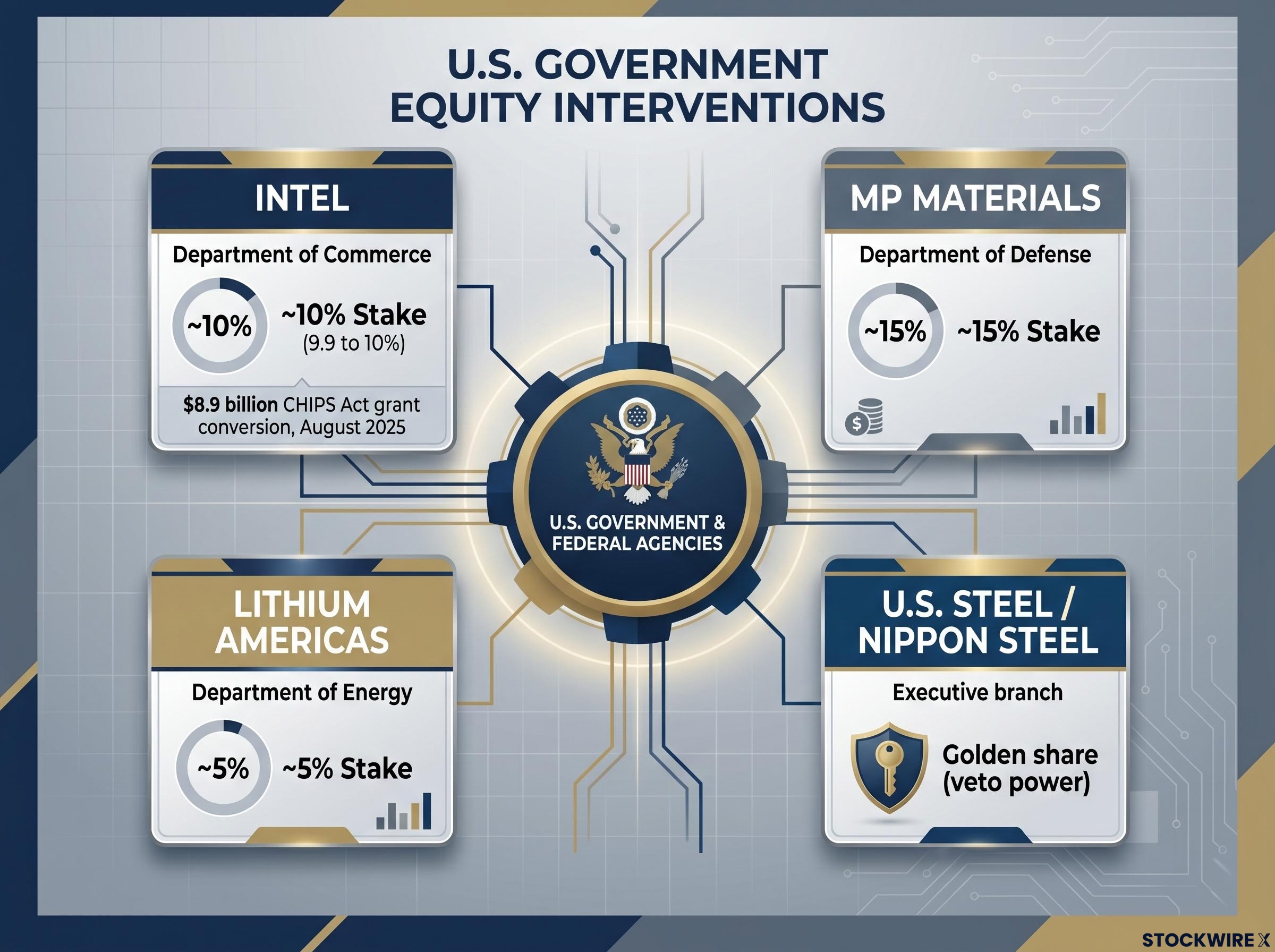

In August 2025, the U.S. government converted CHIPS Act grants into a roughly 10% equity stake in Intel, making Washington a direct shareholder in one of America’s most strategically important chipmakers. Weeks later, a corporate partnership announcement involving that same company was delivered not through standard investor relations channels, but by the president.

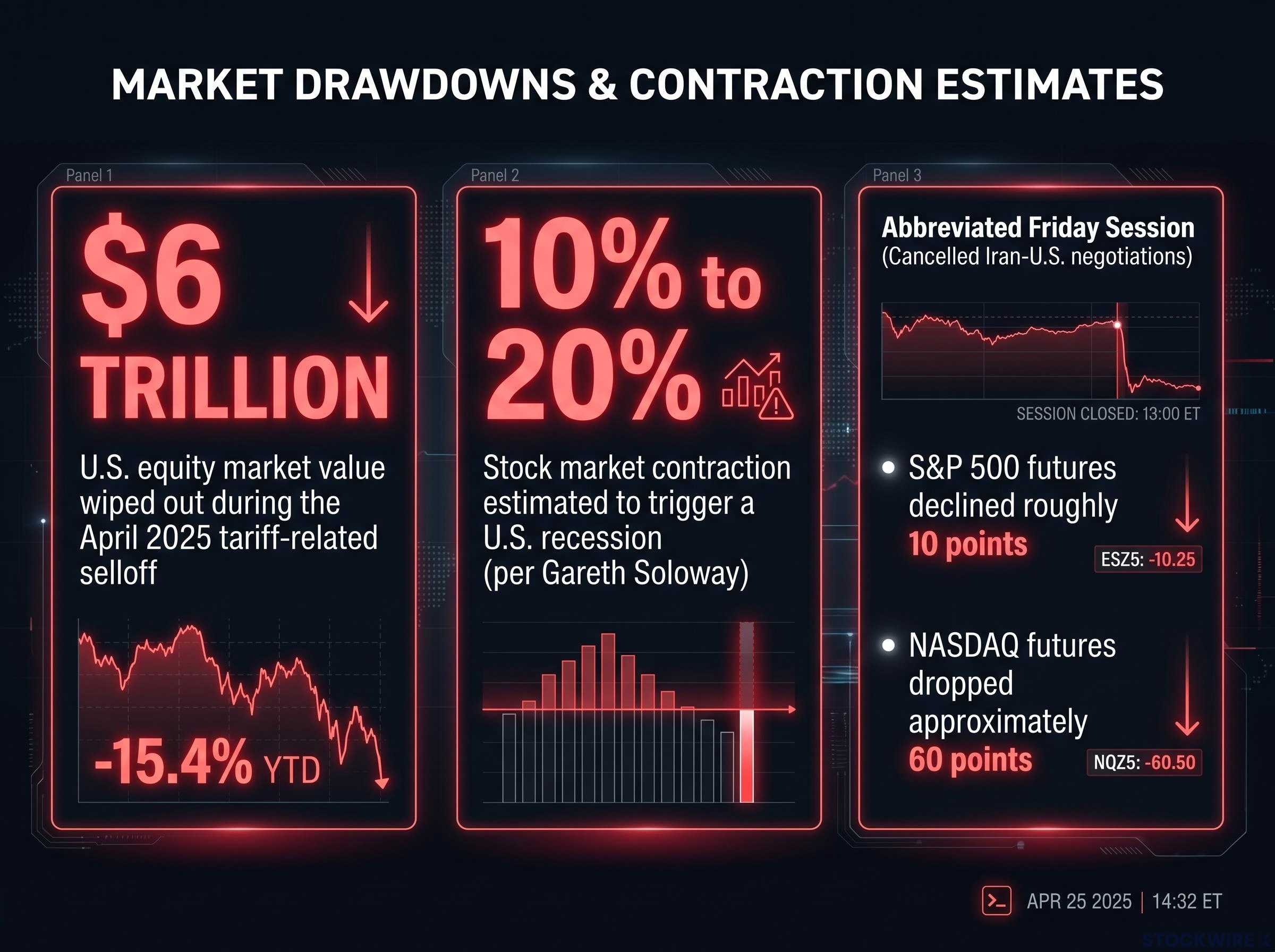

The episode was not isolated. A diplomatic announcement was reportedly moved forward by two days to counteract an unfavourable Federal Reserve statement. A roughly $6 trillion equity drawdown followed a tariff announcement in April 2025. These events raise a question retail investors rarely consider: are equity prices being set by the market, or managed by the executive branch?

What follows is an examination of the documented mechanisms behind political influence on stock market prices, the structural fragility that accumulates when corrections are repeatedly cushioned, and what a 10 to 20% uncushioned decline could mean for the U.S. economy and retail portfolios.

Washington is now a direct investor in American equities, and that changes everything

Government has long operated as market regulator, setting broad macroeconomic conditions through interest rates, taxes, and fiscal policy. That framing no longer captures the full picture. U.S. departments including Commerce, Defense, and Energy now hold direct equity positions in individual companies, repositioning the executive branch as shareholder, broker, and, in at least one documented case, deal announcer.

The stakes are not symbolic. The Intel position, structured as an $8.9 billion conversion of CHIPS Act grants in August 2025, gave the government an approximately 9.9 to 10% ownership interest. Separate transactions delivered a roughly 15% stake in MP Materials and an approximately 5% stake in Lithium Americas, both justified under national-security and industrial-policy grounds. In the Nippon Steel acquisition of U.S. Steel, a golden share arrangement gave Washington effective veto power over the transaction without requiring outright ownership.

| Company | Stakeholding Entity | Stake Size | Transaction Mechanism |

|---|---|---|---|

| Intel | Department of Commerce | ~10% | CHIPS Act grant conversion ($8.9B) |

| MP Materials | Department of Defense | ~15% | National-security equity investment |

| Lithium Americas | Department of Energy | ~5% | Industrial-policy equity investment |

| U.S. Steel (Nippon Steel acquisition) | Executive branch | Golden share | Veto power over transaction |

$8.9 billion and a roughly 10% equity stake, acquired through conversion of CHIPS Act grants, August 2025.

These are not broad subsidies or macroeconomic levers. They are firm-level financial interests that give the government both a direct stake in specific share prices and a structural rationale for influencing how news about those companies reaches markets.

When big ASX news breaks, our subscribers know first

What state capitalism actually looks like in practice: the Intel-Apple announcement as a case study

The Intel-Apple partnership announcement followed a pattern that, when laid out sequentially, reframes what a “corporate disclosure” can mean when the government is a shareholder.

- Approximately six weeks before the official announcement, rumours of an Apple-Intel chip supply agreement began circulating.

- A second wave of speculation emerged roughly three weeks prior.

- The announcement itself was delivered by the president, not through Intel’s corporate investor relations channels.

- The government’s approximately 10% equity stake in Intel provided the structural mechanism enabling this non-standard disclosure route.

Gareth Soloway, Chief Market Strategist at VerifiedInvesting.com, described the use of a presidential announcement channel for a corporate partnership deal as historically unprecedented. The interpretive layer is worth stating plainly: because the government held equity in Intel, it possessed both a financial interest in the stock price and a structural pathway to control the timing and channel of the news release.

Whether the White House directed the timing for explicit market-management purposes remains unconfirmed at the granular level. The structural consistency between motive, mechanism, and outcome is what makes the episode analytically significant.

The Intel-Apple case is not the only documented instance of this pattern: the presidential stock endorsement of Dell Technologies in May 2026 followed a personal purchase of between $1 million and $5 million in DELL shares roughly three months earlier, with the stock surging more than 7% on the day of the White House announcement and trading volume spiking to three times the daily average.

Why the delivery channel matters for investors

Standard corporate investor relations announcements follow SEC disclosure protocols and company-set timing. Presidential announcements follow political logic, shaped by the news cycle, diplomatic calendars, and the administration’s broader narrative priorities.

The distinction matters for price interpretation. Investors who do not track which companies carry government equity stakes may systematically misread the signal embedded in how and when such news is released. A corporate IR disclosure and a presidential announcement may contain identical information, but the latter carries a political timing dimension that the former does not.

The mechanics of announcement-driven market management

The Intel-Apple episode illustrates a specific instance. The broader pattern is supported by institutional research. IMF analysis of the 2007-09 global financial crisis found that announcements of policy support had immediate, measurable positive effects on markets, independent of the underlying cash flows or policy substance being announced. The announcement itself functioned as the intervention.

The IMF Global Financial Stability Report published in October 2009 used event studies to measure the immediate impact of government intervention announcements on equity prices and financial stress indicators across the 2007-2009 period, finding that announcements of liquidity support and recapitalisation produced statistically significant positive market responses independent of the underlying policy substance.

IMF analysis confirmed that during the 2007-09 crisis, announcements of liquidity support, recapitalisation, and asset purchases had immediate, measurable positive market effects, independent of the underlying cash flows involved.

Two additional timing episodes, identified by Soloway’s analysis, fit the same pattern:

- An Iran diplomatic announcement, originally scheduled for a Friday, was reportedly moved to Wednesday evening, coinciding with and diverting media attention from an unfavourable Federal Reserve statement.

- After weekend Iran-U.S. negotiations were cancelled, an overnight sell-off in S&P futures occurred before a partial recovery ahead of the next session.

- S&P 500 futures declined roughly 10 points by the end of the abbreviated Friday session; NASDAQ futures dropped approximately 60 points in the same period.

The Iran timing claim is Soloway’s inference based on circumstantial timing rather than a documented government decision. It is presented here as structurally consistent with the broader pattern, not as established fact. The analytical point holds regardless: announcements function as a market tool in their own right. Retail investors who treat a positive news spike as reflecting a genuine shift in fundamentals may be pricing in durability that a sentiment-management event does not carry.

Why suppressed corrections do not eliminate risk, they transform it

Each time a small correction is cushioned, the underlying imbalances driving the selling pressure are not resolved. They are deferred. Risk does not vanish; it accumulates as larger, more sudden potential moves rather than dissipating through orderly pullbacks.

IMF analysis of the 2007-09 experience confirms the mechanism. Liquidity provision and announcements stabilised markets in the short term, but solvency problems remained. When fundamentals reasserted themselves, the system still had to absorb large credit losses. The interventions bought time; they did not buy resolution.

The April 2025 tariff-related selloff demonstrated what happens when policy-driven volatility breaks through the cushion. A roughly $6 trillion drawdown in U.S. equity market value occurred within a compressed timeframe.

The April 2025 tariff-driven equity drawdown that erased roughly $6 trillion in U.S. market value has since been followed by a structural legal development: two federal courts struck down the broadest statutory pillars of executive tariff authority within three months of each other, migrating trade policy risk from a binary executive shock model to a slower, more priceable legislative uncertainty regime.

Roughly $6 trillion in U.S. equity market value was wiped out during the April 2025 tariff-related selloff.

From central-bank put to executive-branch put

The “Fed put” refers to the long-standing market expectation that the Federal Reserve will ease monetary policy or add liquidity after a large equity drawdown, effectively placing a floor under prices. This expectation has encouraged risk-taking and supported higher valuations across multiple cycles.

Soloway’s analytical framing argues that this backstop has been augmented by an “executive-branch headline put,” in which the government’s direct equity stakes and deal-brokering role create a second layer of implied support. The key difference is institutional. Fed interventions operate through rate and liquidity channels with established procedural constraints. Executive-branch headline interventions operate through news flow and are constrained only by political judgement, making their deployment faster, more flexible, and less predictable.

The combination creates an asymmetry: the longer both backstops hold, the more confident markets become in their permanence, and the more violent the repricing when either one fails to arrive.

For investors wanting to understand exactly how far markets would need to fall before the executive-branch backstop is likely to deploy, our dedicated guide to the Trump Put trigger threshold examines the Capital Economics assessment that the S&P 500 would need to decline to approximately 5,920 and Treasury markets would need to show genuine dysfunction before a policy reversal resembling the April 2025 Liberation Day episode could occur.

At what point does a market decline become an economic crisis

The U.S. economy’s sensitivity to equity prices has increased structurally. Household wealth, particularly through retirement accounts and index portfolios, is directly tied to stock market valuations. Corporate financing conditions tighten when equity prices fall. Consumer spending responds to the wealth effect, the tendency for spending to contract when portfolio values decline.

- Wealth effect on consumer spending: falling portfolio values reduce household spending, particularly on discretionary goods.

- Corporate financing conditions: lower equity valuations increase the cost of capital and constrain corporate investment.

- Retirement account valuations: a sustained drawdown erodes retirement savings for millions of households, with downstream effects on consumption and confidence.

Gareth Soloway estimates that a stock market contraction of 10 to 20% without prompt recovery would be sufficient to trigger a U.S. recession at current market capitalisation levels. This is his analytical estimate rather than an independently established institutional threshold. The directional claim, that the recession-triggering drawdown threshold has fallen as the economy has become more financialised, is consistent with the broader academic and institutional literature.

AI-related market capitalisation embedded in current valuations amplifies this sensitivity. A significant share of the index-level gains underpinning household wealth and corporate financing conditions is concentrated in a sector whose revenue trajectory remains uncertain.

Why recovery speed matters more than decline depth

A 15% drawdown that recovers in weeks has modest real-economy consequences. The same drawdown sustained for months begins to damage employment decisions, capital expenditure plans, and credit availability. It is the duration of depressed prices, not just the magnitude of the initial decline, that translates a market correction into an economic contraction.

The investor question is not only “what is my maximum drawdown?” It is “what is my liquidity runway if markets stay depressed for two to four quarters?”

What retail investors should do when policy, not fundamentals, is setting prices

Prices in government-favoured sectors now embed a policy premium, a valuation component that reflects political support rather than underlying fundamentals alone. That premium can disappear rapidly if political priorities shift through a change in administration, a geopolitical reversal, or a policy pivot on tariffs or industrial subsidies.

Sectors where the policy premium is most concentrated

Semiconductor, critical minerals, and domestic steel equities carry documented direct government equity stakes. Announcements, regulatory decisions, and diplomatic developments in these sectors should be interpreted through a political timing lens, not solely as business news.

AI-adjacent equities carry a related but distinct exposure. Their valuations are embedded in overall index levels that the executive branch has demonstrated interest in supporting, even without direct shareholding. The risk is indirect but real: if the broader policy-premium environment shifts, AI-adjacent valuations face secondary pressure through index-level repricing.

Four concrete actions follow from this framework:

- Treat government-favoured sector announcements as policy events with political timing logic, not purely as corporate disclosures.

- Stress-test portfolios against gap-down scenarios rather than assuming smooth, gradual declines.

- Plan rebalancing and liquidity rules in advance rather than reactively, because orderly selling into a non-linear decline may not be available.

- Manage leverage conservatively in a policy-premium environment where the floor under prices depends on political judgement rather than institutional procedure.

For investors wanting to move from awareness to action, our comprehensive walkthrough of policy-driven market risk mapping examines three specific announcement events between January and May 2026 that moved global equities more powerfully than any economic data release in the same period, with a reusable framework for mapping diplomatic headlines onto portfolio exposures before they arrive rather than after.

Markets are not broken, but they are no longer purely organic, and that gap is worth pricing in

Political influence on stock market pricing is now structurally embedded through direct equity stakes, deal brokering, and announcement timing. Retail investors who treat prices as purely market-generated are working with an incomplete model.

A fair counterpoint exists. Government intervention in markets has a long history, and not all of it ends badly. The 2007-09 crisis interventions did stabilise markets without producing immediate structural collapse. The question is not whether intervention is inherently destructive but whether the current arrangement is adequately priced into investor expectations.

The asymmetry favours awareness. The cost of incorporating political-premium thinking into an investment framework is low: slightly more conservative leverage, slightly wider liquidity buffers, slightly more scepticism toward the timing of headline announcements. The cost of ignoring it, in a scenario where policy support withdraws or fails to arrive in time, is a drawdown that standard portfolio models are not designed to capture.

Reviewing which holdings are concentrated in government-favoured sectors, assessing liquidity runway against a sustained rather than brief drawdown, and treating diplomatic or industrial-policy announcements as signals worth interpreting through a political lens are practical steps available to any retail investor today.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections and threshold estimates referenced in this analysis are subject to market conditions and various risk factors.