CURE and CLNE: the ASX ETFs Returning 25% in 2026

4 hrs ago

Heading into the midpoint of July 2026, global equity markets had delivered returns of around 9% across both US and international stocks. For investors tracking Fisher Investments’ annual outlook, that number carries a twist: it is ahead of schedule. The firm’s original forecast called for a muted, back-and-forth first half, with the real strength building toward year-end. Instead, most of the projected annual return arrived in the first six months.

That gap between expectation and result makes the mid-year mark a useful moment to pause. Fisher publishes one of the more widely followed institutional market outlooks each year, and checking how that forecast has held up halfway through offers a concrete lens on how big-picture market calls are constructed, absorbed, and revised in real time.

Not all institutional managers share the same conviction: the bull market 2026 outlook from BlackRock, J.P. Morgan, and Fidelity reflects continued overweight equity positioning, while Morgan Stanley and Bank of America hold a late-cycle view that flags a 10-20% drawdown as plausible even within a broadly positive year.

Here is what the mid-year data reveals: not just whether Fisher’s numbers are tracking, but what the review tells you about how professional forecasters define success, handle surprises, and set expectations for the months ahead. The framework that emerges is one you can apply to any institutional forecast you encounter, not just this one.

The number itself is straightforward. Global equities, covering both US and non-US markets, posted gains of roughly 9% across the opening six months of 2026. Against a full-year forecast calling for returns above 10%, that means the vast majority of the anticipated annual move has already arrived.

The original outlook told a different story about when that return would show up. The forecast pointed toward subdued, choppy conditions in the first half, with equity strength expected to gather pace later in the year and reach its high point in Q4. What happened instead was front-loaded strength, not a different destination but a faster route.

Ken Fisher, Founder, Executive Chairman, and Co-Chief Investment Officer of Fisher Investments, framed the deviation in measured terms.

Ken Fisher characterised the first half as “a little stronger in the first half of the year than we thought it would be” and the overall trajectory as “not too far off” the beginning-of-year forecast.

That language matters. A forecast being beaten on its timeline does not automatically mean the forecast was wrong. Understanding that distinction is what separates investors who evaluate predictions rigorously from those who treat any deviation as either vindication or failure.

| Metric | Original H1 Expectation | Actual H1 2026 Result |

|---|---|---|

| US equity return | Muted, back-and-forth | Approximately 9% |

| Non-US equity return | Muted, back-and-forth | Approximately 9% |

| Return timing profile | Strength building toward Q4 | Front-loaded into H1 |

| Deviation characterisation | N/A | “Not too far off” (Ken Fisher) |

Two events that were absent from the original 2026 forecast emerged during the first half. Neither, in Fisher’s assessment, altered the underlying bull-market thesis. The firm’s logic for dismissing each is more instructive than the events themselves, because it reveals the triage process professional forecasters apply when reality deviates from the plan.

The operative question Fisher applies to any unexpected development is not “did we anticipate this?” but “does this materially alter earnings, growth, or risk premia?” That distinction matters. Not all forecast misses carry equal weight, and the evaluative framework tells you which unexpected events deserve to recalibrate your positioning and which do not.

The war in Iran was absent from Fisher Investments’ published forecast at the start of the year. Ken Fisher assessed the event as having limited lasting market impact, concluding that it had not derailed the bull market or the full-year forecast.

The firm’s treatment of this geopolitical shock illustrates how it evaluates risk: the question is not whether the event occurred, but whether it is sufficient to damage the macroeconomic conditions underpinning the thesis. In this case, Fisher’s answer was no.

The triage logic Fisher applies to the Iran conflict mirrors a well-documented pattern: geopolitical risk and stock market behaviour have diverged repeatedly across recent major events, with equity prices driven by earnings fundamentals rather than proportional headline shocks in each case.

The decision by European monetary authorities to raise rates during spring 2026 was similarly absent from what the firm had projected at the outset. Ken Fisher characterised it as a minor adjustment rather than a regime change in global rates.

Interest rate conditions more broadly remained largely stable, in line with what the firm had originally projected. The European hike was treated as isolated rather than systemic, meaning it did not challenge the forecast’s core assumption about the global rate environment.

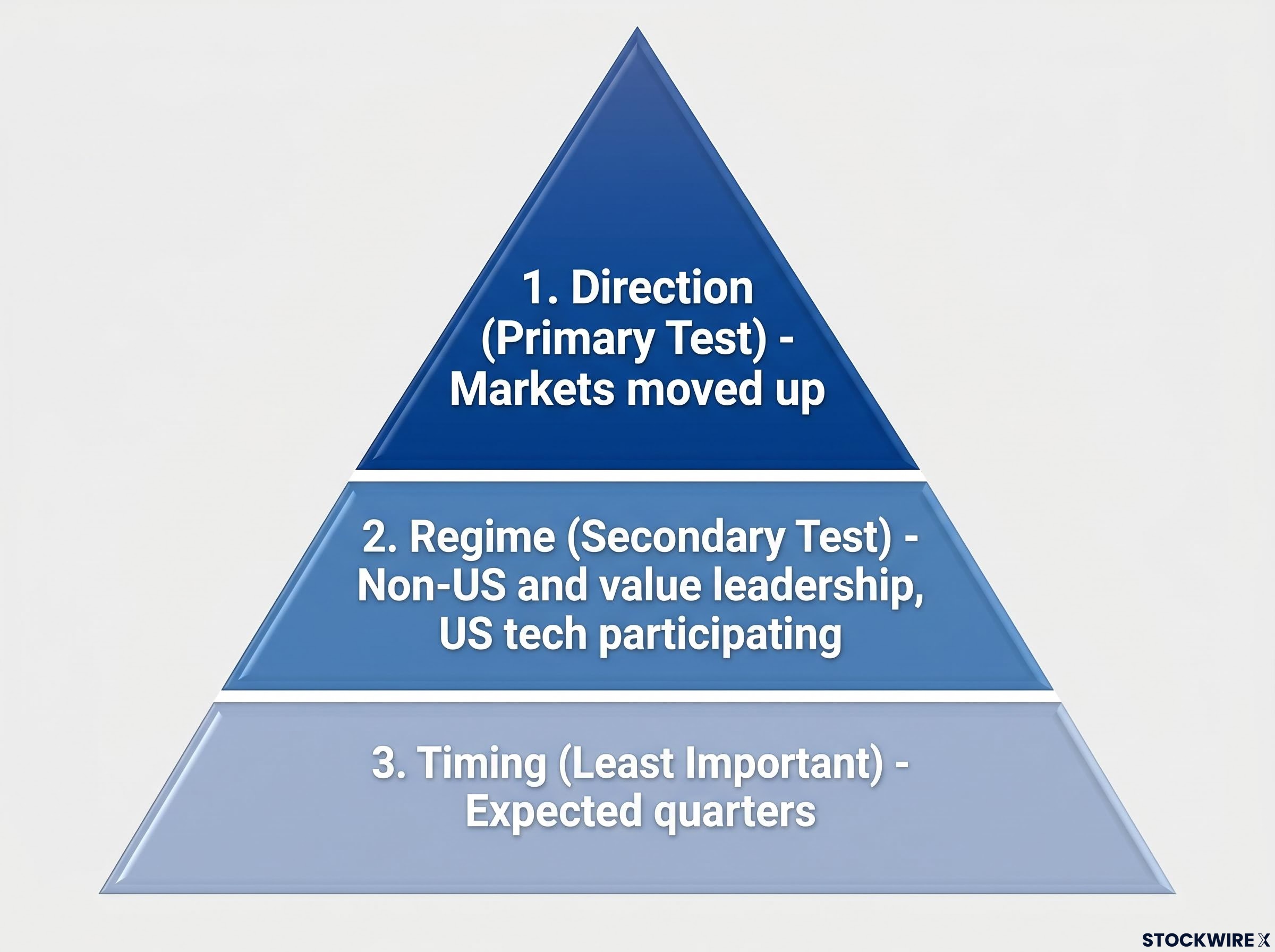

Most investors apply a binary test to market predictions: right or wrong. Fisher’s framework operates differently, and understanding the distinction changes how you evaluate any institutional outlook.

The 2026 forecast was framed in probabilistic terms from the start. It was not a point prediction (“the S&P 500 will close at X”). It was a regime call: the most likely outcome was a global equity return above 10%, with the odds skewed toward a positive year, weaker than 2025. That framing is deliberate. A probabilistic call is evaluated against whether the regime it described materialised, not whether the index hit a specific number in a specific month.

Fisher applies a clear hierarchy when assessing forecast accuracy:

Tetlock’s superforecasting research identifies probabilistic, regime-level thinking as the hallmark of accurate forecasters, distinguishing those who score themselves on whether the broad environment they described materialised from those who stake credibility on hitting precise numerical targets.

That hierarchy explains why Fisher’s mid-year language, “not too far off” and “working out pretty well,” reads as confidence rather than concession. By the firm’s own scoring system, the forecast is passing its primary and secondary tests. The timing miss is real but sits at the bottom of the evaluative stack.

H1’s approximately 9% gain represents strength arriving earlier than modelled. The annual story the forecast told, a positive year with global equities returning above 10%, is not changed by this. If you hold long positions through volatile periods, this is a concept worth internalising: intra-year timing can be wrong while the annual outcome still aligns with the original call. Evaluating a forecast by whether the index hit a specific number in a specific month is applying the wrong standard.

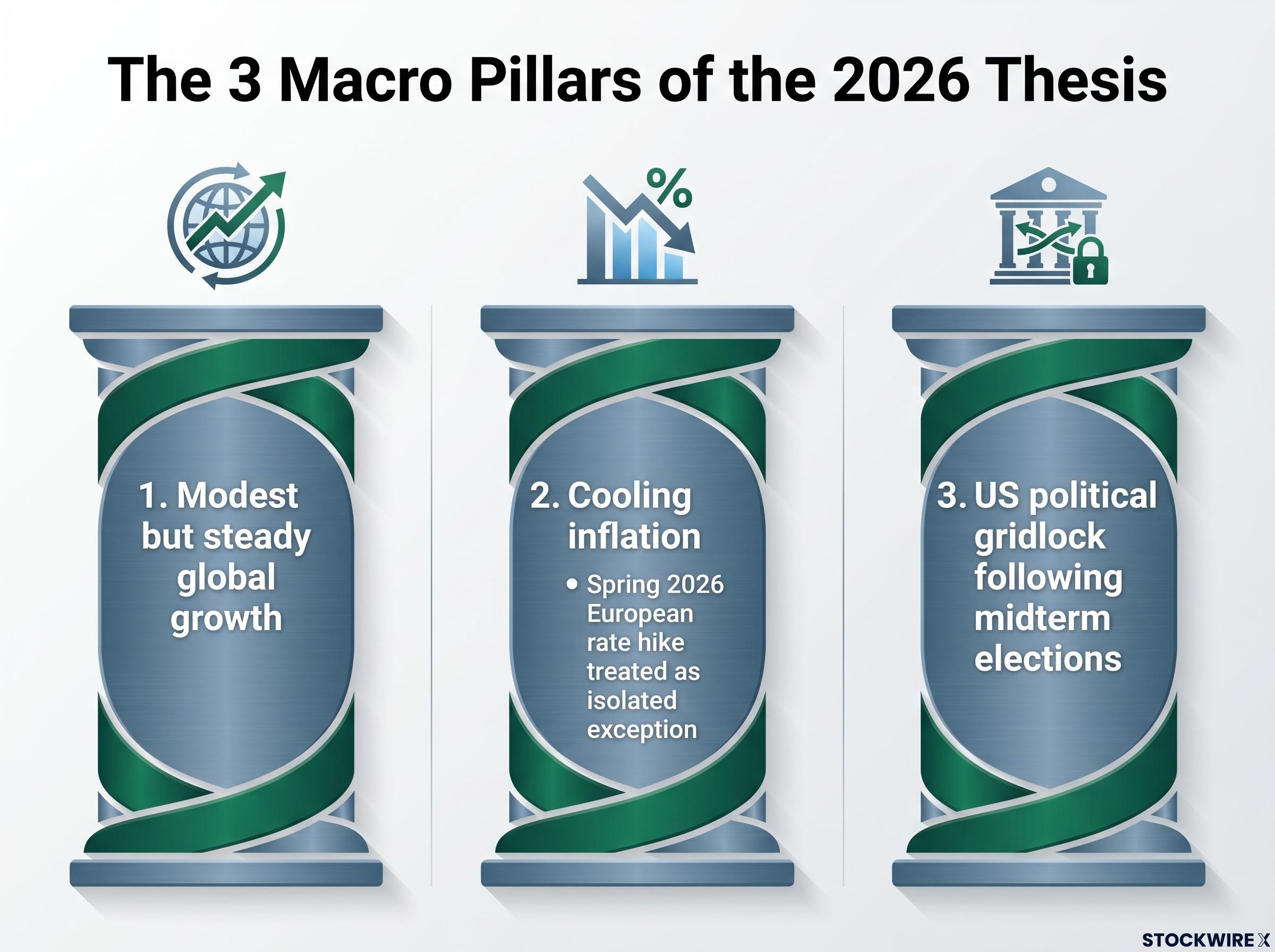

The bull-market forecast did not rest on a single claim. It was built on three macro pillars, each of which you can assess independently at the halfway mark.

Global central bank divergence adds a layer of complexity to the rate stability assumption embedded in Fisher’s thesis: the Fed holding at 3.50-3.75%, the ECB poised to hike into near-recession conditions, and the BOJ tightening faster than expected each represent distinct pressures on the macro environment Fisher’s model assumes will remain accommodative.

Fisher highlights that US midterm elections tend to produce legislative gridlock, which historically has been a tailwind for stocks in the back half of the election year and the subsequent first half.

For investors holding globally diversified equity positions, these three pillars are the specific conditions to monitor through H2. If they shift materially, the ongoing forecast deserves revision. If they hold, so does the outlook.

The aggregate return figure tells one story. The relative performance picture underneath it tells another, and Fisher’s original forecast carried explicit calls at this level too.

The 2026 outlook favoured non-US stocks over US stocks, value over growth, and US tech “doing fine but not leading the world.” These were not throwaway observations. They were testable, layered predictions that investors with style or geographic tilts can evaluate independently of the headline index return.

At the mid-year mark, Ken Fisher characterised global stocks as having behaved largely as expected, with some segments modestly better and some modestly worse. His summary of the year: “working out pretty well, not perfectly.”

| Asset Class / Segment | Original 2026 Forecast Call | Mid-Year 2026 Assessment |

|---|---|---|

| US equities | Positive but not leading | Broadly in line |

| Non-US equities | Outperforming US | Largely as expected |

| US technology | Fine but not leading the world | Participating, not dominating |

| Value stocks | Outperforming growth | Modestly tracking |

If your portfolio carries a tilt toward value or non-US equities, these are the specific positions Fisher’s original thesis favoured. The mid-year data suggests those relative bets are broadly tracking as intended. Relative performance analysis is often overlooked in favour of absolute return figures, but a well-constructed forecast carries layers, and it deserves evaluation at each one.

Fisher’s greater-than-10% full-year forecast remains intact as of the mid-year review.

With H1 delivering approximately 9%, the full-year target of above 10% requires only modest additional gains in the second half to be met.

That arithmetic is favourable, but it does not mean the forecast has already been settled. The original outlook carried specific expectations about how H2 would unfold, and these remain open questions that you can monitor against a defined set of markers.

Forecasts only deliver value to investors who know how to track them in real time. These four markers turn Fisher’s mid-year update into a live monitoring framework you can apply through year-end.

The Fisher mid-year review is useful beyond its specific numbers. It embeds three lessons about how institutional forecasting works, lessons that apply to any market outlook you encounter.

Fisher’s triage question, whether a surprise materially alters earnings, growth, or risk premia, is itself a partial answer to a deeper problem: forecasting blind spots in any model, whether human or algorithmic, are concentrated in the tail outcomes that consensus tools systematically compress away, making explicit scenario analysis a necessary complement to any probabilistic regime call.

Ken Fisher’s summary of the year as “working out pretty well, not perfectly” is itself a forecasting lesson. It tells you that the firm defines success as getting the regime right, not getting every detail right.

The skill of evaluating forecasts is itself worth developing. Knowing when a prediction has genuinely broken down versus when it is simply taking a different path is worth more than knowing whether any specific number was hit. That is the reusable takeaway from this mid-year check, and it applies well beyond Fisher’s 2026 outlook.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Fisher Investments entered 2026 forecasting global equity returns above 10% for the full year, with a muted and choppy first half followed by strength building toward Q4, and a preference for non-US stocks, value over growth, and US tech participating but not leading.

Global equities posted roughly 9% gains in the first half of 2026, ahead of the subdued H1 Fisher expected but broadly consistent with the firm's full-year direction call; Ken Fisher described the year as 'working out pretty well, not perfectly' and characterised the deviation as 'not too far off' the original forecast.

The firm did not anticipate the war in Iran or a European central bank rate hike in spring 2026; Fisher assessed both as having limited impact on the underlying bull-market thesis because neither materially altered the earnings, growth, or risk premia conditions the forecast was built on.

Fisher applies a hierarchy that prioritises direction first, broad regime patterns second, and quarterly timing last; a forecast that gets the regime right but sees returns arrive earlier than expected is treated as passing its primary test, not as a failed prediction.

The firm's H2 outlook depends on non-US and value stocks continuing to lead, US tech participating without dominating, political gridlock persisting as a market tailwind, and Q4 delivering a further leg of strength consistent with the original timing call.