Australia’s capital gains tax regime changed on 12 May 2026. The federal government’s 2026-27 Budget confirmed the replacement of the 50% CGT discount with cost base indexation and a 30% minimum tax on net capital gains, effective 1 July 2027. Public debate has centred on property investors and negative gearing. But for startup founders and early employees who accepted equity instead of competitive salaries, the reform triggers a different problem, one that has received far less scrutiny. Indexation delivers almost no benefit when the original outlay was minimal. The long-term upside that made accepting equity instead of a salary rational has been structurally diminished. What follows is an analysis of the specific financial mechanics behind that asymmetry, what it means for Australia’s capacity to produce new companies of scale, and how comparable reforms in Canada and the United Kingdom have attempted to carve out space for entrepreneurs.

Why indexation sounds fair but maths against founders

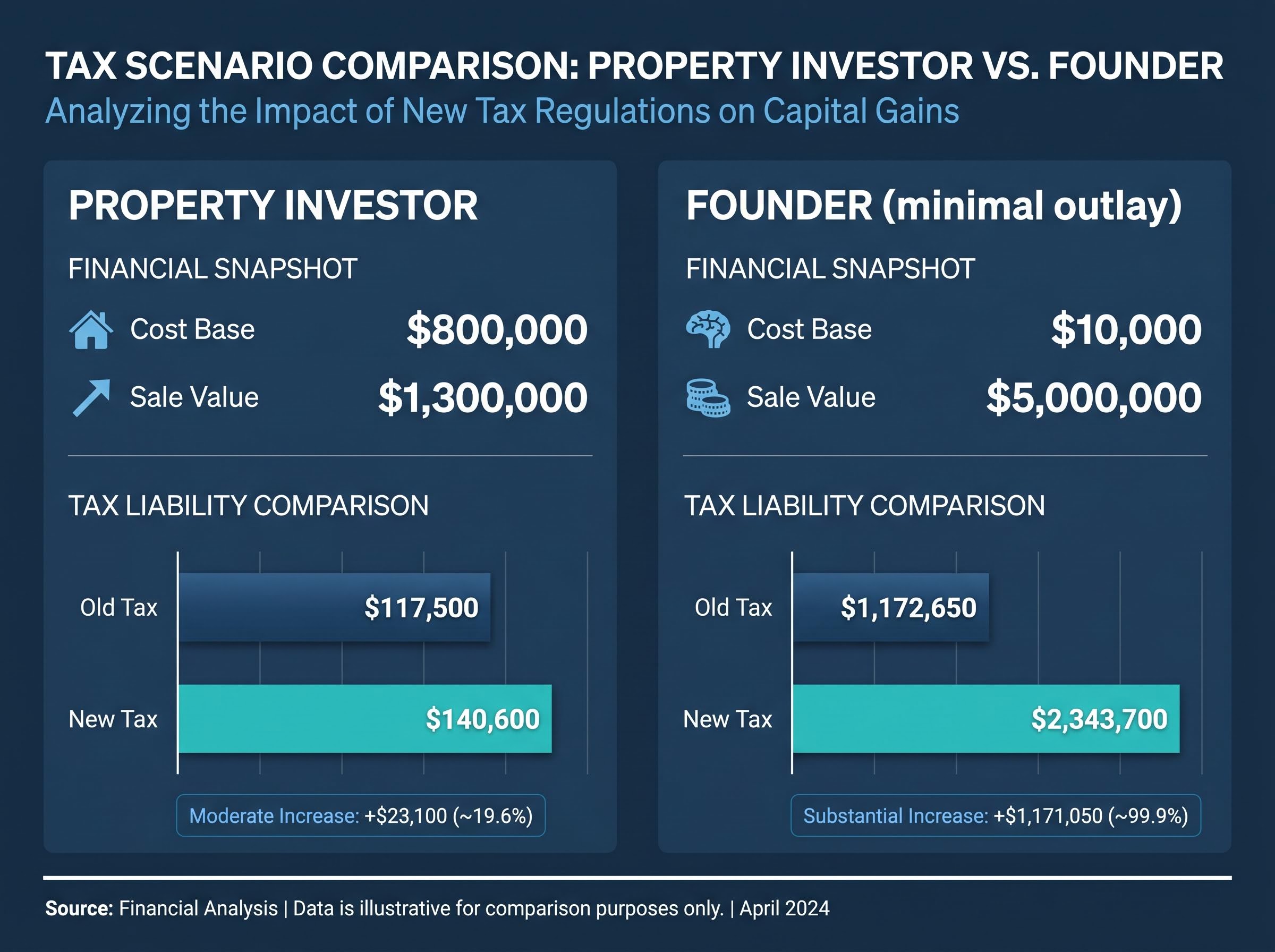

On the surface, cost base indexation is a reasonable principle. It adjusts an asset’s purchase price for inflation so that only real gains are taxed. For an investor who paid $800,000 for a property and sold it a decade later for $1.3 million, indexation meaningfully lifts the cost base, narrowing the taxable gain and lowering the effective rate.

For a founder who invested $10,000 in sweat and seed capital, then sold for $5 million after a decade of compounding risk, the arithmetic works differently. Indexation adjusts the $10,000 cost base upward by the cumulative CPI movement. Even at 3% annual inflation compounded over ten years, that adjustment is roughly $3,400. The taxable gain falls from $4,990,000 to $4,986,600, a reduction so small it is functionally irrelevant.

Low-inflation indexation risk compounds the asymmetry the current article identifies: in an environment where the RBA is targeting a 2-3% band, annual CPI adjustments to a $10,000 cost base produce an uplift measured in hundreds of dollars, making the 30% minimum tax the operative rate in virtually every realistic founder exit scenario.

Under the old 50% discount, that same founder would have been taxed on $2,495,000. The difference between the two regimes is not marginal. It is structural.

| Scenario | Cost Base | Sale Value | Tax (Old 50% Discount) | Tax (Indexation, 47% Rate) |

|---|---|---|---|---|

| Property investor | $800,000 | $1,300,000 | $117,500 | $140,600 |

| Founder (minimal outlay) | $10,000 | $5,000,000 | $1,172,650 | $2,343,700 |

| Early employee (options) | $50,000 | $1,000,000 | $223,250 | $439,400 |

The table illustrates the core asymmetry. Indexation scales with the size of the original investment. When the original outlay is small and the gain is large, the effective tax burden approaches the top marginal income tax rate, collapsing the distinction between capital and income.

Research into the reform’s mechanics found that a flat 33% CGT rate would generally produce a better after-tax outcome for founders than indexation, because a flat discount applies to the full gain rather than adjusting only the original cost base.

Pre-1 July 2027 gains remain grandfathered under existing rules, providing a limited window under the old framework.

When big ASX news breaks, our subscribers know first

What founders actually sacrifice before they see a gain

The CGT discount has never been a windfall for founders. It has been the tax system’s partial recognition of a financial reality that most salaried professionals never experience.

A founder typically invests personal, after-tax capital with no guarantee of return. The early years involve absorbing operating costs while drawing minimal or no salary. Stockspot founder Chris Brycki has publicly disclosed that he received no salary in his first year and, in subsequent years, earned approximately 10% of his prior corporate income.

The specific financial sacrifices accumulate long before a single dollar of capital gain is realised:

- Salary foregone: years at zero or below-market income

- Personal capital at risk: after-tax savings invested with total loss possible

- Opportunity cost: corporate career earnings and superannuation contributions permanently surrendered

- Holding period uncertainty: equity realisation often delayed a decade or more from founding, with no liquidity along the way

These sacrifices are not theoretical. They are the financial inputs that precede any gain the tax system later captures.

The tax system’s implicit bargain with risk-takers

The 50% discount was introduced alongside CGT reforms in 1999 partly to distinguish entrepreneurial and long-term investment risk from ordinary income. It encoded an implicit bargain: accept years of deferred, uncertain compensation, and the tax system will recognise that the eventual gain is qualitatively different from a salary.

The enacted reform withdraws that recognition. Under the new regime, a founder who spent a decade building a company and realised a gain will be taxed at an effective rate approaching that of salaried income, despite having borne risk that salaried employees never face. Canada’s recently introduced Canadian Entrepreneurs’ Incentive explicitly preserves this distinction. Australia’s reform, as legislated, does not.

How the current ESS rules work and where the new reform intersects

Employee share schemes (ESS) allow companies to offer shares or options to employees as part of their compensation. For early-stage startups that cannot match the salaries offered by established firms, ESS arrangements are often the primary tool for attracting and retaining talent. Employees accept a lower cash salary in exchange for equity that may appreciate significantly if the company succeeds.

Since the Treasury Laws Amendment (Cost of Living Support and Other Measures) Act 2022, the ESS landscape for unlisted companies has been substantially liberalised. The previous $5,000 cap on tax-deferred concessions was removed in many circumstances, disclosure requirements were simplified, and tax concessions for employees of unlisted startups were expanded. The ATO’s employer guidance, updated 14 December 2023, details the current concession framework.

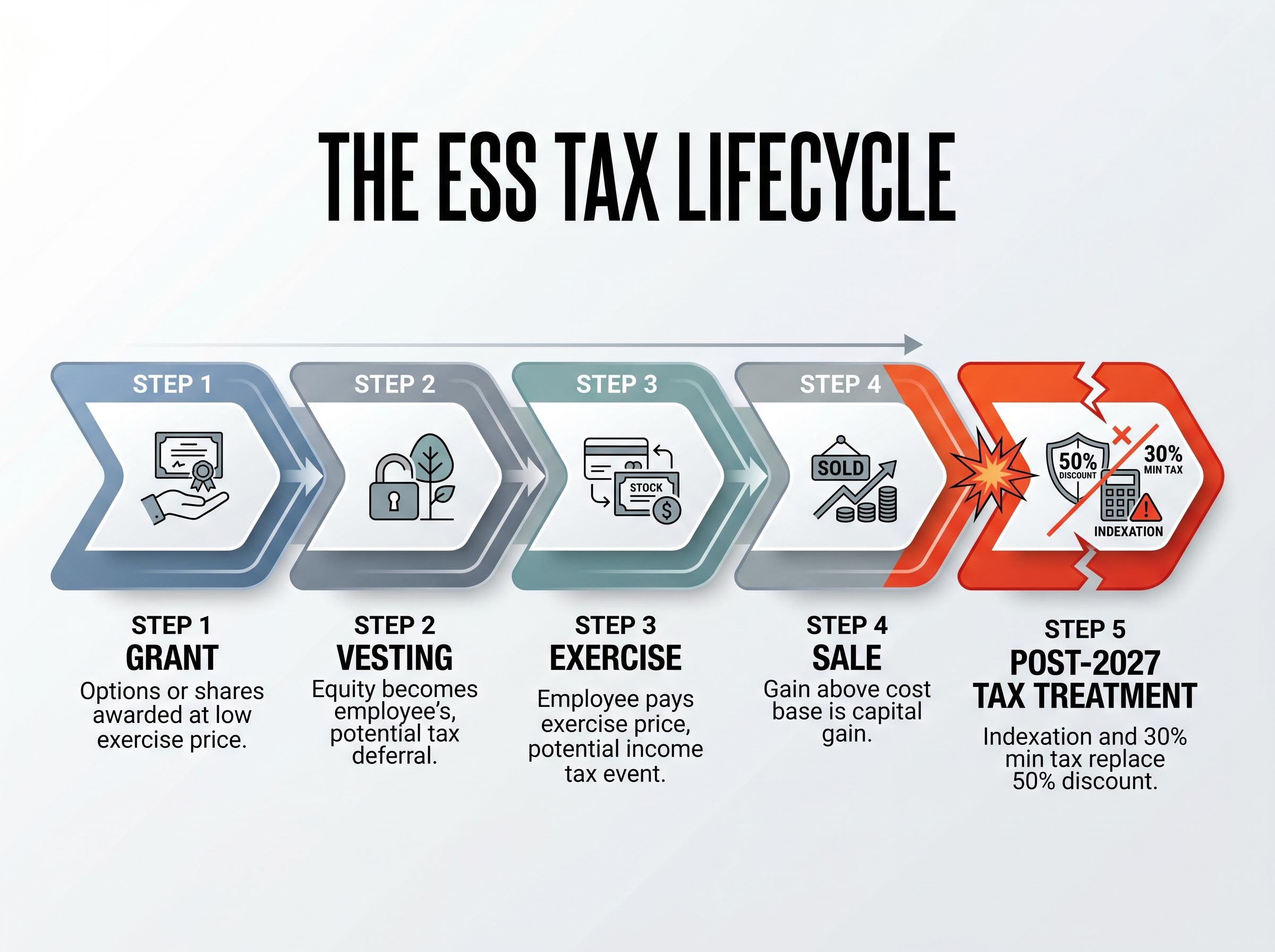

The sequential tax events in a typical ESS lifecycle illustrate where the CGT reform intersects:

- Grant: Options or shares are awarded at a low exercise price, often at nominal value in early-stage companies

- Vesting: The equity becomes the employee’s once conditions are met; in many cases, a tax deferral applies under the startup concession

- Exercise: The employee pays the exercise price and acquires shares; the difference between the exercise price and market value may trigger an income tax event

- Sale: The employee sells the shares; the gain above the cost base (exercise price plus any amount already taxed as income) is a capital gain

- Post-2027 tax treatment: Under the new rules, this capital gain will be subject to indexation rather than the 50% discount, and the 30% minimum tax on net capital gains will apply

Equity granted at a low exercise price accumulates most of its value as capital gain, not income. The CGT treatment at exit is therefore the single variable that determines whether the deferred compensation trade-off made financial sense.

For employees holding options or shares from a low grant price, replacing the discount with indexation directly reduces the after-tax return at the point where it matters most.

Division 152 small-business concessions interact with the new 30% minimum tax in ways that remain unresolved, creating a consequential unknown for founders approaching a capital event: whether existing retirement exemptions and active asset tests will operate as intended alongside the new floor, or be partially neutralised by it.

Australia’s innovation gap and the structural cost of removing the incentive

The ASX tells a story that tax policy alone cannot explain, but one that tax policy should not make worse.

Of Australia’s 10 largest listed companies, the most recently founded is Goodman Group, established in 1989. Its recent growth has been driven partly by AI-related data centre demand. The remaining nine were founded before 1985. In more than three decades, no new Australian company has built sufficient scale to displace any of them.

The structural constraints behind this record are well documented. Australia’s domestic market is small. Access to growth-stage capital is constrained relative to the United States and parts of Europe. Corporate culture favours dividend distribution over reinvestment for scaling. The Australian Investment Council’s “State of Australian Startup Funding 2024” report, published in February 2025, emphasised the importance of a competitive policy environment for early-stage capital formation. Research from Monash University on the Australian venture capital landscape in 2024 identified similar structural early-stage challenges.

Goodman Group, founded in 1989, is the most recently established company among Australia’s 10 largest listed businesses. The rest were founded before 1985.

The CGT discount was one of the limited policy levers working against these constraints. It partially compensated for the financial asymmetry founders and early employees accept when building companies in a market that structurally disadvantages them. Removing it without a founder-specific carve-out withdraws that compensation at a specific moment.

A capital lock-in effect emerges when higher effective CGT rates make asset sales economically irrational relative to continued holding, and for founders whose equity is already illiquid, the new regime adds a tax-driven disincentive to realisation on top of the structural liquidity constraints that already characterise private company ownership.

The AI window and why timing matters

AI-driven industry transformation is creating new company formation opportunities globally. The policy environment at this particular moment will influence whether Australian founders pursue those opportunities domestically or offshore.

The anticipated behavioural response is straightforward: prospective founders either remain in salaried employment, where after-tax returns are now comparatively more attractive, or incorporate offshore from the outset, where the tax treatment of entrepreneurial gains is more favourable. Neither outcome benefits the Australian economy.

How other countries have handled the founder equity problem

The question of whether entrepreneurial gains should be treated differently from passive investment gains is not unique to Australia. Two comparable jurisdictions have recently legislated explicit answers.

Canada’s Budget 2024, delivered on 16 April 2024, raised the general capital gains inclusion rate from 50% to 66.67% for annual gains above CAD 250,000 for individuals. Simultaneously, it introduced the Canadian Entrepreneurs’ Incentive, which reduces the inclusion rate to 33.3% on up to CAD 2 million of qualifying founder gains, phased in from 2025. The policy acknowledged that raising rates on capital generally and protecting founder equity specifically are not mutually exclusive objectives.

The United Kingdom has maintained Business Asset Disposal Relief (BADR), which explicitly treats gains from business ownership differently from other capital gains. The relief’s lifetime limit was reduced from GBP 10 million to GBP 1 million in March 2020, but it was retained in the Spring Budget 2024 alongside a residential property CGT rate reduction from 28% to 24%.

New Zealand and Singapore do not face this design question in the same form, because neither levies a broad-based capital gains tax.

| Jurisdiction | Recent CGT Change | Entrepreneur-Specific Relief | Relief Details |

|---|---|---|---|

| Australia | 50% discount replaced by indexation + 30% min tax (eff. 1 Jul 2027) | None | Grandfathering for pre-2027 gains only |

| United Kingdom | Residential CGT rate cut to 24% (2024) | BADR retained | GBP 1M lifetime limit since 2020 |

| Canada | Inclusion rate raised to 66.67% | Entrepreneurs’ Incentive introduced | 33.3% rate on up to CAD 2M for qualifying founders |

| New Zealand | No change | No broad CGT exists | N/A |

| Singapore | No change | No CGT exists | N/A |

Australia’s reform, as enacted, includes no equivalent founder-specific provision. The absence is not an oversight; it is a policy choice that stands in contrast to the direction taken by comparable economies.

The policy gap Australia still has time to close

The shift from discount to indexation is not neutral across asset classes. It is structurally more damaging for low-outlay, high-appreciation equity, the kind founders and early employees hold, than for high-cost-base property assets. The arithmetic is unambiguous: indexation scales with the size of the original investment, and when that investment is small, the benefit is negligible.

The grandfathering provisions offer a limited buffer. Gains arising before 1 July 2027 remain under existing rules, giving founders with pre-2027 equity a finite period under the old framework. For anyone founding a company or accepting equity compensation after that date, the calculus has materially changed.

The grandfathering provisions apply at asset level, not taxpayer level, meaning a founder holding both pre-Budget equity and post-Budget grants will face different calculations on each parcel, adding record-keeping complexity that compounds the underlying tax cost.

The ATO’s CGT reform guidance confirms the transitional arrangements in detail, including the grandfathering provisions that preserve existing rules for gains arising before 1 July 2027, making the cut-off date a material consideration for anyone holding equity positions today.

Canada and the United Kingdom have both demonstrated that raising general CGT rates and protecting founder equity are not mutually exclusive objectives. Australia’s reform, as legislated, makes no such distinction. The policy gap is identifiable, the international precedent exists, and the legislation has not yet taken effect.

For founders evaluating whether to proceed, and for employees weighing equity against salary, the post-2027 after-tax outcomes under the new regime should be modelled before any commitment is made. The financial logic that previously made equity sacrifice rational has been rewritten.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Tax outcomes depend on individual circumstances, and the legislation discussed may be subject to amendment before its effective date.