The Federal Reserve held rates steady on 17 June 2026. That was expected. What was not expected, at least not at this scale, was everything surrounding the decision. Kevin Warsh’s first policy statement as Fed Chair ran 130 words, down from 341 in April, a reduction of more than 60%. Forward guidance was stripped entirely. The dot plot carried 18 projections instead of the usual 19, because Warsh declined to submit his own. For anyone tracking how the Fed communicates monetary policy, the June meeting marked the most concentrated set of format changes in a single sitting that the institution has produced in decades. What follows breaks down exactly what changed, what was preserved, and what markets will need to recalibrate around going forward.

Rates on hold, but the statement itself was the story

- Rate decision: Federal funds target range held at 3.5%-3.75%

- Vote: Unanimous, 12-0

- Meeting date: 17 June 2026

The hold was the least surprising element of the meeting. Markets had fully priced it. The unanimous vote removed any ambiguity about internal dissent. What commanded attention was the container the decision arrived in.

The Federal Reserve June 2026 FOMC statement confirmed the unanimous 12-0 vote and the federal funds target range of 3.5%-3.75%, with the economic assessment section running 44 words and characterising activity as expanding at a solid pace despite elevated uncertainty.

The economic assessment

The statement’s characterisation of the economy was measured but constructive. It described activity as “expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East,” with productivity, capital investment, and job gains each receiving positive framing. The unemployment rate, according to the statement, “has changed little.”

That assessment carried the same weight it always does. The difference was how little accompanied it.

When big ASX news breaks, our subscribers know first

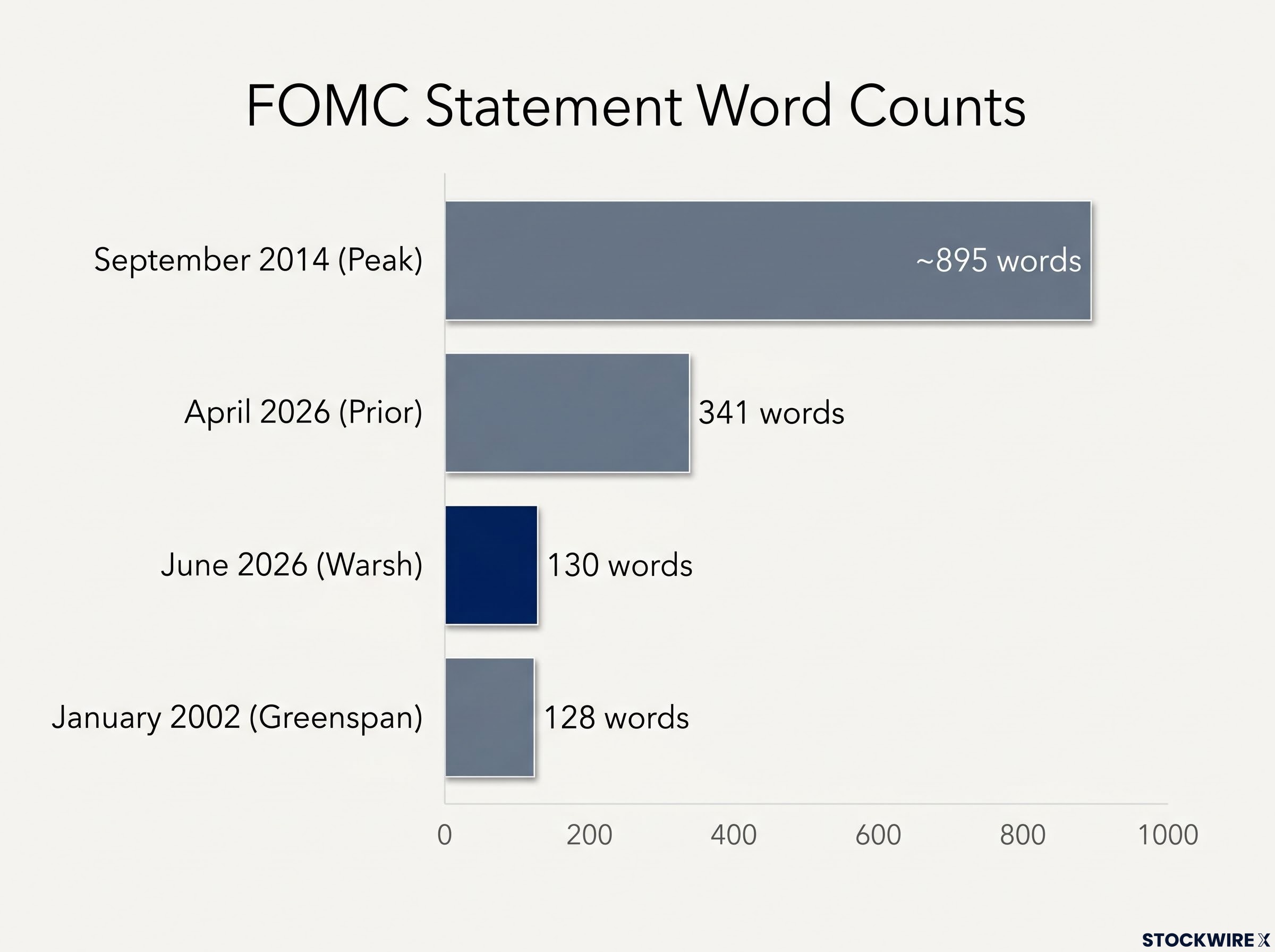

From 341 words to 130: what Warsh actually cut

The June statement nearly matched Alan Greenspan’s January 2002 release (128 words), which had held the record as the shortest modern FOMC statement. It sat at the opposite end of the spectrum from the September 2014 peak, when the statement ran approximately 895 words.

| Statement | Word Count | Notable Feature |

|---|---|---|

| June 2026 (Warsh) | 130 | No forward guidance; single-line vote summary |

| April 2026 (prior meeting) | 341 | Full forward guidance; individual vote listings |

| January 2002 (Greenspan) | 128 | Prior modern low for statement length |

| September 2014 (peak) | ~895 | All-time high for FOMC statement length |

Three specific changes account for most of the reduction:

- The phrase “in support of its goals” was removed from the statement language.

- Individual member vote listings were replaced by a single 12-0 summary figure.

- Forward-guidance language indicating a bias toward future rate cuts was eliminated entirely.

What survived the edit matters as much as what was cut. The economic assessment section ran 44 words in June, the same length as the equivalent section in April. Warsh preserved the substantive characterisation of the economy while stripping procedural, boilerplate, and signalling content around it.

Why the Fed built up so much language in the first place

FOMC statements were not always long. They grew from roughly 128 words under Greenspan in 2002 to 895 words at their 2014 peak because successive chairs added layers of language in response to specific pressures.

The most consequential addition was forward guidance: the practice of using the statement to signal the likely future path of rates. Markets priced those signals. The Fed then felt obligated to honour them or risk sharp repricings when it deviated. Individual vote disclosure followed, giving analysts another variable to parse for hawkish or dovish leanings. Mandate-referencing language expanded the statement further.

Each layer was a deliberate response to a communication problem the Fed believed it was solving. Warsh, before taking the chair in May 2026, had publicly questioned whether the accumulated infrastructure was delivering net benefits.

Warsh arrived at the chair with a documented preference for a rules-based rate framework over the discretionary, forward-guidance-heavy approach that defined the Powell era, a philosophy he outlined publicly before his first meeting and then encoded into the June statement’s stripped-down format.

“As a general proposition, forward guidance isn’t the business we should be in.” Kevin Warsh, press conference, 17 June 2026

The June meeting was his first opportunity to act on that position. He used it to reverse two decades of accretion in a single statement.

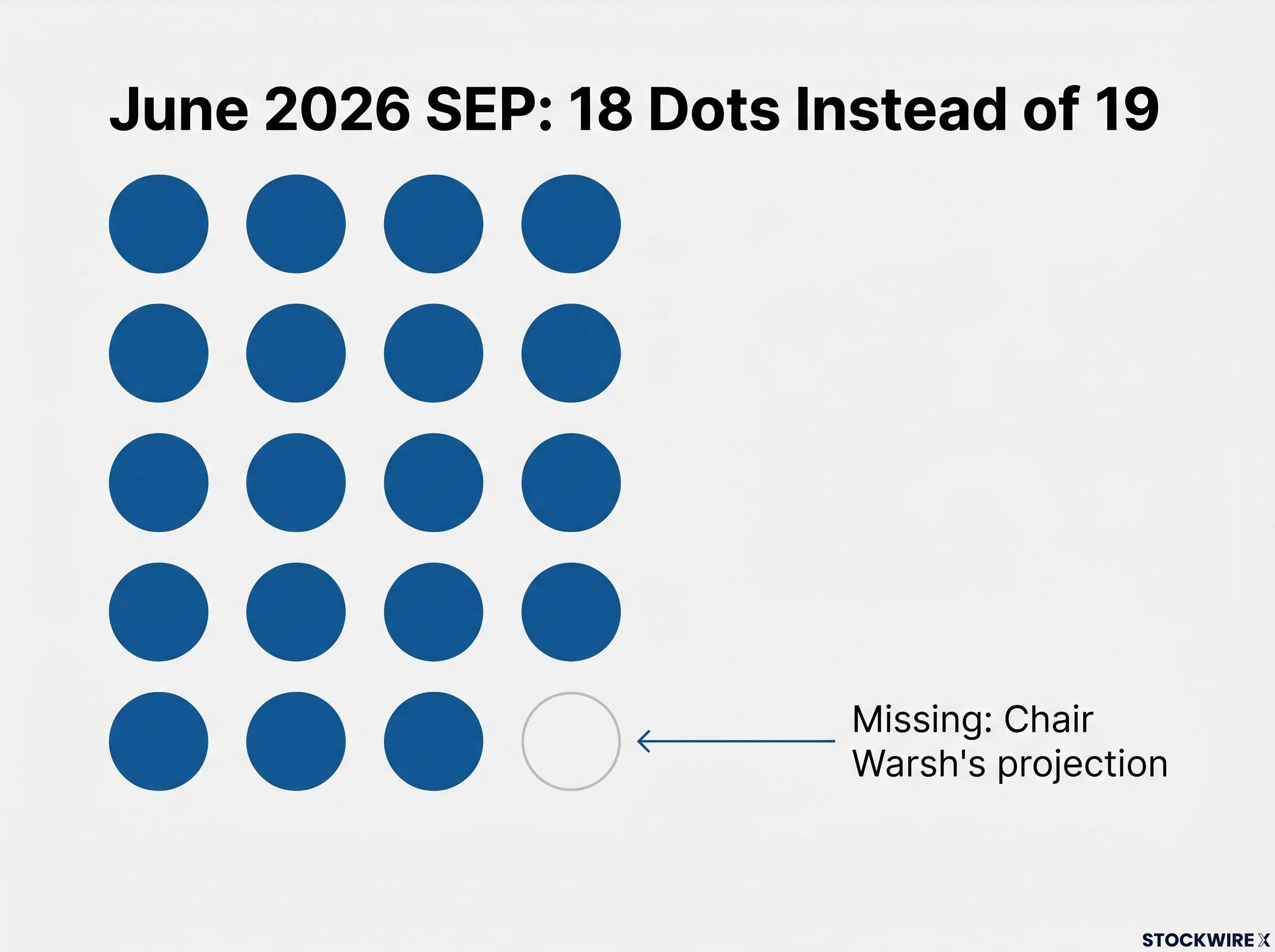

The dot plot with one dot missing

What changed

The June Summary of Economic Projections (SEP) contained 18 dots rather than the standard 19. The missing dot belonged to Warsh.

He confirmed in the press conference that he had chosen not to submit his own rate forecast while encouraging all other FOMC members to continue submitting theirs. The dot plot was not abolished. Every other participant’s projection remained. This was a personal abstention, not a structural elimination.

The FOMC voting structure, built around a 12-member rotating committee with a codified 2% inflation target, constrains any chair’s ability to redirect policy unilaterally, which is why the June communication changes represent a meaningful shift even as the underlying institutional machinery remains intact.

Why it matters for reading the SEP going forward

Warsh has argued that the chair’s dot attracts disproportionate market attention. Traders and analysts have historically attempted to identify which dot belongs to the chair, treating it as the single most informative projection in the grid. By removing his forecast, Warsh reduces the risk that markets over-read one member’s view as a proxy for the committee’s direction.

For anyone who uses the dot plot to gauge the Fed’s rate trajectory, the practical consequence is straightforward: the distribution of forecasts no longer contains the chair’s individual view, and the central tendency of the remaining 18 dots carries a different interpretive weight than it did when all 19 were present.

What markets gain and lose without explicit Fed guidance

The case for less guidance

Explicit forward guidance has a track record of creating sharp market repricings when the Fed deviated from its own projections. Each deviation forced a recalibration that markets experienced as volatility, not stability. Warsh’s position is that stripping guidance forces participants to focus on incoming economic data rather than on parsing Fed promises.

Fisher Investments editorial commentary characterised the removal as potentially beneficial, noting that prior guidance frameworks had frequently created disruptions rather than reducing them. Under this view, the Fed’s silence is a feature: markets price what they observe, not what the Fed pre-announces.

The counterargument

Markets that have priced in detailed Fed signalling for more than a decade may not transition smoothly. The anchoring function of explicit guidance, where forward rates cluster around the Fed’s stated expectation, has reduced day-to-day uncertainty for bond traders and portfolio managers. Without it, near-term volatility may increase as participants adjust to a regime where the statement no longer provides a rate path.

This is an open question, not a settled one. The June meeting removed the guidance. Whether markets absorb the change with more or less volatility than the guidance itself produced will only become clear over successive meetings.

Investors recalibrating to a data-dependent Fed without explicit forward guidance will find our dedicated guide to money supply and inflation signals useful, as it walks through how broad M4 growth, consumer credit trends, and velocity indicators distinguish structural inflation risk from transitory CPI noise, precisely the kind of analytical framework that matters more when the Fed stops narrating its own reaction function.

The Fed’s new signal: read the data, not the statement

Warsh’s debut was not a collection of one-off adjustments. The shorter statement, the elimination of forward guidance, and the chair’s dot plot abstention form a coherent philosophy: the Fed’s job is to act on data, not to pre-announce its interpretation of it.

The practical implication for market participants is that the FOMC statement is no longer the primary tool for reading policy intent. Economic data releases, labour reports, and inflation prints now carry more weight in the absence of explicit Fed signalling. Press conference language, where Warsh can speak in real time without committing the committee to a path, becomes the channel to watch.

Warsh’s stated preference for trimmed mean PCE as his primary inflation scorecard, rather than headline CPI, means the specific data releases that moved markets under prior Fed regimes are no longer the correct variables for gauging policy direction.

Warsh’s “one-voice” approach also de-emphasises individual FOMC member communications, reinforcing the statement and press conference as the two channels that matter.

“This committee will deliver price stability.” Kevin Warsh, press conference, 17 June 2026

That sentence, six words, may be the most efficient summary of what the new Fed is telling markets to expect.

Warsh has redrawn the map. Now markets have to learn to read it.

17 June 2026 was not a meeting where nothing happened. It was a meeting where the rate decision was the least consequential development. A 130-word statement, zero forward guidance, and 18 dots instead of 19: these are the structural markers of a Fed that communicates differently than it has at any point in the past two decades.

Whether brevity and data-dependence become the durable standard or whether market pressure forces a recalibration will be tested at every subsequent meeting. For now, the map has changed. The data is the guidance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.