Australia’s consumer confidence index just posted its weakest reading since 1973. Diesel has nearly tripled in price since January 2026. The Reserve Bank of Australia (RBA) has raised rates twice in two months. Yet the most recent official gross domestic product (GDP) figures, from late 2025, still show 2.6% annualised growth.

Something does not add up. The gap between backward-looking economic statistics and the lived reality of Australian households has rarely been wider. A confluence of an Iran-linked energy shock, an aggressive rate-tightening cycle, and collapsing business and consumer confidence is producing conditions that economists are explicitly comparing to 1970s stagflation. What follows is an examination of each of these fault lines, why the official data flatters a picture that is deteriorating quickly, and what Australian households and investors should be watching in the weeks ahead.

Why the headline GDP number is misleading Australians right now

Australia’s annualised GDP grew 2.6% in Q4 2025, the strongest pace in nearly three years. On its face, that figure suggests an economy with momentum. The trouble is that headline GDP measures the total size of the pie, not the size of each person’s slice.

When population growth outpaces economic output, the average individual’s share of that output shrinks even as the total expands. This is what economists call a per capita recession, and Australia has been in one for an extended period. The economy is technically growing; the standard of living for the median household is not.

The ABS national accounts for Q4 2025 confirm that while headline GDP grew 2.6% annually, GDP per capita rose only 0.4% in the December quarter, a figure that makes the per capita recession framing precise rather than rhetorical.

The temporal gap compounds the problem. GDP is a backward-looking measure, captured months before publication. More revealing real-time signals tell a different story:

- April Flash Purchasing Managers’ Index (PMI): Recovered to 50.1 from a contractionary 46.6 in March, barely crossing the expansion threshold

- Consumer sentiment (Westpac-Melbourne Institute): Fell 12.5% in April to 80.1, the lowest since the COVID-19 period

- NAB forward orders: Falling, with purchase costs rising simultaneously

April PMI cost inflation reached its highest level since August 2022, signalling that input prices are accelerating even as output barely holds above contraction territory.

The headline GDP figure describes where the economy was. These indicators describe where it is heading.

When big ASX news breaks, our subscribers know first

How the Iran-driven energy shock is hitting Australian household budgets

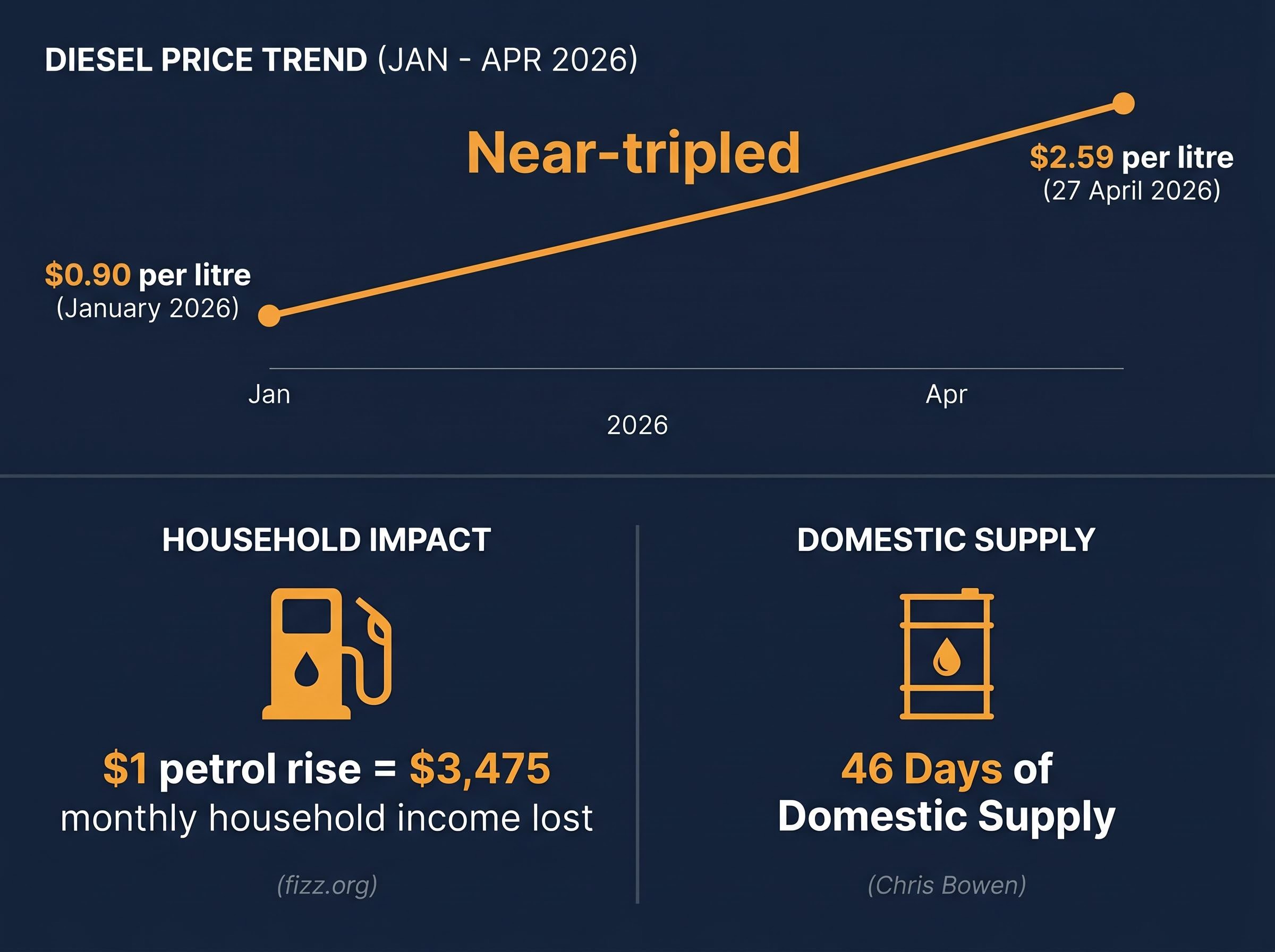

The numbers arrive at the petrol pump first. Australian diesel prices averaged approximately $0.90 per litre in January 2026. By 27 April 2026, that figure had reached $2.59 per litre, a near-tripling driven by the Strait of Hormuz closure triggered by US-Israeli strikes on Iran.

Australia sources approximately 80% of its fuel from overseas. Despite an 8 April ceasefire, maritime disruptions and a US naval blockade continue to suppress normalisation. Crude oil peaked near US$110 per barrel before retreating to approximately US$95 post-ceasefire, a level still well above pre-crisis pricing.

Research from fizz.org found that a $1 rise in petrol prices is equivalent to losing approximately $3,475 in monthly household income, capturing the cascading effect on transport, groceries, and discretionary spending power.

According to Westpac estimates, the fuel shock alone added more than 1 percentage point to headline inflation in March. Energy Minister Chris Bowen’s most recent statement placed Australia’s domestic petrol reserves at just 46 days of supply.

The pass-through extends well beyond the bowser. Fuel is an input cost for nearly everything Australians buy:

| Stage | Impact |

|---|---|

| Diesel price near-triples | Direct transport and logistics costs surge across all freight corridors |

| Fertiliser costs rise | Agricultural input prices increase, lifting farm-gate food prices |

| Food transport costs rise | Supermarket supply chains pass through higher freight charges |

| Grocery and construction prices climb | Households absorb compounding cost increases across multiple budget categories |

The fuel shock is not a single line item. It is an input multiplier rippling through the entire cost structure of Australian daily life.

Electricity and construction cost pressures compound the fuel shock in ways the petrol price headline does not capture: electricity costs rose 25.4% annually after the Energy Bill Relief Fund lapsed, and new dwelling construction costs accelerated to 0.48% month-on-month in March, more than triple February’s pace as oil-derived building materials absorbed the crude price surge.

What stagflation means, and why the RBA cannot simply raise its way out of this

Stagflation occurs when high inflation and weak or contracting economic growth arrive simultaneously. It is the condition central bankers fear most, because the standard tools for fighting one problem make the other worse. Raising interest rates to suppress inflation slows an economy that may already be stalling. Cutting rates to support growth risks entrenching inflation that is already running above target.

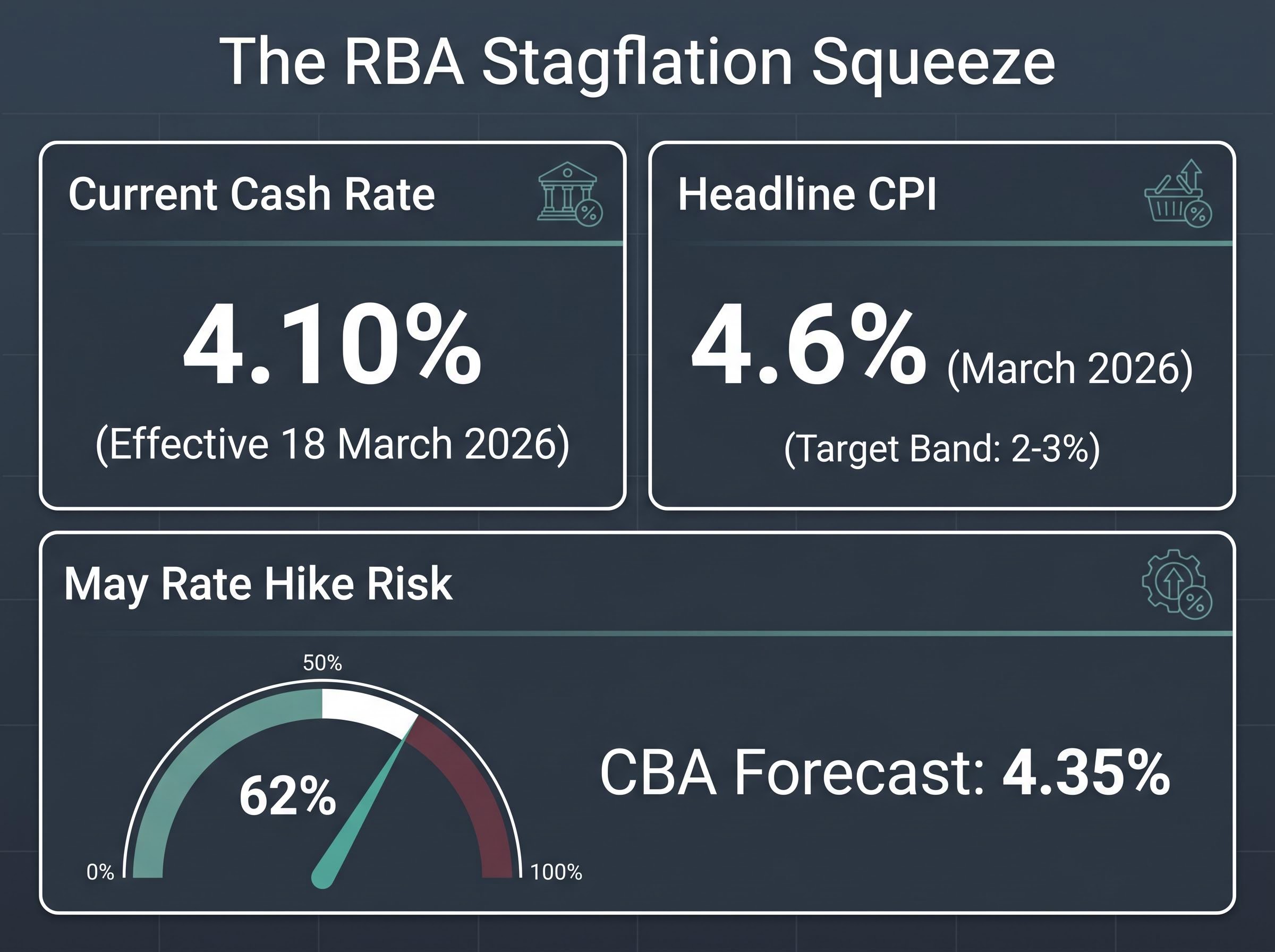

The RBA is living this dilemma in real time. The cash rate stands at 4.10%, effective since 18 March 2026, following two consecutive hikes in February and March. Headline consumer price index (CPI) inflation surged to 4.6% in March 2026, up from 3.7% in February, well above the RBA’s 2-3% target band. Trimmed mean inflation sits at approximately 3.5-4%, also above target.

RBA Deputy Governor Andrew Hauser described navigating stagflation as a “nightmare,” with the bank “feeling its way” through the crisis and uncertain whether rates at 4.10% are sufficient to contain inflation without tipping the economy into recession.

The policy dilemma breaks down into two equally unappealing paths:

- If the RBA hikes further: Higher mortgage repayments deepen the household squeeze, risk accelerating the spending pullback, and could convert a slowdown into a contraction

- If the RBA holds or cuts: Inflation expectations may become entrenched above target, requiring even larger rate increases later and prolonging the period of real wage erosion

Commonwealth Bank forecasts a potential third consecutive hike to 4.35% at the May 4-5 meeting, describing it as a “line-ball” decision. Market pricing assigns a 62% probability to a May rate increase. Every Australian with a variable-rate mortgage or business loan has a direct stake in the outcome.

For investors and mortgage holders trying to parse which CPI number actually drives RBA decisions, our dedicated guide to Australia’s headline versus trimmed mean inflation split examines why the 4.6% headline and the 3.3% trimmed mean tell such different policy stories, and what household inflation expectations reaching 5.9% could mean for second-round wage and price effects.

How deteriorating sentiment is reshaping spending and borrowing behaviour across Australia

The severity of the confidence collapse is difficult to overstate. The Westpac-Melbourne Institute Consumer Sentiment Index fell 12.5% in April to 80.1, its lowest reading since the COVID-19 period.

The ANZ-Roy Morgan Consumer Confidence Survey recorded its weakest result since the survey’s inception in 1973, a benchmark that predates the 1990s recession, the global financial crisis, and the pandemic.

Two complementary surveys arriving at the same conclusion is not coincidence. It is confirmation.

What households are doing differently

The behavioural response is already visible:

- Discretionary spending on clothing and dining has pulled back materially, with retailer share prices reflecting the shift: Nick Scali and Harvey Norman have declined 20-25% over two months

- Buy now, pay later uptake has increased for non-discretionary necessities including utilities, insurance, and healthcare

- Pantry-loading behaviour, echoing early COVID-19 patterns, has re-emerged as households anticipate further price increases

- Household expenditure declined 0.5% in December and remained subdued into 2026

Financial counsellors report mortgage stress as the leading concern at the National Debt Helpline, a signal that the rate hikes are translating directly into household-level distress.

What businesses are doing in response

- The NAB Business Survey recorded a 29-point fall in confidence in March 2026, a collapse that typically precedes hiring freezes, deferred capital expenditure, and reduced operations

- Corporate insolvencies in 2025 set an all-time record, with 2026 projected to match or exceed that level

- Construction sector collapses reached 3,595 in 2025, representing 21% of all national failures and the worst year on record for the sector

- Hospitality insolvencies rose 57% in the 12 months to March 2025

- NAB capacity utilisation has fallen to levels consistent with unemployment above 5%

Record-low confidence is not simply a mood indicator. It is the lead driver of the spending pullback that, if sustained, is the precise mechanism that converts a per capita recession into a technical one.

Labour market and real wages: the quiet erosion hidden beneath low unemployment

Australia’s unemployment rate held at 4.3% in both February and March 2026. That figure, taken in isolation, might suggest a labour market still providing a buffer against recession. The direction of movement tells a different story.

Unemployment has already begun trending higher rather than holding at a stable floor. More critically, the relationship between wages and prices has reversed:

Inflation has exceeded wage growth for the first time in two years as of early 2026, meaning Australian workers are receiving effective pay cuts without any change to their nominal salary. The brief period of real wage recovery has ended.

Three labour market signals, read together, paint a more complete picture than the headline unemployment rate alone:

- Official unemployment (4.3%): Still low by historical standards, but a lagging indicator that has begun moving in the wrong direction

- Real wage growth: Now negative, with inflation outpacing wage increases for the first time since early 2024, eroding purchasing power across all income brackets

- NAB capacity utilisation: Fallen to levels historically consistent with unemployment above 5%, suggesting the official figure understates the degree of softening already underway

CBA data shows households still absorbing higher petrol and utility costs rather than cutting back dramatically, suggesting the full adjustment phase may lie ahead rather than behind. Workers relying on low unemployment as a safety net face a risk that is already materialising through a different channel: the steady erosion of what their pay can actually buy.

What tipping Australia from slowdown into recession would actually look like

The base case: stagnation without a technical recession

The central view among analysts remains an extended period of very low growth rather than outright contraction. Total GDP can remain technically positive while per capita GDP continues to decline, a scenario in which the economy avoids the formal definition of recession while living standards continue to fall. This is the most likely path based on current data.

Three triggers that could push the economy over the edge

Three specific developments could convert the current slowdown into a technical recession, defined as two consecutive quarters of negative GDP growth:

- Renewed Strait of Hormuz deterioration: Any re-escalation of hostilities or further disruption to oil transit routes would push fuel prices higher again, amplifying the inflationary shock and deepening the household spending contraction

- A sharper-than-anticipated consumer spending collapse: Retail sales grew 4.8% year-on-year in February 2026, but that figure preceded the full CPI acceleration to 4.6% in March; a sharp pullback in coming months would remove one of the economy’s remaining supports

- A worse-than-expected employment result: If unemployment rises faster than the gradual trajectory currently anticipated, the feedback loop between job losses, mortgage stress, and reduced spending could accelerate beyond what monetary policy can offset

Belinda Allen at CBA has drawn explicit comparisons to 1970s stagflation dynamics if oil prices persist at current levels. NAB forward orders are falling while purchase costs rise simultaneously, a combination that, according to the Bendigo Bank chief economist, raises the central policy question: whether the oil price shock will critically distort the supply-demand balance or whether the RBA can “look through” it without triggering recession.

Not all analysts accept that rates will remain elevated through mid-2027: oil futures backwardation signals the market views the Hormuz disruption as temporary, and historical supply shock cycles suggest a faster RBA policy pivot may follow within 6-12 months of a shock’s peak, particularly if Oxford Economics modelling of back-to-back GDP contractions in June and September 2026 proves accurate.

Past performance does not guarantee future results. These forward-looking assessments are subject to change based on market developments and geopolitical conditions.

Where this leaves Australian households and what to watch before the May RBA decision

Three forces are converging on Australian household budgets simultaneously: an energy shock that has nearly tripled diesel prices, a rate-tightening cycle that has lifted the cash rate to 4.10% with a potential third hike imminent, and a confidence collapse that is already reshaping spending behaviour. The result is a stagflationary squeeze with no easy policy exit.

The May 4-5 RBA meeting is the next major inflection point. CBA, ANZ, and NAB all project a further hike to 4.35%, and the market assigns a 62% probability to that outcome.

The indicators to monitor before and after the 5 May decision:

- RBA May rate decision: Whether the board delivers a third consecutive hike or pauses, and the language of the accompanying statement

- Strait of Hormuz developments: Any re-escalation or, alternatively, meaningful normalisation of shipping routes that could shift fuel price trajectories

- Next consumer sentiment release: Whether the record-low confidence readings stabilise or deteriorate further

- Labour market data: The next employment release will indicate whether the unemployment rate continues its upward drift toward the 5% level implied by NAB capacity utilisation

The official GDP figures will not tell the story in real time. These indicators will.

For investors who have absorbed the macro picture and want to translate it into portfolio positioning, our deep-dive into stagflation investing strategies for Australian portfolios examines why traditional safe havens are behaving differently in a supply-side shock, which asset classes are benefiting from the current environment, and how high cash buffers, hydrocarbon exporters, and short-duration fixed income fit together in a practical defensive allocation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.