As of Budget night, 12 May 2026, the 50% capital gains tax discount that Australian investors have relied on for more than two decades no longer exists for gains accruing after 1 July 2027. In its place, the 2026-27 Federal Budget introduced two interlocking changes: CPI-based indexation of the cost base, and a 30% minimum tax floor on real gains. Published six days after the announcement, and before professional guidance has widely circulated, this article sets out precisely how the new indexation calculation works, what the minimum tax floor does to planning options, how the transition period operates, and what investors need to consider before the 1 July 2027 start date. The ATO has confirmed that this measure is not yet law; final details remain subject to parliamentary passage.

The 50% discount is gone. Here is what replaced it

For more than two decades, Australian investors who held an asset for longer than 12 months could exclude half of the nominal gain from their assessable income. That mechanism is now being replaced by CPI-based indexation of the cost base, a framework that strips out inflation so that only the real gain is taxed.

The indexation formula has three steps:

- Divide the Consumer Price Index (CPI) at the quarter of sale by the CPI at the quarter of purchase.

- Multiply the result by the original cost base to produce an inflation-adjusted cost base.

- Subtract the indexed cost base from the sale price. The remainder is the taxable real gain.

This is not a new invention. CPI indexation operated as the standard CGT framework before 1999, when it was replaced by the flat 50% discount specifically because of administrative complexity. Its reinstatement means investors and their advisers will need to track CPI data on a per-parcel basis for every holding.

The CGT reform since 1999 that comes closest in scale to the current changes was the Howard government’s 1999 introduction of the 50% flat discount, which itself replaced the very CPI indexation model now being reinstated; that reform simplified administration but embedded the inflation-blind gain calculation that the 2026 Budget is now unwinding.

The Australian Treasury CGT reform factsheet, published on Budget night alongside Budget Paper No. 1, confirms that the 50% discount is replaced by cost base indexation and a 30% minimum tax rate for gains accruing after 1 July 2027, with the measure applying to assets held by individuals for more than 12 months.

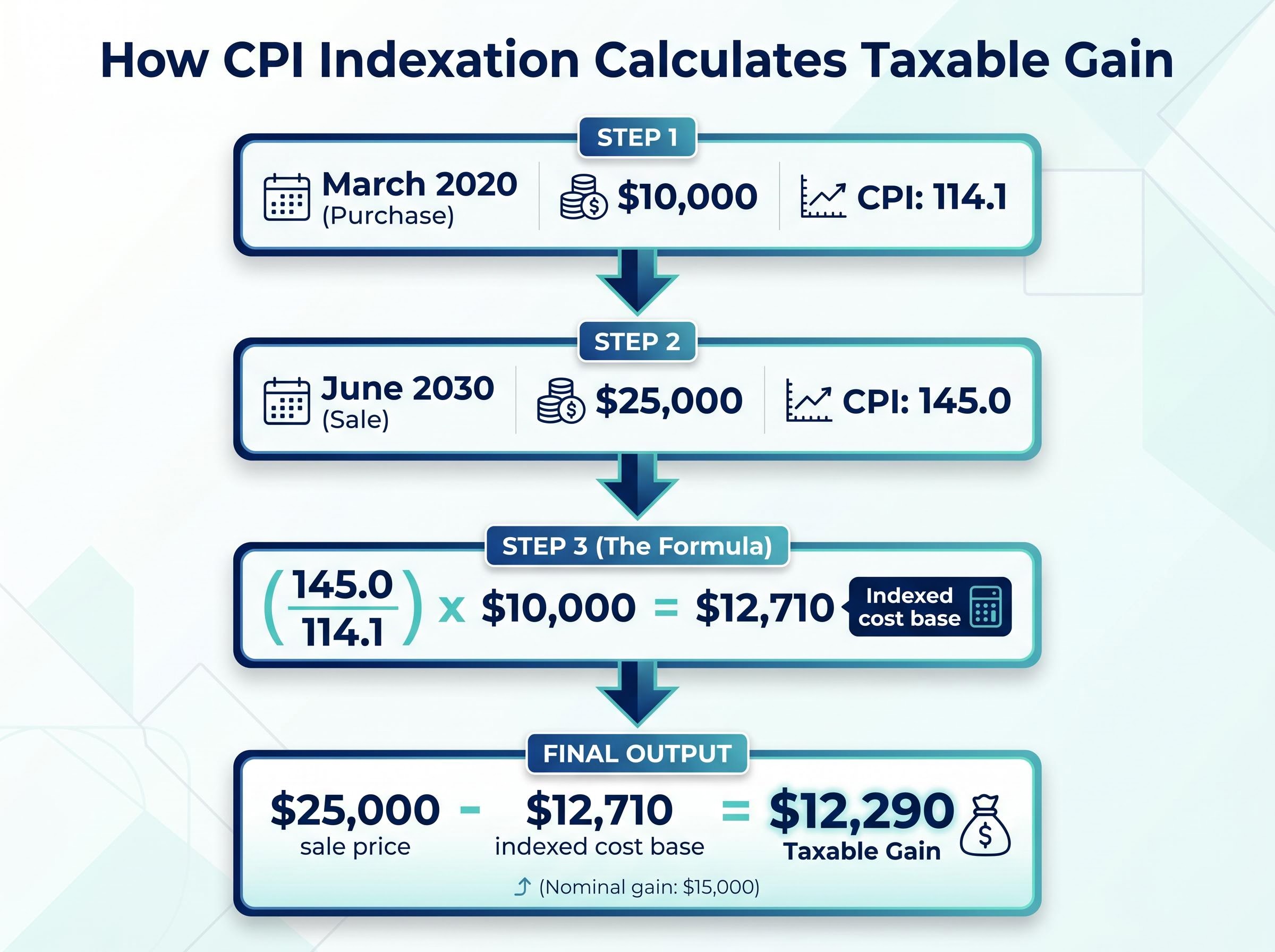

Worked example: how the indexation calculation produces a taxable gain

Worked example: Shares purchased for $10,000 in the March 2020 quarter (CPI 114.1), sold in a hypothetical June 2030 quarter (CPI 145.0), produce an indexed cost base of $12,710. If sold for $25,000, the taxable gain is $12,290 rather than the $15,000 nominal gain.

The formula in action: (145.0 / 114.1) x $10,000 = $12,710. The sale price of $25,000 minus the indexed cost base of $12,710 produces a taxable gain of $12,290. Only that real gain above the inflation adjustment is assessable.

The RBA publishes the inflation data used in the calculation, and ATO calculation tools are expected ahead of 1 July 2027, though none had been released as of 18 May 2026.

The ABS Consumer Price Index methodology underpins the indexed cost base calculation, providing the quarterly CPI figures that investors and advisers must use to adjust acquisition costs on a per-parcel basis across every asset class subject to the new regime.

When big ASX news breaks, our subscribers know first

Why the new system sometimes produces a higher tax bill than the old one

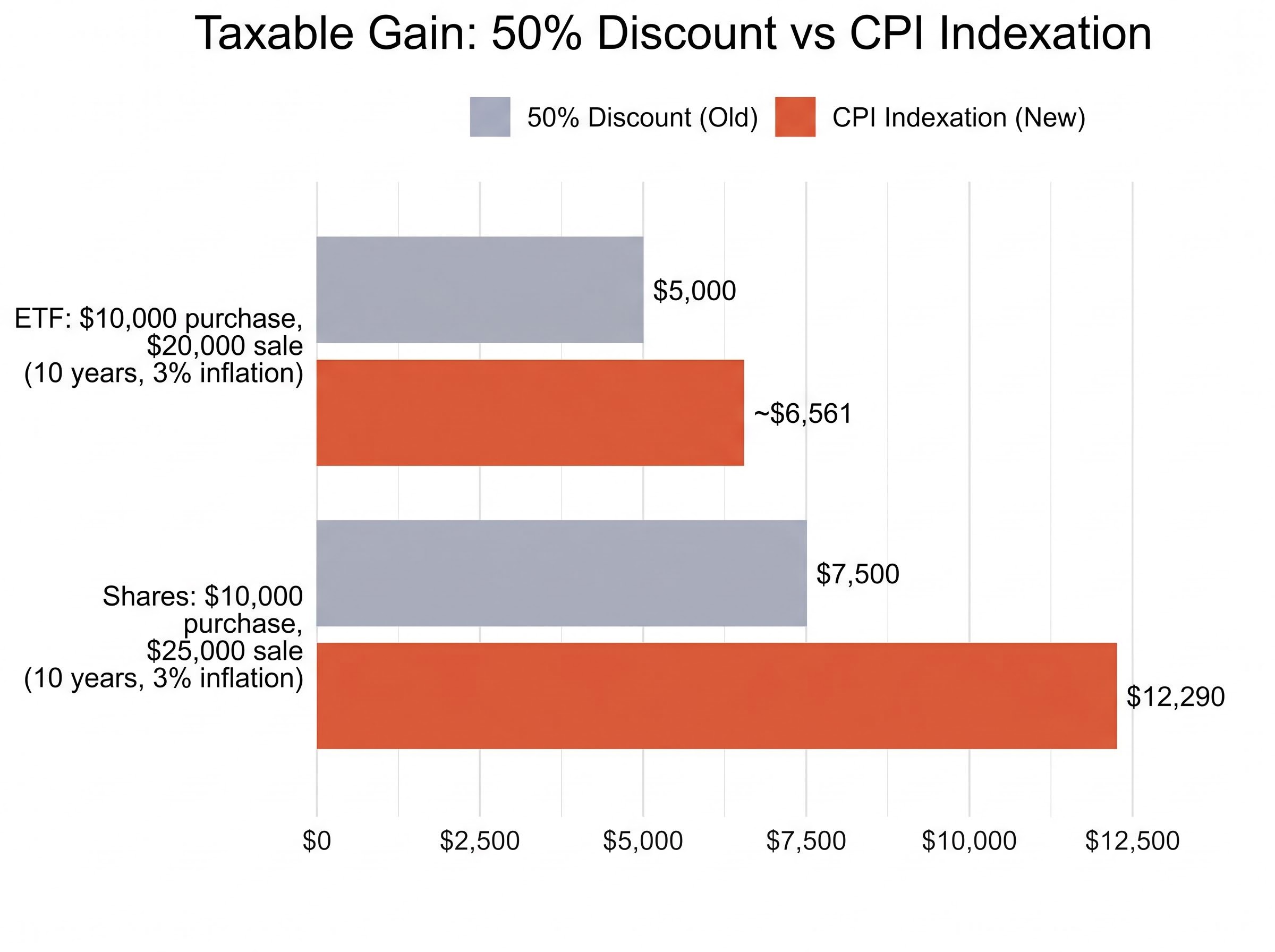

The two regimes do not produce the same outcome. Which one delivers a lower tax bill depends on how fast the asset grew relative to inflation.

Consider an ETF purchased for $10,000 and sold for $20,000 a decade later, roughly a 7.2% annual return. Assuming 3% annual inflation, the indexed cost base rises to approximately $13,439, producing a taxable gain of about $6,561. Under the old 50% discount, the taxable gain on the same transaction would have been $5,000.

The difference is not trivial. High-growth assets that outpace inflation generate a larger taxable gain under indexation, because the inflation adjustment strips out only a modest portion of a large nominal gain. The 50% discount, by contrast, halved the gain regardless of how much of it was real versus inflationary.

The inverse also holds. Assets growing at rates close to inflation can produce a smaller taxable gain under indexation, particularly in elevated inflation environments where the CPI adjustment is large relative to the gain.

| Scenario | Taxable gain: 50% discount (old) | Taxable gain: CPI indexation (new) |

|---|---|---|

| ETF: $10,000 purchase, $20,000 sale (10 years, 3% inflation) | $5,000 | ~$6,561 |

| Shares: $10,000 purchase, $25,000 sale (10 years, 3% inflation) | $7,500 | $12,290 |

The asset-type profiles most affected by this difference include:

- High-growth, low-yield equities where nominal gains far exceed inflation

- Low-cost-base legacy holdings where adjusting a small base still leaves most of the gain assessable

- Assets growing near the inflation rate, which benefit from indexation relative to the old discount

What the 30% minimum tax floor means for your planning options

Regardless of the indexation outcome, a minimum effective CGT rate of 30% applies to all real gains from 1 July 2027. Even if an investor’s marginal tax rate falls below that threshold, the tax on a capital gain cannot fall below this floor.

“The 30% floor removes the ability to time a disposal to coincide with a low-income year to reduce CGT below that threshold.”

This eliminates a specific planning strategy that many investors have used or intended to use: timing asset disposals to coincide with low-income years, such as retirement, a career break, or a sabbatical, to leverage a lower marginal rate on the gain. Under the previous rules, an investor with no other assessable income in a given year could pay as little as 0% on the first portion of a gain falling within the tax-free threshold. That option no longer exists for gains subject to the new regime.

The retirement income-timing strategy that the 30% floor eliminates was more valuable than many investors realised: under the old rules, an investor with no other assessable income could reduce their effective CGT rate to as low as 8.25% by timing a disposal in a year where the discounted gain fell entirely within the lower marginal rate bands, an option the floor permanently removes regardless of income in the disposal year.

The scope of the floor is worth clarifying:

- Affected: Most individual investors disposing of assets held for more than 12 months after 1 July 2027

- Not affected: Superannuation fund members and self-managed super fund (SMSF) holders, whose existing CGT treatment is unchanged; pension phase accounts also remain unaffected

The measure is not yet law as of 18 May 2026, and final design details remain subject to parliamentary process. For investors who had planned retirement-year asset sales as a tax minimisation strategy, the 30% floor removes a meaningful lever and requires revised modelling.

Understanding the Transitional Rules and Grandfathering Provisions

The reform does not wipe out the value of the 50% discount on gains already accumulated. A grandfathering rule applies: assets held at 7:30 pm AEST on 12 May 2026 retain the 50% discount on gains accrued up to 1 July 2027. Only gains from that date forward fall under the new indexation rules.

The market value of the asset on 1 July 2027 acts as the dividing line. The apportionment process works as follows:

- Identify the acquisition date and original cost base of the asset.

- Determine the market value of the asset at 1 July 2027 (via formal valuation or an ATO-approved apportionment formula, once published).

- Calculate the split: gains up to the 1 July 2027 value attract the 50% discount; gains from that date forward are subject to CPI indexation.

- Apply the respective CGT regime to each portion when the asset is eventually sold.

| Period | Gain amount | CGT regime |

|---|---|---|

| Purchase ($10,000) to 1 July 2027 ($12,200) | $2,200 | 50% discount (old rules) |

| 1 July 2027 ($12,200) to eventual sale ($14,400) | $2,200 | CPI indexation (new rules) |

| Total gain | $4,400 | Apportioned across both regimes |

Assets acquired after Budget night (12 May 2026) follow the same split framework. ATO guidance tools are expected but had not been published as of 18 May 2026.

The new-build property carve-out: what it covers and what it does not

Purchasers of newly constructed dwellings can elect between the 50% discount and CPI indexation on eventual sale. This carve-out does not extend to existing dwellings, shares, ETFs, or other asset classes.

The policy rationale is targeted: the carve-out is designed to preserve incentives for new housing supply investment. Build-to-rent investment and affordable housing programmes are also exempt from the associated negative gearing changes. No separately citable evaluation of the carve-out’s likely effectiveness in stimulating housing supply had been published as of 18 May 2026.

Exclusions and Exemptions: What the Reforms Leave Untouched

Several components of the existing CGT and dividend tax system are entirely unaffected:

- Short-term gains (assets held less than 12 months) remain fully included in assessable income at the investor’s marginal rate; indexation and the minimum tax floor apply only to assets held longer than 12 months

- Superannuation fund CGT treatment, including SMSFs, is unchanged

- Carry-forward capital losses are preserved, measured against the nominal cost base consistent with the pre-1999 framework

- Franking credits and dividend imputation are entirely unaffected

- Domestic versus international equities receive equivalent treatment under the new rules; indexation applies identically to both

“The franking credit imputation system is entirely unaffected by the Budget changes.”

Investors managing mixed portfolios of income stocks and growth assets, or those with SMSFs, can be reassured that these structural components of their strategy require no adjustment in response to the reform.

One year to act: what Australian investors should do before 1 July 2027

The transition window to 1 July 2027 is a planning opportunity, not a reason to restructure an entire portfolio in haste. Core allocation decisions, including risk tolerance, return expectations, liquidity needs, and time horizon, remain primary. Tax settings are a secondary consideration.

That said, the reform does incrementally improve the relative appeal of fully franked ASX income stocks, not because the imputation system changed, but because the CGT treatment of long-held growth assets became less favourable by comparison.

Five concrete steps for the year ahead:

- Identify holdings that will be affected by post-1 July 2027 indexation rules.

- Obtain or note market valuations as close to 1 July 2027 as practicable, for apportionment purposes.

- Model the indexation versus 50% discount comparison for high-growth holdings to quantify the difference.

- Consult a financial adviser and accountant before any disposal decision, given the complexity of per-parcel indexation for share portfolios and the not-yet-law status of the measures.

- Monitor ATO and Treasury publications for draft guidance on calculation methodology as the start date approaches.

Indexed cost base tracking on a per-parcel basis is the administrative consequence that CPA Australia flagged as the reform’s most significant compliance burden for ordinary investors: each parcel of shares purchased at a different date requires its own CPI ratio calculation at sale, a requirement that the 50% discount system never imposed.

CPA Australia, May 2026: “A tax grab that punishes aspiration and deters investment.”

CPA Australia’s characterisation reflects advocacy framing, and the measures remain subject to parliamentary revision. The broader reform package is estimated to deliver $3.531 billion in receipts by 2029-30, according to Budget Paper No. 1 and Budget Paper No. 2. No ATO draft guidance or Treasury consultation paper on calculation methodology had been published as of 18 May 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The measures described are not yet law and remain subject to change based on parliamentary process and final legislative drafting.

The reform in context: a structural shift, not a marginal tweak

The CGT changes sit within a broader Budget package targeting what the government describes as intergenerational inequity in asset taxation, particularly in housing. The policy rationale rests on three pillars:

- Addressing intergenerational equity by reducing the tax advantages of existing asset holders relative to new entrants

- Directing investment incentives toward new housing construction rather than existing dwellings

- Ensuring capital gains are taxed on real economic value rather than nominal gains inflated by CPI movements

Taxing real gains rather than nominal gains is conceptually defensible. CPA Australia, however, has raised concerns that the complexity of per-parcel CPI indexation disproportionately burdens ordinary investors compared to sophisticated, professionally advised ones. The revenue impact of the broader reform package, estimated at $3.531 billion by 2029-30, has been described by the government as broadly revenue-neutral when paired with associated tax cuts.

The measure is not yet law. The ATO confirmed this explicitly as of 18 May 2026. The legislative and administrative detail that emerges over the next 12 months will be as consequential as the headline announcement for determining the reform’s real-world impact on Australian investors.

For investors wanting to quantify the long-run compounding cost of the new regime and identify which structural changes, including low-turnover ETF selection, superannuation contribution sequencing, and buy-only rebalancing, offer the most effective mitigation, our dedicated guide to CGT-efficient portfolio structuring models a $100,000 portfolio over a 30-year horizon and shows where the terminal wealth gap between old and new regimes exceeds $100,000.

Past performance does not guarantee future results. Financial projections and tax estimates are subject to market conditions, legislative change, and various risk factors.