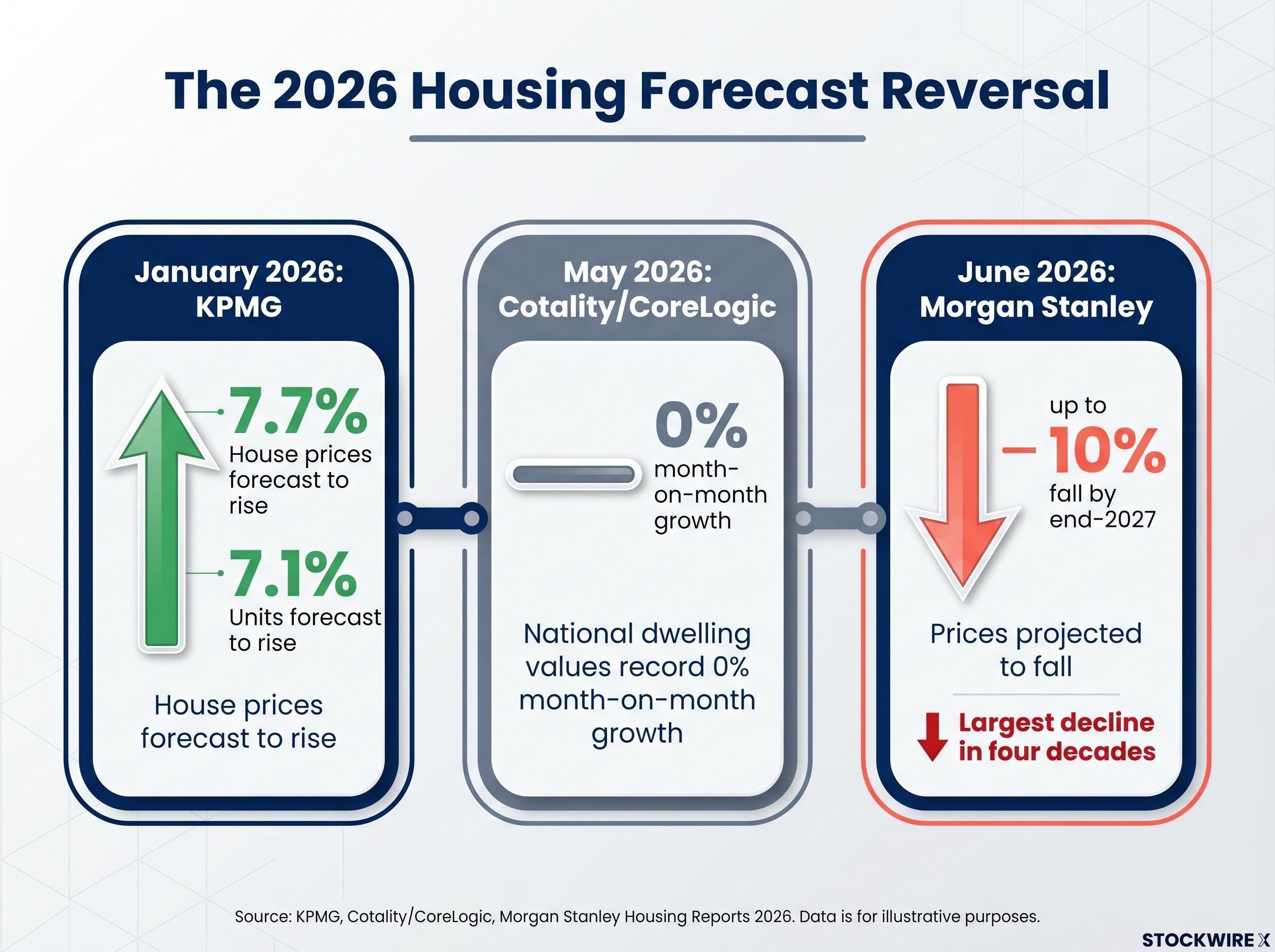

As recently as January 2026, KPMG was forecasting Australian house prices would rise 7.7% through the year. By June 2026, Morgan Stanley was projecting a fall of up to 10% by the end of 2027, potentially the largest decline in four decades.

The shift in outlook has been rapid. Three RBA rate hikes in 2026 alone, flat dwelling values in May 2026 (per Cotality/CoreLogic), falling auction clearance rates, and a Federal Budget targeting property investor concessions have converged into a compounding pressure sequence. Together, these forces represent more than a housing story. They represent a direct threat to the earnings base of Australia’s largest listed banks.

What follows traces the specific channels through which property stress translates into slower lending growth, margin compression, rising bad debts, and earnings downgrades for ASX bank investors, and where the structural limits on that thesis lie.

Morgan Stanley’s forecast signals a decisive shift in housing momentum

In January 2026, KPMG’s Residential Property Market Outlook projected national house prices rising 7.7% and units rising 7.1% through the year. Five months later, Morgan Stanley analyst Richard Wiles issued a forecast projecting residential prices could fall by up to 10% by the close of 2027.

Morgan Stanley described this potential decline as the largest in four decades for Australian residential property, a characterisation that reframes the sector’s risk profile for bank investors.

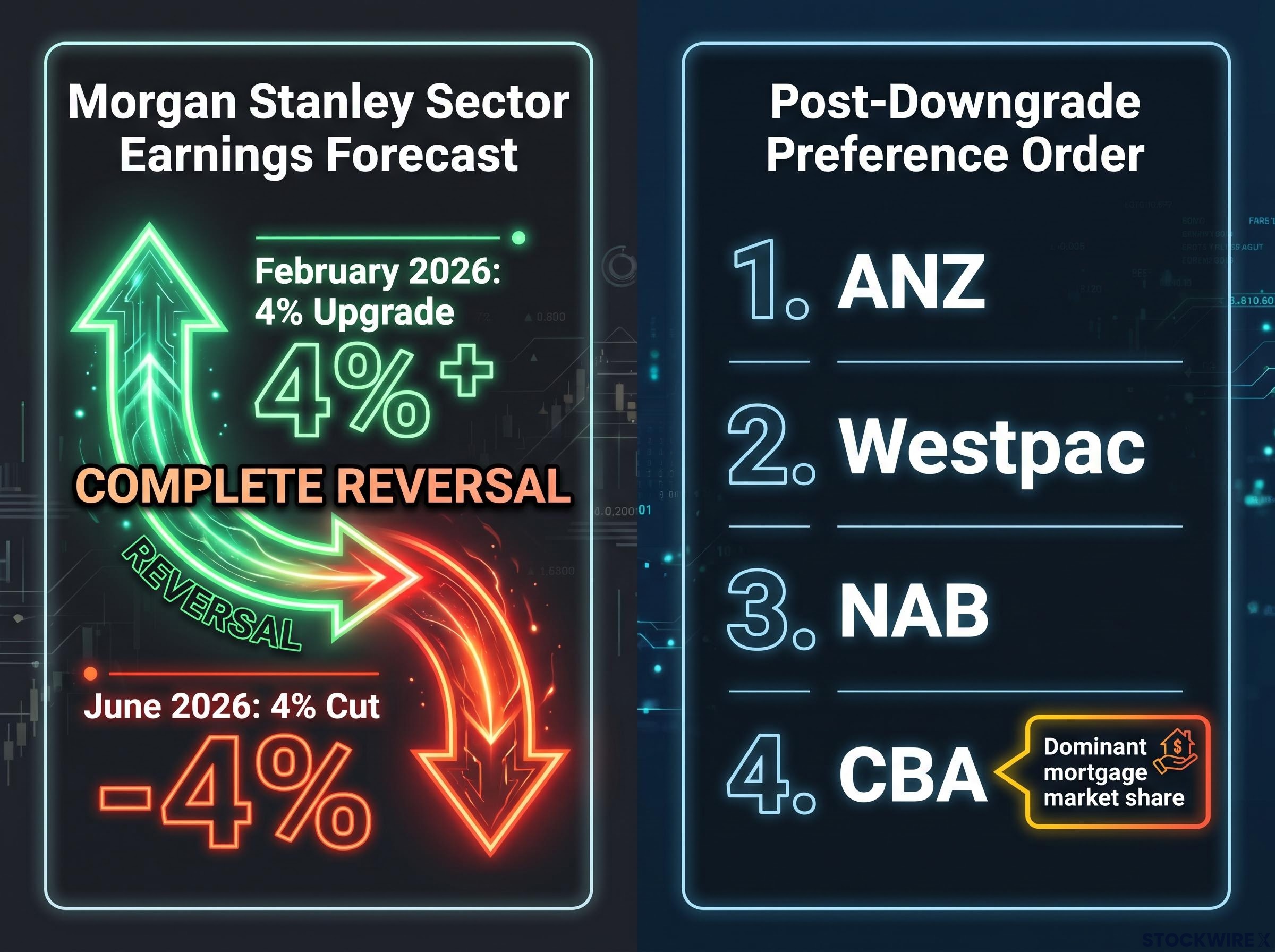

The reversal was not incremental. Wiles had issued a 4% earnings upgrade across the major ASX banks in February 2026. By June 2026, he reversed it entirely, cutting sector earnings forecasts by an equivalent 4% and lowering price targets. This was a complete recalibration, not a marginal adjustment.

The headline numbers capture the speed of the shift:

- KPMG (January 2026): National house prices forecast to rise 7.7%

- Morgan Stanley (June 2026): Residential prices projected to fall up to 10% by end-2027

- Cotality/CoreLogic (May 2026): National dwelling values recorded 0% month-on-month growth

Investors who anchored to early-2026 consensus outlooks are now operating with a materially different risk landscape. The speed of the forecast reversal matters as much as the magnitude.

When big ASX news breaks, our subscribers know first

How three rate hikes in five months became the primary catalyst

The RBA delivered three consecutive 25-basis-point hikes across the first five months of 2026, bringing the cash rate to 4.35% as of 6 May 2026. This unwound prior easing and reintroduced tightening at a point in the cycle where household buffers had already been substantially drawn down.

The cumulative weight of those decisions, rather than any single hike, is what shifted the outlook. Each increase compounded borrower stress on a base where mortgage serviceability was already stretched:

The third consecutive tightening move delivered the cash rate to 4.35% on 5 May 2026, with eight of nine Board members voting in favour, a margin that understates how close the threshold between hiking and holding had become by that meeting.

- First hike (early 2026): Reversed the trajectory of the prior easing cycle, signalling the RBA’s willingness to tighten again

- Second hike: Pushed repayment obligations above the levels many borrowers had budgeted for under the assumption rates were heading lower

- Third hike (effective 6 May 2026): Brought the cash rate to 4.35%, with the cumulative 0.75% increase in five months erasing the relief delivered by earlier cuts

The next RBA meeting was scheduled for 16 June 2026, with futures pricing at the time of the downgrade suggesting no immediate further change.

From rate decisions to lending volume: the direct line to bank revenue

Higher rates reduce borrower capacity mechanically. Each rate increase shrinks the loan amount a borrower qualifies for, which compresses new origination volumes even before any increase in defaults or arrears appears.

Morgan Stanley projected mortgage growth would decelerate from approximately 7.5% to 3-4% on a forward basis. Mortgage lending is the primary revenue driver for Australia’s major banks. A deceleration of that magnitude is not a slowdown; it is a structural repricing of lending volumes, with direct consequences for revenue forecasts even if credit quality remains stable.

The transmission channels from falling prices to bank balance sheets

A property price decline does not appear on a bank’s income statement in a single quarter. It arrives through a sequence of interconnected channels, each amplifying the next. Understanding these transmission mechanisms allows investors to read housing data releases as lead indicators for bank earnings, not just property market news.

A loan-to-value ratio (LVR) measures the size of a mortgage relative to the value of the property securing it. As property prices fall, LVRs rise automatically, even if the borrower has made every repayment on time. When an LVR exceeds 100%, the borrower is in negative equity, meaning their loan balance exceeds what their property is worth, which constrains refinancing options and elevates default risk.

The National Housing Supply and Affordability Council’s 2024 report documented that borrower affordability and resilience were already constrained before the 2026 rate cycle accelerated, meaning the buffer available to absorb further deterioration was thinner than it would be in a cycle starting from a position of strength.

The National Housing Supply and Affordability Council’s 2024 report found that borrower affordability and resilience were already constrained before the 2026 rate cycle accelerated. That pre-existing stress means the buffer available to absorb further deterioration was thinner than it would be in a cycle starting from a position of strength.

The following table traces each transmission channel from property price decline to its impact on bank earnings:

| Transmission Channel | Mechanism | Bank Earnings Impact |

|---|---|---|

| Rising LVRs | Falling property values increase loan-to-value ratios on existing mortgages | Higher risk-weighted assets, increased capital requirements |

| Negative equity | Borrowers whose loans exceed property values lose refinancing options | Elevated default probability, constrained portfolio mobility |

| Elevated arrears | Financial stress drives higher rates of missed mortgage repayments | Rising bad debt charges on income statements |

| Higher impairment charges | Banks increase provisions against anticipated loan losses | Direct reduction in reported earnings |

| Slower credit growth | Weaker housing conditions reduce demand for new mortgages | Lower lending volume growth compresses revenue |

| Weaker capital generation | Earnings pressure and higher risk weights reduce organic capital accumulation | Reduced capacity for dividends, buybacks, or balance sheet growth |

These channels operate sequentially and can reinforce each other. Rising LVRs feed negative equity, which feeds arrears, which feeds impairment charges, which weakens capital generation. The compounding nature of this sequence is what makes housing the single most consequential variable for ASX bank earnings.

Net interest margin compression emerged as the most consequential earnings miss of the May 2026 reporting season, driven by deposit competition and mortgage refinancing pressure squeezing margins from both sides simultaneously, a dynamic that was visible in share price declines of between 7% and 14% across the Big Four before the full housing cycle deterioration had materialised.

Policy headwinds add a second layer of structural pressure

The rate cycle alone would have been sufficient to shift the outlook. Federal Budget changes to negative gearing on residential dwellings added a second, structurally distinct source of pressure.

Negative gearing allows property investors to offset rental losses against their taxable income. Reducing or restricting this concession dampens the after-tax return on investment property, which in turn reduces investor demand for residential dwellings. Unlike rate hikes, which are cyclical and reversible, policy changes to tax concessions represent a structural shift in the incentive framework for property investment.

The 2026 Federal Budget negative gearing reforms limit the concession to new residential properties from July 2027 for properties purchased after 12 May 2026, a structural change that directly reduces the after-tax return on established investment property and underpins the investor withdrawal Morgan Stanley’s channel checks identified.

Morgan Stanley’s channel checks identified observable early indicators that these pressures were already translating into changed behaviour:

- Declining auction clearance rates across capital cities

- Property investors stepping back from the market

- New development approvals being paused

- Downward revision of price expectations among sellers and developers

Capital has simultaneously been rotating away from ASX bank shares and toward mining companies such as BHP, driven by surging commodity prices. This investor rotation adds a valuation headwind for bank shares that compounds the fundamental earnings pressure from housing weakness.

The convergence of cyclical rate pressure and structural policy change is what distinguishes this period from prior housing slowdowns where only one force was operating at a time. Investors tracking ASX banks face headwinds arriving from multiple directions simultaneously.

Bank earnings compression during May 2026 reflected all three forces operating simultaneously: the rapid re-hiking cycle, an energy price shock flowing through construction and services costs, and Federal Budget property measures that structurally reduced after-tax investor returns, with the major banks collectively building approximately $800 million in additional loan loss provisions across the most recent reporting season.

The structural floor: why supply shortages complicate the bearish case

The bearish case is well supported, but it is not the only case. Three structural factors provide a floor that limits the severity of any correction and explains why Morgan Stanley’s projection is framed as “up to 10%” rather than a base case certainty.

- Chronic undersupply of housing stock: Both KPMG and the National Housing Supply and Affordability Council have identified persistent supply shortages as a structural feature of the Australian housing market, with the Council projecting an extended period of undersupply that restricts the scope for a severe price collapse

- Rental market tightness: A tight rental market sustains investor interest in residential property by supporting rental yields, even as policy changes to negative gearing reduce the tax-driven component of returns

- Expanded 5% Deposit Scheme: KPMG cited the broadened scheme as a demand-side support factor, expanding first-home buyer access and sustaining transaction volumes at the entry level of the market

These factors do not invalidate the bearish thesis. They define its boundary conditions. A reader who absorbs only the headwinds holds an incomplete picture; the structural supply argument is the reason a correction of this magnitude would find resistance before reaching the severity of a free fall.

What the downgrade means for ASX bank investors tracking this cycle

Morgan Stanley’s post-downgrade preference order ranks ANZ first, followed by Westpac, NAB, and CBA last. The ordering reflects differential exposure to the housing cycle, with CBA’s dominant mortgage market share positioning it as the most directly affected if housing conditions deteriorate as projected.

The broker anticipates further earnings downgrades and continued valuation de-rating across the sector over the 12 months from June 2026 if housing conditions evolve in line with its projections.

Four data signals to monitor as the housing cycle unfolds

The following indicators serve as lead signals for further bank earnings pressure, listed in order of reporting frequency:

- Monthly Cotality/CoreLogic dwelling value readings: Published monthly, these provide the most timely measure of property price direction and momentum shifts

- Auction clearance rates: Published weekly, these function as a real-time demand signal that tends to lead price movements by several months

- RBA meeting outcomes: Scheduled approximately every six weeks (next meeting 16 June 2026), each decision recalibrates borrower capacity and lending volume projections

- Loan arrears data: Published quarterly by the major banks and APRA, arrears trends provide the earliest direct evidence of borrower stress translating into credit losses

Housing market data is not real estate news for ASX bank investors. It is a leading indicator for the earnings cycle of the sector that constitutes a significant share of the ASX 200.

The housing risk premium is not yet fully priced into bank valuations

The convergence of three consecutive rate hikes, structural policy changes to negative gearing, and observable deterioration in auction clearance rates and investor sentiment has shifted the Australian housing market from a tailwind to a headwind for bank earnings with unusual speed. Morgan Stanley’s 4% earnings cut and preference reordering are the first institutional response to that shift; they may not be the last.

The uncertainty range remains wide. A decline of “up to 10%” by end-2027 is a risk scenario, not a certainty, and the structural supply supports documented by the National Housing Supply and Affordability Council and KPMG provide genuine friction against the most severe outcomes.

Broader household stress visible in consumer confidence falling to its weakest level since 1973 and corporate insolvencies hitting an all-time record in 2025 suggests the conditions feeding bank credit risk extend beyond the housing channel alone, with per capita GDP growth of just 0.4% in Q4 2025 confirming that aggregate figures have been masking individual-level deterioration throughout the current rate cycle.

What is not in dispute is the direction of the change. The Australian housing market is now the single most significant macro variable for bank investors to monitor over the 2026-2027 period, and the gap between where consensus stood in January and where it stands in June is as wide as any in four decades.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.