A fund delivering 10% returns sounds compelling, until the benchmark turns out to be 5% in cash. That gap may say more about the benchmark than the manager. For Australian investors navigating an expanding universe of alternatives, private credit, and actively managed funds, the benchmark question remains one of the most consequential and most overlooked steps in fund selection. ASIC’s Corporate Plans for 2024-25 and 2025-26 both flag “poor design and disclosure of fees and costs” in managed funds as a continuing regulatory concern. APRA’s December 2024 review of unlisted asset governance explicitly flagged that performance assessment frameworks must reflect underlying risk and liquidity. Yet at the retail level, few investors interrogate the benchmark before committing capital. This guide provides a repeatable, practical process for doing exactly that: what to look for, where to find it, how to classify what you find, and what red flags should prompt a harder look.

Why the benchmark is the most underread line in any fund document

Most investors open a fund document and go straight to the return figure. Then fees. Then the manager’s track record. The benchmark, if it is read at all, registers as a technical detail rather than the interpretive lens it actually is.

A benchmark does two distinct jobs inside a fund structure:

- Performance reference: it is the comparator used in reporting to show how the fund performed relative to a relevant market or target.

- Fee hurdle: in most active funds charging performance fees, it is the threshold the manager must exceed before those fees are triggered.

This dual role means the benchmark frames every performance number an investor sees. A 10% return against a 5% cash benchmark tells a fundamentally different story than a 10% return against a 9% equity index. The first implies significant outperformance; the second implies the manager barely kept pace with the market. ASIC’s Moneysmart guidance advises investors to check “what your investment is being compared to” and whether returns are quoted before or after fees. Chris Brycki, founder of Stockspot, has noted that benchmarks are commonly presented as simple reference points, but their actual function is to establish the hurdle a manager must exceed, shaping how results are communicated.

Investors who skip benchmark assessment are effectively reading performance data without the context that gives it meaning.

Appropriate versus inappropriate benchmarks: the core distinction

Benchmark appropriateness refers to the degree to which the chosen comparator reflects the fund’s actual risk level, asset class, and liquidity profile. An appropriate benchmark makes genuine outperformance visible. An inappropriate one, particularly one set too low, can make average risk-adjusted returns look exceptional and trigger performance fees that reward market exposure rather than manager skill.

When big ASX news breaks, our subscribers know first

How to classify the benchmark you are looking at

Identifying a fund’s benchmark is the first step. Classifying it is what turns raw information into structured interpretation. Australian fund documents contain three main benchmark types, each with different implications for how performance numbers should be read.

Recognised market indices include the S&P/ASX 200, MSCI World, and global high-yield indices. These are independently constructed, publicly transparent, and widely used across the industry. Cash-plus or CPI-plus targets express performance as a margin above the RBA cash rate or consumer price inflation (for example, RBA cash rate plus 4% or CPI plus 3%). Custom or proprietary indices are constructed by the fund manager or a related party; their composition, methodology, and rebalancing rules may or may not be publicly disclosed.

Each type serves a purpose in the right context. Equity and balanced funds typically use market-cap indices. Alternatives and private credit funds commonly use cash-plus or CPI-plus targets. Some absolute-return funds use fixed return targets. The warning sign is not the benchmark type itself but whether it matches the fund’s actual risk and asset profile. APRA’s December 2024 review stressed that performance assessment frameworks for unlisted assets must “adequately reflect the underlying risk, liquidity, and valuation uncertainty.” Morningstar’s Fund Ratings Methodology (updated October 2024) explicitly examines whether the benchmark matches the fund’s investable universe and whether tracking error and active share are measured against that index. CBA Institutional Insights (May 2025) argued that private credit benchmarks should reflect “credit, liquidity and structural risks” closer to sub-investment grade debt than term deposits, suggesting high-yield bond indices or credit spreads over swap curves rather than the RBA cash rate.

Investors should consult three document sources to locate and classify the benchmark:

- Product Disclosure Statement (PDS): the primary legal disclosure document.

- Target Market Determination (TMD): outlines the intended investor audience and the fund’s key features.

- Fund website: often provides the most current benchmark and performance reporting detail.

| Benchmark Type | Typical Use Case | Red Flag If Used For | Example Index |

|---|---|---|---|

| Recognised market index | Equity, balanced, listed property | Highly concentrated or alternative strategies | S&P/ASX 200, MSCI World |

| Cash-plus or CPI-plus | Absolute return, conservative alternatives | High-yield credit, illiquid or leveraged strategies | RBA cash rate + 4%, CPI + 3% |

| Custom or proprietary index | Niche or multi-asset strategies | Any strategy where construction is not disclosed | Manager-constructed composite |

What benchmarks actually do to your fees

The mechanics of how a benchmark interacts with a fund’s fee structure are straightforward, but the cumulative impact is often underappreciated. Most active Australian funds operate on a base fee plus performance fee structure, where the performance fee is directly tied to returns above the benchmark.

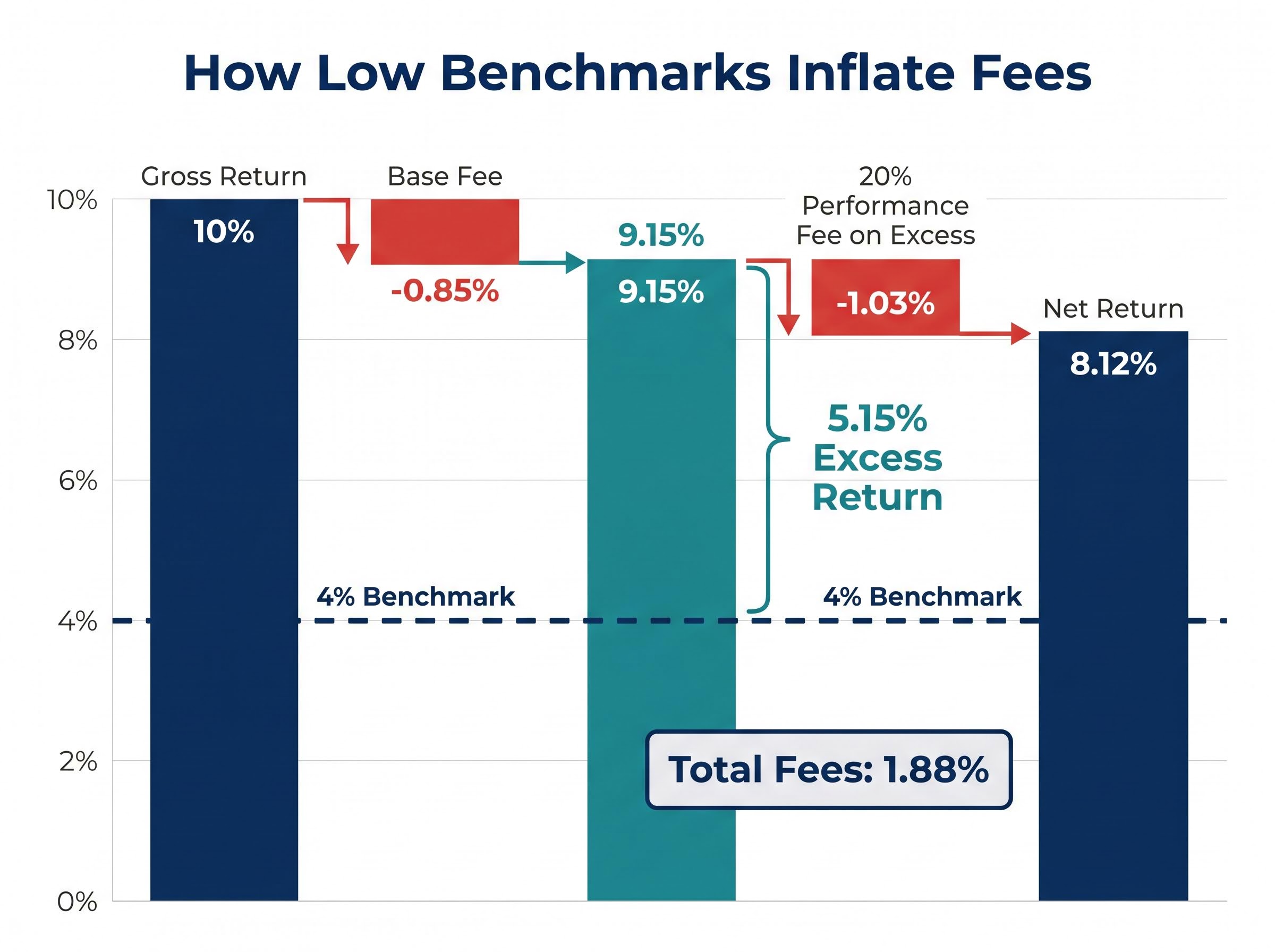

Consider how this works in practice. Take a managed infrastructure fund charging a 0.85% management fee and a 20% performance fee above a 4% benchmark:

- The fund delivers a gross return of 10% for the year.

- After the 0.85% base management fee, the net return before performance fees is approximately 9.15%.

- The return above the 4% benchmark is approximately 5.15%.

- The performance fee is 20% of that excess: roughly 1.03%.

- Total annual fees come to approximately 1.88%, and the investor’s net return falls to around 8.12%.

A 9% net return from an infrastructure strategy carrying illiquidity and concentration risk is not exceptional. Yet the fee structure rewards the manager as though it were, because the 4% hurdle sits well below the risk level of the underlying assets. Had the benchmark been an infrastructure-appropriate index returning 7%, the performance fee calculation would look very different.

The second dimension of fee fairness is the high-watermark. Without a permanent high-watermark, a manager can charge performance fees repeatedly across market cycles even after delivering losses, potentially leaving investors paying fees on gains they have not yet cumulatively recovered. APRA’s December 2024 review flagged a specific concern: performance fees charged on unrealised gains from unlisted assets, where valuation uncertainty means the gains may never be realised in a market transaction.

Chris Brycki has noted that typical base management fees sit around 1% annually, with performance fees commonly 10%-20% of returns above the benchmark.

An incremental annual fee drag of 0.5%-1%, compounded over a decade or more, could reduce an investor’s total balance by 10% or greater.

The benchmark is the mechanism through which the fund’s fee structure either rewards genuine skill or extracts fees for ordinary market exposure.

Red flags that should make you look harder

Benchmark issues rarely appear in isolation. They tend to cluster in fund structures where benchmark design and fee mechanics work together in the manager’s favour. Four specific patterns warrant additional scrutiny:

- Cash-plus or CPI-plus benchmark for a high-risk strategy: A fund holding illiquid, leveraged, or credit-risk-heavy assets while benchmarking to a cash-based hurdle has set the bar low enough that fee generation becomes near-automatic, regardless of manager skill. Morningstar Australia’s research (2024-25) notes that cash-plus benchmarks “may not reflect the equity-like downside risk of some private credit and unlisted property funds.”

- Proprietary or custom benchmark without public disclosure: Investors should ask who constructed the index, whether it is independently calculated, and whether its composition is publicly available. Opacity in benchmark construction is a structural concern, not a minor administrative detail.

- No permanent high-watermark, combined with fees on unrealised gains: This combination allows fee extraction before investors have recovered prior losses and before valuations have been tested by a market transaction. APRA’s December 2024 review specifically flagged this risk for unlisted asset funds.

- Unusually narrow and consistent outperformance: When a fund’s reported returns track barely above its benchmark across multiple market environments, this may indicate the benchmark was engineered to be beatable rather than genuinely reflective of risk-adjusted peer-group performance. Chris Brycki has noted that consistent and wide outperformance should prompt scrutiny of whether the benchmark is set appropriately, not only whether the manager is highly skilled.

Several private credit funds have been reported earning double-digit returns yet benchmarking to cash plus 3%, making performance fees near-guaranteed and obscuring equity-like downside risk.

Recognising these patterns gives investors a meaningful filter before committing to deeper analysis.

The five-step due diligence checklist investors can use right now

The following checklist synthesises regulatory expectations (APRA December 2024 review, ASIC Moneysmart), Morningstar methodology, and adviser best-practice commentary into a concrete sequence investors can apply to any fund document.

- Identify the benchmark. Locate the benchmark used for both performance reporting and performance fee calculation. Check the PDS, TMD, and fund website. Confirm whether the same benchmark serves both functions.

- Assess appropriateness. Ask whether the benchmark matches the fund’s asset class, liquidity profile, and risk level. An illiquid private credit fund benchmarked to the RBA cash rate is a mismatch.

- Classify the benchmark type. Determine whether it is a recognised market index, a cash-plus or CPI-plus target, or a custom index. If custom, establish who constructed it and whether its methodology is publicly disclosed.

Applying the checklist to fee terms and regulatory cross-checks

- Examine performance fee terms. Determine whether the hurdle is realistic or trivially easy to exceed. Check whether a permanent high-watermark exists. Establish whether fees are charged on unrealised as well as realised gains, and whether any clawback mechanism applies if returns later reverse. ASIC Moneysmart advises checking whether returns are quoted before or after fees.

- Cross-check against regulatory and best-practice expectations. Does the benchmark align with APRA’s expectation that performance assessment frameworks for unlisted assets reflect underlying risk, liquidity, and valuation uncertainty? Does it meet a Morningstar-style standard of alignment between investment objective, risk, and comparator index? Does the fund’s disclosure conform to the FSC Guidance Note GN 27 and RG 97 framework?

| Step | What to Do | Document Source | Key Question |

|---|---|---|---|

| 1 | Identify the benchmark | PDS, TMD, fund website | What is the fund measured against? |

| 2 | Assess appropriateness | PDS, fund factsheet | Does the benchmark match the fund’s risk and asset class? |

| 3 | Classify benchmark type | PDS, fund website | Is it a market index, cash-plus, or proprietary? |

| 4 | Examine fee terms | PDS, periodic statements | Is there a permanent high-watermark? Fees on unrealised gains? |

| 5 | Cross-check against standards | APRA review, Morningstar, FSC GN 27 | Does the framework reflect risk, liquidity, and valuation uncertainty? |

For private credit and alternatives, steps four and five carry disproportionate weight given APRA’s December 2024 findings and the specific risk of fees on unrealised valuations. The dual benchmarking approach recommended by Australian licensee research heads, as reported by Professional Planner in March 2025, offers a practical supplement: assess the fund against both a risk-free anchor (such as cash or CPI-plus) and a risk-matched market index (such as a global high-yield or leveraged loan index).

Running through these five steps before committing capital takes under an hour and can reveal structural issues that headline performance numbers alone will not show.

Benchmark literacy is a permanent investor skill, not a one-time check

ASIC’s Corporate Plans for 2024-25 and 2025-26 confirm that “poor design and disclosure of fees and costs” in managed funds remains a continuing regulatory focus. APRA’s supervision priorities for 2025-26 include scrutiny of whether return targets for private credit and illiquid assets properly reflect the risks involved. The regulatory direction is clear: benchmark and fee disclosure standards are tightening.

No regulator, however, checks benchmarks on an investor’s behalf at the fund-selection stage. That responsibility sits with the investor. The RIAA Responsible Investment Standard 2024 expects “clear articulation of the reference benchmark or target return” and explanation of how it aligns with the fund’s strategy and asset mix. Investors are entitled to this information.

As Chris Brycki has observed, headline performance figures attract investor attention, but the benchmark is what determines how those figures should be interpreted. The skill of reading benchmarks does not require technical expertise; it requires the willingness to ask the question before being persuaded by the headline number.

Three principles are worth carrying forward:

- Investors are entitled to know the benchmark, its rationale, and who constructed it.

- Returns should always be assessed after fees, and investors should confirm whether reported figures are pre-fee or post-fee.

- A benchmark that cannot be independently verified or that structurally understates risk is a warning, not a detail.

Benchmark assessment is not a gate investors pass through once. It is the interpretive layer that makes every future performance claim legible, and investors who develop this skill now hold a durable advantage in evaluating any fund structure the market produces next.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.