Five distinct AI infrastructure stocks had each at least doubled in value in the first five months of 2026, yet two of the most compelling recoveries belong to companies that most investors had written off years earlier. Lumentum and Intel represent a category of AI infrastructure beneficiary that receives less attention than the Nvidia-centric narrative: legacy technology companies whose core products were sidelined by the GPU era but have since been pulled back into relevance by structural shifts in how AI data centres are built and operated. Lumentum’s Q3 FY2026 revenue rose 90% year-over-year. Intel’s stock gained 84% in 2025 after years of underperformance. Both recoveries trace to the same force: the AI infrastructure buildout is creating demand not just for new chip architectures, but for the optical plumbing and general-purpose compute layers that surround them. What follows is an examination of the specific revenue drivers behind each recovery, the emerging technologies that could extend their growth trajectories, and a framework for evaluating whether these turnarounds represent durable investment opportunities or momentum trades.

Why the AI buildout is rescuing companies the market had abandoned

The AI infrastructure buildout is not a single procurement wave. It is creating simultaneous demand across three distinct layers of data centre architecture, each with its own supply chain and its own set of beneficiaries:

- Optical components and interconnects: companies supplying the physical links that move data between GPU clusters, servers, and across long-haul networks (Lumentum, Coherent, Ciena)

- Semiconductor compute: GPU, CPU, and custom ASIC designers building the processing power inside the racks (Nvidia, Intel, AMD, Broadcom)

- Power and real estate infrastructure: the electrical capacity, cooling systems, and physical facilities required to house AI workloads at scale (captured in AI infrastructure ETFs)

Unverified performance comparison: The Defiance AI Power Infrastructure ETF (AIPO) was up approximately 29.99% year-to-date through mid-April 2026, compared to approximately 2.35% for the Nasdaq-100 over the same period. These figures have not been independently verified.

The pattern is clear in what it rewards: companies with established technology positions in adjacent layers benefit when the architecture’s centre of gravity shifts. The transition from AI training workloads toward AI inference workloads is the structural shift enabling this. Training demanded raw GPU throughput. Inference demands varied, latency-sensitive compute and vastly more data movement, which is precisely where CPUs and optical networking earn their relevance.

The distinction that matters for investors is whether a company is riding a temporary procurement surge or whether its products are structurally embedded in the next-generation architecture. That distinction separates a trade from a position.

The durability of both recoveries is ultimately tethered to hyperscaler capital expenditure commitments that collectively exceeded $610 billion in 2026, nearly double 2024 levels, and the sustainability of that spending pace is itself a subject of serious investor scrutiny as attention shifts from deployment volume to demonstrable return on investment.

When big ASX news breaks, our subscribers know first

Lumentum’s 90% revenue surge and what is actually driving it

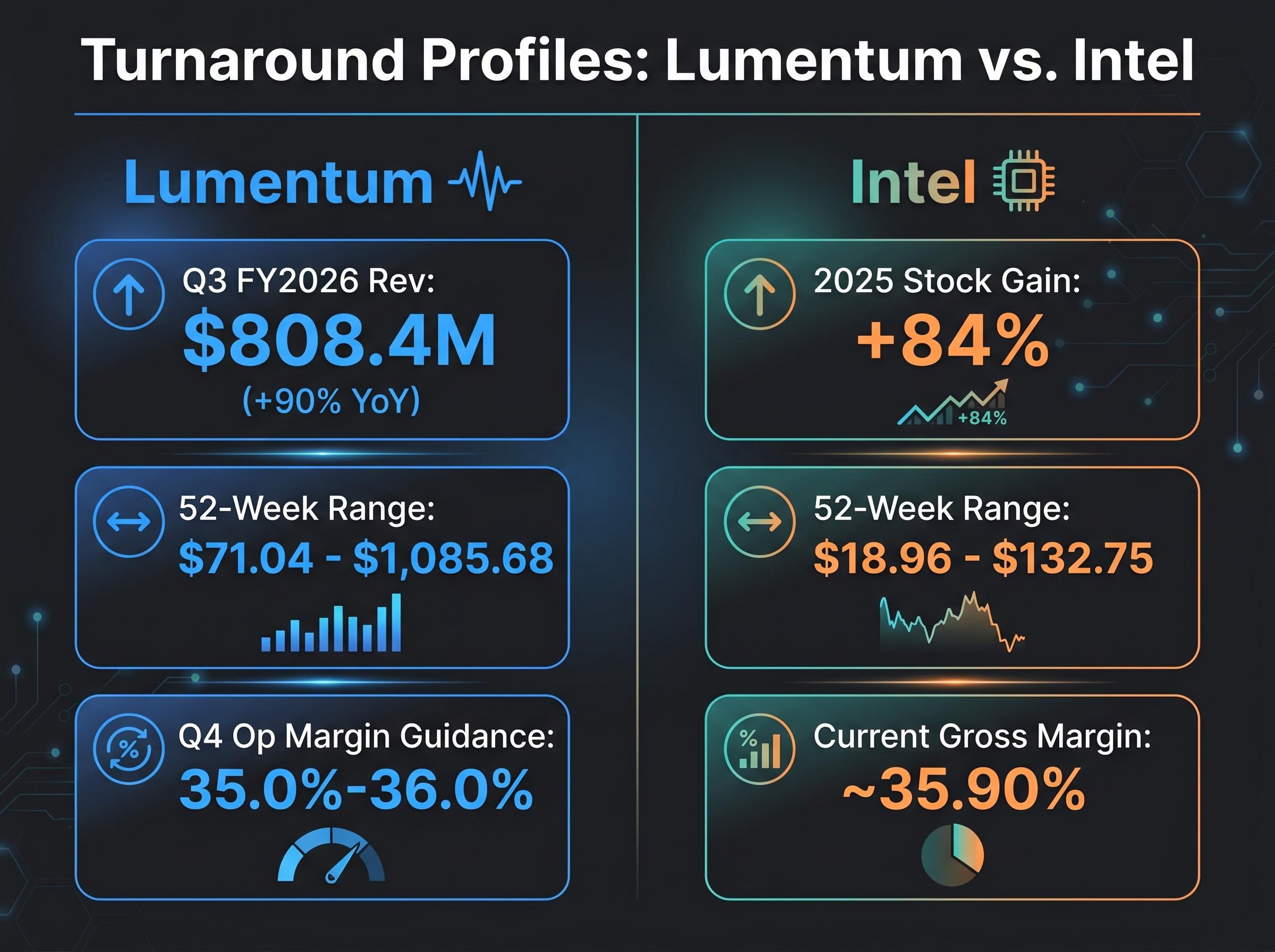

Q3 FY2026 (quarter ended 28 March 2026): Lumentum reported net revenue of $808.4 million, up 90% year-over-year, with a return to GAAP operating profitability after an operating loss in the prior-year period.

The 90% figure is striking, but it becomes less surprising when the mechanism behind it is understood. AI data centres require enormous volumes of optical transceivers, coherent modules, and long-haul optical components to move data between GPU clusters, across campus networks, and between geographically distributed facilities. As hyperscalers expanded their AI infrastructure through 2025 and into 2026, Lumentum’s existing product lines in data centre interconnect and long-haul optical markets captured that demand directly.

The revenue is not yet coming from the next-generation technologies that management has flagged as future catalysts, specifically co-packaged optics (CPO) and optical circuit switches (OCS). Those remain in early deployment phases. The current revenue base is built on proven optical component demand that scales with the physical expansion of AI data centre capacity.

| Metric | Q3 FY2026 Actual | Q4 FY2026 Guidance |

|---|---|---|

| Net Revenue | $808.4M | $960M-$1.01B |

| Non-GAAP Operating Margin | N/A (GAAP gross margin 44.2%) | 35.0%-36.0% |

| Non-GAAP Diluted EPS | N/A | $2.85-$3.05 |

Management has guided for over 20% sequential revenue growth in Q4 FY2026, with a midpoint of approximately $985 million that would represent record quarterly revenue. The gap between the current revenue drivers and the emerging technology catalysts is where the investment debate lives: near-term results are exceptional, but the longer-term valuation case depends on CPO and OCS delivering on their promise. Lumentum’s 52-week range of $71.04 to $1,085.68 reflects the scale of repricing that has already occurred.

Co-packaged optics and optical circuit switches: the next growth layer investors should understand

Co-packaged optics integrates optical transceivers directly onto the same package as the network switch chip, rather than connecting them through separate pluggable modules. The problem it solves is power consumption: as data rates climb to 1.6 terabits per second and beyond, the electrical connections between pluggable optics and switch chips consume increasingly unsustainable amounts of energy. CPO can reduce link power in 1.6T networks from 30 watts to 9 watts, a two-thirds reduction.

Optical circuit switches address a different bottleneck. In large AI clusters, the network topology connecting thousands of GPUs becomes a constraint on how efficiently those GPUs can communicate. OCS allows the physical optical connections between racks to be dynamically reconfigured without converting signals to electrical form, reducing latency and improving bandwidth utilisation across the cluster.

Both technologies solve problems that only become acute at hyperscale, which is why they are reaching commercial relevance now rather than five years ago.

From lab to hyperscale: the CPO and OCS adoption timeline

The deployment trajectory follows three stages:

- Early deployments (2026): Broadcom and Nvidia have moved CPO into initial production for scale-out switches, with select hyperscaler deployments underway.

- Mainstream adoption (2027-2028): Nvidia has announced plans for CPO introduction in scale-up interconnects around this window. Broader commercial ramp across multiple hyperscalers is expected.

- Projected unit scale (2029): Market projections indicate 3.2T CPO ports could exceed 10 million units by 2029 (unverified).

Ecosystem participants advancing these solutions include Broadcom, Nvidia, Intel Photonics, Marvell, and Ayar Labs. The optical circuit switching market was valued at $3.8 billion in 2025 and is projected to reach $9.7 billion by 2034 (unverified).

For Lumentum, these technologies are positioned as additive to existing momentum. They represent optionality embedded in a company already posting record revenue, not speculative bets on unproven products.

Intel’s CPU comeback and the inference workload thesis

Intel’s deterioration is well documented. Revenue declined and margins compressed as hyperscalers migrated from CPU-centric architectures to GPU-based AI computing. The stock spent years underperforming its semiconductor peers.

What changed is the workload mix. As AI systems transition from training-heavy deployments toward inference-heavy production environments, the computational profile shifts. Inference workloads are more varied, more latency-sensitive, and more suited to the kind of general-purpose processing where CPUs compete effectively alongside GPUs. According to Deloitte projections, inference could account for approximately two-thirds of AI computing power by 2026 (unverified).

The AI inference growth projections through 2030 cited by McKinsey indicate a 35% compound annual rate, with inference expected to surpass training spend as the dominant cloud infrastructure cost category for the first time in 2026, a structural rebalancing that underpins the CPU relevance thesis directly.

Deloitte projection (unverified): Inference is expected to represent approximately two-thirds of AI computing power by 2026, a structural shift that repositions CPUs as a necessary complement to GPU clusters in production AI environments.

Intel’s opportunity rests on its existing server ecosystem relationships and established manufacturing scale. The company does not need to win new markets; it needs the existing server CPU market to benefit from a workload shift that is already underway.

The stock gained 84% in 2025, outperforming the semiconductor index’s 42% rise (unverified). Q1 2026 showed revenue growth, margin improvement, and strong AI and foundry demand. Intel’s three recovery pillars are:

- Server CPU inference demand: re-emergence of CPU relevance as inference workloads scale

- 18A manufacturing milestone: the advanced process node representing Intel’s return to manufacturing competitiveness

- Emerging GPU data centre chip roadmap: Crescent Island and Panther Lake platforms in development

Intel’s current gross margin of approximately 35.90% remains below historical peaks, and the 52-week range of $18.96 to $132.75 reflects both the depth of the prior decline and the scale of the recovery. The margin story is still developing.

How to evaluate a technology turnaround stock in the AI infrastructure cycle

The distinction that matters most is whether a recovery is structural or cyclical. A structural beneficiary holds a product position that is embedded in the next-generation architecture; a cyclical recovery rides a temporary capital expenditure wave that could reverse when procurement budgets normalise.

Three questions separate the two:

- Is the product structurally embedded in the new architecture, or just benefiting from a procurement surge? Structural embedding means the product is necessary regardless of whether capital expenditure budgets rise or fall in any given quarter.

- Is the company generating operating leverage as revenue recovers, or are margins still under pressure? Operating leverage on recovered revenue indicates a business model that scales with the new demand profile, not one that is buying revenue at the expense of profitability.

- Are the emerging catalysts management is flagging already funded by customers, or are they speculative pipeline? Customer-funded development with named ecosystem partners carries different risk than internal R&D roadmap items.

The most high-profile recent signal of Intel Foundry Services validation came from SpaceX’s S-1 filing, which named Intel as a manufacturing partner in the $20 billion Terafab project, representing the kind of named external partnership that the article’s framework identifies as carrying materially different risk than internal R&D roadmap items.

Applying the framework to Lumentum and Intel

Lumentum answers all three favourably in the near term. Optical components are structurally embedded in next-generation data centre architecture; every AI cluster needs physical optical links regardless of which GPU or CPU sits inside it. Operating leverage is demonstrated in the Q3 FY2026 return to GAAP operating profitability, with Q4 non-GAAP operating margin guided at 35.0%-36.0%. CPO and OCS catalysts are in early production with named ecosystem partners including Broadcom and Nvidia.

Intel’s answers are more mixed. CPU demand is structurally supported by the inference workload shift, but it faces ongoing competition from GPUs and custom ASICs optimised for specific inference tasks. Margin recovery is in progress, with gross margin at approximately 35.90%, below historical peaks. Crescent Island and Panther Lake are roadmap items that have not yet generated material revenue.

The competitive headwind Intel faces in inference is not only from established GPU suppliers; custom silicon competition from hyperscaler-built accelerators at Alphabet, Amazon, and Microsoft is projected to capture an increasing share of inference workloads, precisely the segment where Intel’s CPU recovery thesis depends on sustained volume growth.

The framework applies beyond these two names. Any investor evaluating smaller AI infrastructure suppliers can use these three questions to distinguish between companies with durable revenue exposure and those riding a temporary spending wave.

The trajectory ahead: what the next 18 months could mean for both positions

The bull case for each company rests on specific, identifiable catalysts, not abstract optimism.

For Lumentum, the next 18 months are defined by whether CPO and OCS transition from early deployment to reported revenue contribution. The 2027-2028 mainstream adoption window is when these technologies would begin appearing in quarterly results. If hyperscaler capital expenditure commitments hold, Lumentum’s revenue trajectory could extend well beyond the current interconnect upgrade cycle. If those commitments pause, or if CPO commercial adoption delays, the stock’s premium multiple faces pressure.

For Intel, the catalyst map centres on margin expansion and evidence that inference-driven CPU volume growth is translating into sustained financial improvement. Management has described 2026 as a pivotal year for the manufacturing technology roadmap, with the 18A node as the key milestone. The risk is that GPU and ASIC designers continue gaining share in inference-optimised workloads, or that execution setbacks on the 18A node undermine the manufacturing competitiveness narrative. Intel’s turnaround is framed as developing over coming months and years, not a single-quarter event.

| Factor | Lumentum | Intel |

|---|---|---|

| Primary AI Infrastructure Role | Optical components and interconnects | Server CPUs and emerging AI accelerators |

| Near-Term Revenue Catalyst | Data centre interconnect and long-haul optical demand | Inference-driven CPU volume growth |

| Key Emerging Technology | Co-packaged optics and optical circuit switches | 18A process node; Crescent Island and Panther Lake GPUs |

| Primary Risk | Hyperscaler capex pause or CPO adoption delay | GPU/ASIC share gains in inference; 18A execution risk |

The two positions serve different roles within an AI infrastructure allocation. Lumentum offers higher near-term revenue momentum with emerging technology optionality. Intel offers a lower-valuation recovery play with a longer timeline and more execution uncertainty.

Two legacy names, one structural shift, and what it means for how you build an AI infrastructure position

The AI infrastructure trade is not confined to GPU designers. It extends across the full data centre stack, and legacy companies with entrenched technology positions can generate asymmetric recoveries when the architecture shifts in their favour. Lumentum is executing now, with a clear near-term revenue trajectory and record quarterly guidance. Intel is a longer-duration recovery with more execution risk but potentially more valuation upside from a lower base.

The practical question for investors is whether their current AI infrastructure exposure captures these layers. A portfolio concentrated in GPU-adjacent names may be missing the optical networking and CPU inference recovery stories that, in percentage terms, are generating some of the strongest returns in the sector in 2026.

Readers wanting to stress-test whether the recoveries in both names already reflect consensus optimism will find our full explainer on the expectations gap framework, which applies Howard Marks and Aswath Damodaran’s return-versus-expectation model to the current AI infrastructure trade and examines where institutional crowding may be creating asymmetric risks relative to what prices already imply.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.