CURE and CLNE: the ASX ETFs Returning 25% in 2026

7 hrs ago

The ASX 200 has already done the hard work of de-rating. Over the past 12 months, the index’s forward price-to-earnings ratio has compressed from roughly 20x to approximately 16.8x to 17x, absorbing higher bond yields, a hawkish Reserve Bank, and a string of earnings downgrades in domestic cyclicals. The multiple is down. The question that remains is whether the earnings embedded in that multiple can actually be delivered. Morgan Stanley, UBS, and J.P. Morgan have each arrived at the same conclusion from different angles: the risk that defines the second half of FY26 is not further valuation compression but earnings execution. With Australian 10-year bond yields at approximately 5.1% and the RBA explicitly refusing to rule out further rate increases, the ASX 200 valuation leaves little room for disappointment. This analysis examines where that earnings risk is concentrated, which sectors face the sharpest pressure from a higher-for-longer rate environment, and what the current setup means for investors reassessing domestic equity allocation.

The de-rating is a completed event. The ASX 200’s forward P/E contracted from approximately 20x to around 16.8x to 17x over the prior 12 months, a significant adjustment that priced in persistently higher interest rates and a more cautious earnings outlook. For investors who watched the drawdown unfold, the instinct is to read a lower multiple as a safer market.

That instinct is wrong in this context.

The compression from 20x to 17x forward earnings is the product of the discount-rate channel working precisely as theory predicts: as bond yields rise, the present value of future corporate cash flows shrinks, and multiples contract even when no earnings revision has occurred.

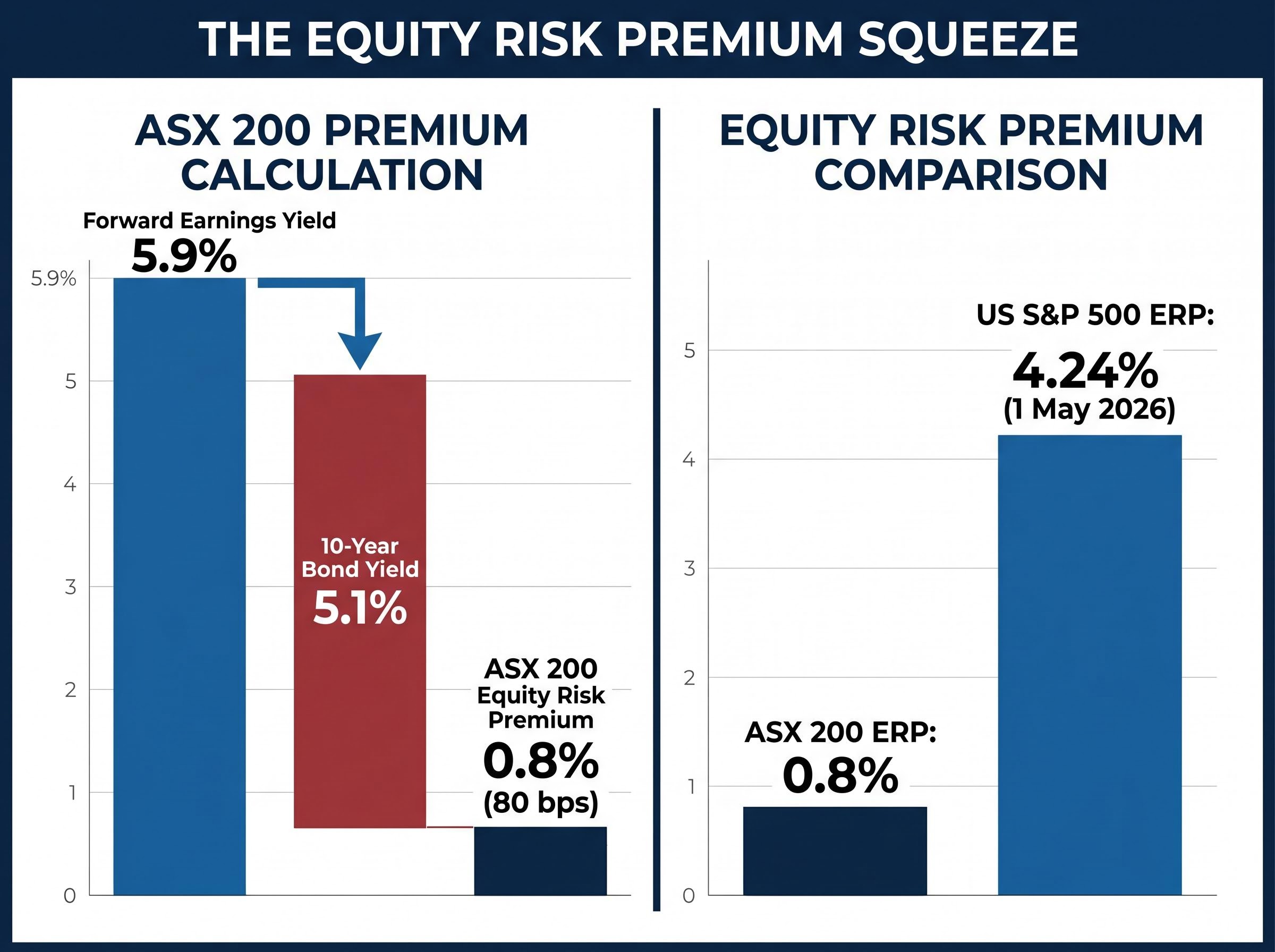

At 17x forward earnings, against an Australian 10-year bond yield of 5.1%, the index sits at a boundary rather than deep inside a comfortable valuation zone. Morgan Stanley’s mid-year equity strategy framed the position precisely.

Morgan Stanley noted that a forward P/E of 16.9x sits “at the upper boundary of the range historically consistent with Australian 10-year bond yields in the 5% to 6% band.”

The boundary distinction matters because it determines what the market is actually pricing. Three data points frame it:

A market sitting at the upper boundary of its historically consistent range is not discounting earnings failure. It is pricing in earnings delivery. That distinction changes the risk equation entirely: returns from here are almost wholly dependent on whether FY26 profits materialise as forecast.

A forward P/E of 17x sounds moderate in isolation. It is below the long-run average and well below the 20x the index traded at a year ago. Taken alone, it could suggest a market that has already adjusted.

The P/E ratio, however, does not account for the return available from competing alternatives. A 17x multiple when government bonds yield 2% is a very different proposition from a 17x multiple when government bonds yield 5.1%. The equity risk premium is the corrective lens: it measures the extra return investors receive for holding equities over risk-free government debt.

The mechanism is direct. As bond yields rise, the hurdle rate for equities rises with them. Investors demand a wider premium to justify the additional risk of owning shares. If that premium compresses, it means equity holders are accepting less compensation for more risk, or the market is betting that earnings growth will deliver the gap.

Applied to the ASX 200 right now, the arithmetic is tight. The forward earnings yield (the inverse of 17x) is approximately 5.9%. Subtract the 10-year bond yield of 5.1%, and the premium investors are earning for holding Australian equities over government bonds is roughly 80 basis points.

| Metric | Current reading | Implication |

|---|---|---|

| Forward P/E | ~17x | Fully valued at current yields |

| 10-year bond yield | ~5.1% | Compresses equity risk premium |

| Forward earnings yield | ~5.9% | Only 80bp above risk-free rate |

| Equity risk premium | ~0.8% | Historically thin |

For context, New York University’s Aswath Damodaran estimated the US S&P 500 implied equity risk premium at 4.24% as of 1 May 2026. The ASX 200’s 80 basis points is a fraction of that, reflecting how aggressively Australian bond yields have compressed the domestic premium.

The compressed equity risk premium is not a new phenomenon confined to the current reporting season; analysis from earlier in May identified a near-zero equity risk premium as one of three converging pressures on the Australian market, alongside a 13% global oil supply deficit and Budget-driven capital reallocation.

UBS argued that a P/E near 17x “prices in a soft landing” and leaves “limited room for disappointment” if earnings miss.

“Fairly valued” in this environment is not a neutral position. It is a position where the margin of safety is thin and the cost of an earnings miss falls directly into price.

The headline consensus for FY26 ASX 200 earnings per share growth sits at approximately 10% to 11%. UBS revised its forecast down from 12% to 10% in late May. Goldman Sachs estimated roughly 11%. Those numbers sound healthy for a market that has already de-rated.

The composition of that growth tells a different story.

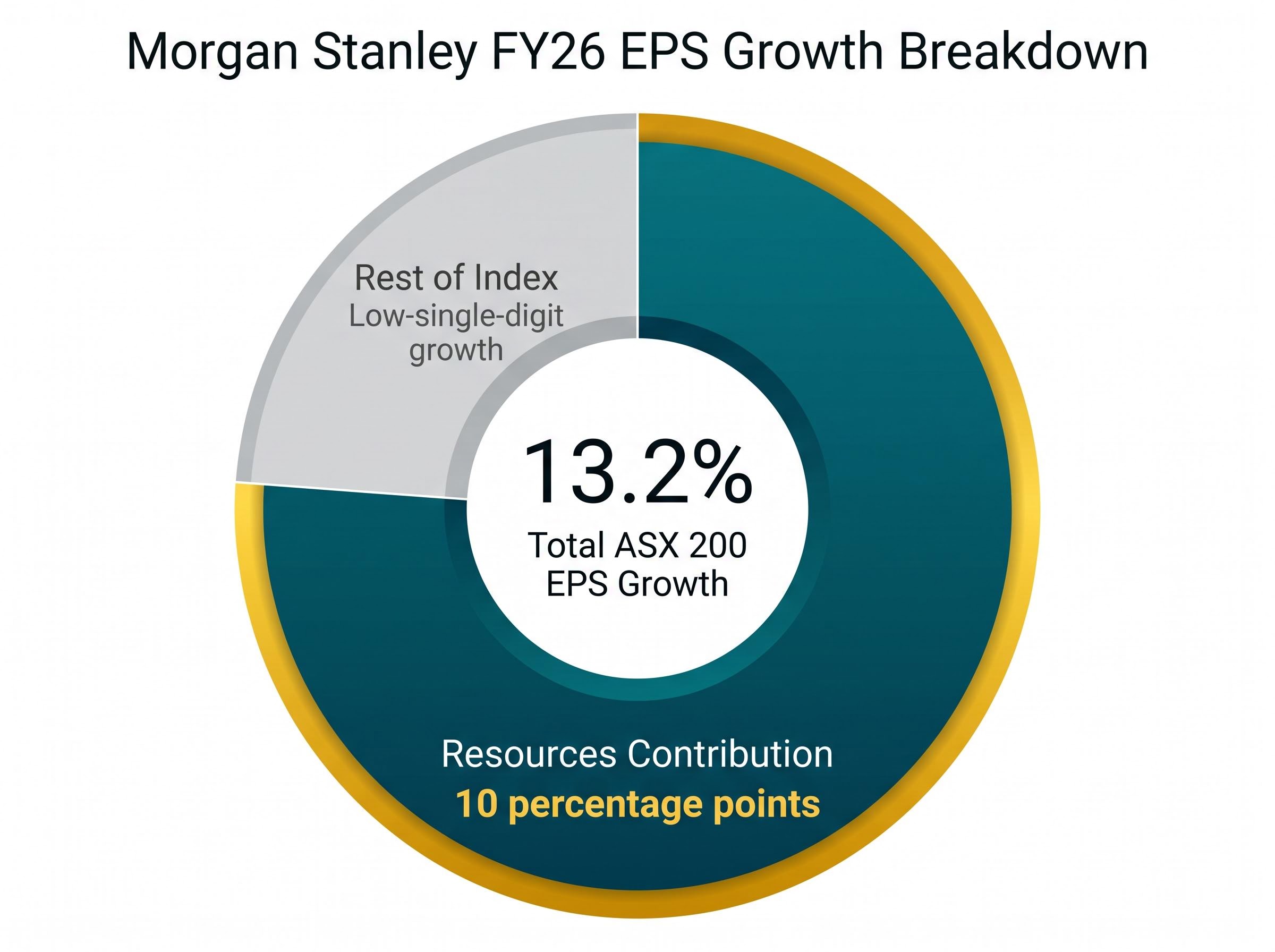

Morgan Stanley’s earlier FY26 EPS forecast of approximately 13.2% total growth attributed roughly 10 percentage points to the resources sector alone. Strip out resources, and the rest of the index was contributing low-single-digit earnings growth at best. UBS’s subsequent downgrade reinforced the pattern: the cut from 12% to 10% was driven by weaker outlooks for banks and consumer discretionary, not resources.

| Broker | FY26 EPS growth estimate | Key driver of revision |

|---|---|---|

| Morgan Stanley | ~13.2% | Resources-heavy baseline |

| UBS | 10% | Banks and discretionary cut |

| Goldman Sachs | ~11% | Resources providing large share of upside |

That concentration matters because the resources earnings outlook is a commodity price bet, and the commodity price outlook is far from certain. Iron ore (62% Fe CFR Qingdao) was trading at approximately US$111 to US$112 per tonne in mid-May, having recovered from below US$100 in April. The rebound was driven by expectations of additional Chinese policy support. Broker forecasts, however, point to range-trading or a gradual drift lower rather than a sustained new plateau:

For investors assessing domestic equity exposure, understanding that a large portion of index EPS growth is effectively a wager on Chinese commodity demand, rather than a domestic earnings story, changes the nature of the risk being taken.

The macro conditions creating earnings pressure are not abstract. The RBA held the cash rate at 4.35% at its May 2026 meeting. The Board Minutes, released on 21 May 2026, revealed that the Board actively discussed the case for a rate increase and explicitly stated that “a further increase in interest rates cannot be ruled out.” The 2026-27 Federal Budget, released on 14 May, offered limited fiscal offset, with economists characterising it as broadly neutral to slightly disinflationary.

The RBA May 2026 monetary policy statement confirmed the Board’s assessment that inflation risks remained elevated and that restrictive policy settings were necessary to return inflation to target within a reasonable timeframe, providing the formal basis for the explicit warning that further rate increases could not be ruled out.

Those conditions are already showing up in company guidance.

JB Hi-Fi issued a trading update in mid-May flagging softer like-for-like sales growth in the March to April period. Management warned that FY26 sales and margin growth would be “more challenging” than previously anticipated. Brokers including Morgans and Macquarie trimmed FY26 earnings forecasts following the update.

Harvey Norman went further. The retailer warned that profit for the second half of FY26 was likely to come in below the prior year, citing weak furniture and electrical demand linked to softer housing turnover. Analysts expected further consensus downgrades.

The pattern of earnings quality deterioration beneath headline beats is documented in detail across the current reporting season, with NAB’s 7.1% cash earnings beat sitting alongside a 45.6% surge in credit impairment charges and UBS identifying 25 ASX 200 names still at risk of further downgrades.

Regional banks delivered similarly cautious signals. Both Bendigo and Adelaide Bank and Bank of Queensland cautioned about rising funding costs and normalising bad debts during May. UBS and Goldman Sachs slightly reduced FY26 EPS estimates for these names.

The dynamic is counterintuitive: high interest rates benefit net interest margins in isolation, but the offsetting drag from rising bad debts and higher funding costs is now dominating broker models for the sector. J.P. Morgan recommended underweight positions in both banks and discretionary retail, citing the RBA’s stance as implying “restrictive conditions well into FY27.”

The valuation analysis, the earnings concentration data, and the sector-level guidance signals converge on a specific asymmetry. At current prices, the risk-reward skew is unfavourable for domestic demand-sensitive exposures and more balanced for resources and defensives.

The strategist positioning reflects this. Platinum Asset Management has characterised Australian equities as “fully valued,” flagging resources and defensives as more attractive than domestic cyclicals. J.P. Morgan recommends underweights in banks and discretionary retail. Magellan offered the sharpest framing of the risk.

The household demand weakness showing up in retail guidance is consistent with a broader macroeconomic picture: per capita output contraction of roughly 0.7% across 2025, corporate insolvencies at their highest level since the 1990-91 recession, and consumer confidence at a 50-year low all preceded the current earnings downgrade cycle.

Magellan noted that the ASX 200 valuation leaves “little margin of safety” if the RBA has to keep policy restrictive into FY27, highlighting banks and consumer stocks as most exposed to downgrades.

The resources caveat deserves explicit acknowledgement. Stability in resources earnings is conditional on Chinese stimulus continuation, and broker consensus points to range-trading commodity prices rather than a fresh upside catalyst. The floor is firm, but the ceiling is limited.

| Sector | Earnings revision direction | Strategist view | Key risk |

|---|---|---|---|

| Banks | Negative | Underweight (J.P. Morgan) | Funding costs and bad debts |

| Consumer discretionary | Negative | Underweight (J.P. Morgan) | Household rate pressure |

| Resources | Broadly stable | Neutral to constructive | Commodity price dependency on China |

| Defensives | Stable | Relatively attractive (Platinum) | Limited upside but limited downside |

FY26 EPS downgrades have been concentrated in banks and consumer discretionary, not resources. That pattern is consistent across UBS, Goldman Sachs, and J.P. Morgan, and it gives investors a sector-level signal grounded in revision data rather than directional opinion.

A 17x multiple against 5.1% bond yields is not a catastrophe signal. It is a market that has stripped out its own margin for error.

The equity risk premium of approximately 80 basis points is the thinnest buffer the ASX 200 has carried in this rate cycle. FY26 EPS growth of approximately 10% to 11% is already embedded in the price, and roughly 10 percentage points of that, according to Morgan Stanley’s decomposition, is contingent on resources sector performance and Chinese demand remaining supportive.

Morgan Stanley emphasised that the key risk has shifted “from multiple de-rating to earnings delivery for FY26.”

The valuation debate is largely settled. The rate debate has clarity: higher for longer, with limited fiscal offset and the RBA explicitly keeping further increases on the table. The only question that remains is execution: whether the earnings the market has priced in will arrive.

The question for investors is not whether to hold domestic equities. It is which parts of the domestic market are pricing in a scenario that underlying earnings can plausibly support.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

As of May 2026, the ASX 200 forward price-to-earnings ratio sits at approximately 16.8x to 17x, down from around 20x a year earlier, with an equity risk premium of roughly 80 basis points above the 5.1% Australian 10-year bond yield.

The equity risk premium measures the extra return investors earn for holding shares over risk-free government bonds; at roughly 80 basis points above the current 5.1% bond yield, the ASX 200's premium is historically thin, meaning investors are receiving very little additional compensation for taking on equity risk.

Banks and consumer discretionary stocks face the sharpest downgrade risk, with companies like JB Hi-Fi, Harvey Norman, Bendigo Bank, and Bank of Queensland all issuing cautious guidance, while J.P. Morgan recommends underweight positions in both sectors.

According to Morgan Stanley's analysis, roughly 10 percentage points of the approximately 13% FY26 EPS growth forecast comes from the resources sector alone, meaning the headline index growth figure is heavily dependent on Chinese commodity demand rather than broad domestic earnings strength.

The RBA held its cash rate at 4.35% at its May 2026 meeting and explicitly stated that a further rate increase cannot be ruled out, which continues to pressure funding costs for banks, squeeze household budgets in consumer-facing sectors, and limit the equity risk premium available to ASX investors.