Mid-2026’s Biggest Market Risks, Ranked by Actual Probability

5 hrs ago

Jesse Livermore made roughly $100 million shorting the 1929 crash, the equivalent of $1.5-1.8 billion in today’s dollars. He died bankrupt eleven years later. The crash did not ruin him. His framework did.

In periods of systemic market disruption, investing during a market crash forces a question most participants never explicitly ask. They focus on what to buy or sell rather than whether the mental model they are using was built for a functioning market or a breaking one. The 1929-1934 period produced three investors whose wildly divergent outcomes cannot be explained by luck or information advantage. What separated them was the architecture of their decision-making frameworks.

What follows reconstructs the strategic logic behind Livermore, Baruch, and Kennedy’s approaches, identifies why each framework succeeded or failed at particular phases of the crisis, and draws direct parallels to the decisions investors face when elevated volatility and ambiguous recovery signals make old instincts dangerous.

Bernard Baruch sold before the peak. That decision alone would have been enough to preserve capital, but what followed was more instructive than the exit itself. Rather than watching prices for re-entry signals, Baruch built a monitoring framework around four categories of systemic stress:

His positioning reflected these inputs. Baruch moved into hard assets and gold mining assets, not as growth instruments but as preservation vehicles. The objective was not to outperform. It was to ensure capital survived a scenario where the crisis deepened and lasted longer than consensus expected.

“Where can capital survive if this gets worse and lasts longer than expected?”

That question, not “where is the highest return?”, defined the Baruch framework. Historical accounts indicate he avoided the worst losses of the Depression years while many contemporaries were wiped out. The honest cost was significant upside foregone; if recovery had arrived faster than macro indicators suggested, the approach would have looked overcautious. In environments where debt levels are high and policy credibility is uncertain, however, not losing everything is itself a sophisticated and rational objective.

The trade-off Baruch accepted, significant upside foregone in exchange for capital survival, has a measurable modern equivalent: crash protection costs for a traditional 60/40 portfolio ran to approximately 14 percentage points of underperformance against the S&P 500 in 2024 alone, a concrete illustration of why the Baruch framework looks overcautious in fast recoveries and indispensable in extended deteriorations.

Livermore’s toolkit was price action, tape reading, momentum, and sentiment. In 1929, these were the right instruments for the right moment. The market was trending sharply downward, panic was accelerating, and price was the clearest real-time signal available. Livermore read it better than almost anyone alive.

His short positions generated an estimated $100 million in profits. The original source estimates his peak accumulated value approached $2 billion in present-day equivalent. For a brief period, he was among the wealthiest individuals in the country.

NBER research on investor psychology during market crashes documents the anxiety, perceived overvaluation, and herding behaviour that characterise systemic selloffs, providing empirical grounding for why momentum-driven frameworks like Livermore’s amplify losses when sentiment turns from fear into forced liquidation.

The crisis did not end with the initial crash. What followed was a multi-phase structure: crash, rally, second leg down, policy shocks, and structural deterioration that unfolded over years rather than weeks. In this environment, prices no longer reliably distinguished genuine recoveries from what can be called “trap-door rallies,” bear-market bounces not supported by genuine improvement in credit spreads, bank funding conditions, or policy credibility.

Livermore read one of these rallies as a return to normalcy and re-entered at the wrong phase. The same momentum instincts that produced his greatest triumph became the mechanism of his destruction. A framework built to read trending markets could not diagnose a market where the underlying credit, banking, and policy structure was still deteriorating even as prices bounced.

The systematic selling mechanics embedded in modern trend-following funds create a structural analogue to Livermore’s price-following framework operating at institutional scale; Bank of America’s June 2026 CTA trigger map estimated that a 3% S&P 500 decline could unleash approximately $100 billion in programmatic global equity selling, meaning momentum-driven exits are no longer the decisions of individual traders but automated responses encoded into the market’s own architecture.

He made and lost several fortunes in the years that followed. On 28 November 1940, Jesse Livermore died bankrupt by suicide.

“Skilful execution inside the wrong framework can still end in ruin.”

His arc demonstrates a principle that extends far beyond 1929: being correct about a crash is not the same as surviving the period that follows it. The framework that wins the first phase can be the one that destroys capital in the second.

Stripped to their structural logic, the three approaches represent distinct answers to a single question: what inputs should drive capital allocation during a systemic crisis?

Livermore’s price-following framework used prices, momentum, and sentiment as the complete toolkit. The objective was trading performance. The core assumption was that price movement itself contains sufficient information to guide positioning.

Baruch’s systemic-stress framework used credit conditions, banking health, and policy signals as primary inputs. The objective was capital preservation. The core assumption was that system-level resilience matters more than individual price signals when the system itself is under strain.

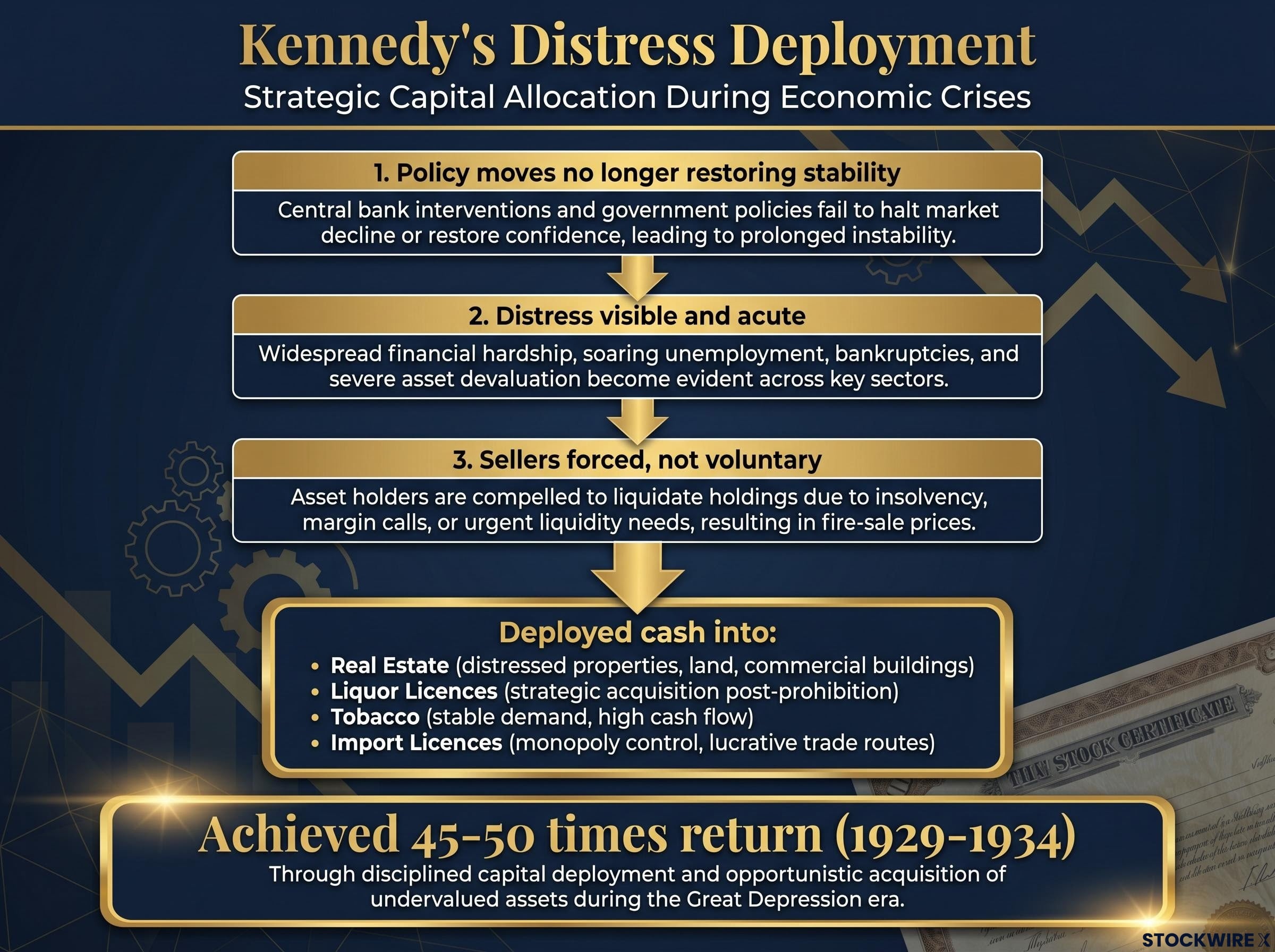

Kennedy’s policy-impact decay framework used the effectiveness of successive policy interventions as the primary signal. The objective was deploying cash into distressed assets at the point of maximum forced selling. The core assumption was that authorities will act, but each action will produce less stabilisation than the last, and the moment of peak policy fatigue is the moment of greatest opportunity.

| Framework | Exemplar | Core Input | Objective | Main Risk |

|---|---|---|---|---|

| Price-Following | Livermore | Prices, momentum, sentiment | Trading performance | Trapped by false rallies in a broken system |

| Systemic-Stress | Baruch | Credit, banks, macro policy | Capital preservation | Misses upside if recovery is quick |

| Policy-Impact Decay | Kennedy | Effectiveness of interventions | Distress deployment | Long, painful waiting; timing risk |

No framework is universally superior. The error is applying the wrong one to the wrong crisis type.

The question that governs framework selection is not “what should I buy?” but rather: is the framework currently in use designed for a normally functioning market, or for a multi-phase systemic crisis?

Decades of central bank-backstopped markets conditioned buy-the-dip reflexes across an entire generation of investors. Those instincts were trained in a specific regime. If that regime no longer exists, the instincts it produced may not transfer to a genuine systemic crisis. The structural question, which macro environment trained my current habits, precedes every individual trade decision.

Joe Kennedy held cash while others deployed. He watched policy interventions arrive, produce a brief reprieve, and then fade. He watched each successive intervention move the needle less than the one before. And he waited.

His deployment criteria were specific and demanding:

When all three conditions aligned, Kennedy moved aggressively into distressed assets: real estate, liquor licences, tobacco, and import licences. According to the original source, he achieved an approximate 45-50 times return on invested capital during the 1929-1934 period. He later became the first chairman of the Securities and Exchange Commission (SEC), reflecting his deep understanding of market structure and regulatory dynamics.

“Cash in a systemic crisis is not money not working. It is the mechanism to exploit policy fatigue.”

The psychological cost of this approach was severe. Kennedy sat out many attractive-looking rallies. Research on the period describes this discipline as extremely difficult to sustain, because each rally looks like the moment the crisis has ended, and sitting in cash while others appear to profit feels like failure. The difficulty is the point. The returns Kennedy captured were available precisely because so few investors could tolerate the waiting required to access them.

The 1929-1934 period was not a single event. It was a multi-phase crisis in which the initial crash, subsequent rallies, policy interventions, and structural deterioration unfolded over years. The current environment of elevated volatility, intermittent policy interventions, and ambiguous recovery signals shares that multi-phase structure.

The specific habit that decades of central bank support created, buying anticipated dips before the intervention has even arrived, is precisely what the framework audit is designed to question. That habit was rewarded in a regime where central banks had the tools and credibility to backstop markets reliably. Whether that regime still holds in its entirety is the open question.

Safe haven asset performance in the 2026 supply-side shock has reinforced the Baruch framework’s core warning in a contemporary setting: gold surged to $5,400 an ounce before retreating 13-15%, bonds repriced against inflation expectations, and the Japanese yen weakened simultaneously, leaving investors who assumed traditional preservation instruments would function as expected with fewer defensive options than their frameworks had anticipated.

The research identifies four stress-monitoring categories for assessing which framework applies:

The bias-toward-confirmation principle accepts a specific trade-off: missing the first leg of a genuine recovery in exchange for avoiding catastrophic engagement with a false one. Multi-variable improvement across credit, banking, policy, and prices together, not a single large up-day in an index, is the confirmation signal this framework requires.

It is worth noting that some analysis flags a potential inflationary-to-deflationary transition as a key trap-door risk in the current environment, though the timing and probability of such a shift remain unverified.

Three questions can structure the self-audit before any deployment decision:

For investors who want to convert the three-framework diagnostic into concrete portfolio actions, our dedicated guide to portfolio crisis preparation provides an eight-point checklist covering liquidity buffer sizing, drawdown stress testing, concentration audits, and rules-based rebalancing triggers, each step actionable within a week regardless of whether a downturn arrives.

Three investors navigated the same crisis with access to similar information. One made a fortune and lost it. One preserved capital through the worst years. One generated a 45-50 times return by deploying cash at the point of maximum distress.

The divergence was not produced by superior information or better market calls. It was produced by whether each investor’s framework was matched to the type and phase of crisis they were actually in. Livermore’s price-following approach was the best tool available for the initial crash and the worst possible tool for what followed.

Jesse Livermore, the investor who was most right about the 1929 crash, died bankrupt in 1940. The framework that made him right was the same framework that destroyed him.

The most important pre-trade question in an elevated-volatility environment is not what to buy, but whether the framework being used was designed for normal markets or systemic ones.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Historical case studies are illustrative and subject to interpretation; the frameworks discussed involve significant timing risk and psychological difficulty in practice.

A price-following framework uses price action, momentum, and market sentiment as the primary inputs for trading decisions. Jesse Livermore used this approach to make roughly $100 million shorting the 1929 crash, but the same framework led to his ruin when false rallies in the multi-phase crisis misled his re-entry timing.

Baruch monitored four systemic stress categories: credit conditions, banking system health, monetary and fiscal policy, and inflation or deflation dynamics. He moved into hard assets and gold mining positions as preservation vehicles, prioritising capital survival over return maximisation throughout the Depression years.

Kennedy waited until three conditions were met simultaneously: successive policy interventions were producing diminishing stabilisation effects, distress was observable in forced sales and institutional failures, and sellers were liquidating because they had no choice rather than from a bearish view. This discipline reportedly produced an approximate 45-50 times return on invested capital during the 1929-1934 period.

The article recommends requiring multi-variable confirmation across credit spreads, banking system stress indicators, policy impact trends, and price together, rather than acting on a single large up-day in an index. A genuine recovery shows improvement across all four categories, not just a price bounce.

The article suggests three self-audit questions: identifying which market regime trained the current instinct, confirming whether a preservation or deployment framework is being used deliberately, and checking whether multiple stress indicators have confirmed improvement rather than price alone. This audit is designed to prevent investors from applying a normal-market framework to a systemic crisis.