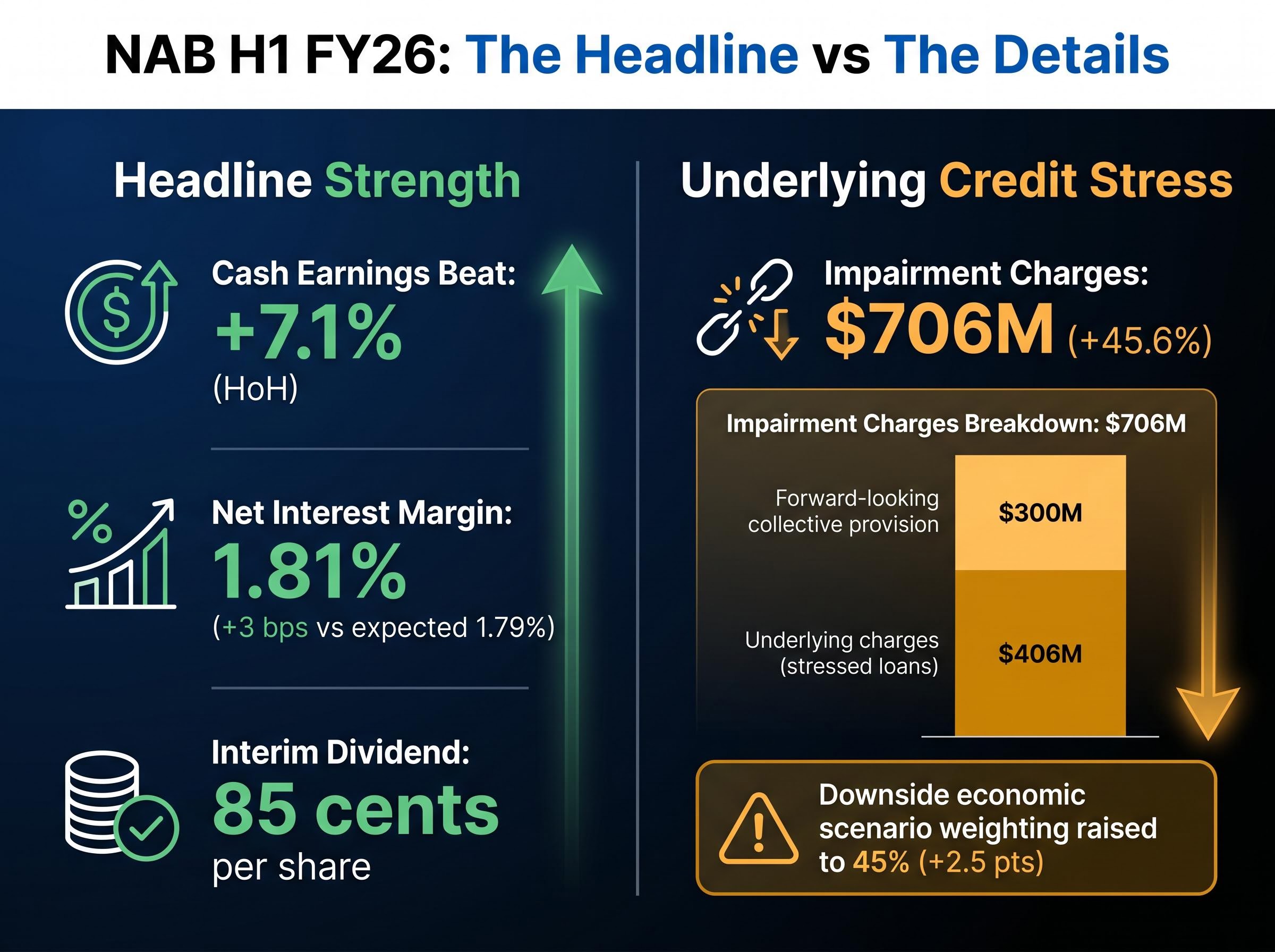

National Australia Bank delivered a first-half FY26 cash earnings beat of 7.1% on a half-on-half basis, the kind of headline that invites relief. Beneath it, credit impairment charges surged 45.6% to $706 million, a figure that tells a sharper story about where Australia’s largest business lender sees conditions heading. The result landed on 4 May 2026, the same session in which Accent Group cut second-half EBIT guidance by 21%, Endeavour Group flagged slowing sales and rising supply-chain costs, and Morgan Stanley downgraded Australia’s 2026 GDP growth forecast to 1.2%, well below the consensus 1.6%. NAB’s numbers are not an isolated data point. They are an entry into a broader pattern reshaping the ASX earnings season narrative. What follows dissects what NAB’s result actually reveals, how it connects to the wider downgrade wave, and what framework investors should use when headline beats are masking deteriorating quality underneath.

NAB beat the number, but the credit story tells a different tale

The positives were real. Cash earnings grew 2.3% half-on-half, beating consensus by 7.1%. Net interest margin came in at 1.81%, three basis points above the 1.79% expectation. The interim dividend held at 85 cents per share.

Then the credit line arrived. Impairment charges hit $706 million for the half, up 45.6% on the prior period.

The $706 million impairment figure represents a 45.6% surge on the prior half, the sharpest step-up in NAB’s provisioning in recent reporting periods.

The composition matters more than the total. Of that $706 million, $406 million reflects underlying charges on loans already showing stress. The remaining $300 million is a forward-looking collective provision build, driven by NAB raising its downside economic scenario weighting to 45%, a 2.5 percentage point increase. Management cited sector stress from Middle East fuel exposure as a specific overlay driver.

NAB shares fell as much as 4.0% intraday before settling around -1.5% by midday.

| Metric | Actual | Consensus / Prior Half | Variance |

|---|---|---|---|

| Cash Earnings Growth (HoH) | 2.3% | Consensus beat | +7.1% vs consensus |

| Net Interest Margin | 1.81% | 1.79% expected | +3 bps |

| Credit Impairment Charges | $706M | Prior half | +45.6% |

Over 40% of the total impairment charge reflects management’s deliberate positioning for worse conditions ahead, not losses already confirmed. That distinction changes how the result should be read.

When big ASX news breaks, our subscribers know first

What a 45% downside weighting actually means for credit risk

Banks do not wait for loans to default before recognising potential losses. Under current accounting standards, they model multiple future economic scenarios, assign probability weights to each, and provision accordingly. The result is a forward-looking estimate of expected credit losses that moves before confirmed defaults do.

The AASB 9 expected credit loss requirements mandate probability-weighted scenario modelling across the full lifetime of financial instruments, meaning the collective provision build that NAB recorded reflects a prescribed accounting methodology rather than discretionary conservatism.

Three steps determine the provision outcome:

- The bank constructs economic scenarios (base case, upside, downside) with different assumptions about unemployment, GDP, and asset prices.

- Each scenario receives a probability weighting reflecting management’s view of how likely that path is.

- Higher weighting on the downside scenario increases expected loss provisions, even when no additional loans have actually defaulted.

When NAB raises its downside weighting to 45%, it means the bank’s models are running a near-recession scenario almost half the time. That is a statement of macroeconomic conviction, not merely a conservative accounting choice.

The collective provision build did not emerge from NAB’s 4 May result in isolation: the bank had signalled the $300 million forward-looking overlay and its $1.8 billion capital initiative, including a discounted DRP and partial underwrite targeting a CET1 ratio above 12%, in an April disclosure that markets had already partially priced.

Why the Q1-to-Q2 acceleration matters more than the half-year total

NAB’s Q1 FY26 update in February 2026 recorded only $170 million in impairments from business and unsecured retail lending. Reaching $706 million for the full half means the bulk of the charge is concentrated in the second quarter.

This is not a steady-state elevated level. It is an acceleration, driven by updated economic overlays applied mid-period as new macro signals emerged. The timing pattern indicates a bank responding in real time to deteriorating conditions rather than adjusting at a scheduled review point.

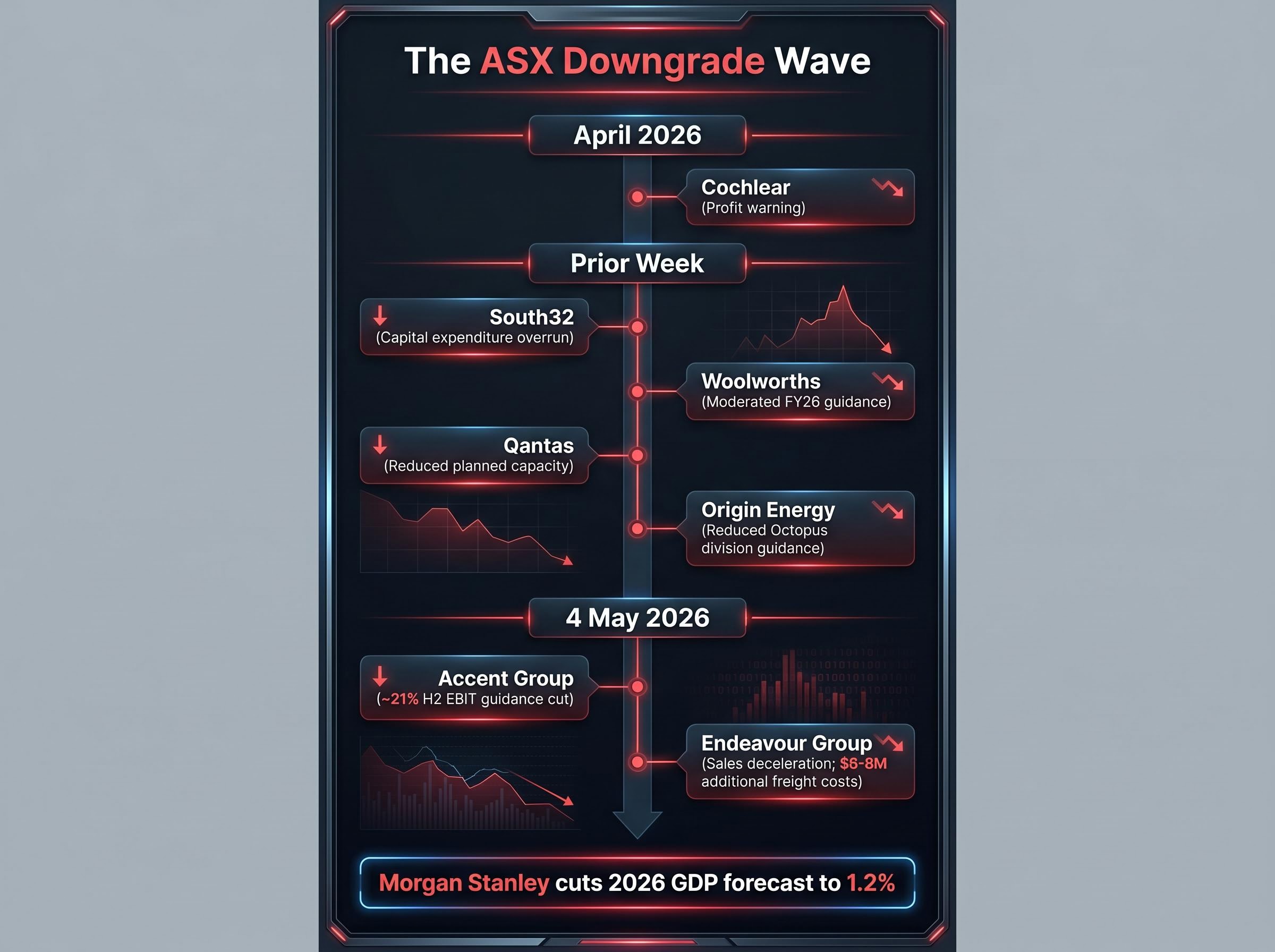

NAB is not the outlier: the ASX downgrade wave of the past week

The week leading into 4 May 2026 produced a sequence of negative revisions across unrelated sectors, building a pattern that became unmistakable by session’s end.

| Company | Announcement | Type | Timing |

|---|---|---|---|

| Cochlear | Profit warning | Earnings downgrade | April 2026 |

| South32 | Capital expenditure overrun | Cost guidance miss | Prior week |

| Woolworths | Moderated FY26 guidance | Outlook downgrade | Prior week |

| Qantas | Reduced planned capacity | Operational downgrade | Prior week |

| Origin Energy | Reduced Octopus division guidance | Divisional downgrade | Prior week |

| Accent Group | H2 EBIT guidance cut (~21% at midpoint) | Earnings downgrade | 4 May 2026 |

| Endeavour Group | Sales deceleration; $6-8M additional freight costs | Margin/revenue warning | 4 May 2026 |

Cochlear’s April profit warning now reads as a leading indicator rather than an isolated event. Endeavour Group’s retail sales growth decelerated from 1.3% in the first seven weeks of the second half to 0.7% on a comparable 16-week basis, while Hotels segment growth slowed from 4.5% to 1.5% across March and April.

UBS has flagged 25 ASX 200 stocks at risk of further earnings downgrades due to stagflation risks, signalling the pattern is unlikely to be exhausted by the companies that have already reported.

Morgan Stanley’s GDP downgrade reveals the macro engine behind corporate stress

Morgan Stanley’s 4 May 2026 note cut Australia’s 2026 GDP growth forecast to 1.2% year-on-year, down from a consensus of 1.6% and a 2025 actual of 2.6%. The deceleration is not modest. It represents a near-halving from the prior year.

Three headwinds underpin the downgrade:

Per capita recession conditions were already embedded in the Australian economy well before NAB’s provisioning signal: corporate insolvencies reached approximately 12,000 in 2025, the highest level since the 1990-91 recession, and real wages declined as Wage Price Index growth failed to keep pace with inflation, creating the household stress that is now flowing through into bank provisioning models.

- Persistent inflation driven by housing costs, wages, and government-administered prices that have proved resistant to prior tightening

- Rate cycle reinstatement: Australia is the only region globally to have recommenced a rate hiking cycle, with an 86% market-implied probability of a 25 basis point hike at the RBA’s 5 May 2026 meeting

- Energy price shock severity: Australia’s diesel price increase from February to April 2026 outpaced equivalent rises in Germany, the United Kingdom, France, Canada, the United States, and New Zealand

Morgan Stanley’s 2026 GDP forecast: 1.2% (vs 1.6% consensus, vs 2.6% actual in 2025), a trajectory that frames the current earnings deterioration as downstream of structural macro conditions.

With the ASX price-to-earnings multiple already having de-rated from approximately 20x to 17x, Morgan Stanley’s framing positions the risk as having shifted from valuation compression to earnings estimate cuts.

The RBA’s February 2026 economic outlook documented the board’s assessment of persistent inflation in housing costs, wages, and administered prices as central risks to the domestic growth path, the same cost pressures that Morgan Stanley’s May note identifies as drivers of its GDP downgrade.

Why Australia’s energy price exposure amplifies corporate cost pressure

Diesel price increases feed directly into freight, logistics, and input costs across the listed corporate sector. Endeavour Group’s disclosure of $6-8 million in additional freight and fuel costs, and NAB’s decision to apply a Middle East fuel sector overlay to its provisioning, are both downstream consequences of the same energy price dynamic that Morgan Stanley identifies as disproportionately severe for Australia relative to comparable economies.

What investors should actually scrutinise during this earnings season

NAB’s result crystallises a problem that will recur throughout this reporting period: a headline beat can coexist with deteriorating underlying conditions. Investors who stop at the top-line number will miss the signal.

A four-point checklist applies to every result from here:

- Impairment composition: Separate forward-looking provisions from confirmed losses. The ratio reveals management’s macroeconomic conviction, not just the current state of the loan book.

- Guidance language on macro overlays: Listen for changes in scenario weightings, economic assumptions, or specific risk factors cited in management commentary.

- Gross margin trajectory: Identify freight, fuel, and input cost pass-through pressure. Where margins are compressing despite stable revenue, cost absorption is eroding quality.

- Divisional revenue deceleration: Total revenue can hold up while individual segments deteriorate. Endeavour’s Hotels growth slowing from 4.5% to 1.5% in March and April is the type of signal that a headline number obscures.

Sectors most exposed to the current stress pattern

Consumer discretionary, banking and financials, and logistics-exposed industrials are the three sectors most directly aligned with the risk factors Morgan Stanley and UBS have highlighted. Broker rating changes on ANZ and Qantas on 4 May 2026, which mostly maintained ratings while trimming price targets, reflect a market still assigning resilience while quietly reducing upside. That pattern is consistent with earnings quality deterioration rather than outright failure.

The ASX 200 declined 33 points (-0.38%) by midday, a measured initial verdict that may understate the cumulative weight of the session’s negative signals.

ASX market breadth tells a sharper story than the headline index decline: 22 ASX 200 constituents hit fresh 52-week lows in the week ending 1 May 2026, doubling the prior week’s tally, with Consumer Discretionary accounting for seven of those new lows as the Westpac-Melbourne Institute Consumer Sentiment Index collapsed to 80.1.

The earnings beat that should put investors on alert, not at ease

The 4 May 2026 session delivered a single, coherent message across multiple data points: headline resilience is masking a widening quality gap underneath. NAB beat earnings by 7.1% and simultaneously revealed a 45.6% impairment surge. Accent Group cut guidance. Endeavour Group flagged cost and revenue pressure. Morgan Stanley downgraded GDP. These are not coincidences.

The defining juxtaposition of this ASX earnings season: a 7.1% headline earnings beat sitting alongside a 45.6% credit impairment surge, in the same result, from the same bank.

The genuine positives deserve acknowledgement. NAB’s NIM improvement is real. The 85 cent dividend is maintained. NAB shares have outperformed the ASX 200 by roughly 22% to 6% over the past 12 months, rising from approximately $37.1 to approximately $45.25. These are not the characteristics of a failing institution.

Dividend discount valuation applies differently when payout ratios are sustained against a backdrop of rising provisions: NAB’s adjusted payout ratio of 72.5% on maintained 85 cent dividends looks defensible in isolation, but a model that discounts future dividends using a discount rate calibrated to current RBA tightening and rising credit costs will produce a materially lower intrinsic value than one anchored to the prior rate environment.

They are, however, insufficient to neutralise the provisioning signal. With the P/E de-rating from 20x to 17x already absorbed, the next leg of downside risk depends on whether consensus earnings per share forecasts are revised lower. The pattern visible on 4 May 2026, corporate stress signals arriving across unrelated sectors, driven by a macro environment Morgan Stanley describes as structurally challenging, is exactly the kind of evidence that accelerates those cuts.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.