Three Catalysts That Could Test the Stock Market This Week

2 hrs ago

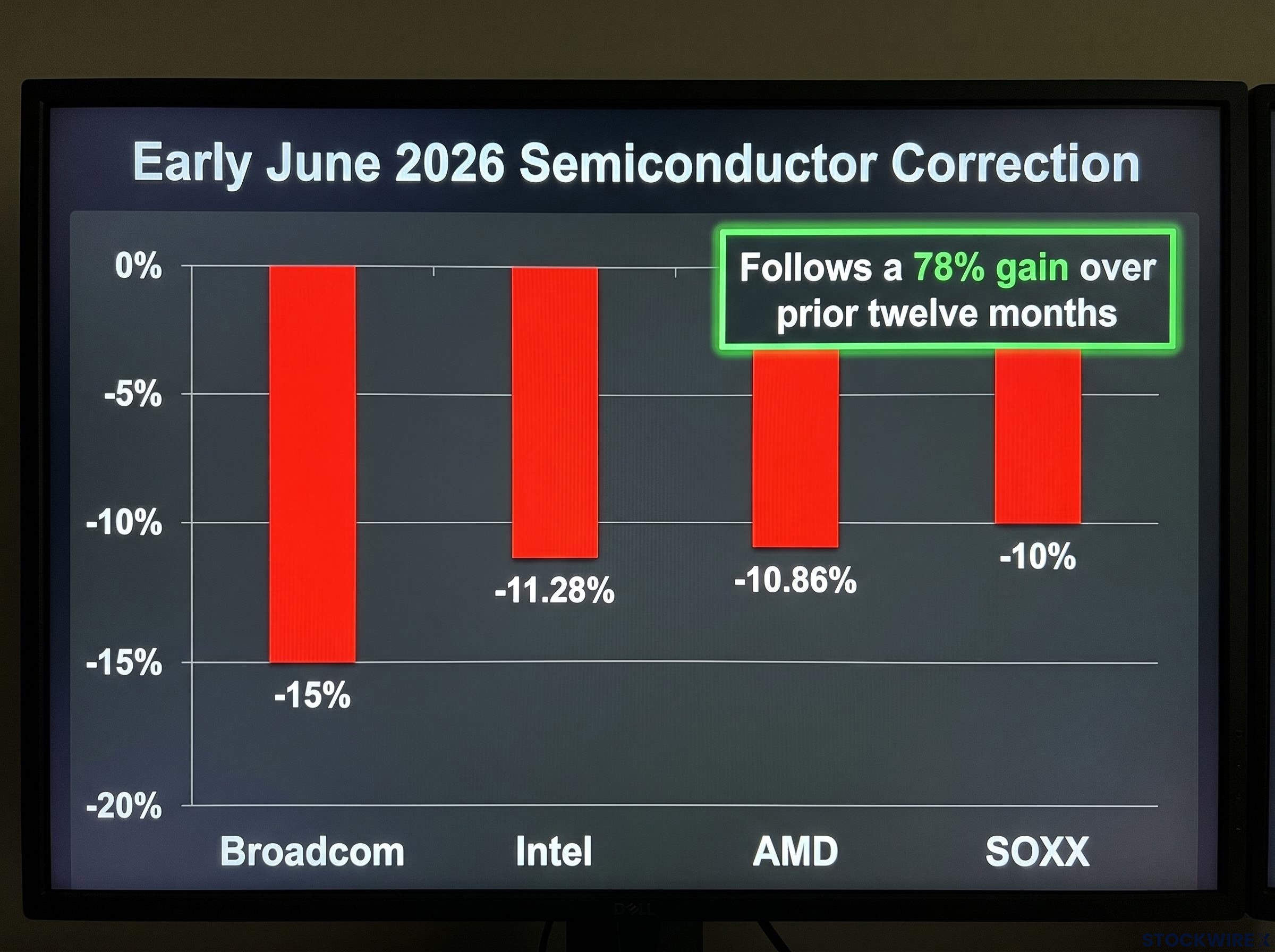

Broadcom held its 2026 guidance steady in early June. It did not cut. It did not warn. It simply told investors that the numbers it had already projected remained intact. The stock fell approximately 15%, and the shockwave dragged the entire semiconductor supply chain with it.

That reaction is the signal worth reading carefully. A company that confirmed nothing had changed triggered a sell-off that implied everything had. Across the Philadelphia Semiconductor Index, AI-linked chip names that had gained roughly 78% over the prior twelve months gave back a tenth of the index’s value in days. The correction was sharp, but the more interesting development is a split forming beneath the surface: chip and hardware-adjacent names are being marked down while software and platform businesses carrying AI exposure are proving more resilient, and in some cases pushing higher.

After this, you will know which variables actually separate the AI names worth holding from those where the risk-reward has quietly shifted against you. Not a generic overview of AI investing, but a specific framework calibrated to the phase this trade has entered as of July 2026.

The numbers arrived first, and they were not subtle:

Those declines followed a roughly 78% run in AI-focused semiconductor names over the prior twelve months. That context matters, because the correction is inseparable from what preceded it.

The issue is not that AI demand collapsed. The issue is that valuations had already priced in near-linear growth stretching years into the future, and the burden of proof flipped.

Chip valuation dispersion within the SOXX is wider than sector-level commentary typically suggests: Micron trades at under 9x forward earnings while Intel sits at approximately 101x forward P/E, meaning correction pressure and genuine earnings strength exist simultaneously inside the same index rather than representing a uniform reset.

When valuations discount indefinite acceleration, the question investors ask shifts from “will AI keep growing?” to “will it grow fast enough to justify this price?” That is a structurally harder bar to clear.

The Broadcom episode is the clearest proof. When holding guidance steady causes a 15% drop, the embedded expectations, not the underlying business, were the problem. What you are watching is a valuation correction, not a demand correction, and misreading the difference leads to either exiting too early or reloading into hardware names where the reset is not yet complete.

The apparent paradox sits in the capex data. Hyperscaler AI spending plans for 2026 are enormous by any historical standard:

| Hyperscaler | 2026 Capex Estimate | Trajectory Signal |

|---|---|---|

| Amazon | ~$200 billion | Expanding |

| Alphabet | $175-185 billion | Expanding |

| Meta | $115-135 billion | Stable |

| Microsoft | $120-190 billion | Expanding |

Collectively, that represents hundreds of billions of dollars in AI infrastructure spending in a single year. The build-out is not over.

Yet the market is not pricing the absolute level of that spending. It is pricing the rate of change. The question driving chip valuations is whether incremental acceleration from here will match prior assumptions, or whether the cycle is entering a digestion phase where existing infrastructure gets leveraged more fully before the next leg upward. That distinction matters: if you are watching capex totals to gauge chip stocks, you may be looking at the wrong metric. The trajectory of guidance, not the size of the number, is what moves semiconductor multiples from here.

Rising bond yields compound the problem. Higher discount rates mechanically compress the present value of future earnings, and that pressure hits hardest on cyclically exposed businesses whose revenues map directly to capex decisions that can shift quarter to quarter.

Geopolitical risk layers on top. Export controls targeting China, broader trade tensions, and regional instability introduce supply-chain uncertainty that further compresses forward multiples, even when underlying demand remains structurally intact. These macro factors do not negate the AI thesis, but they justify risk reduction in crowded trades where valuations are already stretched.

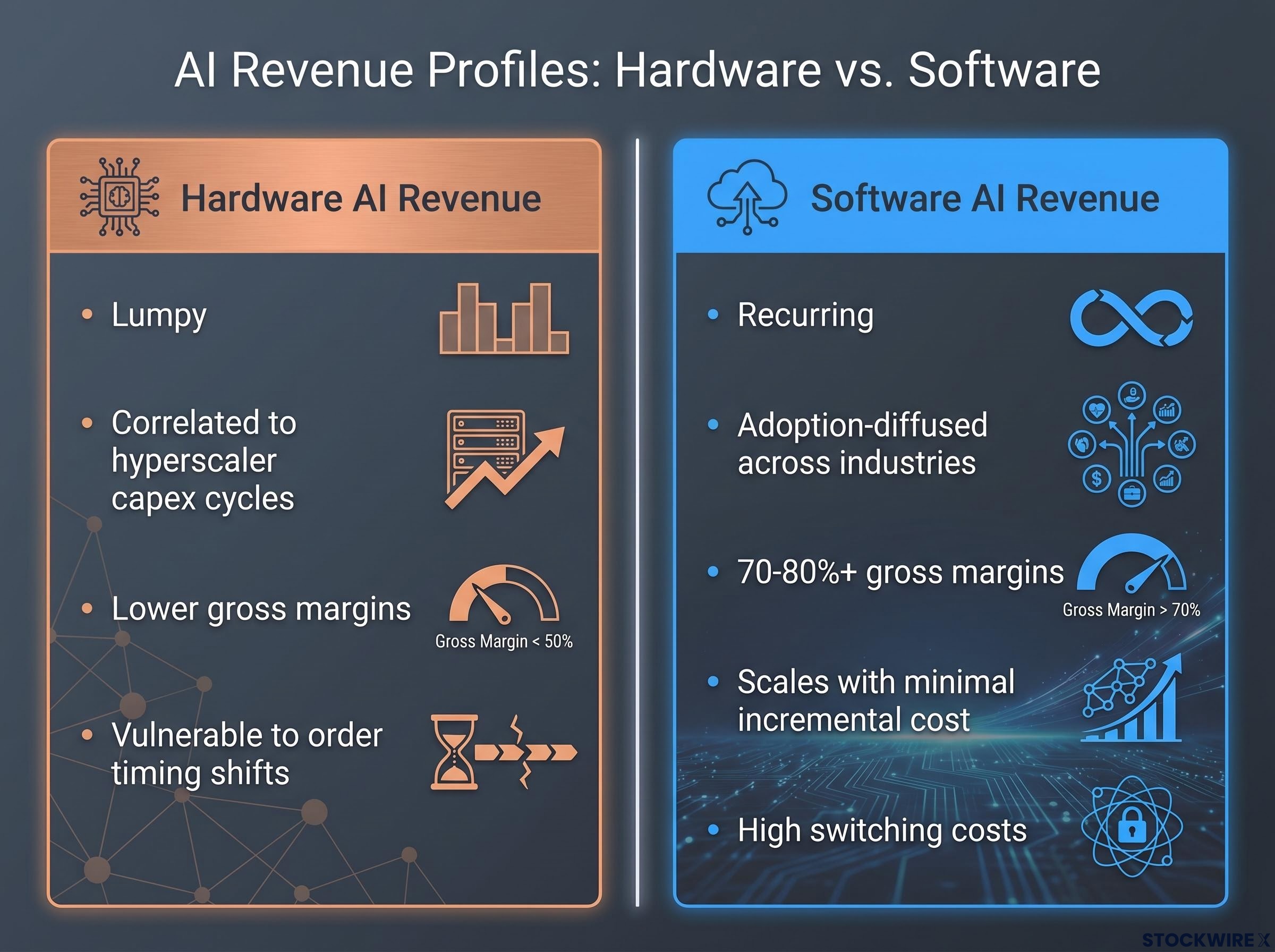

The structural distinction between how hardware and software businesses earn AI revenue is the analytical foundation for the rotation now underway.

Enterprise and cloud software vendors are not selling chips or training clusters. They are embedding AI features into existing products, productivity suites, customer relationship management tools, cybersecurity platforms, enterprise resource planning systems, and charging more per seat or per workflow. Their AI revenue depends on adoption by thousands of enterprise customers across many sectors, not on a handful of hyperscaler capex decisions made quarterly.

That diffusion of demand changes the risk profile entirely. Consider the contrast:

Goldman Sachs has put a specific date on the AI software revenue timeline, projecting 2027 as the inflection point for meaningful outperformance and identifying Microsoft and ServiceNow as the only companies currently producing quantified additive AI revenue evidence rather than qualitative progress disclosures.

Software businesses typically run gross margins of 70-80%+. Once AI features are built and deployed, incremental revenue from those features scales with minimal additional cost, reinforcing earnings quality in a way chip manufacturers cannot replicate at scale.

The third structural advantage is switching costs. Once AI is embedded in a mission-critical enterprise system, from automated document processing to security operations, removing it is operationally disruptive and financially costly. That stickiness supports valuations even during sentiment wobbles.

The margin and stickiness combination means software businesses monetising AI are not merely exposed to the AI theme. They are positioned to compound on it with high-quality earnings. That is why the market is comfortable maintaining higher multiples on these names even as it rerates hardware. For any AI-exposed company in your portfolio, asking whether the business earns AI revenue from infrastructure cycles or from embedded adoption is now a first-order question.

Apple’s recent strength is not contradicting the semiconductor correction. It is confirming the rotation thesis.

Apple is embedding AI into consumer devices and services, not selling training infrastructure. An AI-heavy iPhone upgrade cycle could drive upgrade behaviour across one of the largest installed bases in consumer technology, with services attach (iCloud, App Store, subscriptions) amplifying the revenue impact of each device sold. That gives investors AI upside without direct sensitivity to hyperscaler capex decisions.

The absence of hyperscaler dependency is the key differentiator. The fact that Apple is gaining ground while AI chip names sell off indicates that the market is distinguishing between types of AI exposure rather than retreating from the AI trade altogether. That distinction is worth watching closely: it confirms that capital is flowing toward businesses where AI enhances a proven product rather than businesses whose entire revenue depends on the infrastructure build-out continuing to accelerate.

Tesla is a more complicated read, and that complexity is itself the lesson.

The company has genuine AI assets. Its autonomous driving programme and in-house training compute are real. But Tesla’s stock moves also reflect traditional auto-sector pressures: demand growth challenges, price competition, margin compression, and regulatory scrutiny. These are company-specific headwinds that have little to do with whether the broader AI trade is healthy.

Because Tesla trades heavily as a story stock, its volatility can be misleading as a gauge of AI sentiment. The useful diagnostic question for any company held as an “AI name” applies directly here:

Is this move tracking AI fundamentals, or is it tracking company-specific factors?

Conflating the two leads to misreads in both directions. Tesla is a useful warning about narrative risk in AI investing, not a clean signal about AI demand.

The evidence and mechanisms point toward a specific set of positioning decisions. Four lenses, calibrated to the phase this trade entered following the early June 2026 correction:

The UBS portfolio rotation from chip and hardware names into defensive AI ecosystem plays in June 2026 followed exactly this logic: the firm cut its chip weighting from roughly 76% to 61% in a single month, using Micron’s earnings-driven rally as the exit window rather than waiting for a negative catalyst.

The framework is only useful if you apply it to what you already own rather than treating it as an abstract taxonomy. For each AI-exposed position, the question is specific: does this business earn AI revenue from capex cycles or embedded adoption, and does its current valuation reflect realistic monetisation or a narrative premium?

The divergence between hardware and software names is not a verdict on AI itself. It is the market identifying which part of the AI value chain is in the monetisation phase and which is in a valuation digestion period. Both phases are normal. What matters is positioning correctly for the one you are in.

The legacy software repricing already underway complicates the straightforward rotation argument: the $2 trillion in US software market wealth destruction in early 2026 fell heaviest on per-seat licensing models, confirming that AI exposure in software is not uniformly positive and that capital is migrating toward consumption-based and infrastructure-adjacent positions rather than the software category broadly.

The variable that determines whether semiconductor names re-enter leadership is hyperscaler capex guidance in the second half of 2026, particularly any signals of acceleration beyond current plans. Until that evidence arrives, the chip trade is likely range-bound while software and platform names carry the AI theme forward.

Staying in the AI trade is reasonable. But the allocation within it now carries more consequence than it did twelve months ago. The question is no longer whether to own AI exposure. It is whether the AI exposure you own is the kind that compounds from here, or the kind still waiting for the next capex signal to justify its price.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI hardware stocks (semiconductors, chip manufacturers) earn revenue directly from hyperscaler capital expenditure cycles, making them lumpy and cyclically exposed. AI software stocks embed AI into recurring enterprise products, earning adoption-diffused revenue at gross margins of 70-80% or higher, with far less sensitivity to any single capex decision.

The SOXX fell roughly 10% not because AI demand collapsed but because valuations had already priced in near-linear growth for years ahead. Broadcom's 15% drop after merely confirming its guidance showed the problem was embedded expectations, not the underlying business.

Hyperscaler capex guidance from AWS, Azure, Google Cloud, Meta, and Microsoft is the primary signal. Any evidence of acceleration beyond current 2026 plans in the second half of the year would be the clearest catalyst for semiconductor names to re-enter leadership.

Apple embeds AI into consumer devices and services rather than selling training infrastructure, meaning its AI upside comes from an upgrade cycle and services attach across its installed base, with no direct dependency on hyperscaler capex decisions that have been driving chip stock volatility.

The UBS approach in June 2026 illustrates the shift: cut chip and hardware weighting (from roughly 76% to 61%) and increase exposure to software and platform names where AI monetisation is visible but multiples have not yet fully caught up, using earnings-driven rallies as exit windows rather than waiting for negative catalysts.