Why AI Makes Markets Safer Daily but Riskier in a Crisis

31 mins ago

Salesforce stock is trading roughly 45% below its 2024 peak and at approximately 22x forward earnings. That valuation is either a rare entry point into one of enterprise software’s most entrenched platforms, or it is the kind of multiple compression that precedes a structurally impaired business trading down further for years.

The selloff reflects a broader market re-rating of seat-licence SaaS businesses amid AI disruption fears. Yet Salesforce sits in an unusually contested position: simultaneously a potential AI agent victim and an AI platform vendor through Agentforce and Data Cloud. As of mid-2025, the debate among institutional analysts is live, split, and unresolved. Morgan Stanley and Bank of America hold Buy-equivalent ratings. JPMorgan sits at Neutral. Bernstein calls the AI fears overdone but has lowered its growth ceiling.

This analysis applies a concrete framework to the Salesforce-specific case, walking through the embedded moat, the real financial metrics, the legitimate bear case around AI agents, and what the current valuation actually implies, so readers can stress-test the investment thesis rather than take a side based on narrative alone.

The selloff in SaaS has not been surgical. It has been an industry-wide repricing that treated high-quality and low-quality platforms as equivalent AI disruption targets. Adobe is down roughly 40% from its highs. Workday, Snowflake, MongoDB, and Okta have all been caught in the same gravity.

A Goldman Sachs software sector note, summarised by the Financial Times in February 2025, described the result bluntly: many traditional SaaS names had compressed to “teens or low-20s forward P/E as investors reassess long-term growth in an AI-automating world.” Salesforce was cited explicitly as trading at a “mature software” multiple despite still growing at high-single to low-double digits.

The selloff affecting Salesforce is part of a wider capital rotation away from legacy per-user licensing models, with the US software market recording over $2 trillion in market capitalisation losses in early 2026 as institutional investors shifted toward consumption-based and native AI infrastructure plays.

The distinction matters because each type of selloff demands a different analytical response:

That gap is both the risk and the potential opportunity. Getting the classification wrong is where most capital is lost.

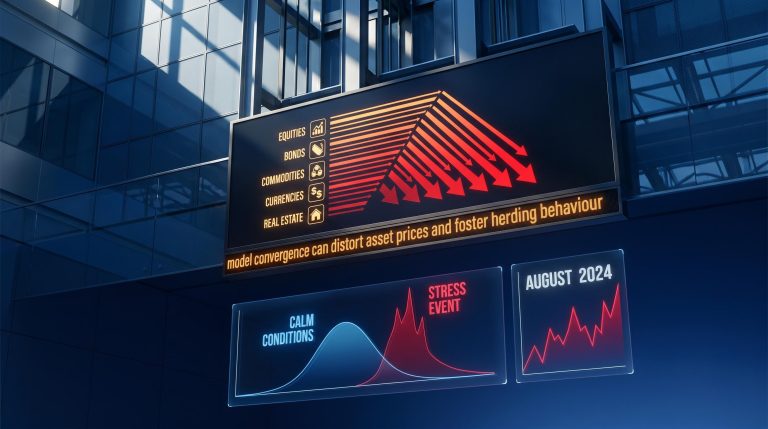

Salesforce operates as the canonical system of record for customer data across sales, marketing, and service functions in mid-to-large enterprises. That phrase, “system of record,” carries specific weight. It means Salesforce is not a tool that sits on top of a company’s data; it is the layer where the data lives.

The structural basis for these barriers is well-documented in vendor lock-in economics, where the combination of proprietary data formats, retraining costs, and integration dependencies creates a self-reinforcing switching cost stack that compounds the longer an enterprise remains on a platform.

Displacing it requires overcoming a switching cost stack that compounds across multiple dimensions:

Morgan Stanley analyst Keith Weiss, in a March 2025 note, pointed to Salesforce‘s integrated platform spanning Sales, Service, Marketing, Slack, Tableau, and MuleSoft as constituting a durable moat. Bank of America analyst Brad Sills reinforced the point in April 2025, noting that CIO interviews suggest AI projects often expand Salesforce‘s footprint rather than reduce it.

Bernstein analyst Mark Moerdler framed the structural argument in April 2025: most enterprises still rely on Salesforce as the canonical customer data system that AI agents will call into, not replace.

Data Cloud adoption supports this reading. Over 25% of large enterprise customers had adopted Data Cloud as of early 2025, up from single digits approximately one year earlier, according to the Q4 FY25 earnings call.

The moat argument is strong. It is not the whole picture.

If AI agents increasingly perform the tasks that previously required individual licensed users in sales and service roles, incremental seat demand erodes even if Salesforce retains its data layer. The platform survives, but the revenue model compresses. That is not a theoretical concern; it is the specific mechanism that JPMorgan analyst Mark Murphy cited in maintaining a Neutral rating in March 2025, arguing that AI upside may be offset by seat-based pressure if enterprises automate aggressively.

The guidance revision in May 2025 added weight. Salesforce lowered its FY26 revenue outlook to $37.6-$38.0 billion, down approximately 1% at the midpoint from initial guidance, citing “more cautious enterprise buying behaviour.” That language is not alarming in isolation, but it is the kind of early signal that precedes larger revisions when an industry-level shift is underway.

| Evidence supporting the bear case | Evidence the bear case is not yet confirmed |

|---|---|

| FY26 revenue guidance cut (~1% at midpoint) | No documented large-scale AI-agent-driven seat rip-outs in the public record |

| JPMorgan flags slowing core CRM seat growth | IDC: only 15% of enterprises deploying fully autonomous AI agents |

| Startups and mid-market firms experimenting with CRM-light stacks (The Information, June 2025) | CIO interviews suggest AI projects often expand Salesforce’s footprint (BofA, April 2025) |

| Consulting firms project seat-licence erosion over 2026-2030 | Over 25% of large enterprise customers adopted Data Cloud, up from single digits |

The confirmed, observable signals are narrow: a modest guidance cut, cautious management commentary, and slowing seat growth in the largest accounts. The forward-looking scenarios, consulting firm projections of autonomous AI agent replacement, broad SaaS seat rationalisation, are prospective.

No large, publicly documented AI-agent-driven Salesforce contract rip-outs exist in the public record as of mid-2025. The disruption case remains primarily a thesis about what could happen over a multi-year horizon. That distinction is where disciplined analysis separates from narrative-driven positioning.

The 15% figure from IDC on enterprises deploying fully autonomous AI agents aligns with broader research showing that enterprise AI deployment rates remain far below the levels required to drive the seat-licence erosion the bear case projects; agentic AI deployment specifically sat at just 17% among enterprises as of April 2026, with 70-80% of AI pilots stalling before reaching production.

The stock is trading as though something is broken. The financial statements do not yet confirm that.

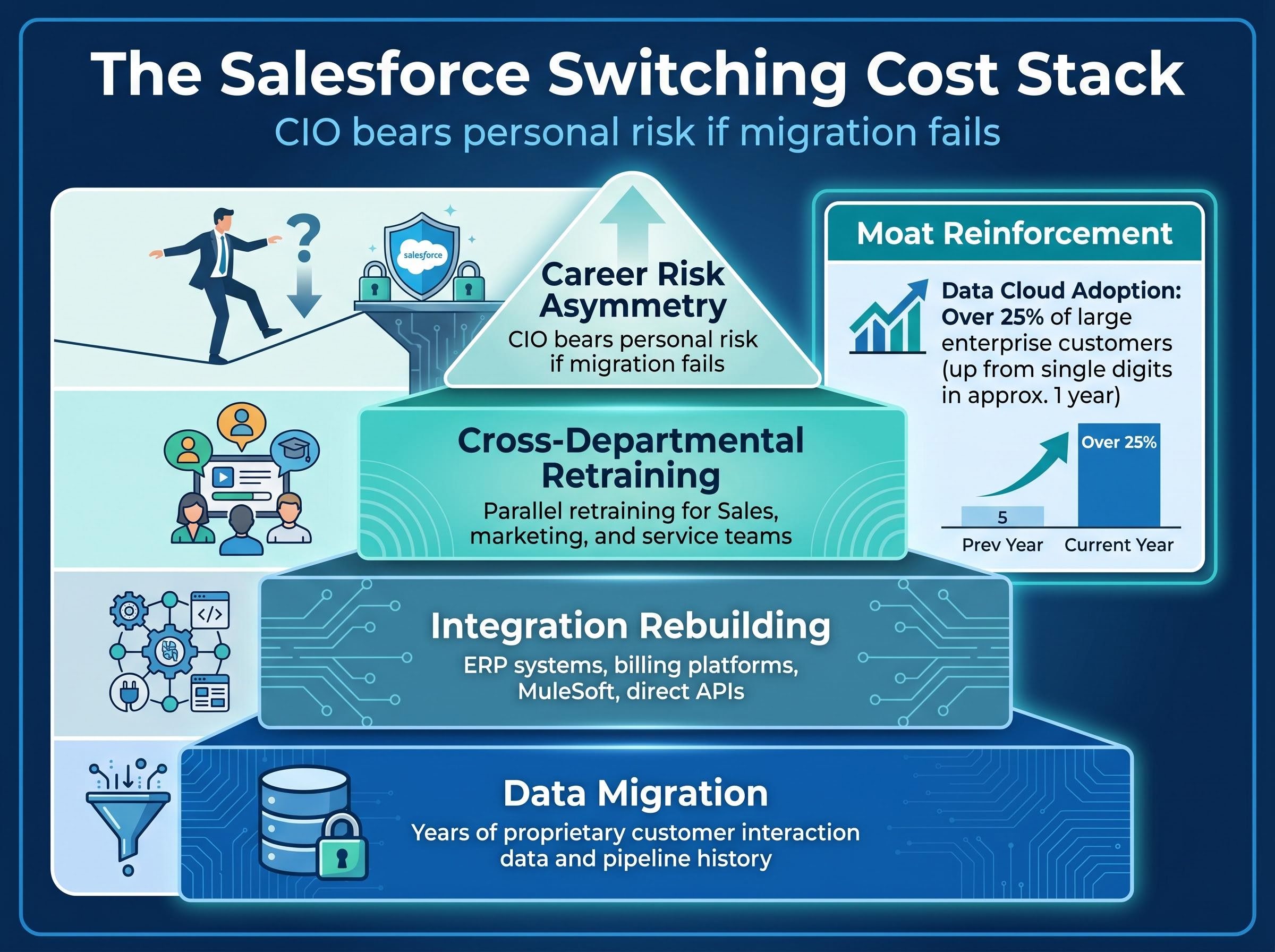

Free cash flow of $10.0 billion, growing at 17% year-over-year, is the single most important number in this section. A business generating that level of cash with accelerating margins is not a business in distress; it is a business whose stock price has decoupled from its current financial output.

The gap between free cash flow growth (17%) and revenue growth (11%) signals a business in a healthy maturation phase, converting more of each revenue dollar into cash. That is the profile of a company pulling margin levers effectively, not one scrambling to defend a deteriorating position.

One qualification: Agentforce and Data Cloud adoption metrics are the leading indicators investors should track. AI revenue is not yet broken out as a separate line in SEC filings, which means the most important growth driver remains qualitative rather than quantitative.

Data alone does not resolve the Salesforce question. The deeper issue is classification: is this a permanent impairment, a temporary dislocation, or an overreaction?

Three historical patterns provide the framework:

| Disruption type | Definition | Historical example | Salesforce implication |

|---|---|---|---|

| Structural (permanent) | Core business model is rendered obsolete by a technological shift | Kodak and digital photography | Bear case: AI agents eliminate the need for per-seat CRM licences entirely |

| Temporary (moat intact) | External shock compresses earnings; the competitive position survives | Texas Roadhouse during pandemic closures (recovered to ~$200) | Bull case: enterprise buying caution is cyclical; moat and data layer remain intact |

| Irrational (overreaction) | Market prices in a threat that does not materialise at the feared scale | Netflix declining from ~$66 to ~$19 on competitive streaming fears before recovering to ~$120 | Bull case (stronger variant): AI agents augment rather than replace Salesforce |

Salesforce‘s price-to-earnings ratio has declined from approximately 100x at its peak to approximately 22x forward earnings, according to FactSet consensus data cited by the Wall Street Journal in June 2025. That magnitude of compression implies the market is moving from the “irrational” classification toward something closer to “structural.”

The analyst community’s split reflects this tension directly. Morgan Stanley and Bank of America hold Buy-equivalent ratings. JPMorgan maintains Neutral. Bernstein holds Market Perform. When institutional analysts with comparable research access reach opposing conclusions, the classification question is genuinely unresolved, not merely a matter of insufficient data.

A 22x forward non-GAAP P/E on FY26 EPS guidance of $8.60-$8.75 implies the market is pricing Salesforce as a business with roughly mature-software growth expectations. Not a declining business, but not the accelerating platform the bull case argues for either.

The deceleration embedded in the numbers sharpens the point. FY25 delivered approximately 35% non-GAAP EPS growth. FY26 revised guidance implies approximately 5-7% growth at the midpoint. That deceleration, from 35% to mid-single digits, is the single most important number in framing the bull-bear tension. Market capitalisation sits at approximately $155-165 billion as of mid-2025.

Salesforce’s Investor Day 2025 commitment to a ‘rule-of-40+’ target connects directly to how institutional capital prices SaaS businesses today; the Rule of 40 benchmark assigns meaningful valuation premiums only to companies whose combined growth rate and free cash flow margin clears 40 points, and as of Q4 2025, fewer than 20% of public SaaS companies were clearing that threshold.

What the bull case requires:

What the bear case requires:

Both sets of beliefs are internally consistent. Neither is yet confirmed by the available data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The three-part evaluation synthesises as follows. Salesforce‘s moat is strong but not invulnerable; switching costs are real and multi-layered, though they do not immunise the business against a structural shift in how enterprises consume software. Financial health is clearly intact, with expanding margins, $10 billion in free cash flow, and a capital return programme that converts compressed valuations into accretive buybacks. The price relative to that financial output is compressed, but whether the compression is an opportunity or a warning depends entirely on whether the moat holds through the AI agent transition.

No large-scale documented AI-agent-driven Salesforce seat rip-outs exist in the public record as of mid-2025. The market is pricing in a prospective risk, not a confirmed one.

The specific data points that will resolve this debate over the next two to four quarters are identifiable:

The analyst consensus split, Morgan Stanley and Bank of America at Buy, JPMorgan at Neutral, Bernstein at Market Perform, is itself a signal that the answer is genuinely uncertain. The framework above gives investors the structure to reach their own conclusion and, more importantly, to update it as each of those data points arrives.

For investors wanting to track the specific Agentforce pilot-to-production and Data Cloud ARR signals identified above as the key resolution metrics, our full explainer on reading earnings reports walks through how to move beyond the headline EPS beat to assess free cash flow alignment, GAAP versus non-GAAP gaps, and forward guidance quality across consecutive quarters.

A system of record is the authoritative data layer where a company's core information lives, not just a tool that sits on top of it. For Salesforce, being the system of record for customer data means replacing it requires migrating years of proprietary data, rebuilding integrations, and retraining entire departments, creating compounding switching costs that protect the business.

Salesforce has fallen roughly 45% from its 2024 high primarily due to an industry-wide repricing of seat-licence SaaS businesses on fears that AI agents will erode demand for per-user software licences, compounded by a modest FY26 revenue guidance cut and cautious management commentary about enterprise buying behaviour.

Salesforce generated $10.0 billion in free cash flow in FY25, up 17% year-over-year, while non-GAAP operating margins expanded to 32.5%, suggesting the core business remains financially healthy even as the stock price has compressed significantly.

The most important signals to track are Agentforce pilot-to-production conversion rates, Data Cloud ARR trajectory, the pattern of guidance revisions through Q2-Q4 FY26, and any publicly documented large-enterprise seat reductions attributed to AI agent deployment.

Analyst opinion is split as of mid-2025: Morgan Stanley and Bank of America hold Buy-equivalent ratings, JPMorgan maintains a Neutral rating, and Bernstein holds a Market Perform rating, reflecting genuine uncertainty about whether the AI disruption risk is structural or overstated.