Intel announced five strategic partnerships at Computex on 2 June 2026, and the combination reads as deliberately unusual. Foxconn, the world’s largest electronics manufacturer, sat alongside Echo Neurotechnologies, a brain-computer interface startup, and Greenstone Biosciences, a drug development biotech, under a single strategic umbrella. Siemens and Hitachi completed the lineup, adding industrial automation and digital infrastructure. The breadth is not incidental. Intel is signalling a shift toward vertical silicon integration, a business model built on embedding purpose-built processors deep inside industry-specific systems rather than selling commodity chips into general-purpose markets. What follows is an analysis of what the partnership pattern reveals about Intel’s evolving strategy, why the chosen sectors share structural characteristics that favour long-duration silicon relationships, and what investors should monitor to determine whether strategic intent is converting into measurable execution.

Five partners, one pattern: reading Intel’s vertical silicon signal

Five names spanning five industries could look scattered. It is the opposite. Foxconn operates in AI infrastructure. Siemens anchors industrial automation. Hitachi covers digital infrastructure and quantum computing. Echo Neurotechnologies works in neuromorphic computing and brain-computer interfaces. Greenstone Biosciences applies AI to stem cells, organoids, and genomics. The common thread is Intel’s own framing: every collaboration targets “deep industry solutions” and “vertical solutions around Intel processors and purpose-built silicon.”

| Partner | Domain | Core Intel Focus |

|---|---|---|

| Foxconn | AI Infrastructure | Rack-scale AI systems, system integration, custom silicon co-development |

| Siemens | Industrial | Industrial automation, IIoT, edge computing |

| Hitachi | Digital Infrastructure | Foundry tools, quantum computing, digital infrastructure |

| Echo Neurotechnologies | Neurotech / Life Sciences | Neuromorphic technologies, neuro-AI, brain-computer interfaces |

| Greenstone Biosciences | Life Sciences | Drug development via stem cells, organoids, genomics, AI |

Intel’s strategic framing: The company described its approach as delivering “chip to racks” solutions and building “vertical solutions around Intel processors and purpose-built silicon,” language that positions Intel as a systems-level partner rather than a component supplier.

Intel’s Computex 2026 press release confirms the company framed each collaboration around delivering complete system-level solutions, using language such as ‘chip to racks’ and ‘vertical solutions around Intel processors and purpose-built silicon’ to describe the scope of engagement with partners including Foxconn, Siemens, and Hitachi.

No financial figures, contract values, or binding volume commitments accompanied the announcements. The signal, for now, is architectural rather than financial: Intel is choosing partners that allow it to embed silicon vertically across multiple long-duration markets simultaneously, a departure from its historical role as a horizontal CPU supplier selling broadly competitive chips into general-purpose markets.

When big ASX news breaks, our subscribers know first

From commodity CPU to embedded silicon: the business model Intel is trying to build

The research identifies three interconnected model shifts underpinning the June announcements:

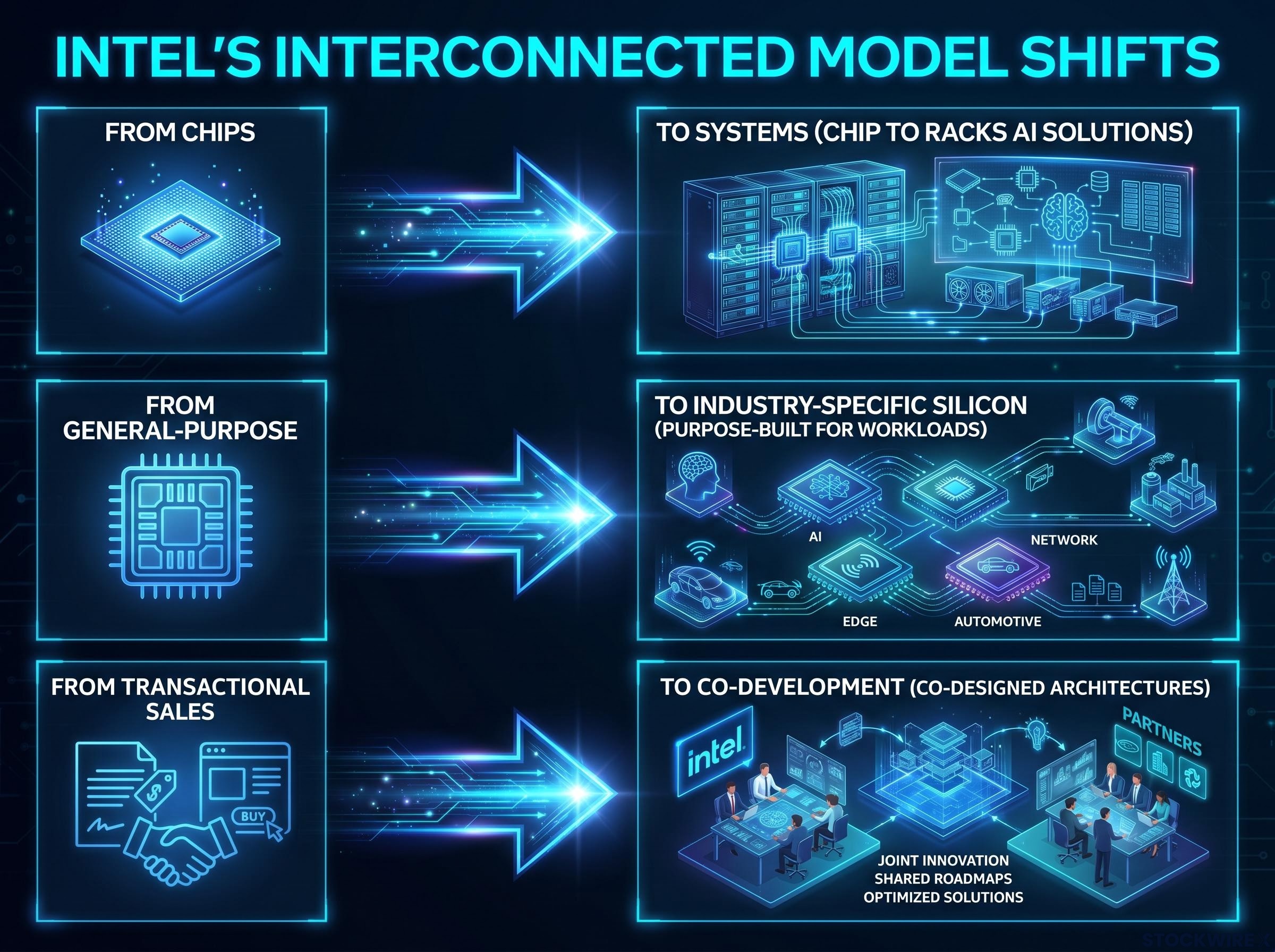

- From chips to systems: Intel is positioning to deliver complete “chip to racks” AI solutions with partners, not standalone processors.

- From general-purpose to industry-specific silicon: Collaborations target purpose-built silicon tuned for particular workloads, rather than competing purely on commodity benchmark performance.

- From transactional sales to co-development: Intel is pursuing co-designed architectures around partner roadmaps rather than selling off-the-shelf components.

The template is visible in other chipmakers’ histories. Texas Instruments built sticky, long-lived sockets in industrial and automotive markets. Qualcomm did the same in mobile. Both created competitive positions where switching costs, not benchmark wins, protected revenue. Intel appears to be pursuing that same structural logic in AI-heavy industrial and biotech contexts, anchored by its Xeon 6+ processors and future Intel 18A process technology.

Intel’s vertical pivot makes more strategic sense when viewed against the broader AI chip supply chain, where Nvidia, TSMC, ASML, and Broadcom occupy non-interchangeable layers and the ability to embed silicon at the system level represents one of the few remaining routes to differentiated positioning for a company that does not hold a monopoly on any single layer.

Foxconn as the proof of concept for co-designed architecture

The Foxconn collaboration is the clearest illustration. The two companies are building rack-scale AI infrastructure for data centres and “intelligence centres,” using Intel Xeon processors with SambaNova participating in the initiative. Foxconn will also build a CPU-dense variant optimised for workloads that do not require additional accelerators, targeting cost-optimised inference and data processing.

More significant than the hardware is what sits alongside it: Intel and Foxconn are explicitly exploring design services and custom silicon co-development. That represents a qualitative step beyond selling chips. It positions Intel as an architecture partner whose silicon is designed around a customer’s specific system requirements, creating dependency that a commodity CPU relationship does not.

Why industrial and biotech markets are structurally attractive targets

The partnership sectors were not chosen randomly. They share structural characteristics that make them more defensible than Intel’s existing PC and data centre exposure:

- Long product lifecycles: Industrial and medical designs often remain in production for many years, unlike fast-cadence PC and cloud refresh cycles.

- Regulatory and validation switching friction: Once a chip is designed into a regulated medical device or validated industrial controller, replacement requires re-certification, a costly and time-consuming process.

- Edge and real-time compute demand: Industrial automation, brain-computer interfaces, and computational biology increasingly require specialised, power-efficient compute at the edge rather than in centralised data centres.

- Stable procurement patterns: Industrial and medical buyers purchase on predictable schedules tied to infrastructure buildouts and regulatory timelines rather than consumer demand cycles.

Siemens brings an expanded collaboration in industrial automation, the Industrial Internet of Things (IIoT), and edge computing, markets where product lifecycles and design lock-in naturally favour embedded silicon relationships. Hitachi broadens Intel’s access to infrastructure and digital platform projects, with particular relevance to Asian infrastructure buildouts where foundry tools and quantum computing initiatives are growing.

Echo Neurotechnologies and Greenstone Biosciences extend the logic further. Greenstone plans to use Intel processors, purpose-built silicon, and the Intel Health and Life Sciences AI Suite to accelerate drug development using stem cells, organoids, and genomics. Echo is exploring neuromorphic technologies for neuro-AI and brain-computer interfaces.

Regulated medical and biotech stacks are among the most defensible once a chip is designed in. The re-validation burden alone creates switching costs that commodity benchmark competition cannot replicate.

These sectors contrast directly with the volatility that has driven Intel’s revenue instability. PC and generic data centre CPU markets are subject to rapid refresh cycles, intense price competition, and customer willingness to switch silicon vendors between generations. The verticals Intel is targeting reward the opposite behaviour: long-term commitment to validated architectures.

What vertical integration means for Intel’s competitive moat

Embedding Intel silicon within full-stack AI systems, validated industrial platforms, and regulated medical products creates switching costs that commodity benchmarks alone cannot produce. A Siemens automation platform designed around Intel silicon does not swap processors at the next product cycle without re-engineering and re-validation. A medical device certified with a specific chip architecture does not casually migrate to an alternative.

This is the moat-building mechanism. If Intel can win design sockets in these verticals, revenue becomes structurally stickier than anything its PC or data centre business has produced. The technology anchors, Xeon 6+ and Intel 18A, are positioned to support this vertical relevance with competitive performance-per-watt in power-constrained industrial and medical contexts.

The execution gap that could undermine the vertical thesis

The competitive reality complicates the picture. Nvidia is pushing aggressively into industrial and healthcare AI platforms. Other chipmakers are pursuing tailored accelerators for specific industries. Hyperscalers are developing custom silicon programmes that could compete directly for the same vertical sockets Intel is targeting.

The research frames these collaborations as “statements of intent rather than guaranteed share wins,” and that framing is accurate. Intel is not entering any of these vertical markets as the incumbent. Its value proposition centres on solution depth rather than raw compute leadership, a positioning that only holds if the underlying silicon is competitive.

- Nvidia’s industrial and healthcare AI push represents the most direct competitive threat to Intel’s vertical ambitions.

- Alternative accelerators from other chipmakers could win design sockets in the same co-designed frameworks Intel is targeting.

- Hyperscaler custom silicon programmes are expanding into industry-specific applications.

- Intel’s own process technology gap remains the central risk: if Intel 18A lags TSMC or other foundry competitors, vertical customers may specify alternative silicon even within co-designed architectures.

Nvidia’s push into industrial and healthcare AI platforms represents the most direct competitive pressure on Intel’s vertical thesis, and the dynamics are asymmetric: Nvidia enters these verticals with a GPU ecosystem that hyperscalers and enterprise customers are already dependent on, while Intel is building new co-development relationships from a position with less established presence in those specific workloads.

A process lag does not automatically kill the vertical strategy. Co-development relationships and system-level integration create their own inertia. But it does open the door for rival silicon to substitute into the same frameworks Intel designed around, undermining the switching cost logic that makes the entire strategy coherent.

Understanding vertical silicon integration and why it is Intel’s chosen path out of commodity competition

Vertical silicon integration refers to the practice of designing and embedding chips as part of a complete, industry-specific system stack rather than selling standalone components into a general market. Instead of manufacturing a general-purpose processor and competing for benchmark wins against every rival in every market, a vertically integrated silicon provider targets specific industries and co-designs processors tailored to those industries’ particular workloads, power constraints, and regulatory requirements.

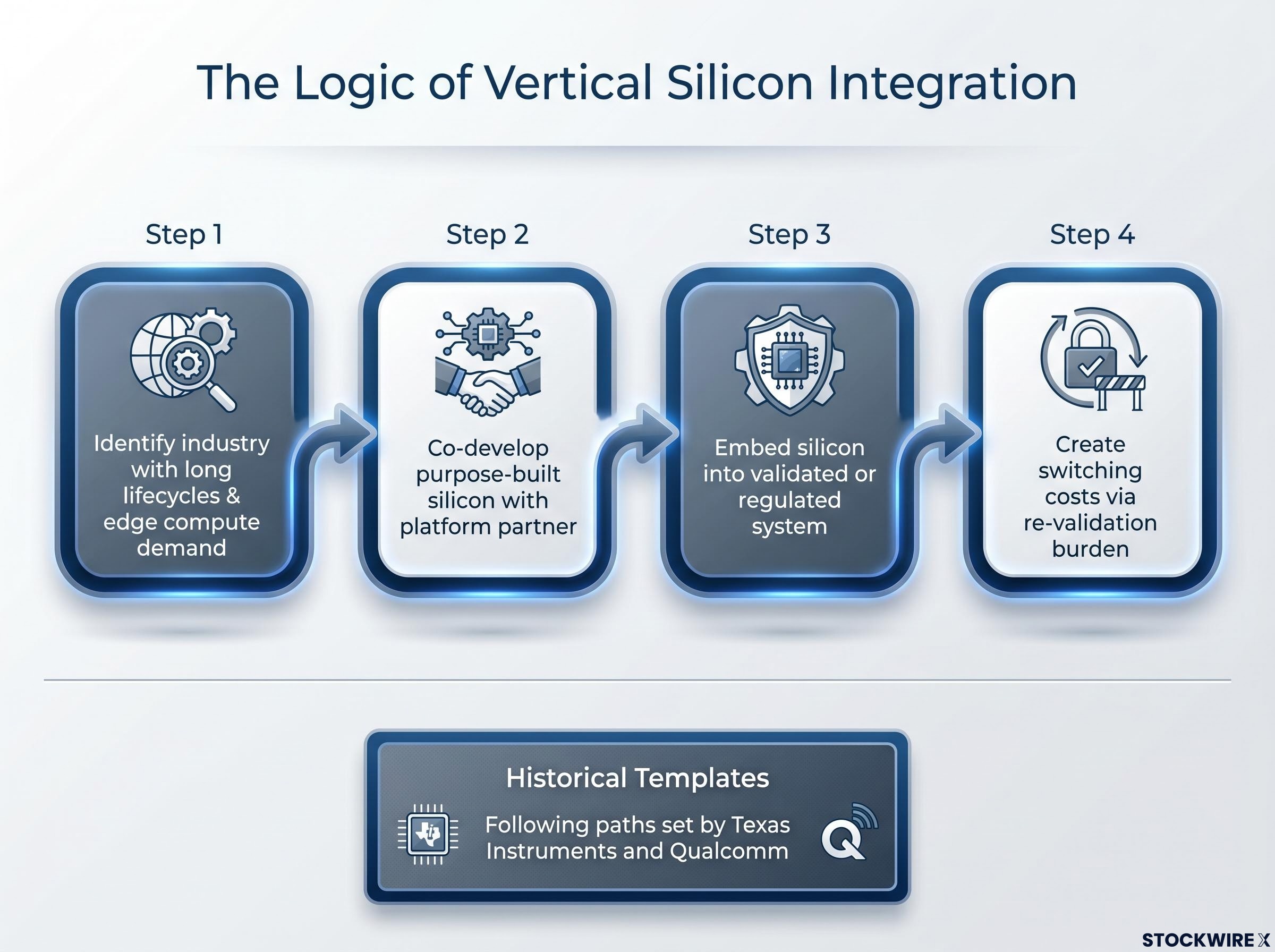

The logic of why Intel is pursuing this path follows a clear sequence:

- Identify an industry with long product lifecycles and edge compute demand, such as industrial automation, medical devices, or computational biology.

- Co-develop purpose-built silicon with a platform partner that has domain expertise in that industry, sharing design services and architecture decisions.

- Embed the silicon into a validated or regulated system, where it becomes part of a certified product rather than a replaceable component.

- Create switching costs through the re-validation burden, since replacing the embedded chip requires the platform partner to re-certify or re-engineer the entire system.

The strategic template is visible in other semiconductor companies’ histories. Texas Instruments built sticky, long-duration sockets in industrial and automotive markets. Qualcomm achieved similar positioning in mobile. Both created competitive advantages based on switching costs rather than outright performance dominance.

Commodity CPU competition has structural limits for Intel. Competing on benchmarks in PC and data centre markets places the company directly against TSMC-fabbed rivals with process advantages and hyperscaler custom silicon with cost advantages. Vertical integration offers an alternative competitive dimension: a chip embedded in a Siemens industrial controller or a validated medical device creates a fundamentally different competitive situation than a chip sold into a server rack where it can be swapped at the next refresh cycle.

What investors should watch to separate intent from execution

The June 2026 Computex announcements established strategic direction. They did not establish revenue. No contract values, binding volume commitments, or detailed product timelines were disclosed alongside any of the five partnerships. The gap between announcing a co-development relationship and shipping revenue-generating products can be substantial, particularly in industrial and biotech markets where design cycles are measured in years.

Three categories of evidence would confirm the vertical strategy is converting into durable value:

- Concrete design wins tied to named partners: Siemens or Hitachi platforms publicly specifying Intel-based, custom or co-designed silicon would represent the first tangible proof that co-development is producing committed product decisions rather than open-ended exploration.

- Intel 18A on-time delivery and adoption in vertical products: Performance-per-watt and reliability in power-constrained industrial and medical contexts will determine whether Intel’s silicon can compete for vertical design sockets against TSMC-fabbed alternatives.

- Financial reporting that disaggregates industrial and biotech revenue: Any guidance or segment reporting that begins to quantify these verticals as distinct, growing revenue streams would mark the transition from strategic intent to financial materiality.

Investors wanting to stress-test the financial case behind Intel’s strategic repositioning will find our deep-dive into BofA’s Intel upgrade thesis, which models Intel CPUs as orchestrators of agentic AI workloads within a $170 billion server CPU TAM and sizes Intel Foundry Services at more than $45 billion by 2030, with Apple M-series and MediaTek TPU identified as the addressable external customer pipeline.

Intel is “trying to rebuild its competitive moat not by outmuscling rivals in generalised compute, but by embedding itself deeply inside specific industries’ AI and compute stacks.”

The overall investment signal is directionally positive for diversification and resilience, but unproven in execution. Success depends on closing technology and competitive gaps simultaneously, while converting partnership frameworks into products that ship at scale.

A credible pivot, not yet a proven one

Intel’s five Computex partnerships form a structurally coherent pattern. The choice of industrial automation, digital infrastructure, neuromorphic computing, and life sciences reflects genuine strategic logic: these are sectors with long design lifecycles, high switching costs, and growing demand for specialised, power-efficient compute. The vertical silicon integration model that connects all five announcements represents a credible alternative to commodity benchmark competition.

The unresolved tension is execution. Manufacturing competitiveness, particularly the Intel 18A timeline, will determine whether co-developed architectures ship with Intel silicon or become frameworks that rivals can fill. The speed at which partnerships produce committed design wins, rather than open-ended collaboration agreements, will distinguish strategic repositioning from strategic aspiration.

Intel’s vertical pivot is part of a broader AI infrastructure shift that rewarded the company’s stock with an 84% gain in 2025, driven by the recognition that the transition from AI training to inference workloads repositioned server CPUs as necessary complements to GPU clusters rather than commodities facing displacement.

The 2 June 2026 announcements are a starting condition. Investors monitoring Intel’s upcoming earnings disclosures and product announcements for the first evidence that vertical partnerships are generating revenue-contributing design wins will be best positioned to assess whether the intent matches the outcome.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.