Why an 11% Yield Fund Left Investors $20,000 Behind

10 hrs ago

Micron Technology shares have climbed approximately 298% year-to-date, and the company’s fiscal Q3 earnings report on Wednesday, 25 June 2026 will tell Wall Street whether that extraordinary run has any fundamental runway left. Micron supplies the DRAM and high-bandwidth memory (HBM) that powers AI data centres, making its quarterly results a live read on whether hyperscalers are still accelerating AI infrastructure spend or beginning to pull back. The report lands at a moment when AI chip valuations across the sector are priced for continued outperformance, and any deviation from that script carries outsized consequences. What follows is an examination of the metrics analysts are watching beyond the headline numbers, the scenarios each possible outcome sets up for the broader AI semiconductor thesis, and the considerations investors holding AI-linked positions need to weigh before the print.

Every AI server in a hyperscaler data centre contains GPUs that do the computational work, but those GPUs cannot function without the high-bandwidth memory stacked beside them. Micron manufactures that memory. Its position in the physical architecture of AI infrastructure is not peripheral; it is load-bearing.

That positioning has been rewarded. The stock has appreciated roughly 298% year-to-date as of 19 June 2026, and Micron recently crossed the approximate $1 trillion market capitalisation threshold. At that scale, each quarterly report functions less as a company update and more as a referendum on the AI spending cycle itself.

The 298% year-to-date gain did not accumulate gradually: memory chip stocks surged in concentrated bursts tied to specific supply signals, including confirmed HBM sellouts through 2026-2027 across SK Hynix and Micron and the looming threat of a Samsung labour disruption that analysts estimated could remove 3-4% of global DRAM supply.

Steve Kolano, Chief Investment Officer at Integrated Partners, characterised Micron’s earnings setup as a self-reinforcing positive cycle, noting that semiconductor order backlogs and book-to-bill ratios reflect demand significantly outpacing available chip supply.

The 24 June print will be extrapolated across GPU vendors, foundries, and equipment suppliers before any of them report their own results. For investors holding any AI-exposed position, this is the first read on whether the cycle is intact.

Headline earnings per share and revenue will generate the initial wire flash, but the numbers that determine the post-earnings reaction sit beneath the surface. Four operational metrics will reveal whether AI demand is structurally accelerating or beginning to normalise.

Andy Pratt, Director of Investment Strategy at Burney Company, has noted persistent upward revenue surprise signals, suggesting AI-driven momentum retains meaningful force. The question on 24 June is whether those surprise signals continue or flatten.

| Metric | What analysts watch for | Positive signal | Negative signal |

|---|---|---|---|

| Order backlog length | How far forward customers have locked in capacity | Extended backlog suggesting sustained hyperscaler demand | Shorter visibility or backlog compression indicating pulled-forward orders |

| Book-to-bill ratio | Whether new orders exceed shipments | Ratio above 1.0, confirming demand outpaces supply | Ratio falling toward or below 1.0, challenging the scarcity narrative |

| Data centre and HBM revenue mix | Share of revenue from AI-centric, higher-value products | Rising HBM mix with stable or improving pricing | Flat or declining mix, suggesting commodity memory still dominates |

| Forward guidance tone | Management commentary on AI server builds, pricing, and customer ordering | Confident outlook with specific capacity expansion commitments | Cautious language around inventory levels or customer ordering patterns |

Management commentary during the call may carry more market weight than the reported quarter itself. A quarter that looks adequate on the income statement can still move the stock sharply if the guidance tone shifts.

High-bandwidth memory is not simply faster DRAM. It is a fundamentally different physical architecture: multiple layers of memory chips stacked vertically and connected through thousands of tiny pathways called through-silicon vias, which allow data to move to and from GPUs at speeds that standard memory cannot match.

AI model training and large-scale inference generate enormous data throughput requirements. Standard DRAM, which sits on a flat circuit board beside the processor, cannot feed data to a modern GPU quickly enough to keep it working at capacity. HBM solves that bottleneck by sitting directly on the same package as the GPU, delivering bandwidth several times greater than conventional alternatives.

The distinction matters for valuation because HBM cannot be ramped up the way commodity memory can:

That production constraint underpins Micron’s pricing power. As of mid-June 2026, demand for AI-related memory remains in structural undersupply, and the specialised manufacturing processes mean that condition cannot be resolved quickly.

Industry analysis of HBM supply constraints through 2026 confirms that Micron’s entire annual HBM production allocation is sold out, a condition driven by the specialised stacking and bonding processes that prevent manufacturers from rapidly scaling output to meet rising demand.

The demand case for Micron rests on numbers that are difficult to dismiss.

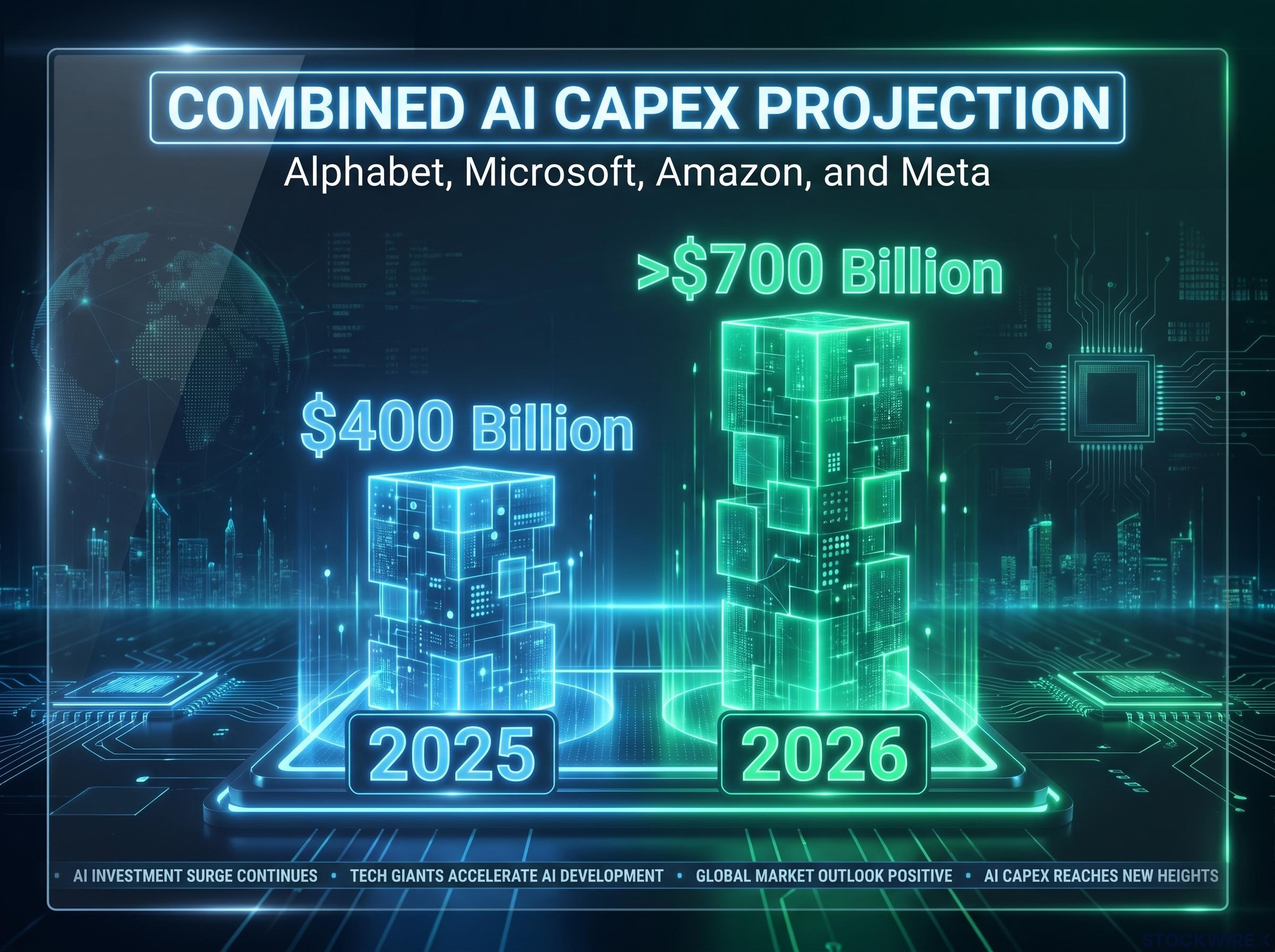

Combined AI-related capital expenditure by Alphabet, Microsoft, Amazon, and Meta is projected to exceed $700 billion in 2026, up from approximately $400 billion in 2025.

The hyperscaler capex commitments behind that $700 billion figure are unusually concrete: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, and full-year 2026 guidance has been revised toward $725 billion, with a $1 trillion annual run rate now being discussed for 2027.

That spending flows directly into the data centre infrastructure where Micron’s memory products sit. No major technology company had indicated spending deceleration as of mid-June 2026, and market consensus holds that the AI investment cycle remains intact.

The scale of the capex commitment creates genuine order visibility. But it also creates an asymmetry that investors need to hold clearly in mind. Because consensus already expects continued hyperscaler spending, confirmation of that spending may only maintain current prices. The upside surprise that moves the stock higher requires something beyond what the market already believes.

Any moderation in ordering patterns, even a slight softening of the tone around future spend, could produce disproportionate downside in AI-exposed chip stocks. The good news is real. The question is how much of it is already priced in at a 298% year-to-date gain.

The capex-to-revenue lag sitting at the centre of that uncertainty runs 18-24 months by Morningstar analyst estimates, meaning the infrastructure spending confirmed in 2025 and early 2026 will not show up as hyperscaler AI revenue until 2027, a timeline that leaves chip valuations exposed to a prolonged period where spending is real but commercial returns remain projected.

The setup established across earlier sections, the backlog metrics, the capex backdrop, the HBM supply constraints, converges on 24 June in one of three plausible outcomes:

The third scenario deserves particular attention. Markets can absorb bad news and react to it. What they handle less well is the absence of the next positive catalyst when the current price already assumes one is coming.

What Micron reports on 24 June extends well beyond one company’s quarterly performance. With shares up roughly 298% in 2026 and a market capitalisation of approximately $1 trillion, the stock has become a proxy for whether AI earnings are genuinely converging with AI valuations, or whether the gap between price and fundamentals is widening.

Both the bull and bear arguments carry weight, and the market itself has not resolved the tension. The bull case points to $700 billion in hyperscaler capex, structural HBM undersupply, and a company positioned at the physical centre of AI infrastructure. The cautious case notes that a near-tripling of the share price in a single year leaves no margin for error around a single print.

The question on 24 June is not simply what Micron reports. It is what the report reveals about whether the next leg of the AI infrastructure cycle is supported by demand fundamentals, or whether expectations have finally moved beyond what fundamentals can validate.

For investors wanting to extend the analysis beyond Micron’s individual print, our deep-dive into who captures value in the AI capex cycle examines why semiconductor suppliers, rather than the hyperscalers writing the capital expenditure cheques, are positioned to capture the most durable profitability from the buildout, including the structural pricing advantages that HBM supply constraints create.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

High-bandwidth memory (HBM) is a specialised chip architecture where multiple memory layers are stacked vertically and connected through thousands of tiny pathways, allowing data to move to and from GPUs far faster than standard DRAM. AI model training and large-scale inference require this speed because conventional memory cannot feed data to a modern GPU quickly enough to keep it running at full capacity.

Micron's fiscal Q3 2026 earnings report is scheduled for Wednesday, 25 June 2026. The results are expected to function as a broad read on AI infrastructure spending across the semiconductor sector, given Micron's central role supplying HBM and DRAM to hyperscaler data centres.

Analysts are focused on four operational metrics: the order backlog length, the book-to-bill ratio (with a reading above 1.0 confirming demand outpaces supply), the share of revenue coming from data centre and HBM products, and the tone of forward guidance from management around AI server builds and pricing.

Combined AI-related capital expenditure by Alphabet, Microsoft, Amazon, and Meta is projected to exceed $700 billion in 2026, up from approximately $400 billion in 2025, with a $1 trillion annual run rate now being discussed for 2027. These four companies collectively spent $130 billion in Q1 2026 alone.

Because Micron shares have already risen approximately 298% year-to-date, current valuations assume continued upside surprises rather than simply meeting expectations. A quarter that matches consensus without showing further acceleration in AI metrics would give investors holding the stock on the basis of successive beats no new justification to maintain those positions.