Every major central bank held rates in April 2026, yet the word “hold” has never meant more different things at once. The Federal Reserve is frozen by inflation it cannot shake. The European Central Bank is preparing to hike into a near-recession. The Bank of Japan is tightening faster than almost anyone expected. Deutsche Bank’s freshly released World Outlook crystallises what has become the defining macro story of mid-2026: a single global inflation shock producing radically divergent central bank responses, with the Fed at 3.50-3.75%, the ECB at 2.00%, and the BOJ at 0.75%, each facing a fundamentally different growth-inflation trade-off. What follows maps why each central bank is in its particular corner, what the divergence means for sovereign bond yields and equity markets across regions, and how investors can use the global central bank policy gap as an analytical lens rather than a source of confusion.

One inflation shock, three irreconcilable policy positions

The same energy-driven inflation shock has hit every major economy. The responses could not be further apart.

SEI Investments Canada characterised the April 2026 meeting cycle as a moment of deceptive surface calm: all five major central banks held rates, yet the divergence in their forward risk profiles has rarely been wider. Identical macroeconomic catalysts have produced the opposite of policy consensus because the structural features of each economy, energy dependence, fiscal capacity, labour market dynamics, have bent the response in incompatible directions.

The three-way split serves as the analytical scaffolding for the rest of this piece. The Fed is frozen by persistent inflation and a divided committee. The ECB faces the prospect of hiking into an economy on the edge of technical recession. The BOJ is tightening more aggressively than anticipated while its growth outlook deteriorates.

| Central Bank | Current Rate | Last Meeting | Next Meeting |

|---|---|---|---|

| Federal Reserve | 3.50-3.75% | 28-29 April 2026 | 16-17 June 2026 |

| European Central Bank | 2.00% | 30 April 2026 | 10-11 June 2026 |

| Bank of Japan | 0.75% | 27-28 April 2026 | 15-16 June 2026 |

Investors who treat all three holds as equivalent signals will systematically misread the direction of travel in each region.

When big ASX news breaks, our subscribers know first

Why the Fed is stuck: neutral rates, core inflation, and a divided committee

The Fed’s paralysis is not indecision. It is a genuine analytical disagreement, playing out inside the committee, about what the data permits.

Chair Jerome Powell’s March 2026 characterisation of the current rate anchors the bind. The rate cuts executed in late 2025 brought the federal funds rate into what Powell described as:

“A range of plausible estimates of neutral,” with inflation that “remains somewhat elevated” relative to the 2% goal.

That framing explains why the Fed neither sees current policy as clearly restrictive nor clearly accommodative. It is, by its own assessment, in a zone of uncertainty.

The Federal Reserve’s March 2026 Summary of Economic Projections sets out FOMC participants’ own estimates for the neutral federal funds rate alongside core PCE inflation forecasts through 2028, providing the quantitative basis for Powell’s characterisation of current policy as sitting inside a range of plausible neutral estimates rather than clearly above it.

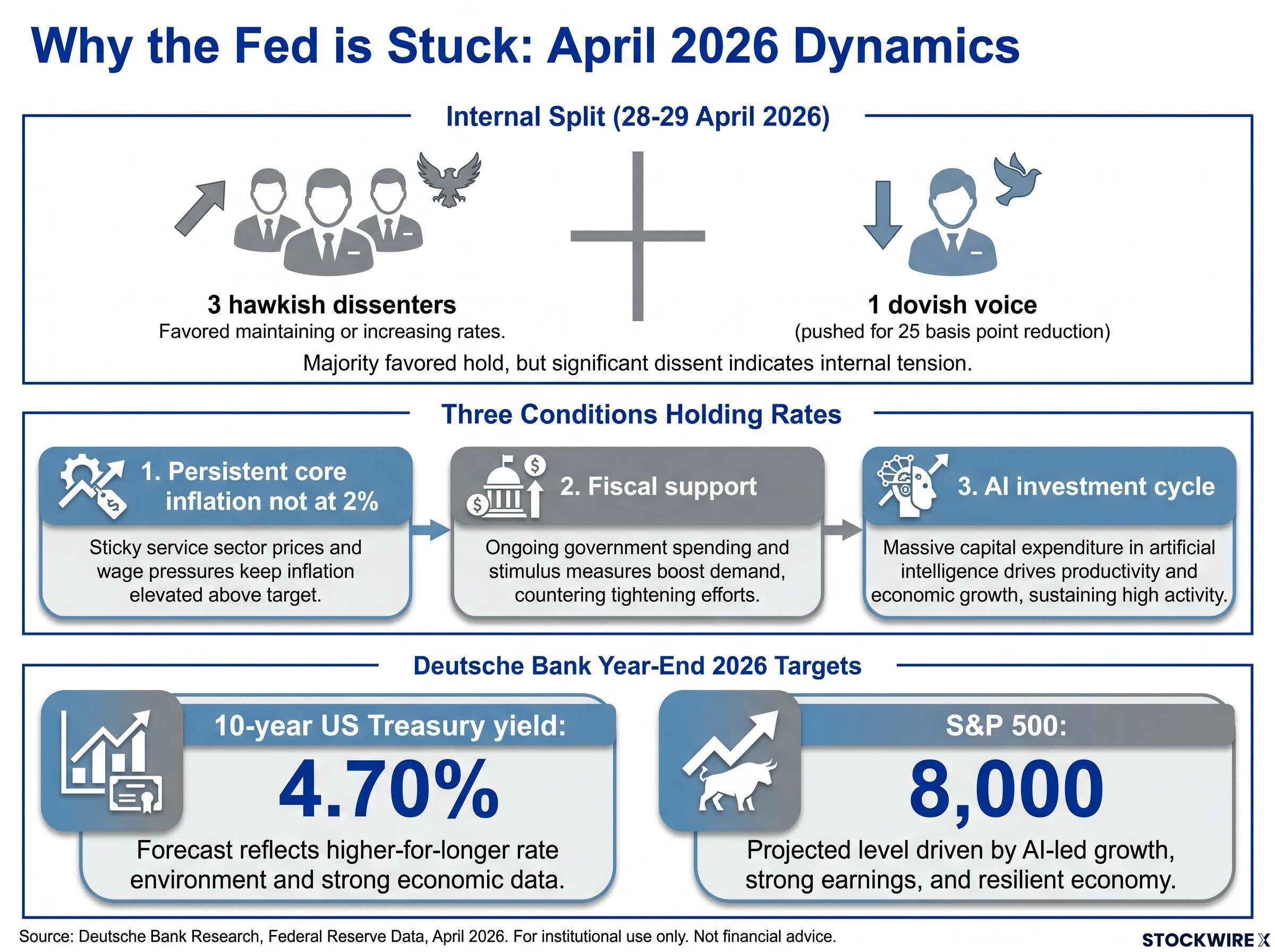

The 28-29 April FOMC meeting, characterised as Powell’s final meeting as Chair, revealed a genuine internal fracture. Three members dissented against language leaving the door open to resumed rate cuts, while one member pushed for an immediate 25 basis point reduction. The split is meaningful: the hawkish dissenters outnumber the dovish voice three to one.

The FOMC’s internal fracture runs deeper than a single meeting’s dissent count suggests; inflation has now exceeded the 2% target for five consecutive years, raising the risk that any committee member who pivots dovish too early will be seen as capitulating to politically uncomfortable data rather than responding to genuine disinflation.

Deutsche Bank’s assessment sharpens the picture further. Persistent core inflation, strong fiscal support sustaining demand, and an AI-driven capital investment cycle sustaining growth make rate cuts essentially indefinitely deferred. The bank projects 10-year US Treasury yields reaching 4.70% by year-end 2026 under its baseline scenario.

Three conditions are keeping the Fed on hold:

- Persistent core inflation that has not returned sustainably to 2%

- Fiscal support continuing to underpin aggregate demand

- The AI investment cycle sustaining business capital expenditure and growth

That 4.70% year-end yield target is a concrete planning point. A frozen Fed with an increasingly hawkish internal lean has direct consequences for the relative attractiveness of US versus European fixed income.

What it means for a central bank to hike into a near-recession

The stagflation arithmetic: why holding is not neutral

A central bank facing supply-driven inflation alongside fragile growth cannot simply choose the easier path. Both inaction and aggressive tightening carry asymmetric risks.

When inflation rises faster than the nominal policy rate, a central bank that holds rates in real terms may actually be easing, because the real rate (the policy rate minus inflation) falls. Inaction becomes an active policy choice with its own consequences: it risks embedding inflation expectations while appearing passive. The ECB itself has cited the Middle East conflict as a complicating factor weighing on the European growth outlook, a supply shock that monetary policy cannot resolve but cannot ignore either.

This is the euro area’s specific vulnerability. Energy import dependence amplifies the inflationary shock while simultaneously compressing household and business incomes, producing the conditions for both elevated prices and stagnant output. That combination, above-target inflation alongside sub-trend growth, is the definition of a stagflation trap.

Deutsche Bank cut its euro area GDP growth estimate for 2026 sharply:

The euro area growth picture is grimmer at the sub-index level than the headline GDP figure alone conveys: Q1 2026 growth came in at just 0.1% quarter-on-quarter while April 2026 inflation re-accelerated to 3.0% year-on-year, narrowing the ECB’s ability to hold without its real rate turning increasingly negative.

Euro area GDP growth forecast: 0.5%, placing the region on the edge of a technical recession.

Against that backdrop, the ECB held its main policy rate at 2.00% on 30 April 2026, its seventh consecutive hold, with no pre-committed hike path. Deutsche Bank, however, projects 50 basis points of ECB rate increases across summer 2026 in response to upward-revised regional inflation. The 10-11 June Governing Council meeting is the first summer 2026 decision point.

SEI Investments Canada highlights elevated stagflation risks in energy-vulnerable regions including Europe and the U.K., where central banks face more binding growth constraints than the Fed. The ECB’s potential hike cycle into near-zero growth is the most counterintuitive element of the 2026 divergence story, and the one with the most direct implications for European sovereign bond spreads and equity valuations in rate-sensitive sectors.

Japan’s hawkish pivot and Asia’s energy fault line

Japan’s tightening is not a laggard catching up to global norms. It is an economy being forced into higher rates by a structural energy vulnerability before the underlying growth picture can comfortably support it.

The 27-28 April BOJ decision held at 0.75% on a 6-3 vote, itself a signal of internal division about the pace of further tightening. Three dissenting members is a substantial minority on a nine-member board.

Deutsche Bank characterises Japan as facing a more aggressive-than-anticipated tightening cycle alongside a weaker growth profile. Energy import vulnerability is the differentiating factor. Japan imports the vast majority of its energy; when global energy prices spike, the inflationary impact is amplified directly into consumer prices, forcing the central bank to respond even as higher energy costs simultaneously suppress growth.

The intra-Asian contrast sharpens the picture:

- Energy exposure: Japan is heavily energy-import-dependent; China has greater domestic energy capacity and diversified supply

- Monetary policy direction: The BOJ faces further tightening pressure; China has more room to support growth

- Growth outlook: Deutsche Bank expects China to fare better than Japan, with strong export activity limiting macroeconomic harm from the energy shock

Investors treating Asia as a single bloc will systematically underweight the Japan-specific tightening risk and overweight the apparent stability of regional average growth. The divergence within Asia is as significant for portfolio construction as the transatlantic divide.

What policy divergence means for bonds, equities, and cross-regional allocation

The three-way policy split translates into distinct, simultaneous pressures across fixed income and equities, a configuration that changes the logic of traditional cross-regional diversification.

BIS research on monetary policy uncertainty and cross-border spillovers finds that heightened uncertainty about neutral rates amplifies international transmission effects, meaning the kind of three-way divergence documented in mid-2026 generates larger spillovers across bond and equity markets than equivalent divergence in a lower-uncertainty environment.

US yields are being pushed higher by the frozen Fed’s hawkish lean. European sovereign spreads face pressure from the prospect of the ECB hiking into weak growth, a combination that stresses peripheral debt more than core. Japanese government bonds face price pressure from an accelerating tightening cycle that few positioned for a year ago. Sovereign bond prices face headwinds across all three regions at once.

Deutsche Bank maintains its S&P 500 year-end 2026 target at 8,000, reflecting the view that strong US corporate earnings can withstand higher yields.

The equity valuation dislocations created by the frozen Fed are most visible at the sector level: technology, growth, and small-cap equities were trading at historically rare discounts of 23%, 21%, and 17% respectively to Morningstar fair value as of early May 2026, while energy had moved from the most undervalued to the most overvalued sector in a single calendar year, driven by the same oil shock that is keeping the Fed on hold.

European equity valuations face a more difficult trade-off. Stagflation risk compresses both the growth numerator and the discount rate denominator in valuation models, a double headwind that does not apply with the same force in the US, where fiscal support and AI-driven capital expenditure sustain the earnings cycle.

SEI Investments Canada notes that US policy staying tighter for longer relative to peers has implications for global bond markets, specifically higher US yields relative to others, and regional equity performance, particularly in Europe where stagflation risk is elevated.

| Region | Policy Direction | Bond Market Implication | Equity Market Outlook |

|---|---|---|---|

| United States | Frozen, hawkish lean | Yields pushed higher; 4.70% 10-year target (Deutsche Bank) | Constructive; corporate earnings resilient |

| Euro Area | Potential hikes into weakness | Sovereign spreads under pressure | Stagflation risk compresses valuations |

| Japan | Aggressive tightening cycle | JGB prices face sustained pressure | Growth outlook weakened by energy costs |

Deutsche Bank’s macro view, sovereign bond yields edging higher while equity markets remain constructive supported by solid corporate earnings, holds in the US. It holds less comfortably in Europe and Japan, where the growth side of the equation is materially weaker.

The divergence is the signal, not the noise

The incompatibility of these three central bank paths is not disorder. It is the logically coherent outcome of the same shock hitting three economies with different structural vulnerabilities, different policy mandates, and different political economies. Once the underlying constraints are mapped, the divergence becomes analytically useful rather than overwhelming.

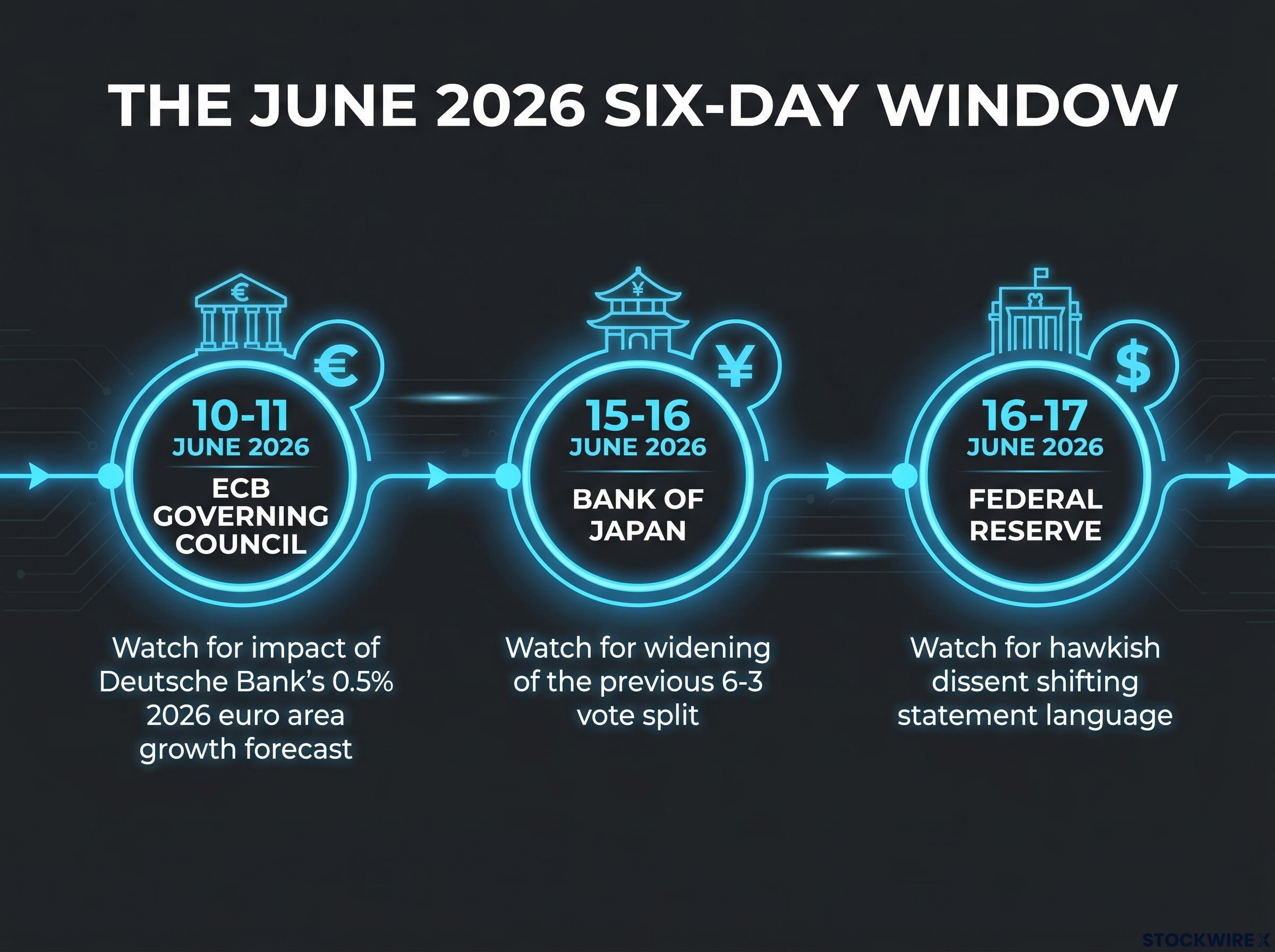

The next major test arrives quickly. Three central bank meetings fall within a six-day window in June 2026:

- ECB Governing Council on 10-11 June: Will the ECB begin the hike cycle Deutsche Bank projects, or will the 0.5% growth forecast force another hold?

- BOJ on 15-16 June: Does the 6-3 vote split widen toward further tightening, or does weaker growth data stabilise the current rate?

- Fed on 16-17 June: Does the hawkish dissent from April harden into a formal shift in the statement language, or does a leadership transition reset the tone?

Warsh’s inheritance is as challenging as any incoming Fed chair has faced in decades: headline CPI at 3.8%, Brent crude above $107, and a committee where three regional presidents have already called publicly for rate hikes by Q3 2026, a combination that limits the new chair’s ability to signal any dovish reset without immediately repricing Treasury markets.

The Deutsche Bank World Outlook provides the analytical framework, but June’s meetings will supply the confirming or disconfirming evidence. The investor who understands why each central bank is where it is holds a structural advantage over one who treats each rate decision as an isolated event.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.