AMD Stock at $424: Has the Market Already Priced a Win?

1 hr ago

Goldman Sachs nearly doubled its AMD price target overnight, from $240 to $450. Bernstein went further, setting a Street-high $525. Both firms cited the same structural force: agentic AI.

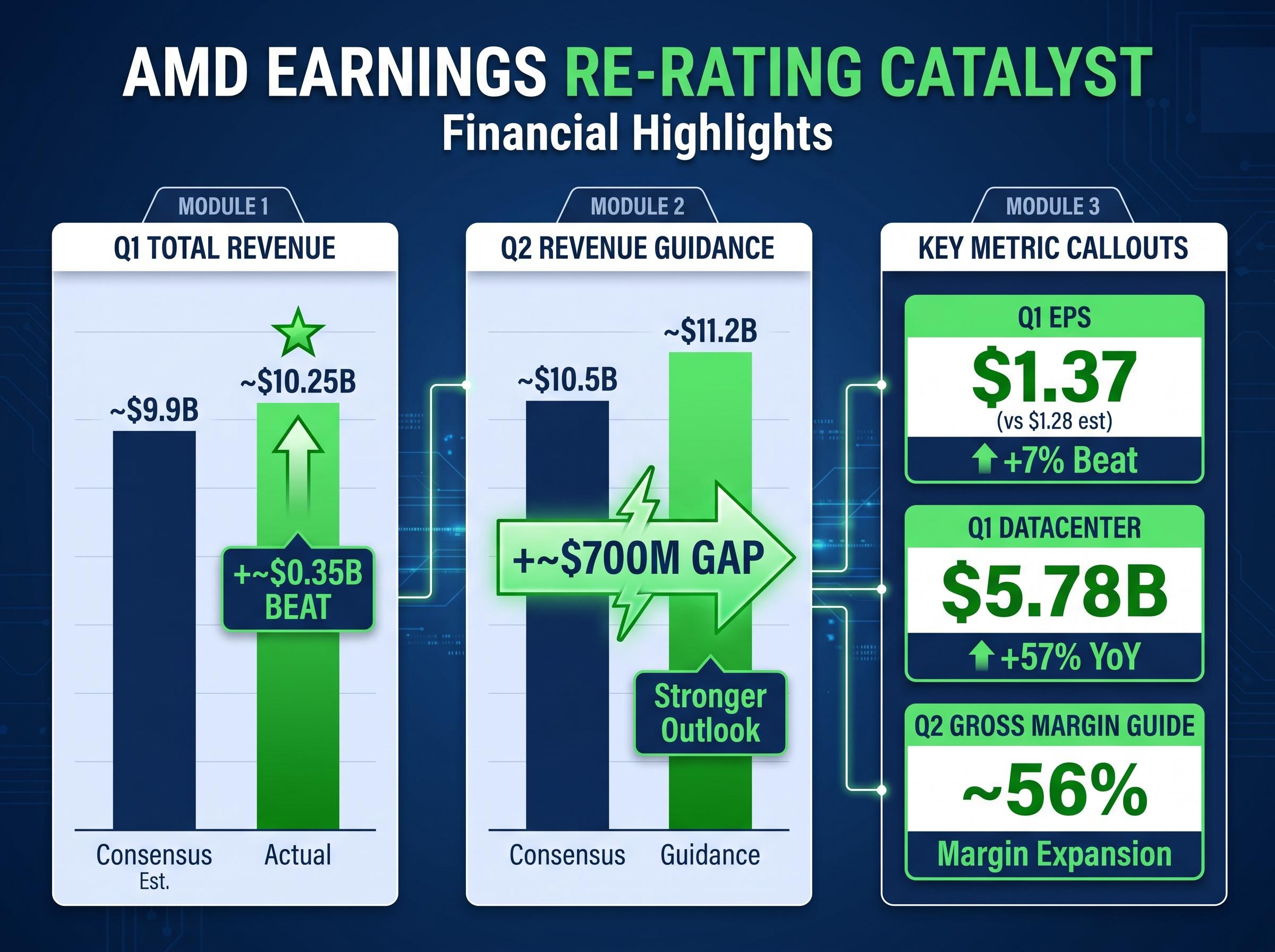

The upgrades followed AMD’s Q1 2026 results, released after close on 5 May, which beat across the board. Datacenter revenue reached $5.78 billion, up 57% year over year. Q2 guidance of approximately $11.2 billion cleared consensus by a wide margin. The earnings beat is the proximate trigger, but the analyst upgrades reach further, arguing that something more durable than a single strong quarter is now underway.

What follows unpacks what Goldman Sachs and Bernstein are actually arguing, why their theses differ from each other in ways that matter, what GPU deployment deals with OpenAI and Meta add to the picture, and where the credible bear case still lives. The aim is to give readers the analytical foundation to form an independent view of whether the Wall Street bullishness is grounded or premature.

The numbers tell the story before any analyst commentary enters. AMD reported Q1 total revenue of approximately $10.25 billion against a consensus estimate of roughly $9.9 billion. Earnings per share came in at $1.37, beating the $1.28 consensus. The datacenter segment, the engine of the bull case, delivered $5.78 billion, a 57% year-over-year increase.

AMD’s Q1 2026 earnings press release confirms total revenue of $10.3 billion, non-GAAP diluted EPS of $1.37, and Data Center segment revenue of $5.8 billion, the primary source figures underlying both the Goldman Sachs and Bernstein upgrade theses.

Q2 guidance may have mattered even more than the Q1 print. Management guided approximately $11.2 billion in revenue for Q2, roughly $700 million above a Street consensus that had expected approximately $10.5 billion. That gap is not incremental; it forced a wholesale re-rating of near-term earnings power.

| Metric | Q1 Actual | Q1 Consensus | Q2 Guidance | Q2 Consensus |

|---|---|---|---|---|

| Total Revenue | ~$10.25B | ~$9.9B | ~$11.2B | ~$10.5B |

| EPS | $1.37 | $1.28 | — | — |

| Datacenter Revenue | $5.78B (+57% YoY) | — | — | — |

Three forward indicators embedded in the Q2 guide elevated the outlook beyond simple momentum continuation:

The two upgrades converge on a bullish conclusion but arrive there by different routes. For investors weighing the targets, those differences matter more than the headline agreement.

| Firm | Rating | New PT | Prior PT | Core Thesis |

|---|---|---|---|---|

| Goldman Sachs | Buy | $450 | $240 | x86 infrastructure demand from agentic AI |

| Bernstein | Buy | $525 | $265 | Earnings compounding through 2028 |

Goldman’s analyst James Schneider frames the upgrade around a structural market share thesis. The argument: AI agents must interact with existing enterprise x86 server stacks, including databases, ERP systems, and legacy APIs. That makes AMD’s EPYC processor the path-of-least-resistance CPU for hybrid AI and enterprise workloads. Schneider projects x86 server CPU total addressable market (TAM) expansion of 50%+ by 2028, with AMD positioned as the disproportionate beneficiary. GPU datacenter upside is flagged as an additional catalyst for 2027 and beyond, but the core thesis is infrastructure-led.

Bernstein’s Stacy Rasgon grounds the Street-high $525 target in specific earnings projections: $14+ EPS in 2027 and approximately $20 EPS in 2028. The analytical basis is AMD management’s revised TAM of approximately $120 billion, growing at 35% compound annual growth rate (CAGR) through 2030, which Rasgon described as “potentially credible” in the agentic AI environment. Rasgon explicitly acknowledged that AMD’s prior performance had exceeded his earlier bull calls, framing the current upgrade as grounded in demonstrated earnings power rather than sentiment.

Goldman’s thesis is a structural market share argument. Bernstein’s is an earnings compounding argument. Which thesis an investor finds more credible should determine how they weight the upgrade.

Agentic AI refers to autonomous software agents that take multi-step actions across enterprise systems, retrieving data, executing tasks, and interacting with other software without continuous human direction. This is distinct from the training and pure inference workloads that have driven GPU demand over the past two years.

The distinction matters for AMD’s investment case because of where the compute bottleneck sits. Training workloads are batch-intensive and GPU-dominated. Pure inference workloads, such as generating a single chatbot response, are increasingly GPU-optimised through architectures like NVIDIA’s Blackwell. Agentic workloads are different: they require low-latency interaction with existing x86-native enterprise systems, meaning the CPU becomes a performance bottleneck that GPU acceleration alone cannot resolve.

Goldman projects x86 architecture will dominate agentic workloads, driving 50%+ server CPU TAM expansion by 2028. Multiple analysts have referenced an “inference shift from GPUs to hybrid CPU/GPU stacks” as agentic workloads scale.

Industry estimates place 35-45% of inference workloads as CPU-bound under agentic deployment conditions, a figure that sits at the centre of the agentic AI hardware investment map and explains why Goldman’s Schneider framed the EPYC opportunity as infrastructure-led rather than GPU-led.

AMD management’s revised TAM estimate: approximately $120 billion growing at 35% CAGR through 2030, representing the company’s own quantification of the agentic AI opportunity.

Without understanding this workload distinction, the upgrade thesis reads as generic GPU hype. It is not. The bull case rests on CPU-specific demand that did not exist at scale before agentic deployments began.

Alongside the CPU thesis, AMD disclosed 6GW total GPU deployment commitments split evenly between Meta and OpenAI. These deals represent a materially different revenue story from the EPYC server CPU ramp.

| Partner | GW Commitment | Products | Primary Workloads | Timeline |

|---|---|---|---|---|

| OpenAI | 3GW | MI300X (2026), MI450 (2027) | o1 models, custom RAG pipelines | ~1GW live by end of 2026; full 6GW by 2028 |

| Meta | 3GW | MI300X and MI450 | Llama 4 agentic inference (~80%), recommendation engines | Deployment begins Q3 2026; full capacity by 2027 |

Goldman Sachs flagged the Meta GPU deployment specifically as a near-term catalyst. The use cases are concrete: Meta is targeting Llama 4 agentic inference for approximately 80% of deployed workloads, alongside recommendation engines. OpenAI is deploying for o1 model workloads and custom retrieval-augmented generation (RAG) pipelines.

The five-year Meta chip supply agreement, covering MI300X and MI325X GPU shipments beginning H2 2026, carries contractually anchored revenue visibility that analysts at Goldman Sachs have described as de-risking a significant portion of AMD’s 2027 revenue outlook.

Bernstein’s Stacy Rasgon stated explicitly that these GPU ramps are not yet fully incorporated into prevailing Street financial models, framing the deals as potential estimate-revision catalysts rather than already-priced news.

Both deployments are non-exclusive. NVIDIA remains the primary GPU supplier for both hyperscalers. The deals confirm AMD is credible in GPU inference at hyperscaler scale, but they do not signal NVIDIA displacement.

At approximately 45x forward price-to-earnings versus a sector average of approximately 30x, AMD is priced for sustained execution. The sceptical case deserves genuine weight.

Morgan Stanley maintains a Hold rating with a $340 price target. The firm’s thesis: NVIDIA’s Blackwell GPUs handle approximately 80% of inference workloads today, the agentic CPU shift narrative remains unproven at scale, and AMD’s 56% gross margin guide for Q2 leaves limited buffer against pricing concessions needed to win incremental hyperscaler share.

GLJ Research holds a Sell rating with a $200 target. The firm characterises agentic AI demand as speculative rather than structural, argues EPYC growth reflects a CPU refresh cycle rather than durable share gains, and flags approximately $50 million in insider sales post-earnings as a cautionary signal.

GLJ Research described the agentic AI demand thesis as “speculative rather than structural,” arguing that EPYC gains are tied to temporary CPU refresh cycles.

Intel presents a competitive response on both fronts: the Xeon 6 “Clearwater Forest” platform ramp, Gaudi 3 AI accelerator pricing approximately 10% below AMD’s MI300X, and a claimed 40% server CPU share versus AMD’s approximately 25%.

The discrete risk categories investors should weigh:

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Bernstein’s $525 target requires specific milestones: $14+ EPS in 2027 and approximately $20 EPS in 2028. Given the current Q2 run-rate guidance of approximately $11.2 billion in revenue, that trajectory implies sustained sequential growth and margin expansion through at least the next eight quarters.

The broader consensus is catching up, but has not arrived. Across approximately 37 analysts, the distribution stands at roughly 32 Buy, 4 Hold, and 1 Sell, with an average price target of approximately $362, up from approximately $291 pre-earnings. That average still sits below the current trading level near $412.50 (intraday, 6 May), which means the consensus is in the process of catching up rather than leading.

Three specific, time-bound conditions will determine whether the bull case holds or compresses:

Goldman Sachs and Bernstein’s upgrades are not sentiment-chasing. They reflect coherent, data-grounded theses about structural CPU demand and compounding earnings power, each supported by specific financial projections and identifiable demand drivers.

The counter-thesis, however, carries its own specificity. Morgan Stanley and GLJ Research have identified real competitive, margin, and valuation risks. At 45x forward P/E, there is limited tolerance for execution shortfalls.

The AI hardware sector rotation that carried Asian semiconductor suppliers to premium inflows at valuations roughly half the Nasdaq 100 multiple offers a structurally different risk-return profile than US chip names trading at 45x forward P/E, context that is directly relevant to investors weighing AMD’s margin of error from here.

The operative question for the next two quarters is whether AMD can demonstrate that agentic AI CPU demand is structural rather than cyclical, and that GPU deployments with Meta and OpenAI begin on the Q3 2026 schedule. The earnings data and the analyst conviction are aligned. The price already reflects that alignment, which means the margin of error from here is thin.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Agentic AI refers to autonomous software agents that take multi-step actions across enterprise systems without continuous human direction. Unlike GPU-dominated training workloads, agentic deployments require low-latency interaction with existing x86 enterprise systems, making AMD's EPYC CPU a critical component and the foundation of both the Goldman Sachs and Bernstein upgrade theses.

AMD reported Q1 2026 total revenue of approximately $10.25 billion, beating the $9.9 billion consensus estimate, with non-GAAP EPS of $1.37 versus a $1.28 consensus and datacenter revenue of $5.78 billion, up 57% year over year. Q2 guidance of approximately $11.2 billion also cleared the Street consensus of roughly $10.5 billion by a wide margin.

AMD disclosed 6GW of total GPU deployment commitments split evenly between OpenAI and Meta, covering MI300X and MI450 products primarily for agentic inference workloads, with deployments beginning in H2 2026. Bernstein's Stacy Rasgon stated these ramps are not yet fully incorporated into Street financial models, framing them as potential future estimate-revision catalysts.

Morgan Stanley holds a $340 price target and argues that NVIDIA's Blackwell GPUs handle roughly 80% of inference workloads today and the agentic CPU shift remains unproven at scale, while AMD trades at approximately 45x forward P/E versus a sector average of 30x. GLJ Research holds a Sell rating with a $200 target, characterising agentic AI demand as speculative and flagging approximately $50 million in post-earnings insider sales.

Bernstein's $525 target is grounded in projections of $14-plus EPS in 2027 and approximately $20 EPS in 2028, implying sustained sequential revenue growth and margin expansion over at least the next eight quarters from the current Q2 run-rate guidance of approximately $11.2 billion.