AMD Stock at $424: Has the Market Already Priced a Win?

19 mins ago

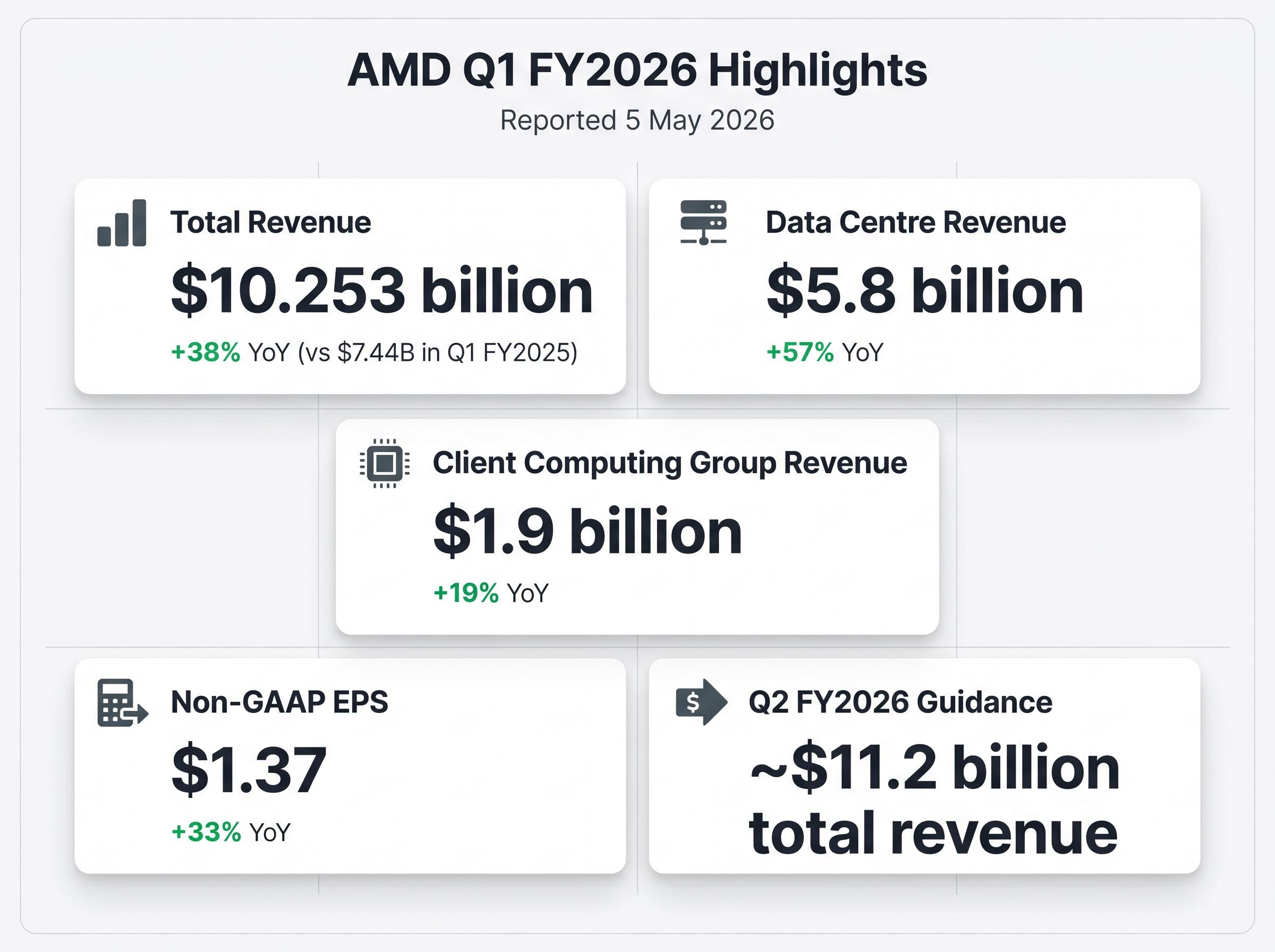

AMD’s data centre segment posted $5.8 billion in revenue for Q1 fiscal 2026, a 57% year-over-year increase. That single number is doing a lot of work in the bull case. The question investors are actually asking is whether it reflects a durable structural shift or a cycle peak dressed up as a trend.

AMD reported Q1 FY2026 results on 5 May 2026, and the headline figures reignited debate about whether the company represents the most asymmetric AI infrastructure trade left on the board or a stock already pricing in flawless execution for years. The debate centres on a specific thesis: the AI workload mix is rotating from training toward inference and agentic AI, and that rotation disproportionately benefits AMD’s EPYC server CPU business in ways the market may not have fully valued.

What follows unpacks the structural logic behind that thesis, what the earnings data supports, where the risks are real rather than hypothetical, and how to think about valuation at current levels.

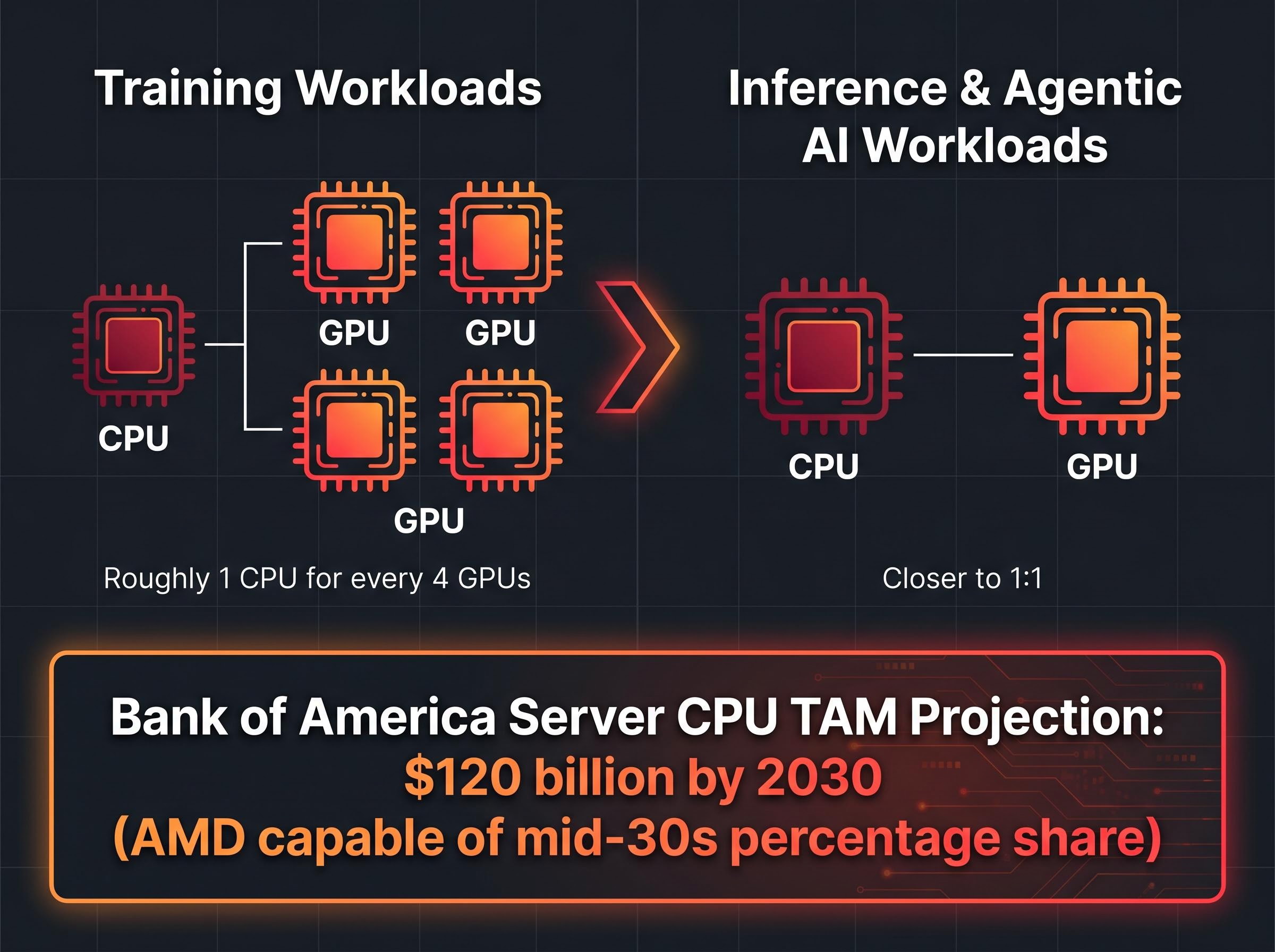

The AI infrastructure build-out began as a GPU story. Training large language models requires dense, parallel processing power, and GPUs owned that workload almost entirely. Data centres configured around ratios of roughly one CPU for every four GPUs.

That ratio is shifting. As AI moves from training toward inference, the compute profile changes:

CPU-to-GPU ratio compression from a historical 1:8 toward 1:1 is not a forecast; it is showing up in Q1 2026 procurement data across Arm, AMD, and Intel simultaneously, with Georgia Tech and Intel research finding that CPU tool processing accounts for 50-90% of total latency in agentic AI workflows.

Agentic AI, where autonomous software agents execute multi-step tasks across systems, accelerates this shift further. Each agent call involves orchestration logic, retrieval from external databases, and context management that runs on CPUs, not GPUs.

The hardware implication is direct. Bank of America projects the server CPU total addressable market (TAM) could reach $120 billion by 2030, with AMD capable of capturing mid-30s percentage share as inference workloads structurally increase CPU intensity.

Goldman Sachs noted that “the more important signal is the sustained CPU opportunity as inference and agentic AI workloads demand more cores and memory bandwidth per accelerator.”

This is why the training-to-inference rotation is an AMD story, not just an Nvidia story. The structural demand for EPYC CPUs grows as inference proliferates, independent of whether AMD wins or loses GPU market share against Nvidia.

AMD’s Q1 FY2026 earnings, reported on 5 May 2026, provide the most recent empirical test of the structural thesis.

Total revenue reached $10.253 billion, up 38% year over year from $7.44 billion in Q1 FY2025. The data centre segment drove the acceleration, posting $5.8 billion at 57% year-over-year growth. Non-GAAP earnings per share came in at $1.37.

| Period | Total Revenue | Data Centre Revenue | YoY Growth (Data Centre) | Non-GAAP EPS |

|---|---|---|---|---|

| Q1 FY2025 | $7.44B | Not separately disclosed in research | N/A | N/A |

| Q1 FY2026 | $10.253B | $5.8B | +57% | $1.37 |

Full-year FY2025 non-GAAP EPS came in at $4.17, confirming that earlier analyst projections from mid-2025 were directionally accurate.

The forward trajectory is where the signal sharpens. AMD guided Q2 FY2026 revenue to approximately $11.2 billion, implying sequential acceleration.

Q2 FY2026 guidance: approximately $11.2 billion in total revenue, suggesting the data centre growth rate is not yet decelerating.

The results do not prove the structural thesis on their own. But they are consistent with it: data centre revenue is growing faster than the rest of the business, and the guidance implies the run rate is still accelerating rather than plateauing.

The instinct when analysing AMD’s AI exposure is to focus on the GPU competition with Nvidia. That framing misses the more durable part of the thesis. EPYC server CPUs are deployed in AI inference pipelines not as replacements for GPUs but as the compute layer surrounding them.

There are four distinct ways EPYC CPUs contribute to AI inference architectures:

Mizuho characterised EPYC as “underappreciated upside” as inference and AI agents proliferate beyond GPU-dense clusters. J.P. Morgan flagged upside risk if EPYC share gains in cloud CPU and AI inference accelerate into 2026-2027.

Industry estimates placing 35-45% of inference workloads as CPU-bound translate directly into AMD’s EPYC attach rate per GPU deployment, with AMD’s own revised server CPU TAM forecast moving from 18% to 35% annual growth after Q1 2026 procurement data confirmed the agentic AI demand signal.

The sell-side consensus on this point is unusually aligned. Bank of America’s $120 billion server CPU TAM projection by 2030 frames AMD as “structurally advantaged” as inference shifts closer to CPUs and memory. CEO Lisa Su has stated a path to more than $20 in EPS within AMD’s strategic timeframe, a target that depends heavily on EPYC’s continued share gains against Intel in cloud deployments.

AMD’s Helios rack systems bundle GPU accelerators, EPYC CPUs, and networking components into unified deployable packages. This matters because the complexity barrier in AI infrastructure deployment is real; enterprises and cloud providers prefer integrated solutions that reduce configuration overhead.

Meta and OpenAI are active AMD hardware customers, giving the Helios product line enterprise validation. The integration approach increases EPYC’s attach rate per deployment, tying CPU revenue directly to GPU sales rather than leaving them as independent procurement decisions.

The structural bull case is coherent. The risks are also specific and measurable, not just generic cautionary language.

D.A. Davidson estimated that if AI demand peaks, semiconductor stock downside risk could range from 40% to 50%.

The Cisco comparison circulates among analysts for a reason. Cisco’s peak dot-com valuation preceded a two-decade flat return. The parallel is imperfect, but the mechanism is relevant: when execution assumptions are already priced into the multiple, even strong results may not generate commensurate returns.

The Cisco comparison that circulates among AMD bears has a specific mechanism worth examining: Cisco’s peak multiple in 2000 embedded a decade of network build-out assumptions that were largely correct on volume but wrong on pricing power, and agentic AI procurement data suggests AMD’s CPU attach rate growth is structurally different from the episodic equipment cycles that preceded Cisco’s plateau.

Analyst consensus projections (based on a May 2025 snapshot, noting these have moved higher since) projected EPS growing from approximately $6.69 in the current fiscal year toward approximately $24 within four years, with revenue growing from approximately $46.8 billion toward approximately $135 billion. Applying a 25x price-to-earnings multiple to the $24 EPS estimate yields approximately $600, representing roughly 25%-30% upside from prior reference levels.

Street-high price targets of $525 from Bernstein and $450 from Goldman Sachs, both issued following Q1 2026 results, rest on the 6GW GPU deployment commitments split between Meta and OpenAI, which Bernstein explicitly described as not yet fully priced into consensus models at the time of publication.

Independent discounted cash flow modelling produces a wider range depending on growth assumptions:

| Scenario | Revenue Growth Assumption | Terminal P/E Multiple | Implied Intrinsic Value |

|---|---|---|---|

| Bull | ~24% annually | 24x | ~$525 |

| Base | ~16% annually | 21x | ~$175 |

| Bear | ~8% annually | 18x | ~$45 |

The spread between the bull and bear cases is roughly 12:1. That ratio reflects how much the valuation outcome depends on which growth trajectory materialises. AMD was trading at approximately $420-$421 as of 18 May 2026.

Net profit margin has expanded to 13.3%, up from approximately 9.5%. Free cash flow reached $8.5 billion in the most recent fiscal year, versus a five-year average of $3.67 billion. These are genuine improvements in the business economics.

Current FY2026 and FY2027 consensus estimates have moved significantly higher than the May 2025 snapshots cited above and require current sourcing for precision.

AMD carries minimal debt, with enterprise value roughly equivalent to market capitalisation. That is a structural positive.

The counterpoint is ongoing share issuance, which creates a compounding drag on per-share returns. At 148x trailing earnings, even modest dilution compounds the gap between business growth and shareholder returns. The five-year return on invested capital of approximately 8.5%, and one-year ROIC of approximately 3%, sit well below what a premium multiple would typically demand.

The empirically grounded components of the bull case are genuine. Data centre revenue at $5.8 billion for Q1 FY2026, Q2 guidance of approximately $11.2 billion, EPYC’s structural positioning in inference architectures, and sustained hyperscaler capex tailwinds all support the thesis that AMD is building a durable AI infrastructure business.

The projection-dependent components carry more uncertainty. The $120 billion server CPU TAM by 2030, the EPS trajectory toward $20 and beyond, and the assumption that EPYC share gains continue uncontested against Intel all require execution over multiple years.

There is a distinction between believing the AMD thesis is correct and believing the current price adequately compensates for the execution risk embedded in those assumptions. At approximately 148x earnings, the stock requires most of the bull case to materialise for investors to generate returns commensurate with the risk.

The specific variables to monitor over the next two to three quarters:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AMD's EPYC is a server-grade CPU that plays a critical role in AI inference architectures by handling retrieval, orchestration, agentic task execution, and memory-bandwidth-intensive microservices that surround GPU accelerators, making it a structurally important asset as AI workloads shift from training toward inference.

AMD's data centre segment posted $5.8 billion in revenue for Q1 FY2026, representing 57% year-over-year growth, with the company guiding Q2 FY2026 total revenue to approximately $11.2 billion.

The key risks include Nvidia's entrenched CUDA software ecosystem, a valuation of approximately 148x trailing earnings that prices in years of flawless execution, ongoing share dilution, a five-year ROIC of roughly 8.5%, and U.S. export controls that limit AMD's access to the Chinese AI accelerator market.

As AI workloads rotate from training toward inference and agentic AI, CPU utilisation per GPU accelerator increases, with the CPU-to-GPU ratio compressing from roughly 1:8 toward 1:1, directly expanding the addressable market for AMD's EPYC server CPUs.

Bank of America projects the server CPU total addressable market could reach $120 billion by 2030, with AMD positioned to capture mid-30s percentage share as inference workloads structurally increase CPU intensity.