Why the Fed’s Language Shift Is Driving Dollar Strength

3 hrs ago

The companies absorbing the most media attention in the AI buildout are rarely the ones where the most durable value is being created. The chip designers and model developers command the headlines, the conference keynotes, and the market capitalisation milestones. Yet the binding constraints on AI adoption sit further down the stack, in infrastructure layers that most investors glance past on their way to the obvious names.

There is a reason for that asymmetry, and it is not new. Every major technological revolution of the past two centuries followed a consistent pattern: the investors who understood it early found value not in the headline technology but in the infrastructure resolving its binding constraints. The railroad era, electrification, and the internet buildout each produced their own version of this dynamic.

Here is the framework for identifying where that dynamic is playing out in the current AI cycle, and a structured checklist for evaluating whether a specific infrastructure stock is genuinely positioned at a binding constraint or simply adjacent to one.

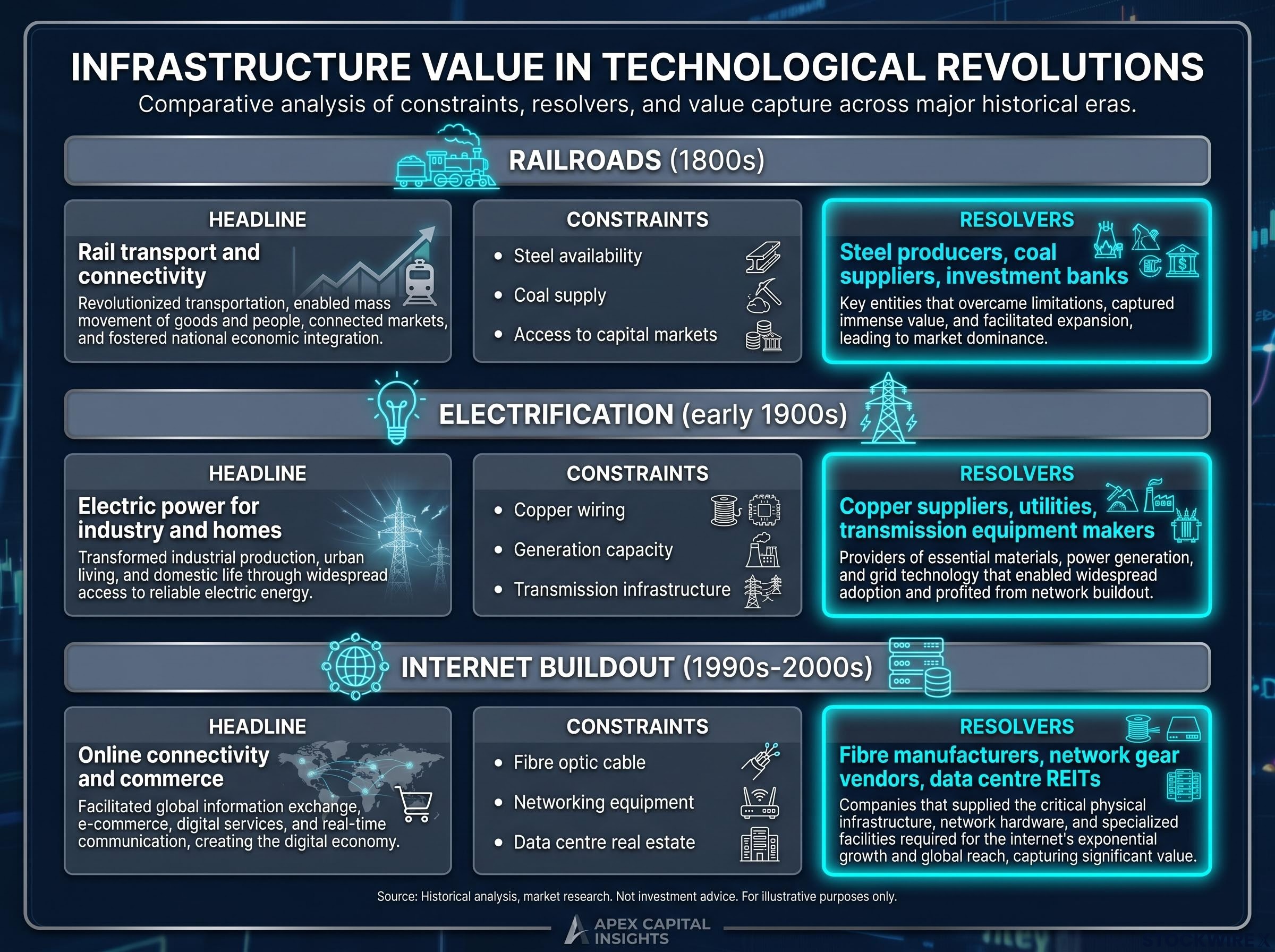

The pattern is remarkably consistent across eras. In each case, a headline technology captured public imagination and investor capital, while the companies resolving the physical and operational constraints on that technology’s adoption built durable, compounding positions.

| Era | Headline Technology | Key Binding Constraints | Constraint-Resolver Categories |

|---|---|---|---|

| Railroads (1800s) | Rail transport and connectivity | Steel availability, coal supply, access to capital markets | Steel producers, coal suppliers, investment banks |

| Electrification (early 1900s) | Electric power for industry and homes | Copper wiring, generation capacity, transmission infrastructure | Copper suppliers, utilities, transmission equipment makers |

| Internet buildout (1990s-2000s) | Online connectivity and commerce | Fibre optic cable, networking equipment, data centre real estate | Fibre manufacturers, network gear vendors, data centre REITs |

None of this was inevitable. Plenty of infrastructure providers in each era failed, overbuilt, or were commoditised before they could capture the value their positioning suggested. The pattern is not “infrastructure always wins.” It is narrower and more useful than that.

Adoption of any transformative technology is gated by its most binding physical or operational constraint. Whoever removes that gate captures value proportional to the scale of adoption. That makes the pattern a reusable lens: identifying where adoption is genuinely gated today tells you where durable value is most likely to concentrate, not which specific company will capture it.

The railroad analogy is not merely rhetorical: roughly three-quarters of historical general-purpose technology booms followed a cycle of massive overinvestment, capital destruction, and then extended productivity growth built on surviving infrastructure, a pattern that the AI bubble history of earlier technology waves traces with uncomfortable precision.

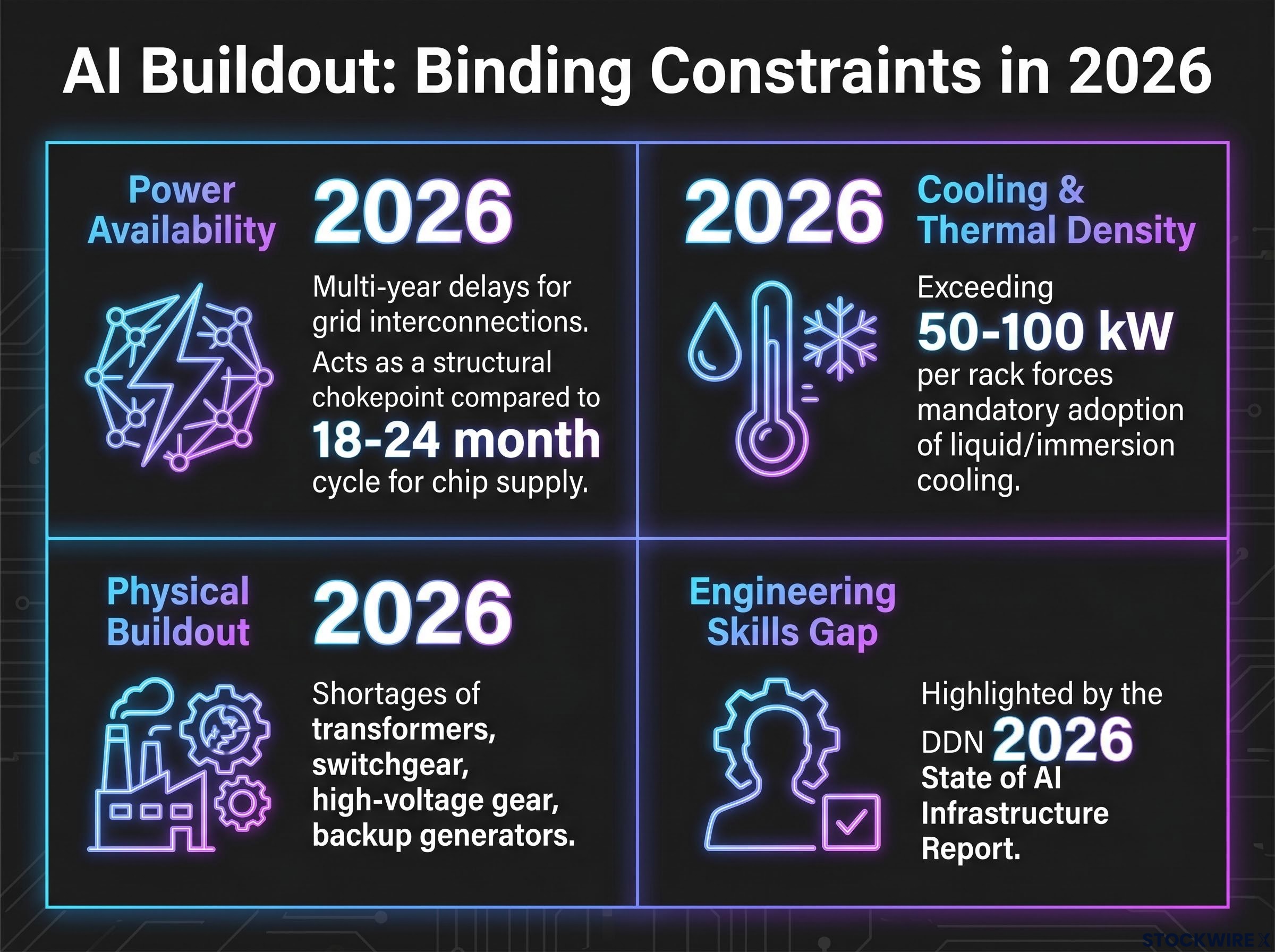

The AI cycle’s bottlenecks are not theoretical. They are already restricting deployment capacity in 2026, shaping where facilities can be built, how quickly they come online, and which operators can compete for new workloads. Four categories stand out.

The multi-year grid interconnection delays utilities are already reporting represent more than a capacity planning problem; the structural grid crisis created by AI energy demand is reshaping where facilities can be built, which operators can compete, and which energy categories attract sovereign-scale capital commitments.

Power is likely the most structurally durable constraint of the four. Chip supply can respond via foundry expansion on a roughly 18-24 month cycle. Grid and transmission upgrades require multi-year regulatory, permitting, and construction timelines. That asymmetry in response time is what positions power at the structural chokepoint.

The investment opportunity in companies resolving these constraints is present-tense, not speculative. The bottlenecks are already binding.

Companies that resolve binding constraints for their customers tend to accumulate competitive advantage in a compounding pattern. Customers become increasingly dependent on integrated workflows. Switching costs rise with each layer of integration. Regulatory barriers and capital scale requirements limit new entrants. This is why infrastructure layers in previous technology cycles produced not just winners but durable franchises.

Contrast that with the headline technology layer, where winner-takes-most dynamics and rapid iteration create higher uncertainty of outcome. The model that leads today may not lead in eighteen months. The chip architecture that dominates this generation may face an architectural challenge in the next.

The focus here is not chip designers or model developers in isolation; the point is to extend the investment aperture across the full infrastructure ecosystem. CoreWeave’s market capitalisation of approximately $55 billion reflects how markets are already attributing significant value to infrastructure enablers. Broadening that aperture is not a dilution of conviction; it is an acknowledgement that durable value in previous technology revolutions spread across the infrastructure stack rather than accruing solely at the headline layer.

The market is already pricing this dynamic in real time: AI infrastructure stocks at the power and optical networking layer have outpaced the Nasdaq-100 in 2026, with niche suppliers like Bloom Energy posting 130% year-over-year revenue growth and returning to profitability after decades of losses, illustrating how constraint-resolving positions can produce returns that headline technology names do not.

CoreWeave operates as a purpose-built, GPU-powered cloud infrastructure provider. The analogy to an early electric utility is structurally precise: just as early utilities enabled factories to access electricity without building their own generators, CoreWeave enables AI labs and enterprises to access GPU compute capacity without constructing dedicated data centres.

What it actually provides goes beyond raw GPU access. CoreWeave offers cluster orchestration, developer tools, tuned networking, and optimised storage, specifically designed for workloads where general-purpose, CPU-centric clouds are insufficient. For organisations developing large language models or AI applications, renting pre-built GPU cluster infrastructure removes a multi-year, capital-intensive buildout process.

CoreWeave’s own operations illustrate the multi-layer infrastructure challenge. Bringing large-scale GPU clusters online means contending with each constraint the framework highlights:

The published analyst consensus puts CoreWeave’s 12-month price target at around $143 per share, which would represent approximately 50% upside from then-current trading levels. This is analyst consensus, not an editorial recommendation.

The risks deserve equal weight. CoreWeave shares lost around 40% of their value across the prior 12-month period, a decline that reflects the significant price swings characteristic of its market position. It is simultaneously a constraint resolver and heavily exposed to the same upstream constraints it helps customers avoid. It competes directly with hyperscalers. Customer concentration and capital discipline are central uncertainties.

CoreWeave illustrates both the opportunity and the complexity of the infrastructure-enabler model. It is useful as a case study precisely because it shows the framework working in practice alongside the risks that remain even when the business model is structurally well-positioned.

The historical framework and the case study give you orientation. These four screening questions give you a practical filter.

The framework identifies where to look. It does not tell you what to buy. History shows infrastructure buildouts produce both spectacular winners and significant losers, and selectivity and valuation discipline remain the primary determinants of outcome even when the framework correctly identifies a structural bottleneck.

| Bottleneck Category | Industry Verticals Positioned at Constraint | Key Evaluation Consideration |

|---|---|---|

| Power | Utilities, IPPs, T&D equipment, grid-scale storage | Multi-year grid interconnection timelines create structural durability |

| Cooling | Liquid cooling vendors, industrial HVAC, data centre REITs | Rack density thresholds force technology adoption, not just preference |

| Compute and networking | Memory, interconnects, networking switches, optical components | Chip supply can expand faster than grid capacity, reducing constraint durability |

| Skills and complexity | MLOps, orchestration, managed services, observability tools | Deepening customer integrations vs. substitutable tooling |

The railroad playbook identifies where to look, not what to buy. That distinction is the difference between a useful investment framework and a dangerous one. Infrastructure buildouts have historically produced overbuilding, commoditisation, regulatory capture, and capital misallocation alongside the genuine winners. The current AI cycle will not be exempt from any of these risks.

The constraints most worth monitoring through the second half of 2026 and beyond are power and grid interconnection timelines, cooling density thresholds in new facility design, and the degree to which orchestration and MLOps platforms deepen customer integrations rather than remaining substitutable. These are the pressure points where the binding-constraint thesis faces its most direct real-world tests.

Translating the bottleneck framework into a portfolio structure requires a view on how to weight the hardware, cloud, and software layers against each other; a three-tier AI infrastructure allocation approach, spanning roughly 50% hardware, 40% cloud, and 10% software, reflects both the capital concentration at the physical layer and the different risk profiles each tier carries in the current cycle.

The framework is a starting point for diligence, not a substitute for it. Historical analogies carry no guarantee that equivalent outcomes will follow, and financial projections for companies positioned at structural chokepoints are subject to prevailing market conditions and competitive dynamics that can shift materially. Readers should conduct independent research and seek guidance from qualified financial professionals before making any investment decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

AI infrastructure stocks are shares in companies that provide the physical and operational layers required for AI deployment, including power and grid infrastructure, liquid cooling systems, GPU cloud platforms, networking equipment, and orchestration software, rather than the AI models or chips themselves.

Roughly three-quarters of historical general-purpose technology booms followed a cycle of overinvestment, capital destruction, and then extended productivity growth built on surviving infrastructure; the railroad playbook identifies that the companies resolving the binding physical constraints on a new technology's adoption, not the headline technology providers, tend to build the most durable franchises.

Power availability is the most structurally durable constraint, with utilities reporting multi-year grid interconnection delays; cooling density is a close second, as rack power exceeding 50-100 kW per rack forces liquid or immersion cooling adoption, while transformer and switchgear shortages and engineering skills gaps add further friction.

The four-question checklist in the article focuses on whether the company resolves a constraint that is actually gating deployment, what protects that position from commoditisation (regulation, scale, IP, or switching costs), whether customer integrations are deepening over time, and whether incremental capital earns defensible returns rather than simply adding capacity to a future price war.

CoreWeave is a purpose-built, GPU-powered cloud infrastructure provider that enables AI labs and enterprises to access large-scale GPU compute capacity without building their own data centres; it is used as a case study because it illustrates how an infrastructure enabler can sit at multiple binding constraints simultaneously, while also demonstrating the risks, including a roughly 40% share price decline over the prior 12 months, that remain even for structurally well-positioned businesses.