Prediction markets are pricing a 95-98% probability that the Bank of Japan will raise interest rates on Tuesday, making it one of the most telegraphed central bank decisions in years. Yet traders are watching closely regardless, because what the BOJ says next will matter far more than the 25 basis points everyone already expects.

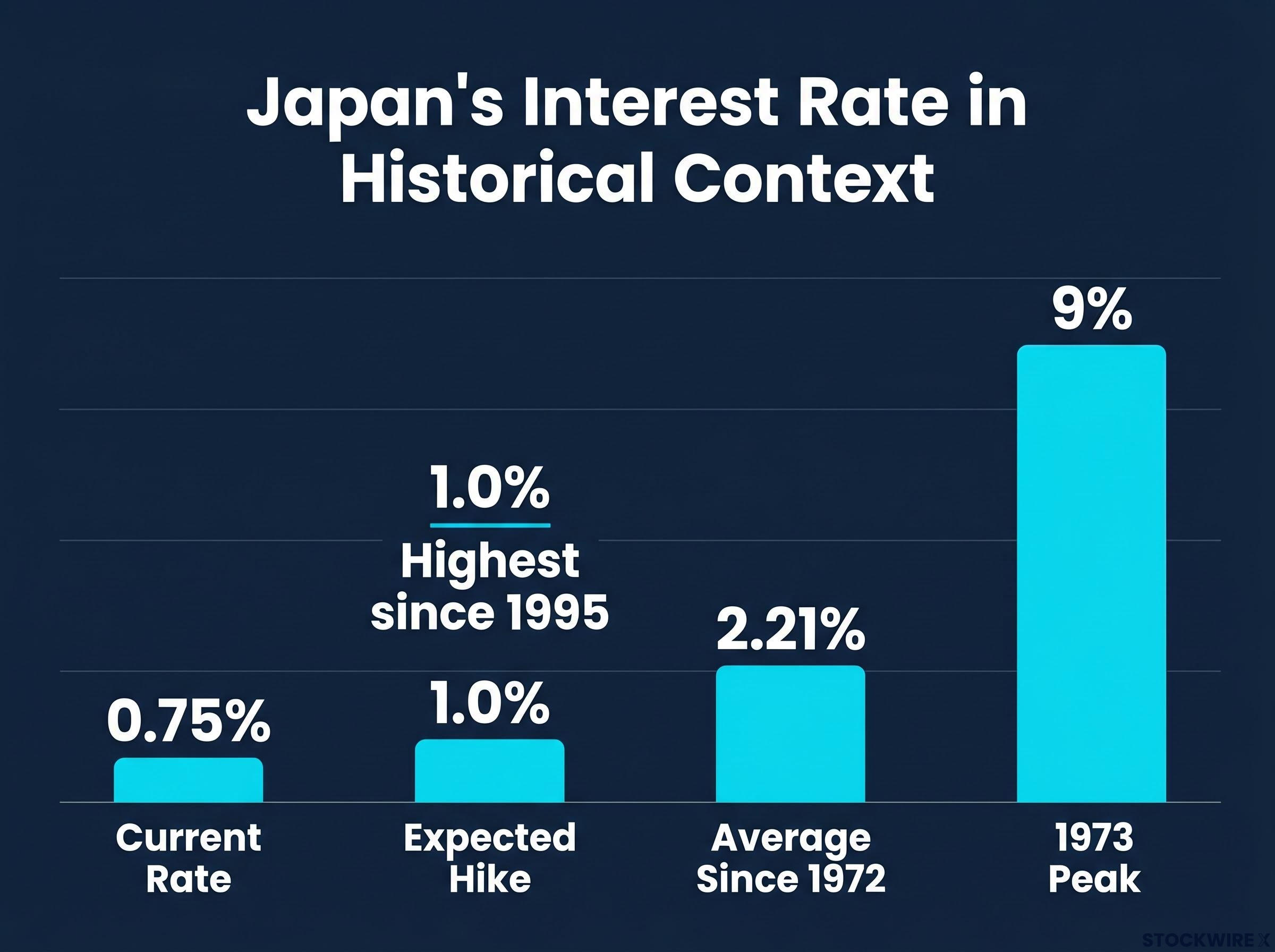

Japanese equities surged on 15 June 2026, with the Nikkei 225 and TOPIX both reported to have set new all-time highs as markets positioned ahead of the BOJ’s two-day policy meeting concluding 16 June. A hike to 1.0% would take the policy rate to its highest level since 1995, extending the most significant monetary policy normalisation cycle Japan has undertaken in three decades.

What follows covers the forces behind the BOJ’s decision, why the post-decision statement and quantitative easing (QE) exit signals are the real market-moving variables, and what each outcome scenario means for Japanese equities, the yen, and broader Asian sentiment heading into a week that also features Reserve Bank of Australia and Federal Reserve decisions.

Nikkei and TOPIX climb to record territory as BOJ meeting gets underway

The numbers on 15 June told a clear story of pre-decision conviction, not caution. The Nikkei 225 surged approximately 5.4% during the session, while the TOPIX advanced roughly 3.6%, with both indices reported to have reached new all-time highs. The rally was broad-based, spanning technology and non-technology sectors alike.

Gains were not confined to Tokyo. US equity futures (ESU26) climbed approximately 1.1% during Asian trading hours, while Australia’s S&P/ASX 200 added roughly 1.3%, extending a constructive global tone into the session.

Note: session figures are based on initial reporting and should be verified against exchange data.

Prediction market pricing: Kalshi and Polymarket data showed approximately 95-98% probability of a 25 basis point BOJ hike as of 15 June 2026, placing this among the most heavily anticipated central bank moves in recent memory.

ANZ analysts cited expectations of a hawkish BOJ pivot as a driver of the positioning. The counterintuitive setup, record equity highs heading into a tightening decision, reflects a market that has already absorbed the rate move itself and is now pricing what comes after it. Whether Monday’s gains represent a durable re-rating or a positioning-driven move that could reverse on a dovish surprise will depend almost entirely on the post-decision statement.

Japan’s equity market re-rating in 2026 has already confounded a bearish consensus built on sovereign debt fears and yen weakness narratives; with the Nikkei and TOPIX now at record highs, the institutional view from Morgan Stanley, UBS, and BlackRock has shifted from structural scepticism toward sector rotation and valuation moderation rather than outright exit.

When big ASX news breaks, our subscribers know first

A 30-year high, not a record: what the BOJ is actually deciding on Tuesday

A hike to 1.0% would not be a record. Japan’s benchmark interest rate averaged 2.21% from 1972 onward and peaked at 9% in 1973. What Tuesday’s expected move would deliver is a 30-year high, the highest policy rate since 1995, and a meaningful step in a normalisation cycle that still has considerable distance to travel by any historical standard.

The current policy rate sits at 0.75%, itself the highest level since 1995, after the BOJ began its hiking cycle from the negative rate regime it maintained for years. The expected 25 basis point increase to 1.0% has been priced by prediction markets at roughly 95-98% probability on platforms including Kalshi and Polymarket.

How the April dissent changed the calculus

The internal pressure behind this move became visible at the April 2026 meeting. The BOJ held rates steady at 0.75%, but three board members dissented in favour of an immediate hike to 1.0%, an unusually strong signal of hawkish conviction within the policy board.

The Bank of Japan April 2026 policy statement confirms the voting record in full, showing three of nine board members dissenting in favour of an immediate hike to 1.0%, a margin of internal disagreement that historically signals the dissenting position prevails at the next scheduled meeting.

Three of nine board members voted for an immediate hike at the April meeting, the kind of dissent that typically precedes action at the following decision.

Persistent inflation running above the 2% target, ongoing yen weakness, and energy-price volatility linked in part to Middle East tensions sustained internal pressure to move. By the time markets opened on 15 June, the question was no longer whether the BOJ would hike, but how aggressively it would frame the path beyond 1.0%.

Why Japan’s inflation story is more structural than cyclical

Previous BOJ tightening cycles stalled because inflation proved transitory, driven by cost-push shocks that faded before domestic demand could sustain price pressures independently. This cycle looks different, and the distinction matters for investors assessing whether the normalisation path is durable or fragile.

Three factors are sustaining inflation above the BOJ’s 2% target:

Japan’s private-sector growth in Q1 2026 adds weight to the structural inflation reading: the economy expanded at a 2.1% annualised rate with government spending contributing only 0.3 percentage points, meaning corporate pricing behaviour and household consumption are doing the heavy lifting that previous BOJ tightening cycles lacked.

- Domestic wage growth: Spring wage negotiations (shunto) have delivered meaningful pay increases, feeding through to consumer spending and corporate pricing behaviour

- Yen weakness and imported inflation: The BOJ explicitly noted concerns about imported inflation at the April meeting, with a weaker yen amplifying the cost of energy and goods priced in US dollars

- External energy-price volatility: Middle East tensions, including Iran-related risks, have kept energy costs elevated, though this remains one contributing factor rather than the primary driver

The BOJ’s own framing has shifted accordingly. Bloomberg reporting indicates officials see “scope for additional increases” beyond June, citing still-low real rates and upside inflation risks as justification for continued normalisation. Markets expect the BOJ to revise core inflation projections in its Outlook Report, which would reinforce the structural reading.

What the spring wage negotiations signal

The annual spring wage round is the BOJ’s preferred real-time gauge of whether inflation has become self-sustaining. If companies are raising wages because they expect to pass costs through to consumers, and workers are spending those wages at higher prices, the inflation loop is domestic and durable rather than externally imposed and temporary.

Investors will scrutinise whether the BOJ’s post-meeting language frames wage momentum as durable or as a phenomenon that could fade if global commodity prices ease.

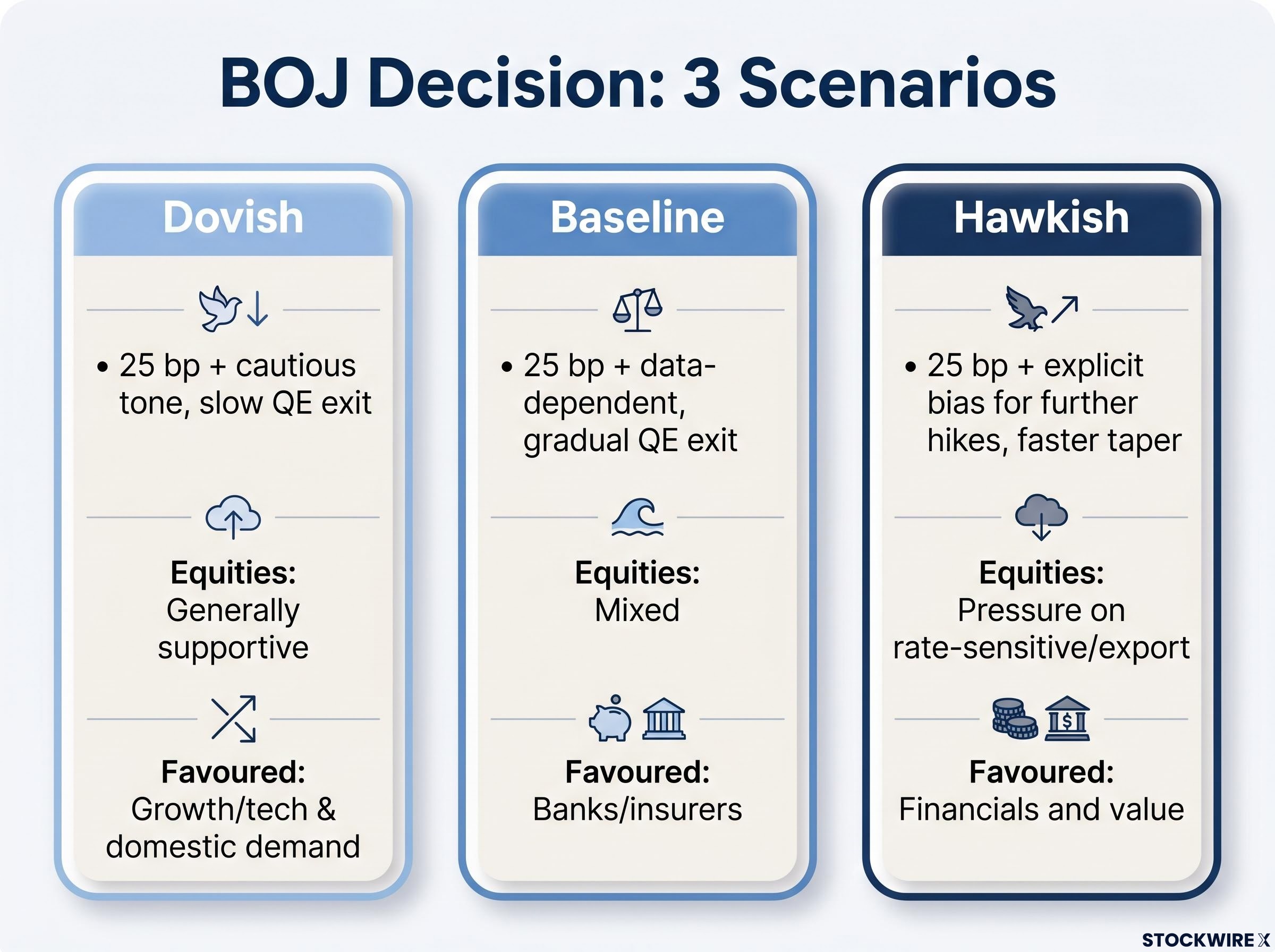

Forward guidance and QE exit: the real market-moving variables

The 25 basis point hike is already priced. The volatility will come from language.

Three elements of Tuesday’s post-decision statement will drive equity, bond, and currency reactions more than the headline rate move: the tone on the scope and pace of further hikes, any explicit references to exchange rate developments and yen pass-through to inflation, and the forward framing of the BOJ’s balance-sheet exit strategy.

Oxford Economics expects the BOJ to announce its FY2027 exit plan from quantitative easing at the June meeting. Any concrete timetable for JGB-purchase tapering could prove more market-moving than the rate step itself.

Bloomberg reporting has flagged “scope for additional increases” due to still-low real rates and upside inflation risks. NHK commentary points to two rate hikes expected this year alongside reduced JGB buying. The spectrum of possible tones ranges from dovish (framing the hike as “calibration” with emphasis on patience) through a data-dependent baseline to an explicitly hawkish stance signalling a clear bias for further hikes and a faster taper.

For global fixed income and FX desks, the JGB-purchase tapering roadmap and yen-language framing in Tuesday’s statement could reprice positions far more significantly than a move the market has already absorbed.

| BOJ Outcome | Yen Reaction | JGB Yields | Equities (Broadly) | Sector Tilt |

|---|---|---|---|---|

| Dovish (25 bp + cautious tone, slow QE exit) | Mildly stronger or flat | Small move higher at front end | Generally supportive; risk-on continuation | Growth/tech and domestic demand favoured |

| Baseline (25 bp + data-dependent, gradual QE exit) | Modest appreciation | Gradual bear-steepening | Mixed; near-term volatility | Banks/insurers benefit; exporters FX-sensitive |

| Hawkish (25 bp + explicit bias for further hikes, faster taper) | Sharper yen gains | Larger rise, especially belly and long end | Pressure on rate-sensitive and export names | Financials and value favoured |

Three scenarios and what each means for the yen, JGBs, and equities

With the hike itself all but certain, investors need a framework for the three paths that Tuesday’s statement could open.

- Dovish outcome. A 25 basis point hike accompanied by cautious language, emphasis on downside risks, and a slow approach to QE exit. This is the most supportive scenario for equities broadly. Yen appreciation would be muted, JGB yields would edge higher at the front end but remain contained, and growth, technology, and domestic demand sectors would be favoured. Financials would benefit less in this framing.

- Baseline outcome. A 25 basis point hike with flexible, data-dependent forward guidance and a gradual QE exit roadmap. Near-term volatility is likely as markets parse the language, but if normalisation is read as growth-positive, sentiment could stabilise. Banks and insurers stand to benefit from a higher rate environment, while exporters remain sensitive to yen movements.

- Hawkish outcome. A 25 basis point hike paired with an explicit bias toward another increase this year and a faster JGB-purchase taper. This scenario would likely trigger sharper yen appreciation, pressure on rate-sensitive and export-oriented names, and a potential consolidation from record highs. Financials and value would be favoured; growth and long-duration equities face the greatest risk.

Across all three scenarios, domestic financials (banks and insurers) remain the primary beneficiaries where rates rise as expected. The differentiation lies in the magnitude of that benefit and whether exporters face offsetting FX headwinds.

BOJ, RBA, and Fed: a historic cluster of central bank decisions in one week

The BOJ decision does not arrive in isolation. Three of the world’s most closely watched central banks are scheduled to deliver policy decisions within the same week, creating an unusually concentrated set of signals for global risk appetite and capital allocation.

- Bank of Japan: Two-day meeting 15-16 June, decision expected 16 June (per official BOJ calendar; date should be verified before publication). A 25 basis point hike to 1.0% is the near-unanimous expectation.

- Reserve Bank of Australia: Meeting date requires verification against the official RBA calendar. The RBA is widely expected to hold its policy rate steady, providing a direct contrast with the BOJ’s tightening stance.

- US Federal Reserve: Policy meeting scheduled later in the week of 15 June, serving as a further focal point for investors assessing the trajectory of US monetary policy.

The divergence across these three institutions is now highly country-specific, particularly across Asia-Pacific. The BOJ is tightening, the RBA is holding, and the Fed’s path remains data-dependent. For global investors, the sequencing of these decisions and any surprises in tone could shift the macro narrative for the remainder of June.

Investors wanting to map the full sequence of policy risk across the week will find our deep-dive into the June 2026 central bank decision window, which covers Kevin Warsh’s first Fed meeting, the simultaneous Fed and Bank of England decisions on 18 June, and how the Strait of Hormuz closure has embedded inflationary uncertainty that every central bank in the window must price with incomplete information.

Carry-trade liquidation transmits BOJ policy surprises well beyond Japan’s borders, with yen strength forcing position unwinds that flow directly into the Australian dollar and higher-beta ASX sectors within hours; investors treating the BOJ decision as a Japan-specific event may underestimate the speed and breadth of cross-asset repricing that a hawkish surprise could trigger.

Japan’s tightest policy in 30 years is just the beginning of a longer story

At 1.0%, Japan’s policy rate would still sit well below the 2.21% historical average since 1972. The rate remains deeply accommodative by any long-run measure. The question investors should carry away from Tuesday is not whether the hike happens, but how fast the BOJ is prepared to move beyond it.

Three signals in the post-decision statement will shape that answer: the tone on future hikes and whether the BOJ frames further tightening as conditional or directionally committed; the specifics on JGB tapering and the FY2027 QE exit plan, where any concrete timetable could reprice global bond markets; and any language on the yen and imported inflation, which will indicate how much FX dynamics are influencing the policy path directly.

If the normalisation cycle is sustained, according to Oxford Economics and Bloomberg analysis, it represents a structural shift in global fixed income and FX dynamics that extends well beyond a single meeting. Japan’s three-decade experiment with ultra-loose monetary policy is ending. What replaces it will take longer to resolve than one Tuesday in June.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding BOJ policy, market reactions, and asset-class implications are speculative and subject to change based on market developments and central bank decisions.