Apple’s AI Bet Is a Services Play, Not an iPhone Supercycle

2 mins ago

Apple’s headline-grabbing WWDC 2026 announcements and its imminent entry into foldable smartphones have generated considerable investor attention over the past two weeks. The more consequential question, however, is what these moves actually mean for AAPL’s financial trajectory over the next three to five years. With a rebuilt Siri AI, expanded Apple Intelligence capabilities, Google Gemini integration, and a foldable iPhone reportedly on track for a September 2026 debut priced above $2,000, the company is making two simultaneous bets on premium differentiation. Neither, on current evidence, is likely to trigger a near-term supercycle. Both reinforce a specific kind of long-duration investment thesis: AAPL as a steady compounder whose value accrues through ecosystem deepening, services revenue growth, and pricing power retention rather than dramatic hardware volume inflections.

What follows breaks down exactly what Apple’s AI architecture does and does not accomplish for upgrade cycles, why the foldable launch is strategically meaningful but financially modest, and what the combined picture implies for investors evaluating AAPL’s long-term outlook as a durable compounder.

The WWDC 2026 announcements amounted to Apple treating Apple Intelligence as a broadening platform layer, not a narrow feature drop. The specific capability additions span several product surfaces:

These additions are individually incremental. Their significance is cumulative: Apple is building a framework designed to support progressively more capable AI functionality across its ecosystem, not shipping a single marquee feature.

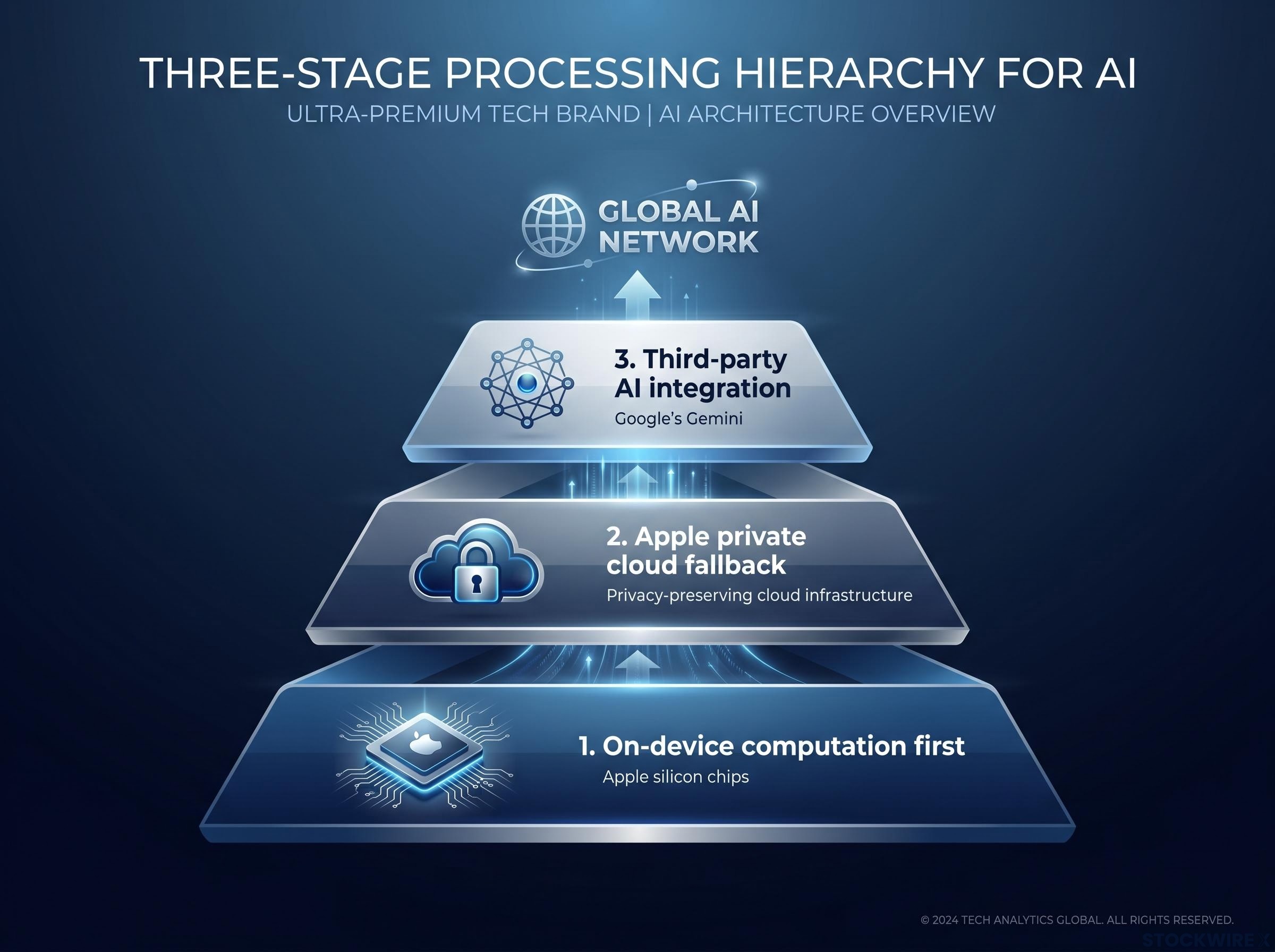

The underlying infrastructure is where the strategic differentiation sits. Apple Intelligence processes computation on-device first, falling back to Apple’s own privacy-preserving cloud layer when needed. This hybrid architecture is explicitly designed to contrast with competitors that rely primarily on external cloud infrastructure, and it reinforces the privacy positioning Apple has spent a decade building.

The full payoff of this design sits on a multi-year horizon. Apple’s stated direction points toward agentic AI functionality, where the system coordinates actions across multiple apps autonomously. That capability is not yet fully realised, but the architectural groundwork laid at WWDC 2026 is designed to support it.

For investors, the distinction between two possible outcomes matters directly for valuation: is Apple Intelligence a catalyst that compresses upgrade cycles and drives a unit-volume surge, or is it a retention lever that deepens ecosystem engagement and grows services revenue per user?

The evidence points firmly toward the latter.

The AI monetisation gap sits at the centre of the market’s ambivalence toward AAPL even as headline metrics set records; Apple’s fiscal Q2 2026 report produced simultaneous all-time highs in revenue, iPhone sales, and EPS, yet shares fell as investors concluded that strong hardware execution does not resolve the open question of how and when Apple Intelligence translates into measurable per-user revenue uplift.

Citi research projects iPhone replacement cycles to hold near approximately four years despite AI enthusiasm, with North American early adopters potentially accelerating upgrades but slower AI uptake in other regions and macroeconomic pressures counterbalancing that effect.

iOS 27 support extending to a wide range of existing iPhones reduces OS-based urgency to upgrade, even where older devices do not receive the full Apple Intelligence feature set. No single WWDC 2026 feature stands out as a “must-upgrade-now” catalyst for the median user.

The financial implications of this distinction are direct:

| Dimension | Ecosystem retention lever | Unit-volume accelerant |

|---|---|---|

| Primary financial impact | Higher services revenue per user | Hardware unit volume surge |

| Monetisation vector | Engagement, ARPU growth | Compressed replacement cycles |

| Valuation implication | Supports higher multiple on services | Justifies pricing in hardware inflection |

Apple Intelligence, as currently constituted, supports the left column. It argues for steady compounding and stable margins over time rather than a sudden volume inflection.

Understanding the infrastructure behind Apple’s AI investments is worth the effort because it determines whether the company’s AI spending creates a durable competitive advantage or merely keeps pace with the industry. The answer sits in three design choices that are genuinely differentiated from the dominant model.

Apple Intelligence operates through a three-stage processing hierarchy:

This architecture contrasts with competitors that route most AI computation through external cloud infrastructure from the outset. Apple’s approach means user data stays closer to the user, which reinforces the company’s privacy brand and creates a structural differentiation that competitors cannot replicate without redesigning their own AI stacks.

The most advanced Apple Intelligence features remain limited to devices with recent Apple silicon chips. In practice, this means older iPhones receive some AI capabilities but not the full feature set, creating a tiered value proposition that maps directly onto the hardware upgrade cycle.

This gating creates a genuine tension Apple must manage carefully. Too restrictive, and the company risks consumer frustration and potential regulatory scrutiny over artificially limiting software features to drive hardware sales. Too generous, and the incentive to upgrade for AI access weakens. How Apple calibrates this line over the iOS 27 and iOS 28 cycles will be a telling signal for investors watching upgrade dynamics.

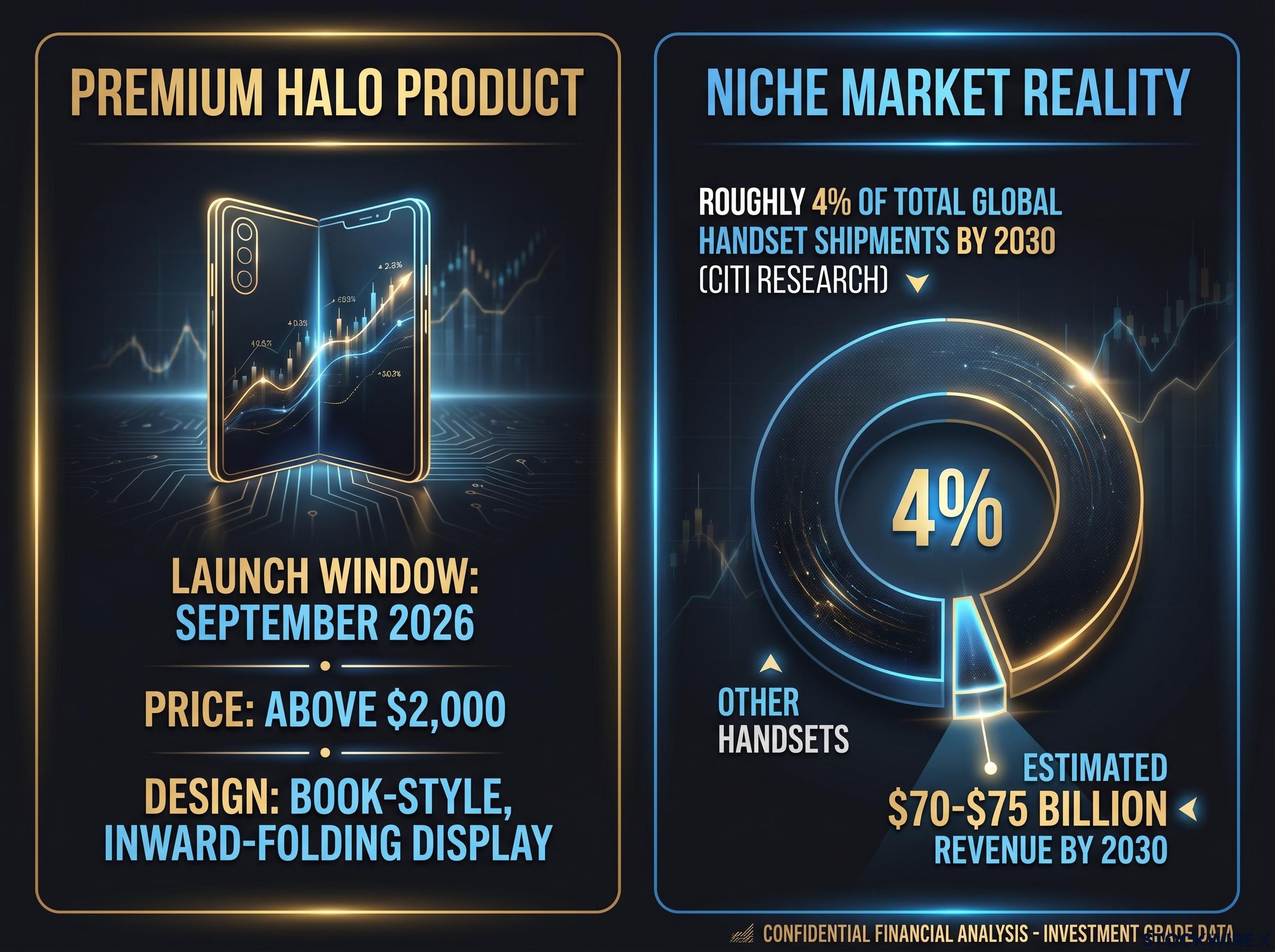

Multiple independent reports place Apple’s first foldable iPhone in the September 2026 launch window, with a book-style, inward-folding display and a price point above $2,000. Supply-chain sources indicate production has slipped relative to initial internal schedules, and initial volumes are expected to be constrained.

The strategic logic for Apple’s entry is straightforward: participation in every major premium form factor defends share at the very top of the market and prevents competitors from owning a visible innovation frontier. The financial reality is more measured.

Foldable smartphones are projected to account for roughly 4% of total global handset shipments by 2030, according to Citi research, underscoring their status as a premium niche rather than a mainstream volume category.

| Parameter | Expectation |

|---|---|

| Expected launch window | September 2026 |

| Price range | Above $2,000 |

| Initial volume profile | Constrained; production slipped from internal schedules |

| Foldable category share by 2030 | Approximately 4% of global handset shipments |

| Strategic classification | Halo and signalling product; brand defence |

Some industry estimates suggest foldable smartphone revenue could reach $70-$75 billion by 2030, though this figure has not been independently verified. Even under optimistic projections, the broader smartphone market is growing at low single-digit annual rates, meaning foldables remain a minority share of total revenue through the end of the decade. Investors who anchor expectations to category-level market forecasts rather than launch-week coverage will build a more accurate model for the foldable’s contribution to AAPL revenue.

The IDC foldable smartphone forecast projects the category growing at a CAGR of 17% through 2029, with foldables representing over 10% of total smartphone market value by that year, a trajectory that makes Apple’s 2026 entry well-timed for capturing share as the segment matures rather than after it does.

The two strategic threads, AI ecosystem deepening and foldable market entry, converge on a single characterisation of AAPL’s investment profile. Each pillar maps to a specific financial mechanism:

Neither pillar, on current evidence, is likely to alter revenue trajectories materially in the next one to two years. The Citi four-year replacement cycle projection remains intact. The foldable category remains a niche through 2030. The AI announcements deepen the ecosystem without producing an identifiable earnings inflection point.

AAPL’s historical valuation premium has been tied to ecosystem stickiness, pricing power retention, and services margin expansion rather than dramatic earnings step-changes. Both the AI architecture and foldable participation reinforce this profile.

Privacy-native AI infrastructure makes switching costs higher for engaged users. Participation in foldables prevents competitive erosion at the top of the market. Services revenue, supported by higher engagement from AI-driven features, continues to carry structurally higher margins than hardware. The combination supports a durable, cash-generative profile that has historically justified premium multiples for AAPL when investors are comfortable with the pace of innovation.

Separating structural advantages from temporary tailwinds is central to any honest valuation of AAPL; the question of durable tailwinds for AAPL, including whether the Q1 2026 smartphone shipment lead reflects genuine share capture or competitor timing gaps, bears directly on how much weight investors should place on recent earnings momentum when modelling the services compounding thesis.

The steady-compounder thesis depends on several execution variables that investors can monitor directly:

Investors wanting to map the full downstream implications of Apple’s hardware supply decisions will find our deep-dive into Apple’s domestic chip manufacturing deal covers the confirmed Apple-Intel agreement for entry-level silicon on Intel’s 18A node, the CHIPS Act subsidy structure supporting the buildout, and the scale gap Intel must close before the relationship can expand beyond non-flagship chips.

A thesis without a falsification framework is not useful. These five signals give investors a structured way to monitor whether the compounding thesis is holding or eroding.

WWDC 2026 and the foldable iPhone launch strengthen Apple’s long-term competitive position without altering near-term financial trajectories. The AI architecture deepens ecosystem retention and supports services revenue growth. The foldable entry defends brand positioning in a premium niche. Neither produces the kind of earnings inflection that would justify short-term event trading.

Apple’s most recent services revenue record of $30.98 billion in fiscal Q2 2026, up 16.3% year over year, provides the clearest available data point for investors modelling the services compounding trajectory; this figure also drove the Q3 2026 guidance surprise that nearly doubled Wall Street’s consensus growth estimate and triggered a significant institutional repricing.

The investor-relevant framing is straightforward: evaluate AAPL on ecosystem durability and services compounding, not on whether AI or foldables trigger an immediate volume surge. Apple’s 2026 product roadmap is consistent with the steady-compounder thesis and rewards patience.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding Apple’s product launches, AI capabilities, and market projections are subject to change based on market developments and company performance.

Apple's 2026 roadmap, including rebuilt Siri AI, expanded Apple Intelligence capabilities, and a foldable iPhone launch above $2,000, supports a steady-compounder thesis built on ecosystem retention, services revenue growth, and pricing power rather than dramatic hardware volume increases.

Citi research projects iPhone replacement cycles will hold near approximately four years despite AI enthusiasm, as iOS 27 supports a wide range of existing devices and no single WWDC 2026 feature creates a compelling must-upgrade-now catalyst for the median user.

Apple's first foldable iPhone is expected to launch in September 2026 at a price above $2,000, with initial volumes constrained due to production slipping from internal schedules.

Apple Intelligence functions primarily as an ecosystem retention tool, deepening user engagement and supporting higher services revenue per user (ARPU growth) rather than compressing replacement cycles or driving a surge in hardware unit volumes.

Investors should watch five signals: Siri AI daily-use adoption rates, how Apple calibrates hardware gating across iOS 27 and iOS 28, foldable screen and hinge quality at launch, regional AI adoption disparities outside North America, and supply-chain yield data on foldable displays heading into a potential second generation in 2027-2028.