CURE and CLNE: the ASX ETFs Returning 25% in 2026

8 hrs ago

Brent crude is sitting near USD $111 per barrel in mid-May 2026, having pulled back from a March peak above USD $126. On the surface, that looks like a market absorbing a supply shock and moving on. It is not.

The Strait of Hormuz has now been effectively closed for roughly ten weeks. The International Energy Agency (IEA) estimates global oil supply is down approximately 13%. Australian headline inflation has already reached 4.6% year-on-year to March 2026, with the Federal Budget forecasting a peak of 5.0% by the June quarter. Bond yields are near post-COVID highs. The equity risk premium on the ASX is compressed toward near-zero.

The calm in asset prices is not a sign of resilience. It is a sign that the full economic transmission of the shock has not yet arrived. This analysis explains why the pricing of risk in Australian markets may be materially wrong, what the historical precedent for delayed oil shock transmission reveals, and what portfolio positioning makes sense given the convergence of pressures building beneath the surface.

Brent’s retreat from USD $126 in March to approximately USD $111 as of 19 May 2026 has given markets something to feel optimistic about. The price action suggests a disruption being contained, supply finding alternative routes, and the worst passing.

The IEA’s numbers tell a different story. A 13% reduction in global oil supply is not a moderate disruption. It is the largest sustained supply deficit in decades, and at that scale, the current price implies markets are betting on a short-lived closure rather than a prolonged one.

The Hormuz supply disruption has removed an estimated 10.8 million barrels per day from global markets at its peak, a volume equivalent to roughly 80% of total US crude output, which explains why bypass pipeline infrastructure in Saudi Arabia and the UAE cannot arithmetically close the gap regardless of how aggressively those alternatives are utilised.

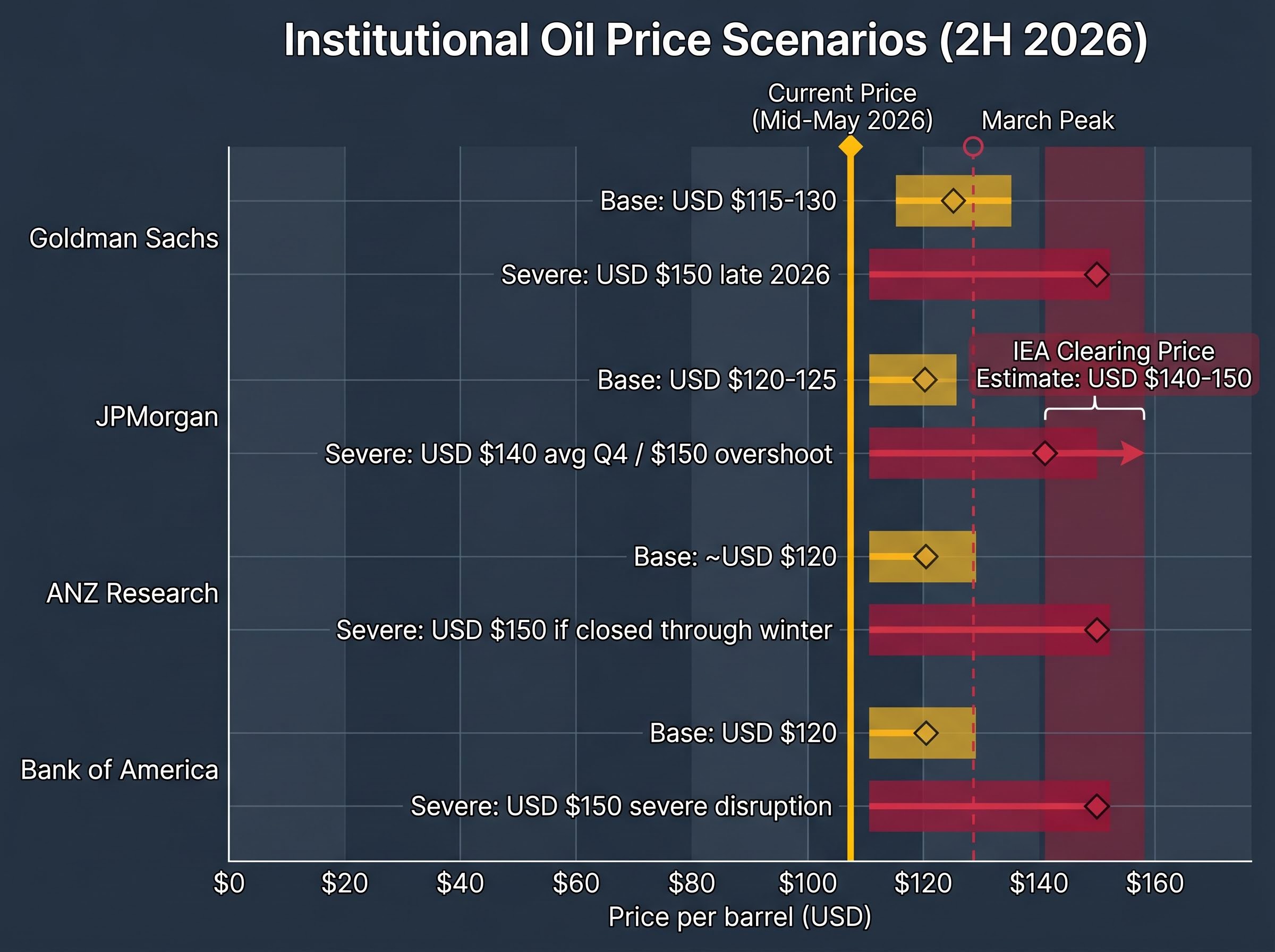

Major institutions are not making that bet. Goldman Sachs, JPMorgan, ANZ Research, and Bank of America all treat USD $140-150 per barrel as a plausible clearing price under sustained closure, not as an extreme tail scenario.

The IEA has framed USD $140-150 per barrel as the level at which “demand destruction and additional non-OPEC supply would clear the market” under prolonged disruption.

The gap between the current spot price and institutional upside scenarios is roughly USD $30-40 per barrel. That gap represents the market’s implicit assumption that the Strait reopens before the full supply deficit is priced in.

| Institution | Base Case (2H 2026) | Severe/Prolonged Scenario |

|---|---|---|

| Goldman Sachs | USD $115-130/bbl | USD $150/bbl (late 2026) |

| JPMorgan | USD $120-125/bbl | USD $140 avg Q4, overshoots to $150 |

| ANZ Research | ~USD $120/bbl | USD $150/bbl (if closed through winter) |

| Bank of America | USD $120/bbl | USD $150/bbl (severe disruption) |

If the closure persists, the market is not priced for the base case that institutional forecasters are modelling, let alone the upside scenarios.

The reason oil at USD $111 can coexist with a 13% supply deficit is that supply shocks do not arrive all at once. They are absorbed in stages, and each stage buys time before the next layer of economic damage materialises.

The cushioning mechanisms follow a predictable sequence:

Each of these mechanisms is currently active. Australian petrol prices remain only marginally above pre-conflict levels, according to Dr Shane Oliver of AMP, despite the excise cut already being in place. That looks like stability. It is actually a delayed fuse.

The pattern has played out before. The 1973 oil crisis took approximately four months before the full price transmission registered across the global economy. The 1979 crisis took over a year for the complete economic impact to materialise, as second-round effects through wages, transport costs, and manufacturing input prices compounded the initial shock.

The current Strait of Hormuz closure commenced in early March 2026. Ten weeks in, the Australian economy has recorded a 32.8% rise in automotive fuel prices in the month of March alone, per Budget Paper No. 1. Headline inflation has hit 4.6%. Yet the broader economic transmission, through freight costs, food prices, manufacturing inputs, and wage demands, is still in its early stages.

By the historical clock, the full repricing has barely started.

The oil shock is the risk Australian investors can see. The second risk is structural, embedded in valuations, and largely invisible to those not watching the bond market.

The equity risk premium (ERP) measures what investors receive for holding shares instead of government bonds. When bond yields are high and equity valuations are also high, the premium shrinks. In practical terms, a compressed ERP means investors are being paid very little extra return for taking on the additional risk of owning equities.

Australian and US equity risk premia have been compressed toward near-zero for approximately two years, according to commentary from Dr Shane Oliver at AMP. The 10-year Australian Government Bond yield sits at approximately 4.3-4.5% in mid-May 2026, near its post-COVID highs. KPMG’s Q1 2026 outlook noted that higher discount rates and softer earnings are capping equity valuations, describing the growth outlook as “fragile.”

Pitcher Partners (April 2026) described “little margin for error” in cyclicals, implying diminished equity risk compensation relative to higher bond yields.

A compressed ERP does not predict when a correction occurs. What it does is eliminate the buffer. There is no valuation cushion to absorb bad news.

The oil shock is precisely the kind of bad news this condition is exposed to. The feedback loop runs in one direction:

That reinforcing cycle is the structural vulnerability most Australian investors are not pricing. Two risks that look separate on paper, the oil shock and compressed valuations, are in fact a single interlocking problem.

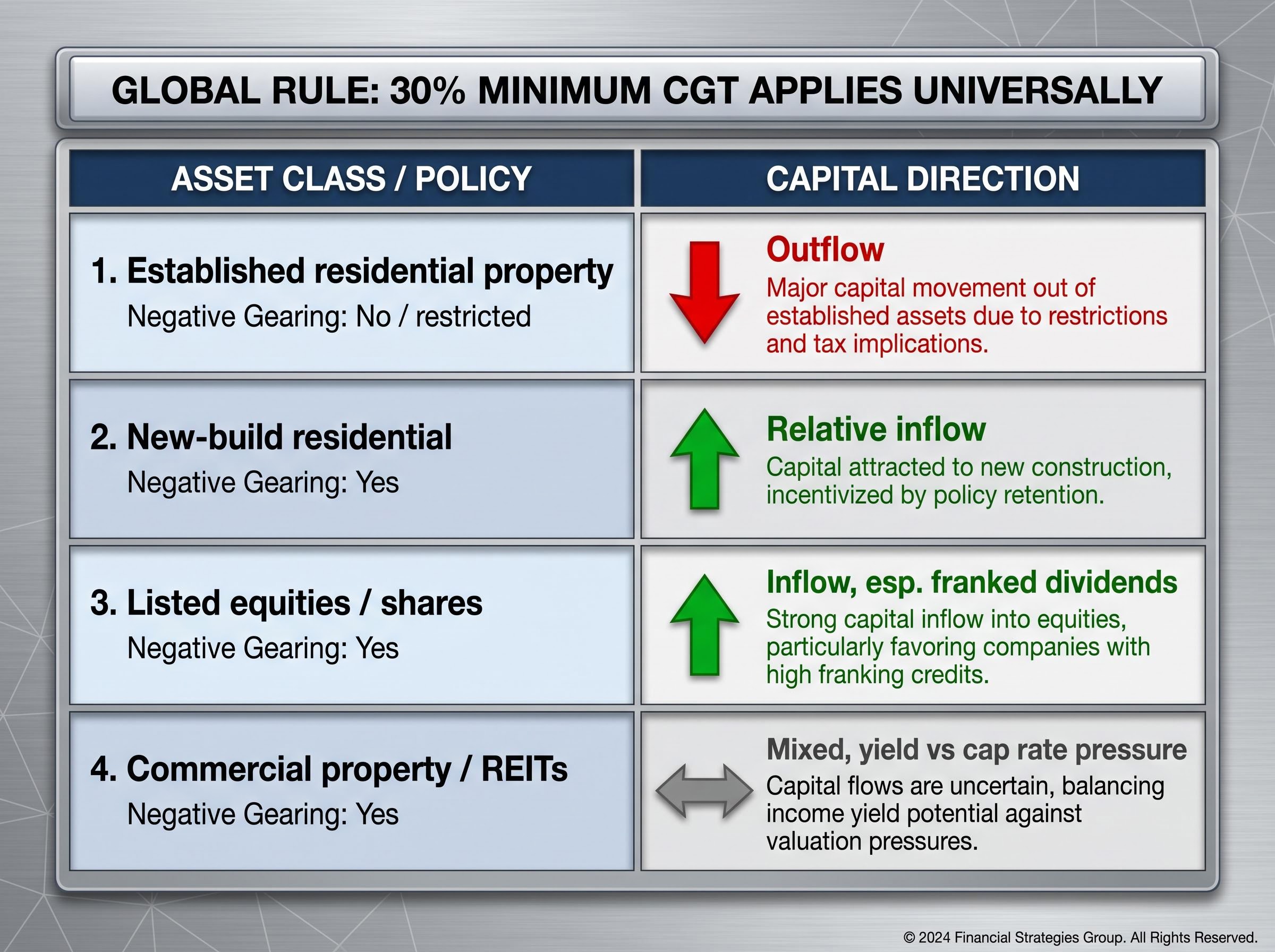

The May 2026 Federal Budget introduced a third layer of pressure. A 30% minimum capital gains tax rate now applies across all asset classes. Negative gearing has been restricted for established residential property, though new builds retain eligibility. A 30% minimum tax on discretionary trust distributions adds further friction to common wealth-structuring arrangements.

The reallocation signal is clear. Capital is being pushed away from speculative, capital-growth strategies (high-turnover trading, leveraged property on existing dwellings) and toward income-generating assets: fully franked dividend equities, fixed income, and superannuation.

Major bank economists at NAB, CBA, ANZ, and Westpac identify the negative gearing ring-fence as only the secondary behavioural driver for investors over the medium term, with the CGT discount replacement carrying greater financial consequence for most portfolios, a distinction that is easy to miss when the negative gearing headlines dominate Budget coverage.

The fiscal picture complicates matters further. The actual budget deficit of $64.1 billion is more than double the headline underlying deficit of $31.5 billion, according to Dr Shane Oliver at AMP. That gap represents near-term fiscal loosening that works against the Reserve Bank of Australia’s (RBA) inflation-reduction task, even as the 32-cent per litre fuel excise reduction and $250 tax offset payments (scheduled more than two years out) provide targeted household relief.

| Asset Class | Negative Gearing Retained | CGT Treatment | Likely Capital Direction |

|---|---|---|---|

| Established residential property | No (restricted) | 30% minimum CGT | Outflow |

| New-build residential | Yes | 30% minimum CGT | Relative inflow |

| Listed equities (shares) | Yes | 30% minimum CGT | Inflow (esp. franked dividends) |

| Commercial property / REITs | Yes | 30% minimum CGT | Mixed (yield vs cap rate pressure) |

The net effect on Australian Real Estate Investment Trusts (A-REITs) is ambiguous. Some retail capital displaced from direct residential property may flow into listed REITs for liquidity and professional management. However, higher cap rates driven by elevated bond yields work against REIT valuations simultaneously.

High-yielding equities with fully franked dividends, particularly banks, telcos, and utilities, are relative beneficiaries. Stable infrastructure distributions also gain appeal in an income-focused reallocation. The Budget is not just tax news; it is a structural shift in asset class attractiveness arriving at a moment when macro conditions are already making risk assets harder to own.

The RBA entered the oil shock already fighting a domestic inflation problem. Underlying inflation sat at approximately 3.3% year-on-year before the Iran conflict commenced, per Dr Shane Oliver at AMP. The Strait of Hormuz closure has layered an external supply shock on top of a pre-existing domestic challenge.

While headline CPI at 4.6% captured most of the attention, the trimmed mean held at 3.3% and came in below forecasts from NAB, consensus, and the RBA’s own February Statement on Monetary Policy, a divergence that matters for interpreting the August rate decision because the RBA’s weight on underlying versus headline inflation determines how aggressively it responds to an externally-driven price shock.

The three-part bind facing the central bank is difficult to resolve with a single policy lever:

The consensus rate path points to one further hike, likely in August 2026, taking the cash rate to the mid-4s. KPMG forecasts the cash rate at 4.60% in 2026, declining to 4.35% in 2027. QIC had expected a 25 basis point hike in May, bringing the rate to 4.35%. GDP growth is forecast to slow from 2.25% in 2025-26 to 1.75% in 2026-27 per the Budget.

The RBA’s May 2026 Statement on Monetary Policy confirmed the cash rate increase to 4.35% and projected underlying inflation remaining above the 2-3% target band until mid-2027, with the cash rate assumed to rise further to 4.70% by year-end, a materially more restrictive path than many leveraged investors had modelled entering 2026.

The Federal Budget forecasts underlying inflation returning sustainably to the RBA target band “in the middle of 2027,” a marker of how long the constrained rate environment is expected to persist.

For every leveraged Australian investor, from mortgage holders to margin borrowers to REIT unitholders, a cash rate peaking in the mid-4s and staying there until mid-2027 is a materially different environment from the rapid easing cycle many were expecting entering 2026.

The three risk vectors, oil supply shock, compressed equity risk premium, and Budget-driven reallocation, converge on a single portfolio-construction implication. Risk assets are harder to own at current valuations, not easier. The portfolios most exposed to what comes next are those built for a low-rate, low-inflation, high-multiple environment that has been structurally dismantled over the past ten weeks.

The consensus positioning tilt from fund managers and strategists in 2026 reflects that shift:

Overweights:

Underweights:

Some multi-asset managers are reassessing domestic versus global equity splits, with tilts toward global quality given better offshore bond yields and a soft Australian dollar that benefits exporters with USD revenue exposure.

For investors reassessing their domestic versus global equity split in light of these pressures, our full explainer on ASX home bias and global diversification examines the 10-year return gap between the ASX and global benchmarks, the structural sector concentrations that make a domestically-heavy portfolio a de facto bet on Australian banks and commodity cycles, and the conditions under which the franking credit advantage does and does not close the performance gap.

Selective energy and resources exposure makes sense as an inflation hedge when oil is the source of the inflationary pressure. Australian energy producers and resource exporters benefit directly from elevated commodity prices.

The risk that undercuts the thesis is demand destruction. If oil at USD $150 tips the global economy into a material slowdown, commodity prices fall alongside equities, eliminating the hedge benefit. The energy tilt works as long as the disruption remains a supply shock rather than tipping into a demand shock.

The moderation in oil prices from March peaks is not a signal of resolved risk. It is the signature of delayed transmission, and historical precedent says the full impact is still ahead. The ASX faces a three-part vulnerability: oil remains well below institutional clearing-price estimates under sustained closure, the equity risk premium provides no buffer against bad news, and Budget-driven reallocation is creating structural sector shifts that will reshape performance for the medium term.

Four variables will determine how the next six months unfold:

Repositioning while the market is still pricing partial disruption is the available window.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The equity risk premium (ERP) is the extra return investors receive for holding shares instead of government bonds. When the ERP is compressed toward zero, as it is in Australia in mid-2026, there is no valuation buffer to absorb bad news such as an oil shock or rising bond yields.

The closure has removed an estimated 10.8 million barrels per day from global markets, contributing to a 32.8% rise in Australian automotive fuel prices in March 2026 and pushing headline inflation to 4.6% year-on-year, with the Federal Budget forecasting a peak of 5.0% by the June quarter.

The Budget introduced a 30% minimum capital gains tax rate across all asset classes and restricted negative gearing to new-build residential property only, with the CGT change carrying greater financial consequence for most portfolios than the negative gearing restriction.

Consensus positioning tilts toward quality large caps with pricing power, cash and short-duration bonds, selective energy and resources exposure, fully franked dividend names such as banks, telcos and utilities, and global quality equities with US investment-grade credit.

The four critical variables are the duration of the Strait of Hormuz closure, the June quarter CPI print, the August RBA meeting decision and guidance, and OECD inventory drawdown levels, which together will determine whether the delayed oil shock transmission forces a broader repricing of Australian risk assets.