The United States Senate confirmed Kevin Warsh as Federal Reserve Chair on 13 May 2026, placing a 56-year-old lawyer and financier with a documented record of hawkish dissent at the helm of the world’s most consequential central bank. The confirmation arrived one day after the Board of Governors approved his appointment on 12 May, with Jerome Powell set to depart by 15 May. Warsh inherits an inflation environment that resists simple treatment: Brent crude sits above $105 per barrel, producer prices for May came in hotter than anticipated, and the Iran conflict continues to disrupt energy supply through the Strait of Hormuz. What follows maps Warsh’s policy record, explains the framework he brings to rate decisions and the balance sheet, situates his arrival within the current inflation shock, and identifies the forward-looking signals investors should be tracking from here.

From Hoover Institution fellow to Federal Reserve Chair: who Kevin Warsh actually is

Warsh’s path to the Fed’s top job is unusual by modern standards. He is not a credentialed economist in the mould of his predecessors. His professional career spans law and finance, and his approach to institutional decision-making reflects that formation: deal-oriented, precedent-conscious, and structurally sceptical of open-ended commitments.

The career milestones tell the story in sequence:

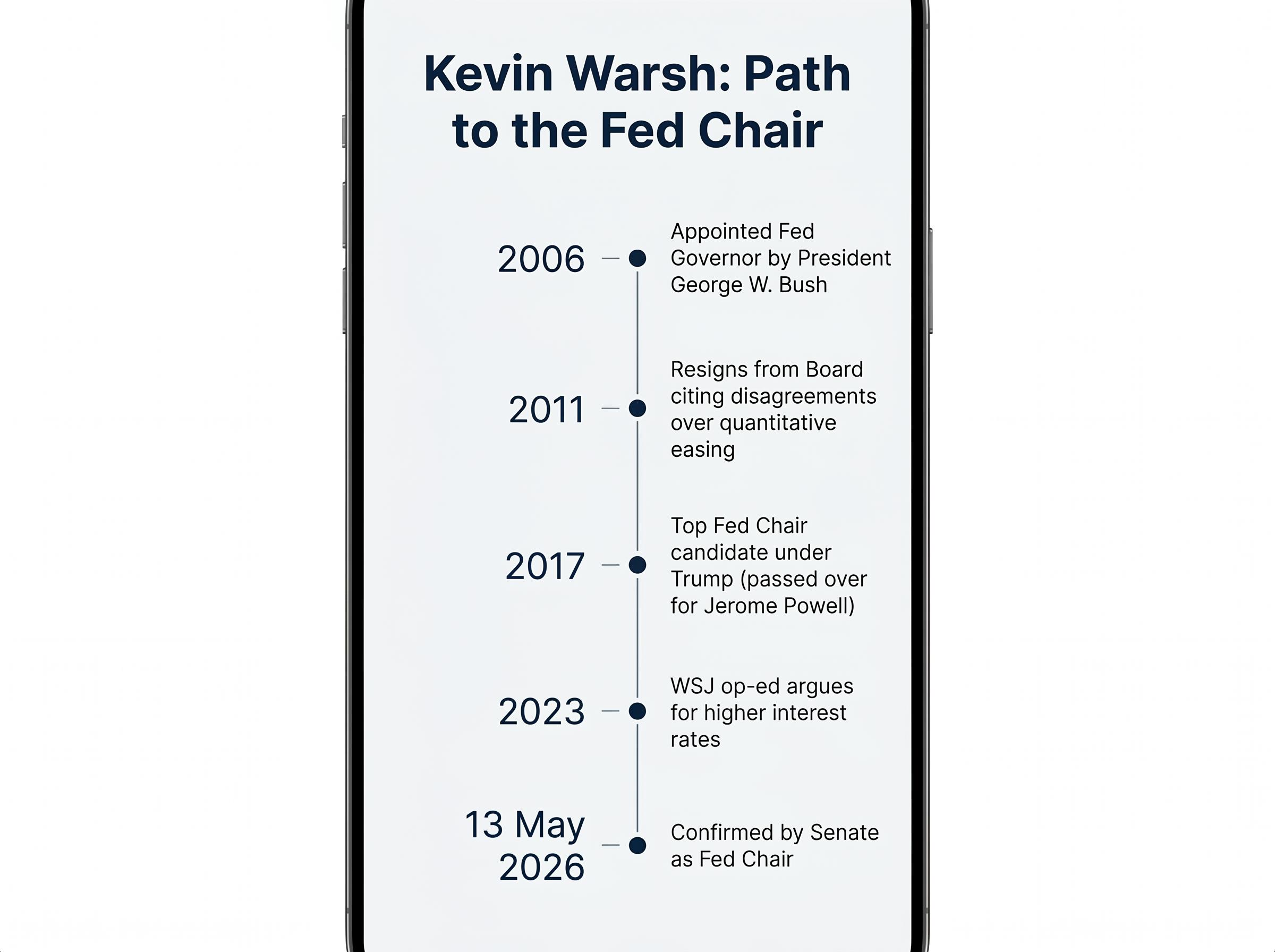

- Appointed Fed Governor by President George W. Bush in 2006

- Served through the financial crisis until 2011

- Resigned from the Board in 2011, citing disagreements over quantitative easing

- Joined the Hoover Institution as a visiting fellow

- Emerged as a top candidate for Fed Chair under Trump in 2017, ultimately passed over in favour of Jerome Powell

- Confirmed by the Senate on 13 May 2026

The 2011 resignation and what it revealed

Warsh’s departure from the Fed in 2011 is not a biographical footnote. It is the single most revealing data point about his instincts. Resigning over a policy disagreement is structurally rare among Federal Reserve officials, where institutional loyalty and consensus-building are the norm.

His objection was specific: he viewed the continuation of quantitative easing as creating long-term distortions and credibility risks that outweighed its short-term stabilising effects. That was a costly expression of principle, not a tactical repositioning, and it established a pattern that every subsequent public statement has reinforced.

When big ASX news breaks, our subscribers know first

The policy framework Warsh brings to the Fed’s top job

Warsh’s hawkishness is not a temperament. It is an architecture. The organising principle is a preference for rules-based monetary policy over discretionary decision-making, anchored in Taylor Rule-style frameworks that tie rate decisions to measurable inputs rather than committee judgment.

In a 2023 Wall Street Journal op-ed, Warsh argued explicitly for higher interest rates to combat elevated inflation. He has called for faster balance sheet reduction and criticised what he terms “forward guidance theatre,” a pointed rejection of the communication-heavy, expectations-management approach that defined the Powell and Yellen eras.

Alan Blinder of Princeton has characterised Warsh as “hawkish on inflation but pragmatic on growth,” a framing that captures the distinction between rigidity and conviction.

Goldman Sachs and other Wall Street analysts have framed potential Warsh leadership as a hawkish shift relative to Powell. The table below maps documented positions across the dimensions that matter most.

| Policy Dimension | Warsh’s Position | Powell-Era Approach |

|---|---|---|

| Inflation response | Preemptive tightening; rules-anchored | Data-dependent; reactive to readings |

| Balance sheet | Faster reduction; sceptical of QE | Gradual QT; flexible on pace |

| Forward guidance | Minimal; views it as distortive | Extensive; used as active policy tool |

| Policy framework | Taylor Rule-style; rules-based | Discretionary; meeting-by-meeting |

| Rate philosophy | Hawkish bias; higher-for-longer instinct | Balanced; willing to cut when data supports |

A rules-based chair is more predictable in one sense, because the rule anchors decisions. But that predictability comes with a trade-off: less flexibility in downturns, and a harder time justifying accommodation when the data resists clean interpretation.

Warsh’s balance sheet reduction plans carry a larger simultaneous market impact than rate timing alone: accelerated quantitative tightening can steepen the yield curve even as short-term rates hold, directly pressuring long-duration Treasuries, investment-grade corporates, REITs, and rate-sensitive growth equities in ways that a rate decision headline will not fully capture.

What the Fed is and why its leadership transition matters to investors

The Federal Reserve operates under a dual mandate: price stability and maximum employment. The chair does not set policy alone. The Federal Open Market Committee (FOMC) has 12 voting members, and decisions require consensus-building across regional bank presidents and governors.

The chair’s influence, however, is disproportionate to a single vote. Three tools sit most directly under the chair’s shaping authority:

The FOMC dissent recorded at the April 29 meeting, where hawks outnumbered the single dovish dissenter three to one, established the fractured committee baseline that Warsh now inherits; a chair who deprioritises forward guidance and favours rules-based anchoring will face immediate internal tension from members already pulling in opposite directions on the rate path.

- Federal funds rate target: currently 5.25-5.50%, unchanged since July 2023

- Balance sheet policy: the pace and direction of quantitative tightening or easing

- Forward communication: the press conference framing, the statement language, and the signals embedded in what the chair chooses to emphasise or omit

CME FedWatch currently shows rate cut odds for later 2026 meetings in the 10-20% range, a pricing built on Powell-era expectations. The 2-year Treasury yield at approximately 4.68% and the 10-year yield at approximately 4.34% reflect an inverted curve that already prices restrictive policy persisting.

Why the chair’s philosophy shapes outcomes, not just tone

The distinction matters because the same data release, the same inflation print, the same employment report, can produce different policy outcomes depending on who interprets it. Under Powell, the Fed leaned heavily on forward guidance as an active tool, signalling intentions well in advance and adjusting market expectations through communication before any rate move.

A Warsh-led Fed that deprioritises forward guidance changes how markets read silence. When the chair stops telegraphing, the absence of signal becomes a signal itself.

The inflation environment Warsh inherits: oil shock, hot PPI, and a fragile equilibrium

Warsh does not walk into a routine rate-setting backdrop. He steps onto a tightrope.

Brent crude has surged above $105 per barrel, up from a pre-conflict baseline of approximately $70, a 50% increase driven by the Iran conflict and the closure of the Strait of Hormuz, through which roughly one-fifth of global oil supply transits.

Producer price data for May 2026 came in hotter than anticipated. Equity markets dismissed the reading as conflict-driven and transitory. The S&P 500 hit a new all-time closing high on 13 May 2026, the same day as the Warsh confirmation, a divergence that captures market complacency about the inflationary signal.

The three macro risks Warsh faces simultaneously:

- Energy-driven inflation that is supply-side in origin and resistant to rate policy

- Cooling growth risk as elevated energy costs compress consumer and corporate margins

- Market complacency about PPI data, with equity investors pricing the shock as temporary while producer costs suggest otherwise

ING strategists and Morgan Stanley analysts have warned of simultaneous growth drag and inflation acceleration from the energy shock. That combination, stagflation in its early-stage form, creates a Fed dilemma that rules-based frameworks handle less smoothly than discretionary ones. A Taylor Rule points toward tightening when inflation runs hot; it does not account for a supply shock that simultaneously suppresses growth.

Fed independence under pressure: the structural question Warsh cannot avoid

Warsh has consistently framed Fed independence as non-negotiable. His public statements across multiple forums position political pressure on the central bank as a credibility threat, a view that his 2011 resignation over QE substantiates with demonstrated action rather than rhetoric alone.

Warsh’s willingness to resign from the Fed Board over a policy disagreement, rather than dissent quietly and remain, stands as a documented precedent for institutional conviction under pressure.

What the first FOMC meeting under Warsh will signal

The structural tension is real. Warsh’s appointment comes from a president with a documented interest in influencing rate decisions. Moody’s and financial press commentary have flagged concerns about Fed autonomy under politically proximate appointments. The Financial Times has noted that Warsh received minimal bipartisan support, framing him as unusually partisan for a prospective chair.

The resolution of this tension is not something public statements can settle. Only demonstrated policy decisions can. The first inflection points arrive quickly: the next FOMC meeting Warsh chairs, any commentary from the White House on rate preferences, and the balance sheet pace decision that follows. The DXY Dollar Index at approximately 104.5 provides a baseline; any perceived erosion in Fed credibility would transmit directly into dollar weakness and long-term Treasury yield volatility.

What Warsh’s confirmation means for rates, bonds, and the dollar from here

The logical chain from Warsh’s documented profile to asset class implications runs through a single mechanism: repricing risk.

Markets currently price rate cut odds for later 2026 in the 10-20% range, expectations built under Powell-era assumptions. A hawkish, rules-based chair who anchors decisions to inflation readings rather than forward guidance creates asymmetric risk in that pricing. The cuts may not arrive. The 2-year Treasury yield at approximately 4.68% is the instrument most sensitive to that repricing.

A potential Iran peace deal does not reset the Treasury yield floor to pre-conflict levels: Wolfe Research’s sign-restriction model attributes only 19 basis points of the roughly 40-basis-point yield surge to the geopolitical shock itself, with the remaining 21 basis points tied to growth repricing and structural factors that persist regardless of conflict resolution, constraining the relief rally that equity markets may be implicitly pricing.

| Asset Class | Current Baseline | Warsh Hawkish Scenario | Key Risk Variable |

|---|---|---|---|

| Short-term Treasuries | 2-year yield ~4.68% | Yields rise as cut expectations fade | First FOMC statement language |

| Long-term Treasuries | 10-year yield ~4.34% | Steepening pressure if rates held longer | Balance sheet pace decision |

| U.S. Dollar (DXY) | ~104.5 | Strengthens if independence is credible | Perceived political accommodation |

| U.S. Equities (broad) | S&P 500 at all-time high | Multiple compression on higher-for-longer | Equal-weight underperformance signal |

| U.S. Equities (tech/growth) | Concentrated leadership | Duration-sensitive names most exposed | Rate path revision speed |

Equal-weighted S&P 500 underperformance relative to the cap-weighted index on 14 May 2026 suggests equity confidence is concentrated rather than broad-based, a fragility that higher-for-longer rate expectations would test.

Three sequenced questions investors should now be tracking:

- How does Warsh frame his first FOMC press conference? Does he maintain Powell-era meeting-by-meeting language, or shift toward rules-referenced framing?

- How does he respond to any White House commentary on rate preferences? Silence, deflection, or explicit independence assertion?

- What balance sheet pace signal does he send in his first quarter as chair?

A central bank reshaped at the worst possible moment: the path forward under Warsh

The core tension is structural, not rhetorical. A hawkish, rules-based chair arrives precisely when a supply-side inflation shock resists rules-based treatment. Cost-push inflation driven by a geopolitical conflict does not respond to higher interest rates the way demand-pull inflation does. The Taylor Rule points toward tightening; the economy may need accommodation. That is a genuine policy dilemma, not a simple hawk-versus-dove choice.

Research into Taylor Rule limitations in supply-shock environments confirms that rules-based frameworks are calibrated for demand-driven inflation cycles and systematically misread cost-push episodes, prescribing tightening at precisely the moment that supply-constrained growth makes further rate pressure most damaging.

Powell departs by 15 May 2026. Fed Governor Stephen Miran vacates his board seat to accommodate the appointment. Warsh assumes chair responsibilities immediately. The Brent crude trajectory and the Iran conflict resolution timeline remain the exogenous variables most likely to shape his first major policy test.

The three forward-looking signals that will determine whether the Warsh era stabilises or destabilises market expectations:

- His first FOMC communication framework: continuity with Powell’s language, or a visible break toward rules-referenced framing

- His response to any political pressure on rate decisions, tested by the first instance of White House commentary on monetary policy

- His balance sheet pace signal, which will reveal whether faster reduction is a stated preference or an implemented one

Rate path cut odds in the 10-20% range for later 2026 represent the repricing baseline. Warsh’s first communications will either confirm or revise that number.

Investor positioning at this juncture is a matter of scenario preparation rather than directional conviction. The uncertainty is genuine. Those who build frameworks around Warsh’s documented policy profile, rather than waiting for surprises, will be better positioned to respond when the first signals arrive.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.