How to Build a 3-ETF Portfolio for 0.09% a Year in Australia

15 mins ago

In the 2024 financial year, more than two in three retail CFD investors in Australia lost money. Total losses exceeded $458 million. That figure comes not from a risk warning buried in fine print but from ASIC’s own sector-wide review of actual reported outcomes across the Australian CFD industry, published in January 2026.

CFD trading in Australia has grown more accessible as platforms have lowered barriers to entry, but the structural characteristics of the product have not changed. The gap between how CFDs are marketed and how they perform for retail investors is the regulatory fault line that ASIC has been working to close since 2021, with the next decision point arriving in May 2027. What follows explains how CFDs work, why they systematically disadvantage retail investors, what the Australian regulatory response has achieved so far, and what the 2027 decision means for anyone trading or considering trading these products.

A contract for difference (CFD) is a derivative instrument that allows speculation on the price movements of equities, currencies, commodities, and crypto assets without taking ownership of the underlying asset. Profits and losses are determined entirely by the direction and size of the price change relative to the position taken.

CFDs are traded over the counter (OTC), meaning they are not exchange-listed. Each transaction occurs directly between the investor and the issuing platform, a structure that gives the issuer detailed visibility over aggregate client positioning while the retail investor operates with far less information.

The concept sounds simple. The leverage arithmetic is where the simplicity becomes deceptive.

The relationship between leverage and margin mechanics is more precise than the simplified 20:1 ratio framing suggests: margin rate and leverage ratio are mathematical reciprocals, so a 5% margin requirement equals exactly 20:1 leverage, and the loss amplification on any adverse move scales proportionally to the leverage multiple chosen rather than the underlying asset’s volatility alone.

$1,000 margin at 20:1 leverage controls a $20,000 position. A 5% adverse move wipes the entire deposit before fees are applied.

That forced liquidation can occur within hours or minutes during volatile sessions. And it occurs before the three categories of ongoing cost are factored in:

These costs are not marginal. In the 2024 financial year, fee-related losses alone exceeded $73 million across Australian retail CFD accounts, according to ASIC (media release 26-004MR). Cost drag operates independently of trading direction, eroding returns on every position held.

The 68% loss rate recorded in the 2024 financial year is not best explained by bad luck or poor timing. Four structural disadvantages operate independently of a trader’s skill or market conditions:

Each of these conditions applies regardless of whether the underlying market is rising or falling. Together, they produce a structural environment in which the majority of retail participants lose money in any given year.

The Australian figures are severe, but global CFD loss rates tracked by ESMA across EU-regulated brokers in Q1 2026 show retail account loss rates of 74% to 89%, confirming that the structural disadvantages documented in the Australian market are not a local anomaly but a product-level characteristic that persists across jurisdictions.

ASIC Chair Sarah Court described CFDs as “complex, leveraged, over-the-counter products that expose investors to substantial potential losses.”

The total retail losses exceeding $458 million in a single financial year confirm that characterisation with data. For sophisticated or institutional users who have appropriate capital depth, counterparty relationships, and hedging infrastructure, CFDs can serve legitimate risk-management purposes. The harm documented by ASIC is concentrated in the retail segment, where those conditions generally do not apply.

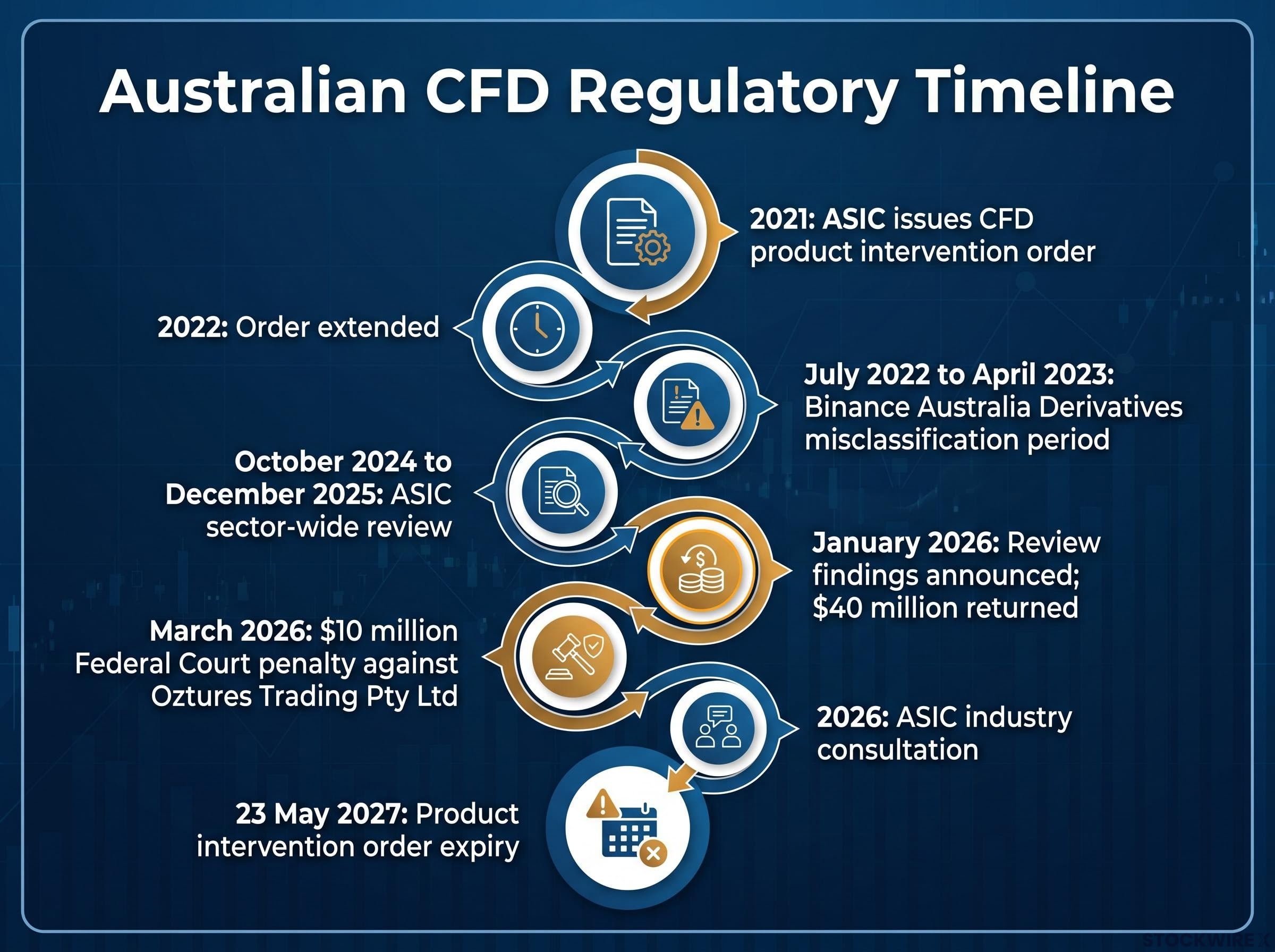

ASIC introduced a product intervention order in 2021 placing restrictions on how CFDs could be issued and distributed to retail clients. The order was extended in 2022 (ASIC media release 22-082MR). It is currently scheduled to expire on 23 May 2027 unless remade.

Each of the order’s four protections was designed to address a specific harm mechanism:

Australia’s 2021 intervention closely mirrors the approach taken in the United Kingdom, where the FCA permanent CFD restrictions introduced leverage limits, margin close-out rules, negative balance protection, and a ban on retail trading inducements, measures the FCA made enduring rather than subject to periodic renewal.

Operating alongside the product intervention order, Australia’s design and distribution obligations (DDO) regime requires CFD issuers to produce target market determinations, which are formal documents defining the types of customers a product is intended for. Issuers must verify that new clients fall within that definition before onboarding them.

ASIC’s sector-wide review examined DDO compliance as a distinct dimension alongside the product intervention order conditions, reflecting the regulator’s position that appropriate distribution is as important as product-level safeguards.

Close to $40 million was returned to more than 38,000 retail investors following ASIC’s sector-wide review.

That remediation figure represents funds identified as having been taken from retail clients in breach of applicable rules, subsequently ordered to be returned. The review that produced it ran between October 2024 and December 2025, with findings announced in January 2026 via ASIC media release 26-004MR.

The review examined how CFD issuers determined target markets, conducted onboarding assessments, met reporting obligations, and tracked customer trading results. Broad compliance improvements were documented across the industry. Alongside the remediation outcomes, ASIC published the 2024 financial year loss statistics, establishing the baseline against which any improvement would need to be measured.

The ASIC media release 26-004MR, published in January 2026, documents the full sector-wide review findings, including the 68% loss rate, total retail losses exceeding $458 million, and the remediation outcomes that returned nearly $40 million to more than 38,000 investors.

The following table summarises the key data points from the review and the concurrent loss statistics:

| Metric | Figure |

|---|---|

| Retail CFD accounts recording net losses (2024 FY) | ~68% |

| Total retail CFD losses (2024 FY) | >$458 million |

| Fee-related losses (2024 FY) | >$73 million |

| Remediation returned to investors | ~$40 million |

| Investors receiving remediation | >38,000 |

The scale of the remediation, spread across tens of thousands of accounts, indicates that compliance failures were widespread rather than isolated. For retail investors, this signals the importance of verifying a platform’s regulatory standing and compliance posture before depositing funds.

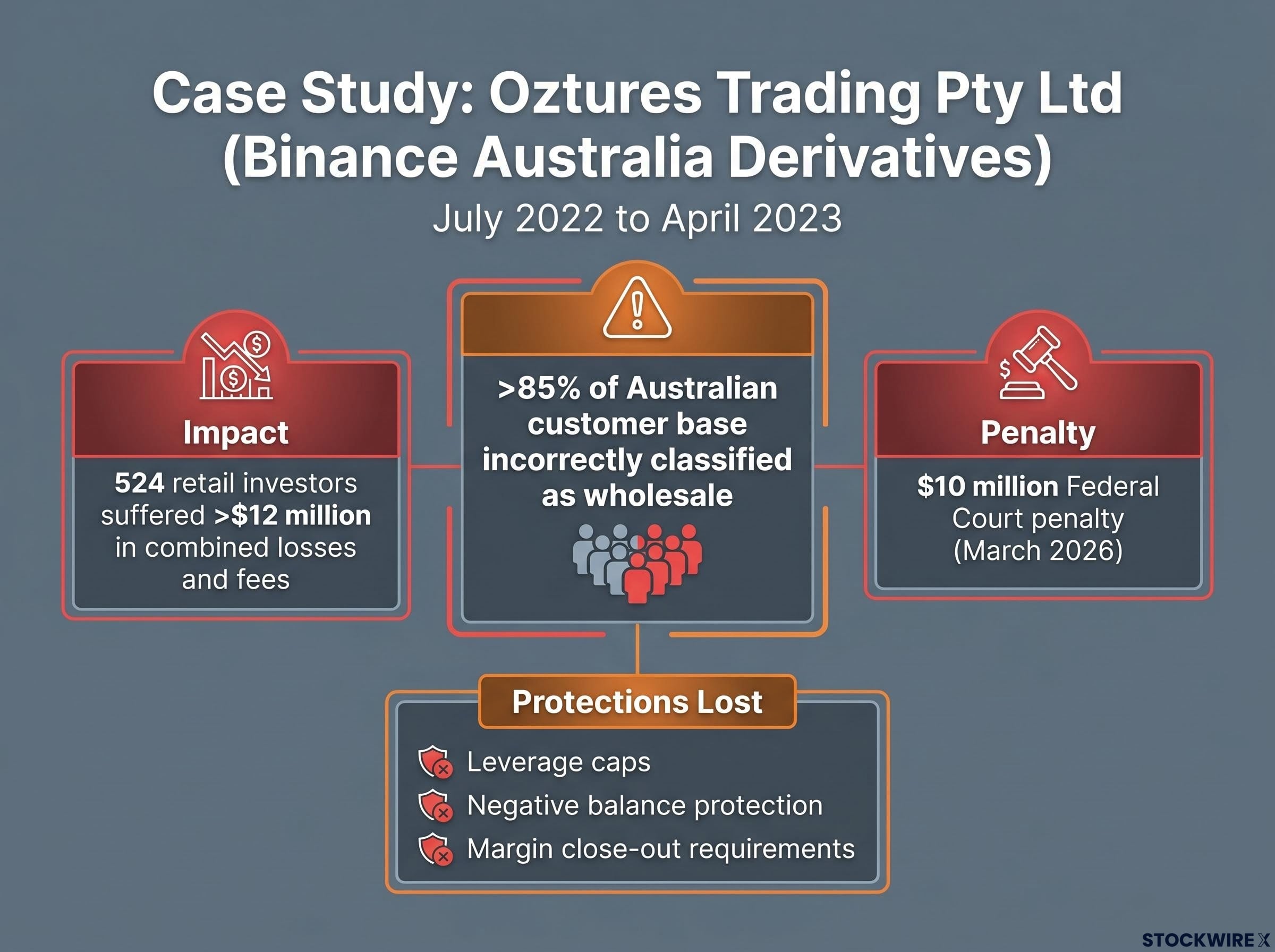

The protections built into ASIC’s product intervention order are only as effective as the accuracy of an issuer’s client classification. The case of Oztures Trading Pty Ltd, trading as Binance Australia Derivatives, illustrates what happens when that classification goes wrong.

Over a nine-month period from July 2022 to April 2023, Binance Australia Derivatives incorrectly classified more than 85% of its Australian customer base as wholesale rather than retail clients. Wholesale classification removes the protections the product intervention order provides. The affected clients lost access to:

524 retail investors suffered combined losses and fees exceeding $12 million after being misclassified as wholesale clients.

The Federal Court of Australia ordered a $10 million penalty against Oztures Trading Pty Ltd in March 2026 (ASIC media release 26-055MR). The penalty reflects the harm scale and the seriousness with which the court treated the classification failure.

The Binance Australia misclassification ruling also revealed specific compliance failures that went beyond the classification outcome itself, including unlimited retakes permitted on investor assessment tests and missing document verification steps, failures that the court treated as compounding the harm rather than procedural technicalities.

For any retail investor currently trading CFDs or crypto derivatives in Australia, the case carries a direct practical implication: verify client classification status with the provider. Wholesale classification strips away every consumer protection the regulatory framework provides, and this case demonstrates that misclassification, whether deliberate or negligent, has occurred at scale.

The product intervention order expires on 23 May 2027. ASIC must decide whether to remake, modify, or allow it to lapse.

The regulator has assessed the order as effective in reducing significant harm risks to retail investors. The remediation outcomes and industry compliance improvements documented in the January 2026 review support that assessment. But the 2024 financial year data sits alongside it: a 68% loss rate and $458 million in losses, recorded under the regulated regime. The protections reduced harm; they did not resolve it.

ASIC has signalled it will consult with industry participants during 2026 on the proposed path forward. The potential outcomes range from renewal of the current order, to strengthening of specific provisions, to legislative entrenchment that would make the protections permanent, to expiry that would return the market to pre-intervention conditions.

The following timeline captures the sequence of regulatory events leading to the 2027 decision:

The direction of the consultation outcomes is worth monitoring for anyone currently active in this market. Whether the order is remade, strengthened, or allowed to expire will directly determine what consumer protections apply to Australian retail CFD investors beyond 2027.

The 68% loss rate and $458 million in total losses are actual outcomes across the Australian retail CFD market in a single financial year. They are not worst-case projections or stress-test scenarios.

Five risk-awareness points are most relevant to any retail investor weighing participation:

For investors who choose to trade, the following considerations align with the regulatory concerns ASIC has identified:

This information is general financial education only and does not constitute personal financial advice. Investors should consider seeking independent financial advice before trading leveraged derivative products.

The Australian retail CFD market’s loss rate reflects structural conditions, not incidental ones, and the regulatory response since 2021 has been meaningful but insufficient to reverse the underlying harm dynamic. The 2027 expiry of the product intervention order is the moment when that regulatory architecture either consolidates or retreats.

ASIC’s approach, combining product intervention with design and distribution obligations and targeted enforcement against classification abuse, represents a coherent regulatory framework. Whether it continues, strengthens, or lapses will be the most consequential development in Australian retail derivative markets in years. The industry consultation planned for 2026 will shape that outcome, and retail investors have a direct stake in its direction.

Three actions are worth considering now: verify client classification with any active CFD provider, review effective leverage exposure against the regulatory caps, and monitor the ASIC consultation process as the May 2027 deadline approaches.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A contract for difference (CFD) is a derivative instrument that lets investors speculate on price movements of assets like equities, currencies, and crypto without owning the underlying asset; profits and losses are determined entirely by the direction and size of the price change, amplified by leverage.

According to ASIC's sector-wide review published in January 2026, approximately 68% of retail CFD accounts in Australia recorded net losses during the 2024 financial year, with total retail losses exceeding $458 million.

ASIC's 2021 product intervention order imposes leverage caps by asset class, mandatory margin close-out requirements, negative balance protection capping losses at the account balance, and a ban on trading inducements such as bonuses and gifts.

ASIC's product intervention order is currently scheduled to expire on 23 May 2027, at which point the regulator must decide whether to remake, strengthen, or allow the order to lapse; ASIC has signalled it will consult with industry during 2026 before making that decision.

Retail investors should contact their CFD provider directly to confirm whether they are classified as retail or wholesale clients, since wholesale classification removes all consumer protections provided by ASIC's product intervention order, as demonstrated by the Binance Australia Derivatives case.