CURE and CLNE: the ASX ETFs Returning 25% in 2026

3 hrs ago

On 13 July 2026, Bernstein analyst David Dai published a client note that directly challenges one of the most common assumptions in semiconductor investing: that equipment stocks and memory stocks move together. Most investors group them instinctively. Both sit inside “semiconductors.” Both respond to chip demand. The assumption feels safe.

It is not. Bernstein’s data, spanning more than a decade and multiple full cycles, shows the two segments run on fundamentally different clocks. Memory prices are driven by supply-demand cycles in commodity chips. Equipment revenues are driven by capital expenditure commitments made quarters or years before those prices peak or crash. The timing mismatch is structural, not random, and it produces divergence windows large enough to reshape portfolio outcomes.

Here is the framework for separating two exposures that look identical from the outside but behave very differently in practice, built on two decades of correlation data, two documented divergence windows exceeding 38 and 49 percentage points, and a live market rotation already underway in Korea.

The shortcut is familiar. Samsung, SK Hynix, and Micron produce memory chips. ASML, Applied Materials, Lam Research, and KLA build the machines that make those chips. Both sit in the semiconductor sector. Both respond to the AI spending cycle. So investors group them into a single “semis” bucket, size them together, and assume that what is good for one is good for the other.

That conflation is structurally wrong, for two reasons.

First, the drivers are different. Memory prices move on supply-demand dynamics in commodity chips: DRAM and NAND prices boom, manufacturers over-invest, supply floods in, prices crash, and the cycle repeats. Equipment revenues move on capex commitments, the spending decisions that Samsung, SK Hynix, and Micron lock in quarters or years before the associated memory price peak or subsequent crash.

The memory chip supercycle now unfolding differs structurally from prior DRAM cycles, with AI data centres accounting for an estimated 70% of total memory shipments and SK Hynix shifting to multi-year foundry-style supply agreements extending through 2028-2030, conditions that affect how quickly oversupply can emerge and how far in advance capex commitments must be made.

Second, the timing is different. Equipment order books fill while memory prices are still rising. Equipment backlogs remain supported even after memory prices roll over. The result is a repeatable, predictable divergence between the two segments at cycle turning points.

The key structural differences:

An investor who treats these as interchangeable is not just being imprecise. They are likely misreading their own risk exposure in a way that can produce unexpected losses at exactly the points in the cycle where the two segments diverge most sharply.

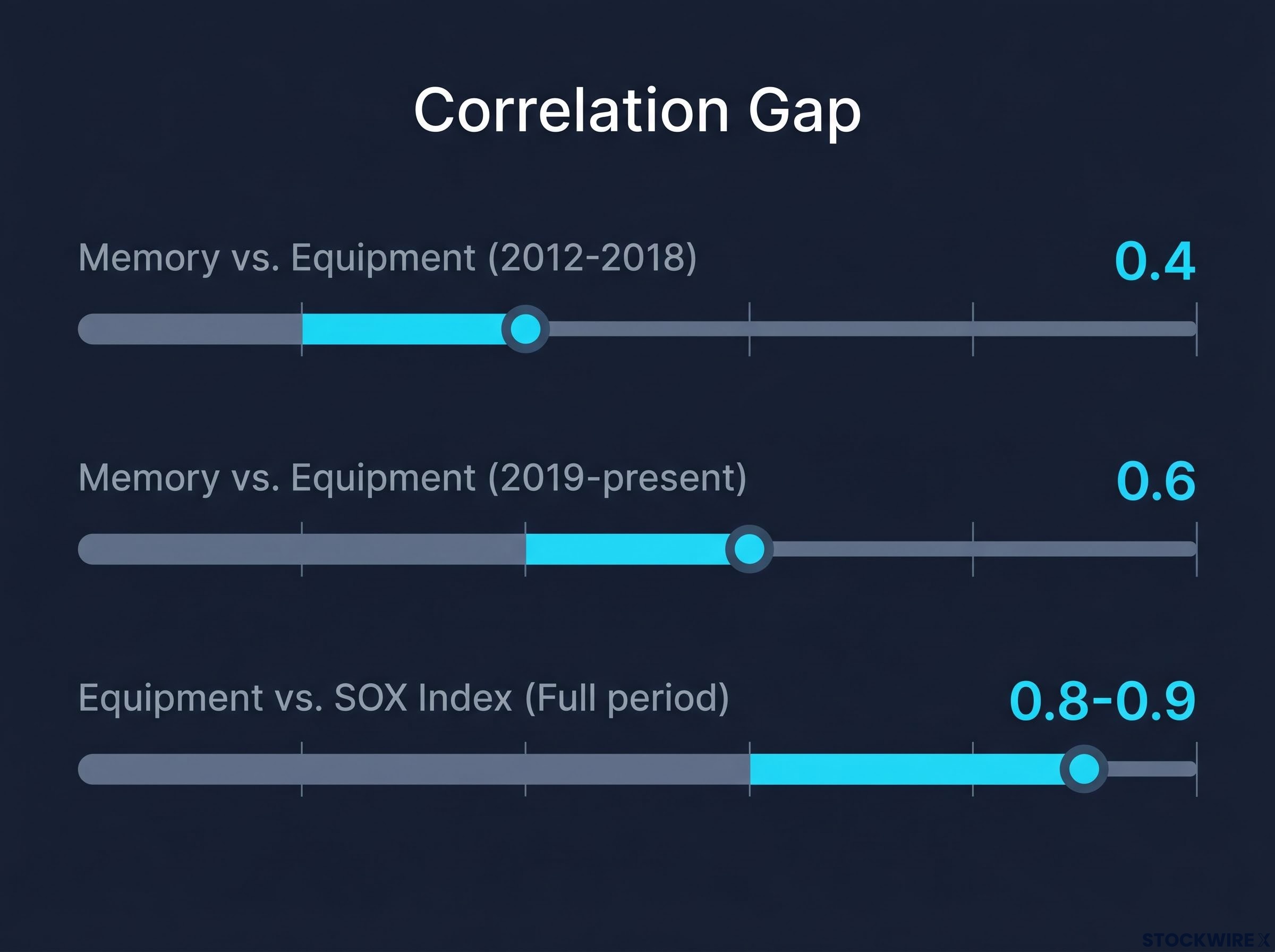

Bernstein’s quantitative work puts hard figures on the gap. David Dai’s analysis found that across the 2012 to 2018 period, price correlation between the leading memory producers and the five biggest wafer fabrication equipment companies came in at just 0.4.

A correlation of 0.4 means roughly 84% of the variance between the two is unexplained by the other. These are genuinely distinct bets, not two expressions of the same trade.

The picture shifted after 2019, with the correlation climbing, though it reached only 0.6. That is a tighter relationship than the prior period, but still well short of the near-lockstep movement most investors assume.

The capex-to-revenue lag that Morningstar analyst Dennis Li identified as an 18-24 month risk sits at the heart of the equipment timing advantage: equipment revenues recognise the capex commitment well before the memory price peak that the same commitment eventually produces, which is the structural mechanism that creates divergence windows rather than synchronised returns.

The comparison that reframes the picture sits in the third figure. According to Bernstein, the relationship between equipment stocks and the broader SOX semiconductor index has held consistently at 0.8-0.9 across the full period measured. Equipment is far more tightly bound to the semiconductor complex as a whole than to memory specifically.

The SOX index composition and weighting illustrates the point directly: memory names like Micron sit alongside equipment names like Applied Materials, Lam Research, and ASML inside the same index, giving broad semiconductor ETF holders simultaneous but structurally distinct exposures they may not be pricing separately.

| Pair Compared | Time Period | Correlation Coefficient |

|---|---|---|

| Memory vs. Equipment | 2012-2018 | 0.4 |

| Memory vs. Equipment | 2019-present | 0.6 |

| Equipment vs. SOX Index | Full period | 0.8-0.9 |

The counterintuitive finding: Equipment stocks correlate at 0.8-0.9 with the broader SOX index but only 0.4-0.6 with memory. Using an equipment basket as a memory proxy is a category error in portfolio construction.

What this means practically: if you hold both memory and equipment positions and assume they provide the same exposure, you are likely carrying concentration risk you have not accounted for, while simultaneously missing the diversification benefit that separating them would provide.

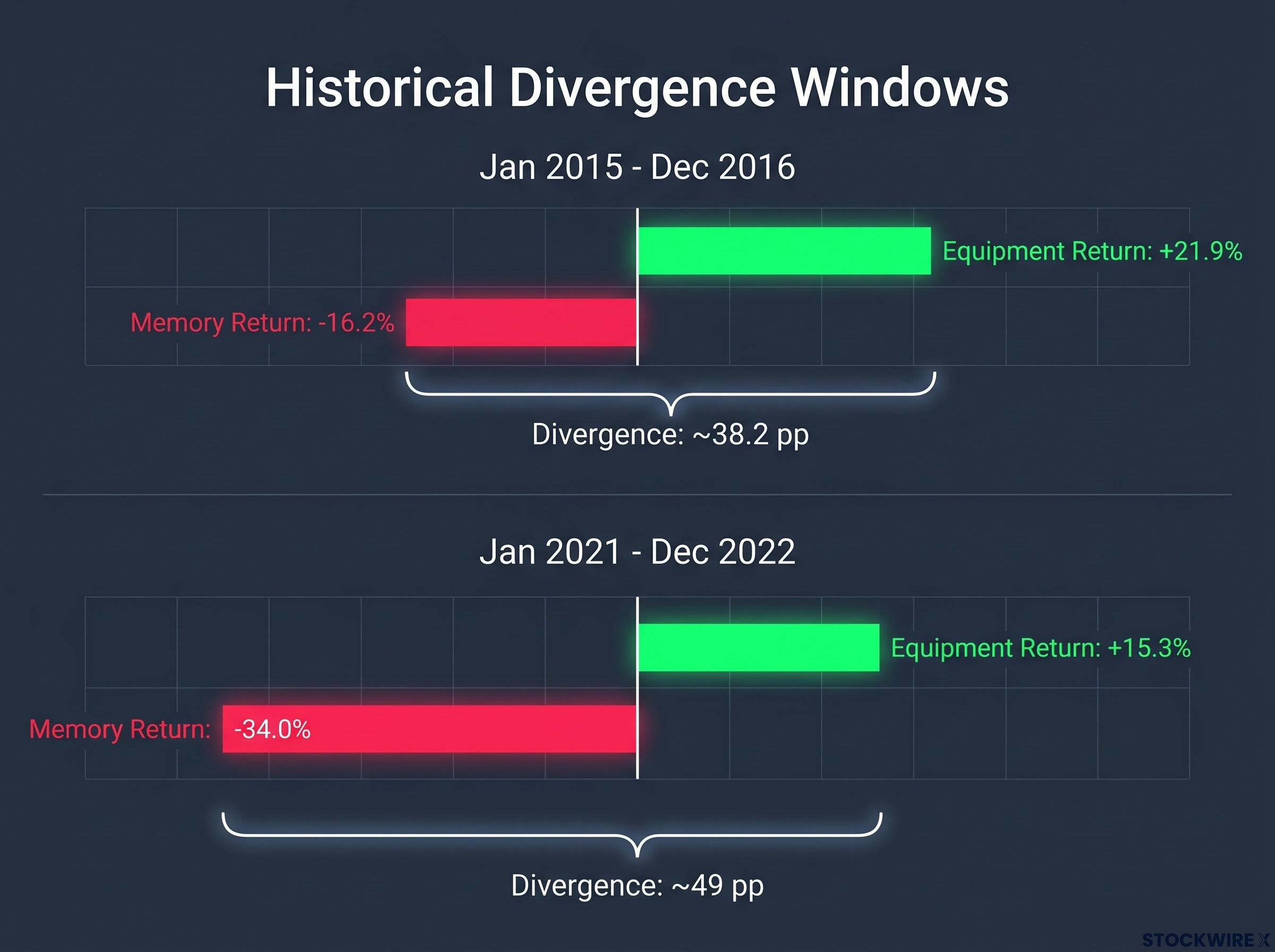

The correlation figures describe the structural gap. The historical divergence windows show what that gap looks like in actual returns.

January 2015 to December 2016 was the first documented case. Bernstein’s data shows that across those two years, wafer fabrication equipment stocks delivered a gain of approximately +21.9% while memory stocks declined by roughly -16.2%, producing a spread of approximately 38.2 percentage points between the two. Equipment was in an up-cycle driven by capex commitments locked in during the prior memory boom. Memory was already rolling over as supply caught up with demand. Same sector. Opposite outcomes.

January 2021 to December 2022 produced an even wider gap. Per Bernstein, equipment stocks advanced approximately +15.3% over that period while memory stocks declined approximately -34.0%, with the total spread between the two legs reaching close to 49 percentage points. This period coincided with intense broader market volatility, and many investors experienced it as a general semiconductor selloff. It was not. The equipment leg held up while the memory leg collapsed.

| Period | Equipment Return | Memory Return | Divergence |

|---|---|---|---|

| Jan 2015 – Dec 2016 | +21.9% | -16.2% | ~38.2 pp |

| Jan 2021 – Dec 2022 | +15.3% | -34.0% | ~49 pp |

49 percentage points of divergence over two years. That is large enough to meaningfully change portfolio outcomes. An investor who held both as separate, distinctly sized positions experienced a fundamentally different result from one who treated them as interchangeable semiconductor exposure.

Neither period was an anomaly. Both were predictable consequences of the capex-versus-price-cycle timing mismatch. And the current cycle is setting up conditions for the next one.

The AI spending wave has created exactly the kind of environment where memory and equipment start pulling apart.

Here is the sequence, drawn from Bernstein’s cycle framework:

Bernstein’s forecast places the memory price peak in H1 2027, followed by a downturn into 2027-2028 as new Chinese and upgraded capacities arrive (this specific timing is drawn from Perplexity-sourced reporting and was not independently confirmed). If that timeline proves correct, the period between now and H1 2027 represents the window where holding equipment and memory as separate, distinctly sized positions matters most, because the two legs of the trade could move in opposite directions, precisely as they did in 2021-2022.

SK Hynix’s $29 billion capacity expansion, scheduled to begin producing from H1 2027, is the textbook supply response that has historically closed memory upcycles, and the memory cycle reversal it represents carries exactly the kind of earnings and multiple compression timing that makes separating equipment and memory exposure most consequential.

Live market evidence suggests active capital is already positioning for this divergence. On 1 July 2026, foreign investors in Korea were selling large-cap memory names dominating the KOSPI while simultaneously buying semiconductor equipment, materials, and component stocks with smaller benchmark weights (this observation is drawn from Perplexity-sourced reporting and was not independently confirmed).

The pattern is consistent with how active capital has historically positioned ahead of memory cycle peaks: rotating from front-end price exposure into back-end capital goods before the turn arrives. It corroborates the structural thesis, though it should be treated as illustrative context rather than confirmation.

The analytical framework translates into four specific portfolio construction principles:

That final point deserves its own space.

Correlation is regime-dependent. In macro stress events, rates shocks, geopolitical disruptions, and broad risk-off episodes where investors sell the entire technology complex indiscriminately, both memory and equipment can sell off together. The intra-sector diversification benefit disappears.

Sector-wide selloffs, including the 6.3% single-session rout recorded on 2 July 2026 where memory names like Micron and equipment names like Applied Materials and Lam Research fell in near-lockstep, are precisely the macro stress events where the intra-sector diversification benefit described above temporarily collapses.

The divergence is greatest during sector-specific rotations, exactly the kind of shift visible in Korea right now, where active capital differentiates between sub-sectors rather than dumping everything at once. The practical sizing implication: the portfolio benefit of separating these exposures is most reliable in normal-to-strong risk appetite environments and should be stress-tested against the assumption that it vanishes in a broad equity drawdown.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Memory prices and equipment order books are two separate clocks. Disciplined positioning in semiconductors requires tracking both simultaneously rather than assuming one tells you the time of the other.

Three variables are worth monitoring as the cycle approaches the Bernstein-forecast peak:

The historical pattern is clear. Divergence windows of 38 and 49 percentage points are documented precedents, not theoretical possibilities. The current AI-driven cycle, with Bernstein’s H1 2027 memory price peak forecast as a timing anchor, suggests the next window may be building now.

The precise timing of memory cycle peaks is uncertain, and investors should manage both positions with that uncertainty explicitly in view. But the investor who tracks two clocks separately is positioned to act on divergence when it arrives. The one who conflates them will likely misread both signals, and either exit too early or stay in too long on the wrong leg of the trade.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Semiconductor equipment stocks are companies like ASML, Applied Materials, Lam Research, and KLA that manufacture the machinery used to produce chips, while memory stocks like Samsung, SK Hynix, and Micron produce the chips themselves. The two segments run on different revenue clocks: memory earnings respond directly to spot and contract chip prices, while equipment revenues are driven by capex commitments made quarters or years earlier.

The divergence is structural: equipment order books fill while memory prices are still rising, and equipment backlogs remain supported even after memory prices roll over. This timing mismatch between capex commitments and memory price peaks produces documented spreads of 38 to 49 percentage points between the two segments at cycle turning points.

Bernstein's data shows equipment stocks correlate at 0.8-0.9 with the broader SOX semiconductor index across the full period measured, far tighter than the 0.4-0.6 correlation they carry with memory stocks specifically.

Memory contract price movements signal where capex commitments are heading, and equipment backlog and order announcements confirm the equipment leg is building or fading. Tracking capex guidance from Samsung, SK Hynix, and Micron on earnings calls provides early warning of whether the equipment cycle is accelerating or decelerating.

The intra-sector diversification benefit disappears during macro stress events, rates shocks, and broad risk-off episodes where investors sell the entire technology complex indiscriminately, causing both memory and equipment names to sell off in near-lockstep as occurred in the 6.3% single-session rout on 2 July 2026.