Australia’s Big Four banks shed between 7% and 14% of their share value in May 2026 alone, making the sector one of the worst performers on the ASX in a period that was supposed to mark a return to earnings stability. The sell-off arrived as reporting season concluded, meaning investors are now digesting a simultaneous combination of below-expectation margin results, an $800 million sector-wide provision build, capital disappointments at two of the four banks, and a Morgan Stanley downgrade that reversed a 4% forecast upgrade made only three months earlier.

Each of these developments would have been significant in isolation. Occurring together, they have reset sentiment across ASX bank shares sharply. This article explains what drove the declines at each bank, what the analyst community is saying about the earnings outlook, and what retail investors should be monitoring in the weeks ahead.

How far ASX bank shares have fallen, and which banks were hit hardest

The numbers tell a story that goes beyond a routine sector rotation. All four major banks have posted steep month-to-date declines through May 2026, with NAB bearing the heaviest losses at roughly 14% over the period, more than double the drawdown at ANZ.

| Bank (ASX Code) | Intraday Move | Month-to-Date | 12-Month Change |

|---|---|---|---|

| CBA (CBA) | ~0.71% lower to $161.73 | ~9% decline | ~6% lower |

| WBC (WBC) | ~1% lower to $36.02 | ~9% decline | — |

| NAB (NAB) | ~1% lower to $36.73 | ~14% decline | — |

| ANZ (ANZ) | ~1% lower to $35.31 | ~7% decline | ~22% gain; ~3% lower YTD 2026 |

NAB’s roughly 14% monthly decline stands as the steepest fall across the sector, signalling stock-specific problems layered on top of the broader headwinds hitting all four banks.

CBA remains the sector heavyweight with a market capitalisation of approximately $270.65 billion, yet even the most defensive name on the ASX has not been spared. ANZ’s comparatively smaller 7% drawdown reflects its stronger capital position and buyback capacity, though the bank is still roughly 3% lower for the 2026 calendar year despite a 22% gain over the trailing twelve months.

The scale of May’s drawdown becomes clearer when placed against the preceding run-up: the ASX bank shares rally through April 2026 had pushed three of the four majors into positive year-to-date territory even as analyst consensus remained almost uniformly bearish, with all 14 covering analysts rating CBA a sell and an average price target implying roughly 25% downside from late April levels.

When big ASX news breaks, our subscribers know first

What the reporting season actually revealed about earnings quality

The sell-off did not emerge from a single headline miss. It built across a sequence of disappointments that, taken together, amounted to a comprehensive downgrade of the near-term earnings picture:

- Net interest margin underperformance: Margins came in below market expectations across all four banks, despite the RBA’s cash rate holding at 4.35%

- $800 million collective provision build: The majors collectively added approximately $800 million to loan loss buffers during the reporting period, reflecting precautionary macro caution rather than observed default spikes

- Capital shortfalls at CBA and NAB: Capital results at both banks landed below market forecasts, with NAB raising approximately $1.8 billion via its dividend reinvestment plan to bolster its position

- Dividend guidance reset: Three of the four banks guided payout ratios toward the midpoint of target ranges, cooling expectations for dividend growth

The margin miss was the most consequential. Banks had entered reporting season with consensus expectations that elevated rates would continue supporting earnings. Instead, competitive pressures on both sides of the balance sheet, deposits and mortgages, proved more intense than forecast.

Dividends and capital: what management actually said

CBA adopted what it described as a “prudent but progressive” dividend stance, signalling comfort with current capital levels but stopping short of committing to larger returns. NAB was more cautious still, flagging a conservative posture following its softer capital outcome and prioritising balance sheet strength over buybacks.

Westpac expressed confidence in sustaining current dividend settings while noting competing demands from investment in risk, compliance, and technology. ANZ, the most constructive of the four, indicated capacity for continued dividends and potential buybacks, though it emphasised the need for flexibility given macro uncertainty. None of the four banks committed to meaningful payout increases.

Why margins are under pressure even with rates on hold

A common assumption among retail investors is that higher interest rates are unambiguously positive for bank profits. The logic seems straightforward: banks earn more on the loans they issue. In practice, the relationship is more complicated, and the current Australian environment illustrates exactly why.

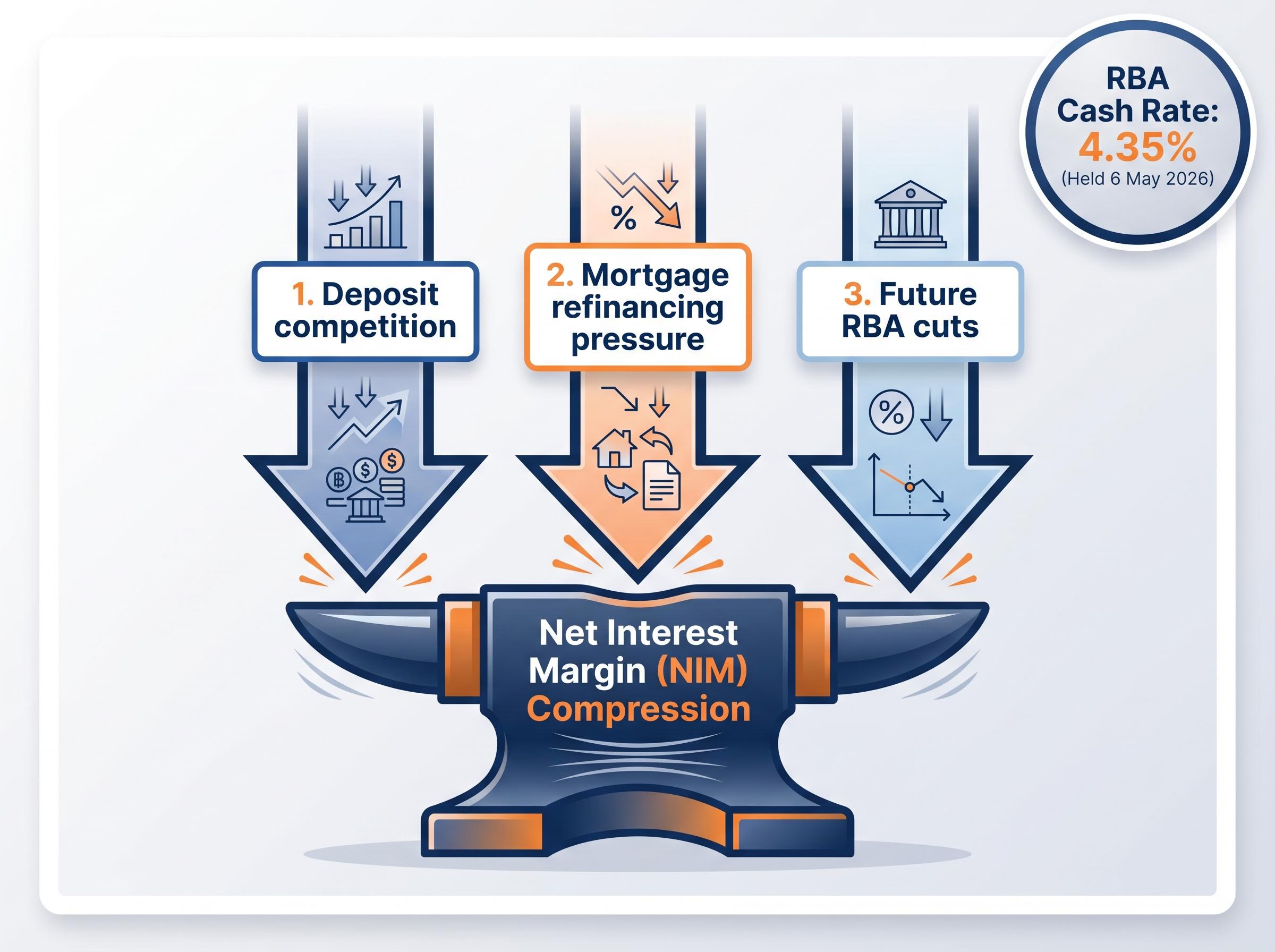

Net interest margin (NIM) is the gap between what a bank earns on its loans and what it pays on deposits. It is the single largest profit driver for all four majors. When that gap widens, earnings grow. When it compresses, profits come under pressure regardless of loan volumes.

Banks are “caught between a still-elevated cash rate and slowing credit growth,” limiting the upside from high rates.

Three specific mechanisms are compressing margins right now:

- Deposit competition: Even with the RBA cash rate at 4.35% (held at the 6 May 2026 board meeting), banks are offering increasingly competitive term deposit rates to retain and attract funding. This raises the cost side of the NIM equation.

- Mortgage refinancing pressure: As fixed-rate loans originated during the low-rate era roll off, borrowers are refinancing at intensely competitive variable rates, compressing margins from the asset side.

- Future RBA cuts: The RBA characterised its current stance as “restrictive” with a data-dependent posture. The next decision is scheduled for 16 June 2026. An eventual rate cut cycle would likely further compress NIMs if mortgage rates fall faster than deposit costs adjust.

The RBA’s May 2026 monetary policy decision confirmed the cash rate target at 4.35% while characterising the current stance as restrictive and signalling a data-dependent approach to future adjustments, setting the stage for the NIM pressure banks are now navigating.

Analysts see incremental NIM pressure persisting into FY27 as fixed-rate rollovers continue.

For investors wanting to stress-test whether the sector’s current earnings profile holds up under different rate scenarios, our dedicated guide to NIM compression and provisioning risk walks through the specific funding composition differences across CBA, ANZ, and NAB, including ANZ’s 30% wholesale funding exposure versus CBA’s 26%, and explains how even a 15-20 basis point NIM move can materially reduce major bank net profit and dividend capacity.

How analysts have responded: downgrades, target cuts, and the Morgan Stanley reversal

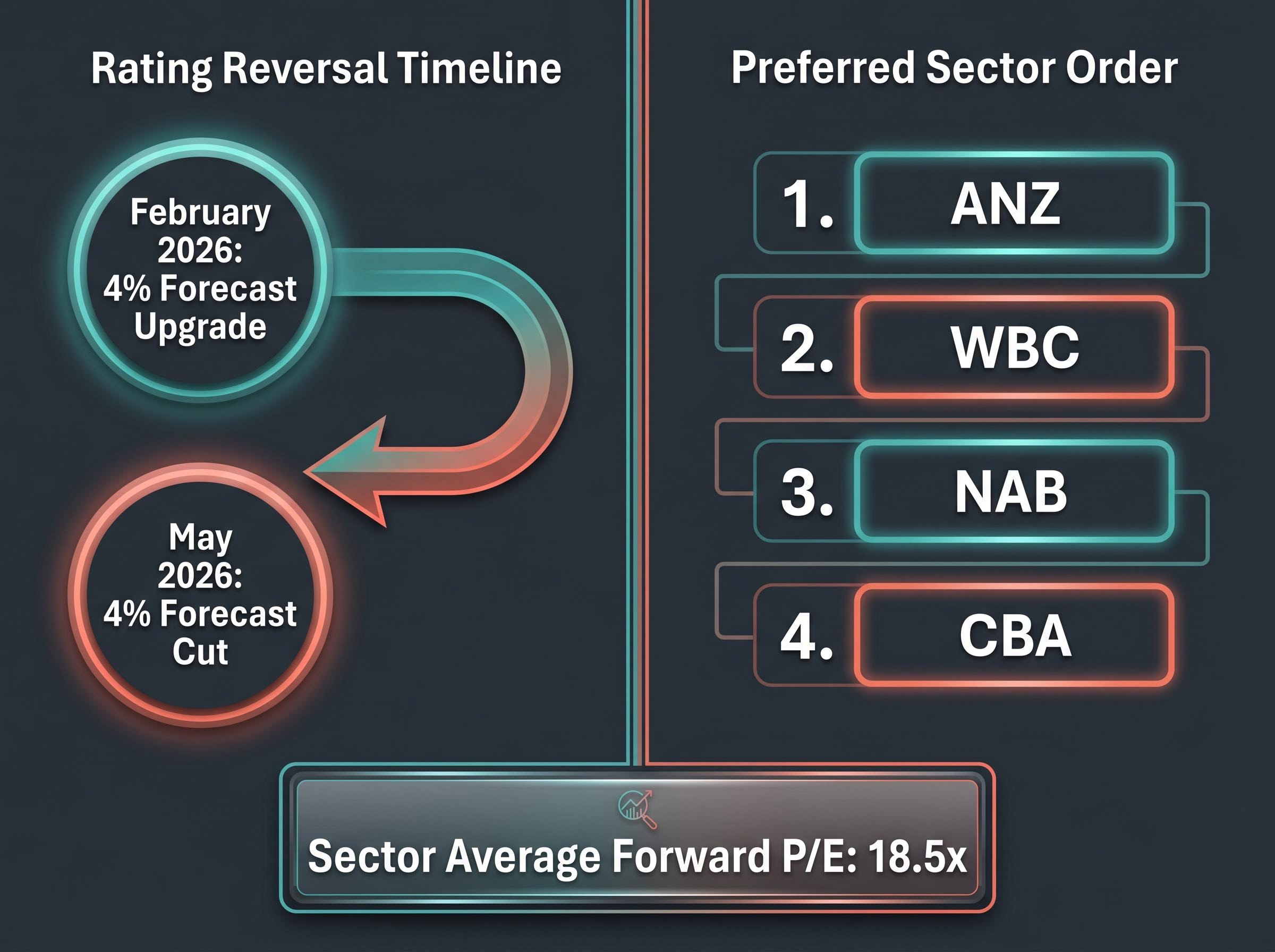

Morgan Stanley analyst Richard Wiles had upgraded sector earnings forecasts by 4% in February 2026. By May, that upgrade was fully unwound. Wiles cited a deterioration in operating conditions that moved faster than anticipated, cutting forecasts by a comparable 4% and noting the sector’s average forward price-to-earnings ratio of 18.5 times on a 12-month basis still has room to contract.

The reversal carries weight because it represents the fastest round-trip in analyst sentiment seen in this cycle. Morgan Stanley’s preferred sector order now runs ANZ first, followed by WBC, NAB, and CBA last.

The broader broker community moved in the same direction. EPS forecast cuts of 1-5% were applied across all four majors, with Neutral ratings dominating.

| Broker | EPS Cut Range | Key Concern | Rating Stance |

|---|---|---|---|

| UBS | ~2-3% | Margin pressure, higher funding costs | Neutral |

| Goldman Sachs | ~5% (NAB) | NAB premium multiple stretched; CBA downside risk | Neutral |

| Macquarie | ~1-2% | Mortgage competition, term deposit pricing | Neutral |

| Jarden | <2% (CBA) | NIM and credit impairment assumptions raised | Hold |

| Morgan Stanley | ~4% reversal | Operating conditions deteriorated faster than expected | Sector order: ANZ, WBC, NAB, CBA |

Goldman Sachs on NAB: “NAB’s premium multiple looks stretched given earnings downgrades and higher provisioning.”

Jarden was slightly more constructive on ANZ, citing capital flexibility, while flagging CBA for downside risk if NIM compression persists.

The macro headwinds compounding the sector’s problems

The banks are not navigating a single headwind. Three concurrent macro pressures are arriving simultaneously:

- Monetary policy tightening: Three RBA rate increases have created cumulative pressure on borrowers, lifting arrears from cyclical lows and constraining credit demand

- Federal budget property tax proposals: Potential changes to negative gearing or capital gains tax concessions for property investors, along with adjustments to vacant property and foreign owner surcharges, could moderate investor loan demand over time. Exact legislative detail remains subject to consultation and parliamentary process.

- Global energy price shock: Analysts have flagged an energy price shock as an additional operating environment headwind, adding to input cost pressures across the economy

Brokers have characterised the budget measures as “incremental negatives” and “second-order” relative to the larger earnings drivers of NIM compression, funding costs, and competition. The measures are unlikely to move quickly through parliament, meaning their full impact would develop over years rather than quarters.

The compounding effect matters most. Slowing credit growth intersects with margin compression to squeeze revenue from both sides: lower volumes and lower margins at the same time.

What investors should be watching before the next RBA decision

The diagnosis is now clear. What matters next is whether conditions stabilise or deteriorate further. Three specific signals deserve active monitoring:

- The 16 June 2026 RBA decision: A rate cut would likely accelerate NIM compression as mortgage pricing falls. A hold maintains current pressure without resolution. Either outcome carries earnings implications for the sector.

- Management commentary on arrears and provisioning: Arrears across the sector have been described as up off a low base but not flashing systemic stress. Any management updates indicating the $800 million provision build needs to be extended would signal deteriorating credit conditions beyond what has already been priced.

- Valuation multiple trajectory: The sector’s average forward P/E of 18.5 times remains elevated by historical standards. Morgan Stanley’s Wiles sees additional contraction potential, with CBA’s premium multiple the most exposed to further de-rating given it trades at a full premium to peers.

Forward P/E multiples clustering around 18.5 times across the sector can create a misleading impression of consistency, because NIM trajectory, regulatory exposure, and management execution vary considerably between the four names; investors relying on a single earnings multiple to compare CBA against ANZ risk missing the qualitative factors that have historically driven the widest gaps in long-term relative returns.

Morgan Stanley’s assessment is that the 18.5 times forward P/E “still has room to contract further.”

Morgan Stanley’s preferred positioning order, ANZ first and CBA last, offers one framework for investors weighing relative exposure within the sector.

The sector remains profitable, but the easy money has been made

All four banks remain highly profitable institutions operating above APRA’s unquestionably strong CET1 benchmarks. The current sell-off reflects concerns about earnings trajectory and valuation, not balance sheet distress. Provisioning remains precautionary, and actual loan losses sit well within historical norms.

APRA’s unquestionably strong capital framework sets the CET1 benchmarks that determine whether Australian banks hold sufficient capital buffers, a standard all four majors currently satisfy despite the capital shortfalls observed in the most recent reporting period.

The convergence of NIM compression, cautious provisioning, elevated P/E multiples, and slowing credit growth represents a structural reset in the sector’s earnings profile rather than a temporary disruption. The conditions that produced the prior period of strong returns, expanding margins, low provisions, and generous capital returns, have materially changed.

The Big Four remain among the most profitable companies on the ASX, but premium valuations were priced for better earnings momentum than the reporting season delivered.

For retail investors holding bank shares in superannuation or direct portfolios, the sector now requires active monitoring at current valuations rather than passive confidence in the Big Four’s historical defensive appeal. The banks are not in crisis. But the market is telling investors, clearly and consistently across all four names, that the easy money has been made.

For readers wanting to move from monitoring these signals to systematically evaluating each bank’s position, our comprehensive walkthrough of ASX bank due diligence covers a six-check framework spanning ROE versus cost of equity, price-to-book against forward ROE, NIM sensitivity, arrears trends, CET1 ratios, and deposit share, all using publicly available data from ASX results announcements, APRA quarterly statistics, and RBA Financial Stability Reviews.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.