Apple Grows Share as Smartphone Market Hits 13-Year Low

3 mins ago

Citi’s research team estimates iPhone replacement cycles will hold at roughly four years even as Apple rolls out its most ambitious AI overhaul in the product’s history. That gap between engineering ambition and consumer behaviour is the tension at the centre of any evaluation of AAPL today.

WWDC 2026 on 8 June gave investors their clearest view yet of Apple’s AI architecture. Within months, the company will also ship its first foldable iPhone into a category that most forecasters agree will remain a premium niche through at least 2030. Both events carry strategic weight, but neither functions as a short-cycle earnings catalyst.

What follows cuts through the product-announcement noise to assess what Apple’s AI roadmap and foldable launch actually signal about the company’s long-term earnings quality, services trajectory, and ecosystem defensibility for US-based investors with a multi-year horizon.

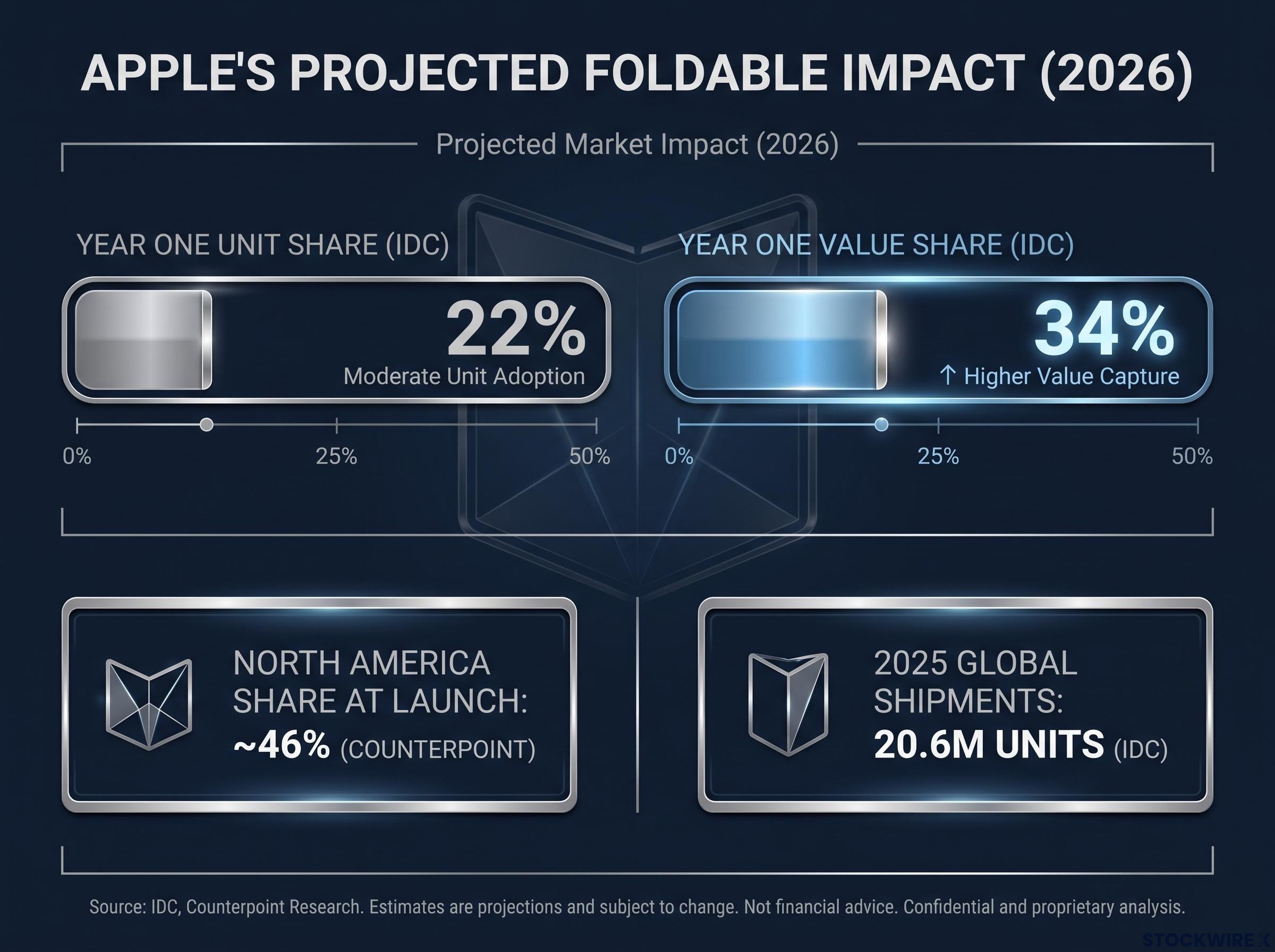

Global foldable shipments reached approximately 20.6 million units in 2025, according to IDC. That figure is projected to grow 20-30% year over year in 2026, pushing annual volumes into the mid-twenties of millions. Against a conventional smartphone market exceeding a billion units annually, foldables remain a fast-growing premium slice, not a mass-market segment.

Apple’s entry, anticipated in the second half of 2026 with supply-constrained initial volumes, is projected to capture approximately 22% unit share and 34% value share in foldables during its first year, according to IDC estimates. Counterpoint Research-style estimates point to roughly 46% of the North American foldable market at launch. The gap between value share and unit share is the investor-relevant signal: Apple will enter this category the same way it entered smartwatches, commanding a disproportionate share of revenue and margin relative to unit volume.

Grand View Research projects the foldable smartphone market reaching approximately $74 billion by 2030 on a mid-teens compound annual growth rate, reinforcing the category’s revenue potential even as unit volumes remain modest relative to the broader handset market.

| Metric | Estimate | Source |

|---|---|---|

| Year One Unit Share | 22% | IDC |

| Year One Value Share | 34% | IDC |

| North America Share at Launch | ~46% | Counterpoint |

| 2025 Global Foldable Shipments | 20.6 million units | IDC |

| 2026 Growth Projection | 20-30% YoY | IDC |

The strategic rationale extends beyond near-term revenue:

Even a dominant position in this category adds a strategically sound but financially modest increment in the near term.

At WWDC 2026, Apple confirmed the architecture underlying Apple Intelligence: a hybrid system where lighter models run on-device while heavier workloads route to Private Cloud Compute on Apple-controlled servers. The design is deliberate. Data either stays on the device or moves to infrastructure Apple owns and verifies, not to generic public cloud.

That privacy architecture is not simply a feature. It is a structural differentiator from cloud-first AI competitors whose default processing model is centralised. The key components of Apple Intelligence as confirmed at WWDC include:

Apple’s chip supply diversification effort, encompassing early-stage talks with Samsung Foundry and Intel Foundry Services over US-based manufacturing, runs in parallel with the AI architecture buildout, since Private Cloud Compute capacity and on-device model performance both depend on sustained access to advanced process nodes.

Apple’s AI data stays on Apple infrastructure, not generic public cloud. This positions the company’s privacy model as a structural moat rather than a marketing claim.

Google’s Gemini role is accurately characterised as a confirmed but evolving component, sitting alongside Apple’s own foundation models rather than functioning as a fixed architectural dependency. As Apple’s proprietary capabilities mature, the balance between internal and external models may shift.

The architectural design clarifies why Apple’s AI payoff is unlikely to appear in quarterly iPhone unit figures. It is far more likely to manifest as services revenue stickiness over a 3-5 year period, as deeper engagement and higher switching costs compound across the installed base.

Previous Siri upgrades improved voice recognition, added language support, or refined response accuracy. Each was incremental. The Siri AI overhaul announced at WWDC 2026 is categorically different because it shifts Siri from a query-response tool to an agentic orchestration layer.

The distinction matters. Siri AI can now initiate and sequence actions across third-party applications using new app intent APIs, meaning it can complete multi-step tasks that span multiple apps without the user manually switching between them. The previous Siri capability set and the new one diverge on several fronts:

Developer testing is underway across iOS 27, iPadOS 27, macOS 27, and visionOS 27 as of June 2026, with an English-language phased rollout beginning fall 2026.

Agentic tasks, those requiring multi-step, cross-app execution, depend on deep operating system integration. Apple has that integration by default. Web-based AI players must negotiate around OS-level permissions, sandboxing, and inter-app communication barriers that Apple controls natively.

Apple’s developer API framework gives it authority over the abstraction layer that agentic assistants depend on. This is the feature category most likely to deepen switching costs over a 3-7 year horizon, and it represents a competitive position that Google or Microsoft would find genuinely difficult to replicate at equivalent depth across Apple’s ecosystem.

A Citi research note places the average iPhone replacement cycle at approximately four years as of mid-2026. A decade ago, that figure sat closer to two years. The lengthening has been steady, and there is no evidence in current data of AI-driven compression.

Citi’s research indicates the iPhone replacement cycle holds at approximately four years, with no measurable pull-forward from AI feature availability as of mid-2026.

The structural factors sustaining this longer cycle are persistent. Macroeconomic headwinds have made consumers more deliberate about premium purchases. Flagship pricing continues to rise. Carrier promotions, not specific software features, remain the dominant trigger for device upgrades. And Apple Intelligence features are bundled with iOS 27 rather than separately monetised, limiting their ability to function as a discrete upgrade catalyst.

| Cycle Period | Approximate Average Replacement Cycle | Primary Demand Driver |

|---|---|---|

| Early iPhone Era | ~2 years | Feature upgrades |

| Mid-2010s | ~3 years | Screen and camera improvements |

| 2024-2026 | ~4 years | Macro conditions and pricing |

Some modest pull-forward among North American users remains plausible as AI-enabled devices become more capable. However, slower uptake in other regions and the absence of a single must-have hardware feature suggest the four-year baseline will persist through at least 2028.

Investors pricing in an AI-driven iPhone supercycle are working from a thesis that current data does not support. Anchoring to the four-year cycle is a prerequisite for constructing a realistic revenue model for AAPL through 2028-2030.

Apple Intelligence and the foldable iPhone are distinct product initiatives, but their financial logic converges on the same outcome: deeper ecosystem retention that converts into incremental services revenue over time.

Bundled AI features do not generate direct revenue today. They deepen engagement, raise perceived ecosystem value, and create the foundation for future subscription expansion. The foldable launch extends Apple’s premium positioning into a new form factor where value share exceeds unit share from day one. Both are retention and monetisation plays at their core, not hardware volume accelerators.

Apple’s most recent services revenue record, $30.98 billion in fiscal Q2 2026, up 16.3% year over year, provides the clearest existing data point for what sustained services momentum looks like before the AI-driven engagement gains from Apple Intelligence are reflected in reported figures.

Apple’s fiscal Q2 2026 results illustrate the gap precisely: the company posted simultaneous all-time records for revenue, iPhone revenue, and EPS, yet the stock fell as investors flagged AI monetisation concerns and the absence of a clear path from bundled features to measurable services revenue growth.

The mapping is direct:

The fall 2026 Siri AI English rollout and the late 2026 foldable launch are platform-initiation events, not earnings inflection points. The back-half-weighted, gradual services growth model is the consensus analyst framing as of mid-2026.

The 2027-2028 services revenue reporting periods represent the earliest window where measurable signals may emerge. Investors evaluating AAPL for a 3-5 year hold need a thesis grounded in services revenue expansion rather than device cycle timing. Both the AI roadmap and foldable launch reinforce that thesis when viewed through the correct lens.

The risks below are ordered from execution variables Apple can influence to structural forces it cannot:

For investors wanting to understand the concrete status of Apple’s manufacturing diversification beyond early-stage talks, the coverage of Apple-Intel foundry collaboration details the confirmed entry-level chip arrangement on Intel’s 18A process node, the 2027 volume production target, and what TSMC’s retained flagship production means for the competitive balance between the two suppliers.

The NIST AI Risk Management Framework establishes the US government’s primary voluntary guidance for trustworthy AI deployment, covering risk identification, governance, and transparency requirements that companies like Apple must navigate as they scale proprietary foundation models and cloud AI infrastructure across regulated markets.

Monitoring signal: Siri AI real-world reviews at the fall 2026 launch represent the earliest quality proxy for the agentic AI thesis. Foldable return and repair rates in early 2027 will follow as the second leading indicator.

None of these risks invalidates the long-term thesis. Each represents a variable that could delay or reduce the services revenue payoff investors are positioned to capture.

Both the AI roadmap and foldable launch are durable investments in ecosystem defensibility, not near-term earnings catalysts. The data signals that will indicate whether the thesis is converting into financial reality are specific: services revenue trajectory from 2027 onward, Siri AI adoption metrics following the fall 2026 rollout, and foldable value share trajectory in the quarters after launch.

Apple’s innovation pipeline supports confidence in its long-term competitive position. However, only investors with a 3-5 year horizon are positioned to capture that value as it materialises through gradual services growth and improved user retention rather than a single-quarter earnings surprise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding Apple’s AI roadmap, foldable launch, and services revenue trajectory are subject to market conditions and various risk factors.

Apple's services revenue hit a record $30.98 billion in fiscal Q2 2026, up 16.3% year over year, and analysts expect AI-driven engagement gains from Apple Intelligence to deepen that trajectory further through the 2027-2028 reporting periods as bundled features convert into measurable subscription and services growth.

At WWDC 2026, Apple confirmed an Apple Intelligence architecture combining on-device foundation models with Private Cloud Compute on Apple-controlled servers, an upgraded agentic Siri capable of cross-app task orchestration via new developer APIs, and a confirmed Google Gemini integration for select workloads.

Citi research places the average iPhone replacement cycle at approximately four years as of mid-2026, up from roughly two years in the early iPhone era, with no measurable evidence that AI feature availability is pulling forward upgrade decisions.

IDC estimates Apple will capture approximately 22% unit share and 34% value share in the global foldable market during its first year, with Counterpoint Research-style estimates suggesting roughly 46% of the North American foldable market at launch.

The primary risks include Siri AI underperforming at launch relative to Google Assistant or Microsoft Copilot, early foldable hardware durability issues, AI engagement gains failing to convert into measurable services revenue, regulatory pressure on AI data handling in the EU and US, and uncertainty around the Google Gemini partnership as Apple's proprietary models mature.