3 ASX Sector ETFs That Returned Up to 136% in One Year

3 hrs ago

Most retail traders notice that certain Thursdays feel chaotic on the ASX, with price moves that seem disconnected from any news. Positions that looked safe at 10:00 am are underwater by lunch, and by the afternoon the pressure has vanished as quickly as it arrived.

This is not random noise. It is a structural event called triple witching, where three classes of derivative contracts expire simultaneously on the ASX. The institutional hedging activity that unwinds around this event creates short-term price distortions, liquidity gaps, and sharp post-settlement moves that can punish traders who are positioned without understanding what is actually driving the market.

The quarterly ASX triple witching calendar is fixed and public. The mechanics behind the volatility are well understood by institutional desks. Here is the mechanical understanding and the specific tactical adjustments you need to trade confidently around this quarterly event, rather than being caught out by it.

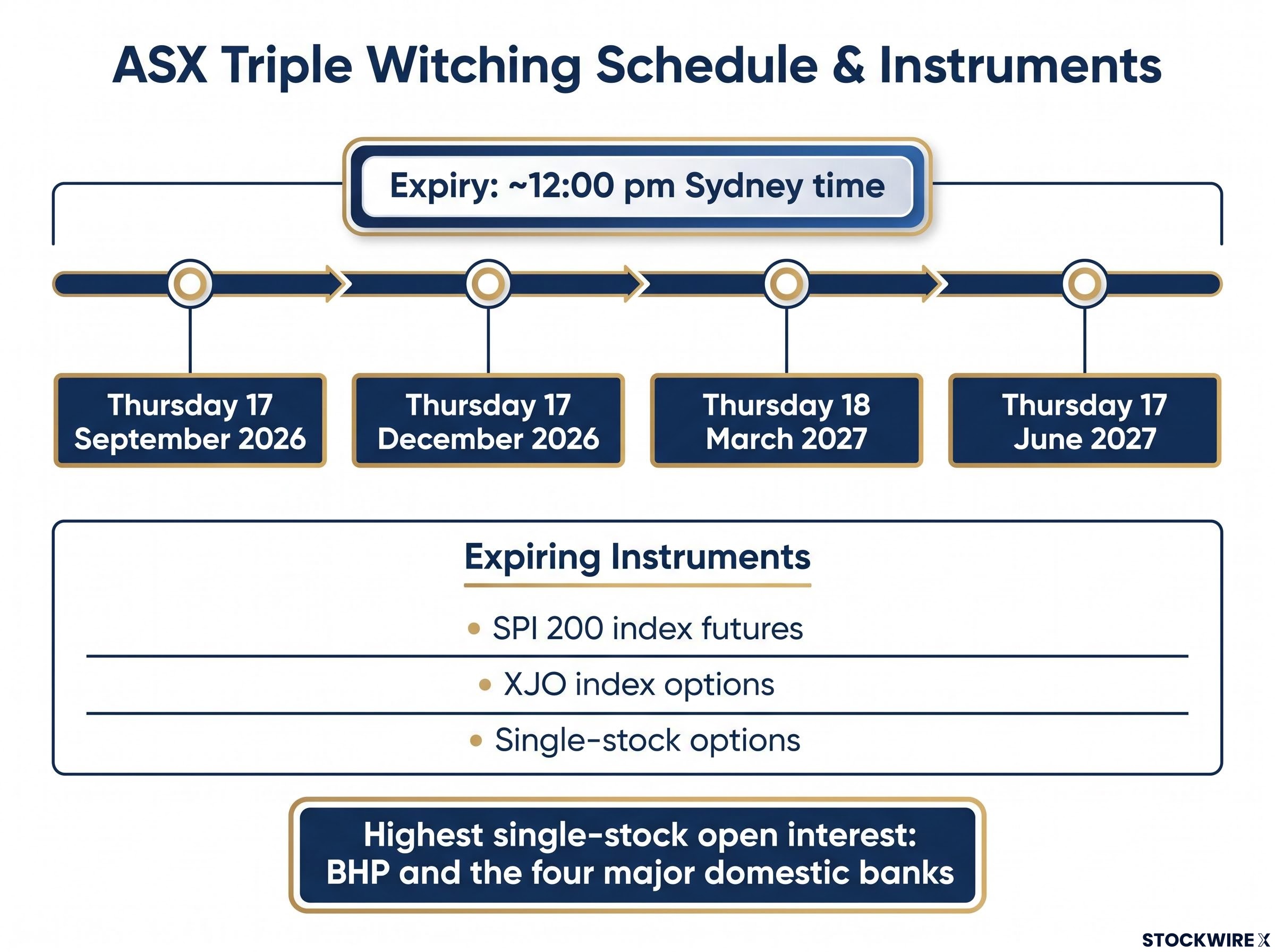

Four times a year, three derivative instruments expire on the same day on the ASX: SPI 200 index futures, XJO index options, and single-stock options. That simultaneous expiration is what “triple witching” refers to, and the dates follow a fixed quarterly pattern.

The expiry falls on the third Thursday of March, June, September, and December, with contracts ceasing to trade at approximately 12:00 pm Sydney time. Public holidays can shift the exact date, so you should verify the specific expiry day each quarter rather than assuming the third Thursday is always correct.

The upcoming ASX triple witching dates are:

The highest single-stock open interest typically concentrates in BHP and the four major domestic banks, making those names the most affected by expiry-day mechanics.

While US markets see expiry volatility build into the closing bell, the ASX settles its derivative contracts at roughly 12:00 pm Sydney time, which shifts the window of structural risk squarely into the middle of the trading day.

Knowing these dates in advance is itself a tactical advantage. The volatility that surrounds triple witching is structural and foreseeable, which means it is something you can prepare for rather than react to. Every other adjustment in this piece builds on that baseline: knowing when the event occurs and which instruments are involved.

If you have read expiry-day guidance written for US markets, the most important thing to understand is that the ASX stress window hits at a completely different time of day, and that difference changes everything about how you manage your risk.

On the ASX, the peak structural stress occurs in a midday window, approximately 11:30 am to 12:15 pm AEST, when expiring contracts settle and dealer hedging activity reaches its most intense point. In the US, triple witching volatility clusters in the final hour of trade on the third Friday. The difference is not cosmetic; it means intraday traders face the highest risk at lunch, not at end-of-day.

The ASX equity options contract specifications confirm that XJO index options are European style, exercisable only on the expiry date, with trading ceasing at 12 noon on the expiry Thursday, which is the structural basis for the midday settlement window that shapes every tactical adjustment in this guide.

| Attribute | ASX | US |

|---|---|---|

| Settlement day | Third Thursday | Third Friday |

| Settlement time window | ~12:00 pm AEST | Final hour of trade (US time) |

| Peak volatility cluster | 11:30 am – 12:15 pm AEST | 3:00 pm – 4:00 pm ET |

| Post-expiry gap risk | Elevated Monday open | Following Monday open |

There is also a compounding effect that stretches the risk window beyond Thursday. The Australian market wraps up its local expiry on Thursday around midday, and the US triple witching then plays out across the Friday Wall Street session, which falls on Thursday night for Australian traders. When the ASX reopens on Monday, it has absorbed two rounds of global expiry flows in quick succession, a combination that regularly produces choppy price action and heightened gap-open risk at the start of the new week.

For you, this means the danger window on expiry week is not Friday afternoon. It is Thursday midday and the following Monday open, a different risk calendar than most internationally sourced expiry guides suggest.

This is the mechanical core that separates traders who understand triple witching from those who merely know it exists. The price behaviour you see on expiry day is not random; it is the emergent consequence of how market makers manage their risk.

Market makers (dealers) sell options to participants and continuously offset their exposure by trading the underlying shares. This process is called delta-neutral hedging. Delta is a measure of how much an option’s price changes when the underlying asset’s price moves; maintaining delta neutrality means the dealer’s total position has roughly zero net exposure to small price moves. Dealers who are net short options buy the underlying when prices fall and sell when prices rise, mechanically dampening moves in both directions.

The pinning and unpinning dynamics described above operate within a broader ASX market structure that governs how orders are matched, how the pre-open auction resolves, and how bid-ask spreads widen under stress conditions, all of which become more consequential on expiry Thursday.

When open interest (the total number of outstanding contracts) is heavily concentrated at specific strikes, this hedging activity creates a pinning effect. As prices approach a high-open-interest strike, dealers repeatedly buy dips and sell rallies around that level, acting as a mechanical anchor. The result is that prices appear stuck at or near the strike, and breakout attempts fail repeatedly.

This effect is most pronounced on triple witching days, when many expiries across all three instrument classes cluster at the same strikes simultaneously.

At the moment contracts expire and settle, the need to maintain those hedges disappears entirely. Dealers then move swiftly to close out the positions that had been keeping the pin in place, and that rapid de-hedging pushes prices sharply away from the strike in what is known as unpinning. These post-settlement moves tend to show short-term directional persistence, with the initial break continuing rather than snapping back.

When you see a large-cap ASX stock repeatedly failing to break through a round-number level on expiry Thursday morning, that is pinning in action. Trading a breakout of that level before settlement is fighting a mechanical force, not reading a technical signal.

A put wall is a large concentration of put open interest at a specific strike price. It creates a distinctive two-stage dynamic:

When price cuts through a significant put wall, the support it was providing evaporates and dealers are forced to sell aggressively to re-hedge their exposure, adding further weight to the downward move.

This risk is amplified on triple witching days, when clustered expiries across multiple instruments magnify the volume of dealer re-hedging required. The names most subject to these dynamics on the ASX are BHP and the four major domestic banks, where single-stock option open interest is consistently the highest.

Open interest mapping is the step that converts abstract mechanical knowledge into a concrete pre-trade routine. Before the market opens on expiry Thursday, you want to know exactly where the high-open-interest strikes sit, because those are the levels where pinning is most likely and where unpinning moves will originate after settlement.

Here is the process as a sequential routine:

During the pre-settlement window, treat repeated price failures around these levels as pinning. Do not trade breakouts against a mechanical anchor. After settlement (post 12:00 pm), respect sharp moves away from those zones as potential unpinning with directional follow-through.

A trader who maps open interest before Thursday’s open has a structural read on where the market is being mechanically held, information that no price chart or news feed provides. That read directly informs whether a level is worth trading or worth avoiding entirely.

For traders wanting to apply the open interest mapping routine in practice, our full explainer on reading trading volume covers how to use volume confirmation alongside price action to distinguish genuine breakouts from mechanical noise, which is particularly valuable in the post-settlement window when pinned levels finally release.

Everything covered above translates into six specific tactical adjustments. Each one responds to a known mechanical feature of the event, and understanding the “why” behind each rule is what makes the difference between consistent application and a checklist you forget by next quarter.

Options traders who use credit spreads to generate positive theta exposure need to account for expiry-week liquidity deterioration when sizing positions, because the bid-ask widening that concentrates around Thursday midday settlement directly compresses the net credit receivable on rolls initiated too late in the week.

Rolling short options positions by Tuesday of expiry week avoids the worst of the spread widening and liquidity deterioration that tends to cluster as Thursday midday settlement approaches.

After 12:00 pm, the structural constraint lifts and the market begins returning to fundamentals-driven movement. For traders who have been patient through the morning, this can create some of the cleanest directional setups of the quarter, because the mechanical noise has cleared and the genuine order flow becomes visible again. The ASX midday timing, not the US Friday-close framework, is the structural feature that shapes all of these adjustments.

Four triple witching events per year are not four disruptions to survive. They are a recurring structural rhythm with consistent characteristics that become increasingly readable the more cycles you observe.

For traders wanting to place the June and September quarterly expiries within a broader seasonal context, our deep-dive into seasonal ASX return patterns covers the structural mechanisms, including superannuation flows and institutional mid-year rebalancing, that shape ASX performance across the calendar year.

The roughly 12-week inter-expiry period is a natural planning horizon for options positions. If you sell covered calls or manage short spreads, aligning your rolling schedule around the quarterly expiry calendar simplifies the process and ensures you are never scrambling to close positions into deteriorating liquidity.

Each quarterly expiry has its own seasonal flavour:

Over three or four cycles, you start recognising the patterns: which strikes tend to pin, how the post-settlement move behaves, how Monday gap opens resolve. That pattern recognition is itself a compounding edge, because it converts a recurring structural event into something you anticipate rather than relearn from scratch each quarter.

Triple witching is the same structural logic repeating four times a year: simultaneous expiry, dealer hedging, pinning around high-open-interest strikes, and unpinning once settlement removes the hedge requirement. The mechanics do not change quarter to quarter. Your familiarity with them does.

The two adjustments that matter most are timing-specific. Know that ASX settlement hits at midday, not at the close, so your risk window is different from what any US-focused guide will tell you. And act early in the expiry week on options positions, because the cost of waiting compounds as Thursday approaches.

Each expiry cycle is also a live observation opportunity. The more cycles you track, marking open interest beforehand and noting how pinning and unpinning actually played out, the sharper your read becomes. Consistent preparation across multiple quarters is what turns triple witching from a source of unexpected losses into one of the most structurally predictable events on your trading calendar.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASX triple witching is the simultaneous expiry of three derivative instruments: SPI 200 index futures, XJO index options, and single-stock options. It occurs four times a year on the third Thursday of March, June, September, and December, with contracts ceasing to trade at approximately 12:00 pm Sydney time.

The upcoming ASX triple witching dates are Thursday 17 September 2026, Thursday 17 December 2026, Thursday 18 March 2027, and Thursday 17 June 2027. Public holidays can shift the exact date, so verifying each quarter is recommended.

The ASX settles derivative contracts at approximately 12:00 pm Sydney time, meaning peak structural stress falls in the midday window of 11:30 am to 12:15 pm AEST. US triple witching volatility clusters in the final hour of trade on the third Friday, making the ASX risk calendar fundamentally different from any US-focused expiry guide.

Pinning occurs when dealer delta-hedging activity mechanically anchors prices near high-open-interest strike levels, causing repeated failed breakout attempts. Unpinning happens immediately after 12:00 pm settlement when dealers rapidly close those hedges, pushing prices sharply away from the strike with short-term directional follow-through.

Traders holding covered calls, short puts, or spreads with expiring contracts should complete the roll by Tuesday of expiry week. Waiting until Wednesday or Thursday means transacting into deteriorating liquidity and wider bid-ask spreads that directly compress execution quality and net credit on rolls.