.

- Strait of Hormuz throughput remains constrained. Vessel movements through the strait remain well below their pre-conflict norms, with the interim agreement having done little to restore normal throughput.

- The Fed is the dominant headwind. With the Fed deliberately tightening financial conditions, any geopolitical good news must fight a powerful rates headwind to move broad risk assets.

Deutsche Bank’s conclusion: Fed hawkishness is the primary factor working against any sustained risk-asset rally following the geopolitical resolution. Diplomatic tailwinds cannot overpower a central bank that is actively leaning against them.

The Iran deal tells you geopolitical resolution is a necessary but not sufficient condition for a risk rally when the Fed is deliberately working in the other direction. Do not build a portfolio thesis around diplomatic good news in this rate environment.

The Iran ceasefire’s market impact tells a more complex story than the headline equity records suggest: a 14-point memorandum committed the Strait of Hormuz to reopen within 30 days, yet Saudi Aramco warned that full physical supply recovery could extend into 2027, and markets are pricing only approximately 17 basis points of Fed rate cuts before year-end, a level that could easily disappoint if the Fed stays hawkish regardless of lower energy prices.

How to navigate a higher-for-longer world: what each asset class faces now

The 2.22% real yield is not a headwind you can wait out. It is the new hurdle rate every position in your portfolio must now justify itself against. Here is what that means across asset classes, built into a single integrated picture rather than disconnected verdicts.

Fixed income and credit

Short-to-intermediate maturity bonds now offer genuine real carry with substantially less duration risk. At these yield levels, bonds regain their role as a real return source, not just portfolio ballast. Long-duration Treasuries and investment-grade credit, however, remain vulnerable if real yields grind higher from here.

In credit, the priority is climbing the quality spectrum. Rising real yields push up all-in borrowing costs, and issuers with large near-term refinancing needs and thin interest coverage feel it first. The refinancing risk that was theoretical at lower rates is now priced into the market.

Equities and yield-sensitive strategies

Higher real rates raise discount rates and compress price-to-earnings (P/E) multiples, the ratio of a company’s share price to its per-share earnings. Cash-flow-light growth names are most exposed. The priority shifts to companies with profitable growth, strong balance sheets, and pricing power.

REITs (real estate investment trusts) and high-dividend strategies face a specific test: when TIPS offer more than 2% real, these yield vehicles must justify their risk premium with genuinely above-market sustainable yields or embedded growth, not merely current payout. Highly leveraged real-estate vehicles are doubly exposed through higher financing costs and tougher valuation comparisons against safer income.

Gold’s opportunity cost rises as real yields climb. Size it as a tail-risk hedge, not a return engine. And in emerging markets, differentiate aggressively: stronger balance-sheet, export-oriented economies can absorb a firm dollar; fragile, twin-deficit names cannot.

| Asset Class | Direction | Key Reason | One Action |

|---|---|---|---|

| Fixed Income | Shorten duration | Real carry available at the short end; long duration vulnerable | Tilt toward short-to-intermediate maturities |

| Equities | Favour quality | Higher discount rates compress multiples on cash-flow-light names | Prioritise profitable growth with pricing power |

| Credit | Move up in quality | Rising borrowing costs hit weak issuers first | Avoid issuers dependent on rolling cheap debt |

| REITs / Yield Strategies | Raise the bar | Must beat 2%+ real TIPS alternative | Require above-market yield or embedded growth |

| Gold | Resize, do not abandon | Opportunity cost rises with real yields | Size as risk-management tool, not return engine |

| Emerging Markets | Differentiate aggressively | Firm dollar environment pressures weak external balances | Favour strong balance-sheet, export-oriented economies |

“Higher for longer by choice, not by crisis”: why this regime is different from past tightening cycles

If your instinct is to sell everything because the Fed is hiking, this is the section that gives you the analytical reason to pause. Not every tightening cycle carries the same risk, and the current one is driven by a fundamentally different logic than the episodes most investors anchor to.

Consider the contrast:

- Current regime: The Fed is tightening because economic growth and demand remain resilient. Warsh has framed his approach as price-stability recentring, not crisis management.

- 2018-2019 cycle: The Fed tightened into slowing growth and ultimately reversed course when markets cracked, a policy-error pattern.

- Current regime: Inflation is above target but not spiralling. The tightening is proactive, not reactive.

- Policy-error episodes: Tightening typically came alongside collapsing confidence, credit stress, or runaway price instability.

Deutsche Bank retained a constructive view over the longer term, arguing that when Fed tightening reflects robust growth rather than crisis conditions, it represents a backdrop that equity and credit markets are capable of digesting.

“Hawkish because the economy is strong” is uncomfortable for leveraged, story-driven assets. But it is navigable for portfolios built around real cash flows and realistic return hurdles. The distinction matters more than the direction of rates alone.

The new hurdle rate is here: recalibrate before the next move

The core positioning shift is straightforward: replace post-2020 sub-1% real rate assumptions with 2%+ as the structural baseline across all models and hurdle rates. Derivative markets have already repriced toward a meaningful probability of further tightening in 2026, and the committee’s centre of gravity supports that view.

Here are the five recalibration actions to apply now:

- Shorten fixed income duration. Capture real carry at the short-to-intermediate end while reducing exposure to further yield increases.

- Favour equity quality and cash flow. Profitable growth with pricing power outperforms story-driven names when discount rates are rising.

- Climb credit quality. Avoid issuers dependent on rolling cheap debt. Refinancing risk is no longer theoretical.

- Resize gold as a risk tool. Maintain it for tail-risk hedging, but do not treat it as a core return engine at 2%+ real yields.

- Differentiate emerging markets by balance sheet. Respect the firm-dollar environment and separate strong external profiles from fragile ones.

This regime is navigable, but only for investors who update their assumptions today rather than anchor to a rate world that no longer exists. The investors most at risk right now are not those who are pessimistic. They are those who have not yet updated their mental model from a 0% real rate world to a 2% real rate world.

For investors who want to work through the broader portfolio construction implications of a structural rate regime shift, our full explainer on 60/40 portfolio recalibration covers the 2022 correlation breakdown that exposed the 60/40 model’s regime dependency, a three-sleeve framework for adding explicit inflation sensitivity, and the behavioural discipline principles that matter as much as allocation ratios in a lower-return environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.