ASIC Hands Director Maximum 5-Year Ban After $12.4M Collapse

6 hrs ago

Hedge funds and institutional investors have built the largest short position ever recorded against Australia’s big four banks, with approximately $10.9 billion now wagered on falling share prices across Commonwealth Bank of Australia, ANZ, Westpac, and NAB. That figure has roughly doubled in six months. Disclosed under ASIC’s short-selling reporting regime, positions of this scale signal that some of the country’s most well-resourced professional investors believe current bank valuations carry material downside risk. The timing carries particular weight: Australian households and superannuation funds hold significant exposure to the big four, making this institutional sentiment shift directly relevant to millions of investors. What follows breaks down who is behind the positions, why they have built them now, which bank carries the heaviest exposure, and what record short interest actually means for retail investors holding bank shares.

The number is $10.9 billion. That is the approximate total short exposure across Australia’s big four banks as of mid-June 2026, and it is the largest dollar-value short position ever recorded against the sector since ASIC began its current short-selling disclosure regime on 1 June 2010.

The figure alone is striking. Its trajectory is more so. Six months ago, the combined short position sat at roughly half that level. The doubling over that period is the central signal: conviction among professional short sellers has not merely persisted but intensified at pace.

ASIC’s short-selling disclosure regime requires holders of significant short positions to report daily to the regulator, with aggregate data published publicly, making Australia one of the more transparent markets globally for tracking institutional bearish sentiment.

Speculators have “never been more bearish” on the big four banks in dollar terms, according to analyst commentary on the disclosed positions.

The last time Australian bank short interest drew headlines of this kind was during and after the Hayne Royal Commission, which ran from December 2017 to February 2019. Offshore macro funds drove the bulk of that activity, treating Australia’s banks as a macro trade tied to regulatory and reputational risk.

This time is structurally different. The current wave is being led primarily by domestic long-short managers, firms deeply familiar with Australian bank earnings, regulation, and the broader economic cycle. Three named managers have disclosed or confirmed short positioning, each with a distinct but overlapping rationale.

The domestic-led nature of the current bank short wave reflects a broader pattern in how domestic short sellers time their entries: rather than fading into earnings selloffs, institutional bears on the ASX have consistently used post-downgrade momentum as confirmation of a thesis already built on fundamental research, a discipline that makes the doubling of bank short positions over six months a more deliberate signal than opportunistic macro positioning.

| Firm | Named Manager | Target(s) | Stated Rationale |

|---|---|---|---|

| Firetrail Investments | Patrick Hodgens (CIO) | All four major banks | Banks “priced for an ideal scenario”; little margin for error |

| Regal Funds | Mark Nathan (Portfolio Manager) | CBA specifically | Outlook shifted from positive to subdued; Federal Budget policy changes a factor |

| Blackwattle Investment Partners | Joe Koh (Portfolio Manager) | Not specified | Potential additional selling wave once Federal Budget legislative changes are enacted |

All three managers were cited by The Australian Financial Review.

Both Blackwattle and Regal cited Federal Budget policy changes as a factor shaping their outlook. Blackwattle’s Joe Koh flagged the possibility that offshore hedge funds are holding back additional short positions until legislative changes are formally enacted. If that trigger arrives, it could represent a second wave of short interest layered on top of the domestic positions already in place.

The short thesis begins with price, not earnings. Firetrail’s Patrick Hodgens characterised the big four as “priced for an ideal scenario”, a framing that carries a specific implication: current share prices embed assumptions of benign conditions, resilient earnings, and an absence of negative surprises.

When a stock is “priced for perfection”, any reduction to earnings forecasts is likely to be met with a more severe market reaction than it would from a lower valuation base.

Beneath that valuation layer sit multiple fundamental pressures that short sellers believe make perfection unlikely:

The combination matters more than any single factor. Short sellers are not betting on a single catalyst but on a valuation that leaves no room for the kind of earnings pressure that multiple headwinds could produce simultaneously.

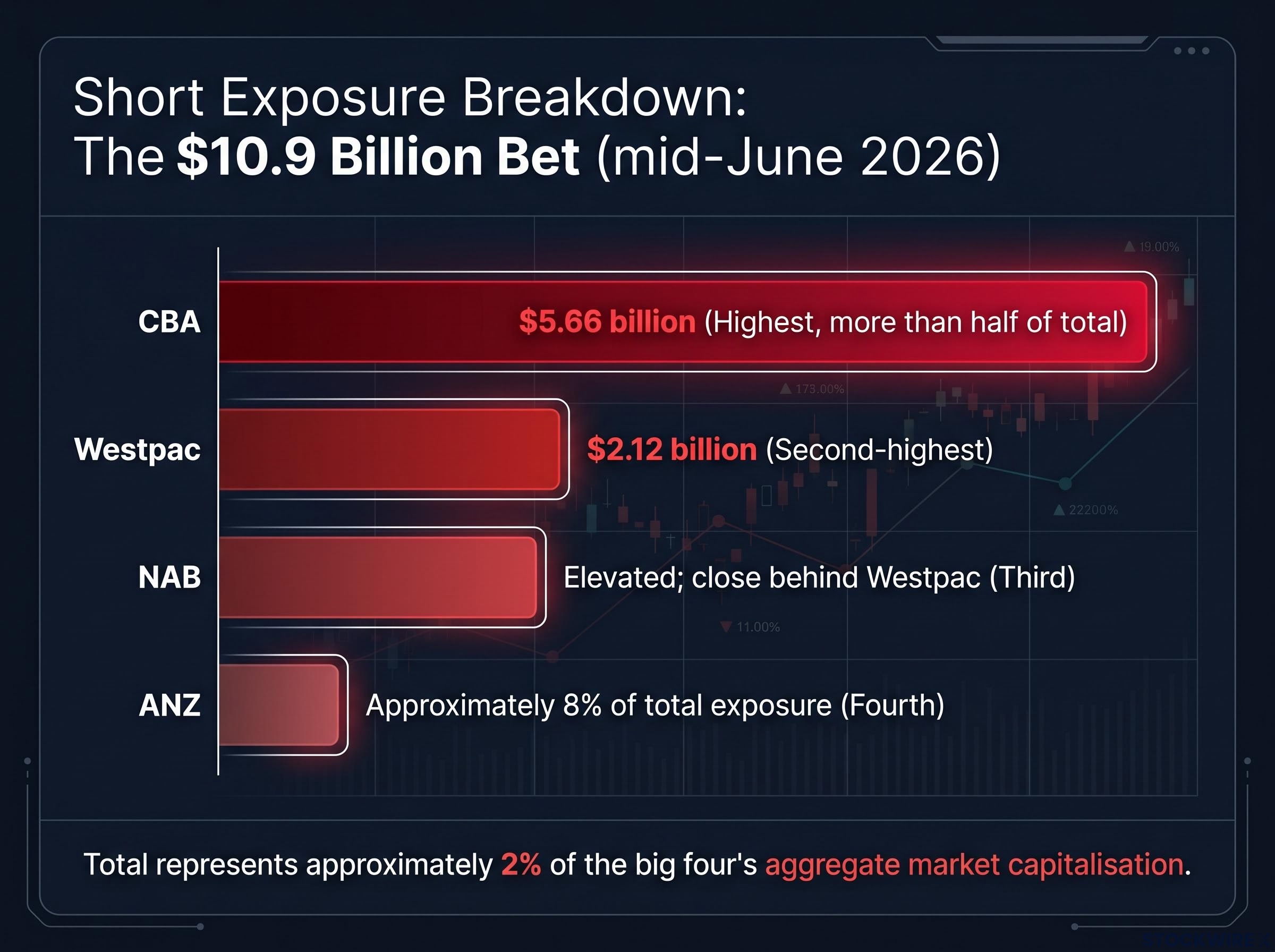

$5.66 billion. That is the approximate short exposure against CBA alone, more than half the total across all four banks.

| Bank | Approximate Short Exposure | Relative Position |

|---|---|---|

| CBA | $5.66 billion | Highest (more than half of total) |

| Westpac | $2.12 billion | Second-highest |

| NAB | Elevated; close behind Westpac | Third |

| ANZ | Approximately 8% of total exposure | Fourth (approximate) |

The concentration logic is straightforward. CBA trades at a material premium to its peers on both price-to-earnings and price-to-book measures. Short sellers view that premium as the sector’s most exposed point: any re-rating from a higher starting valuation carries the largest potential price decline.

CBA’s valuation premium relative to peers is not a recent development: structural forces including ASX 200 index weighting and compulsory superannuation inflows have created persistent mechanical buying pressure that has sustained the gap regardless of earnings trajectory, which is precisely what makes the $5.66 billion short position against it the highest-conviction bet in the current wave.

For investors holding CBA specifically, the concentration of short interest is a direct signal that professional capital views its premium as the position most vulnerable to an earnings disappointment. It does not dictate a sell decision, but it raises the stakes of being wrong on the earnings outlook.

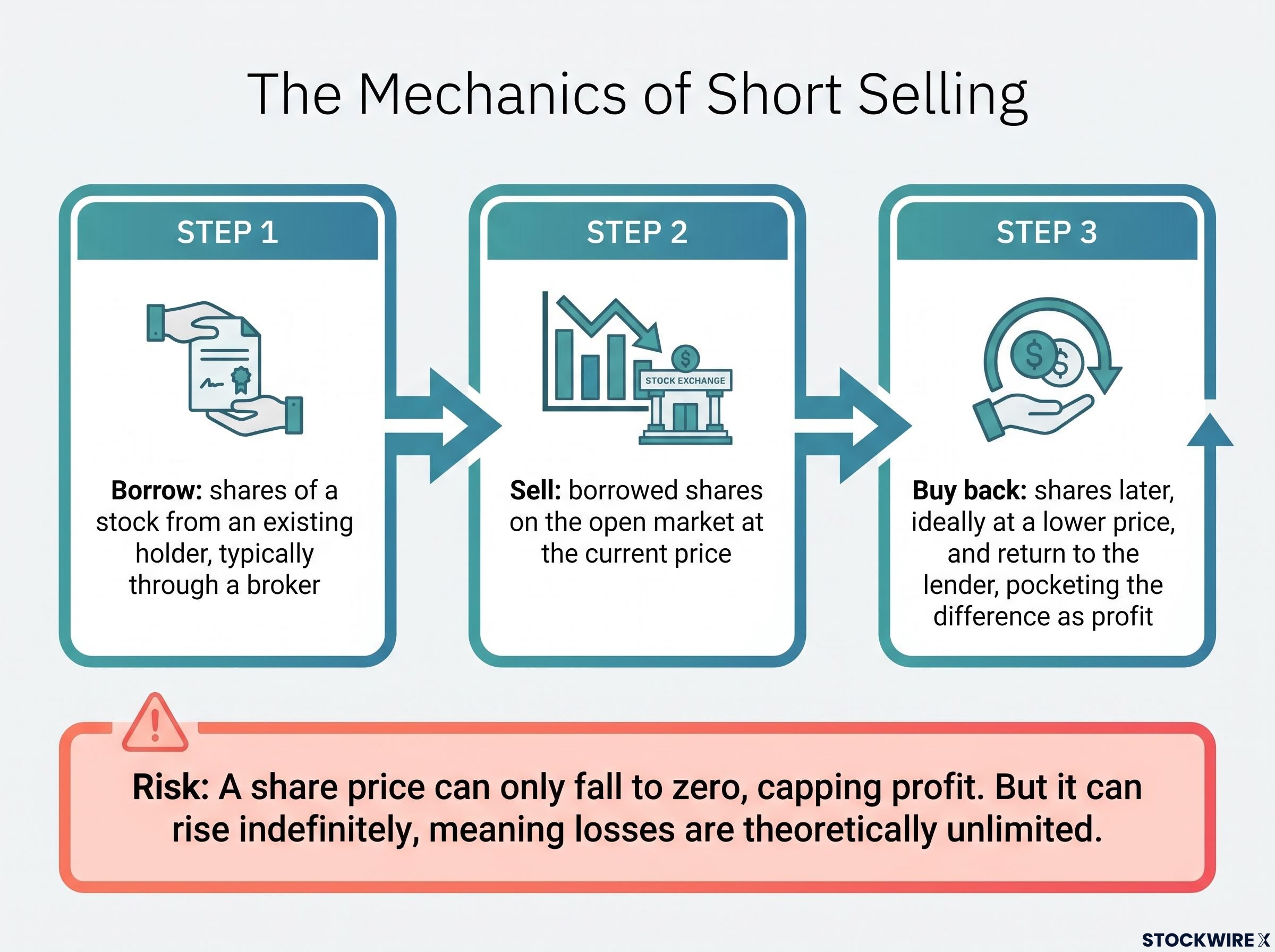

Short selling is one of the most widely referenced but least well understood mechanisms in equity markets. At its core, it involves three steps:

The risk is asymmetric. A share price can only fall to zero, capping the short seller’s profit. But it can rise indefinitely, meaning losses for a short seller are theoretically unlimited. Even well-resourced funds get short trades wrong, frequently.

ASIC (the Australian Securities and Investments Commission) is the regulatory body responsible for short-selling disclosure in Australia. The $10.9 billion figure represents approximately 2% of the big four’s aggregate market capitalisation, meaning the vast majority of institutional capital remains positioned long.

ASIC’s short-selling disclosure regime requires all on-market short sales to be reported regardless of size, making Australia’s system more transaction-granular than equivalent frameworks in the US or UK; a detail that also explains why the Macquarie Securities $35 million penalty in March 2026 for misreporting short sale data across up to 1.5 billion transactions was treated as so consequential for market surveillance integrity.

The post-Hayne Royal Commission period (December 2017 to February 2019) saw elevated short interest against the big four that did not result in a sustained share price collapse. Short sellers were positioned for a fundamental reckoning that, in the end, proved less severe than feared.

If earnings or macro conditions surprise positively, forced short-covering can amplify upside moves, sometimes producing rallies sharper than those driven by fundamentals alone. Record short interest has historically coincided with both genuine downturns and market bottoms. It is a warning signal, not a verdict.

Short-covering dynamics on the ASX can produce price movements that are sharper and faster than those driven by fundamentals alone, as Polynovo’s repeated double-digit intraday surges and Guzman Y Gomez’s 20% intraday move in May 2026 illustrated; with $10.9 billion short against the big four, a positive earnings surprise or macro shift could trigger covering activity at a scale the sector has not seen in the current reporting cycle.

The $10.9 billion short position does not tell any individual investor what to do. It does, however, raise the risk profile for new or heavily concentrated exposures to the sector at current prices.

According to analysis of the current positioning, the risk-reward for buying the big four at current prices is described as “less attractive than at almost any point in the past decade.”

The big four remain significant sources of franked dividend income for retirees and superannuation funds. That income stream is real and valuable. But high dividend yields can be more than offset by capital losses if share prices correct from stretched valuations.

Before dismissing or reacting to the short interest data, retail investors may benefit from asking themselves several specific questions:

These are not rhetorical questions. They are the same questions the domestic fund managers building these short positions have already answered for themselves.

$10.9 billion in short positions against Australia’s banks is the most significant institutional sentiment signal in the sector’s modern history. It deserves to be taken seriously, not because short sellers are always right, but because the scale and domestic origin of this positioning reflect a conviction that current valuations leave little room for error.

Short sellers may be proved correct by a deteriorating earnings environment, or they may be forced to cover at a loss if the economy and bank results surprise to the upside. Both outcomes have historical precedent.

For retail investors, the record short is a reason to review bank holdings with clear eyes, not a reason to panic or to dismiss the signal.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Short selling involves borrowing shares, selling them at the current price, and buying them back later at a lower price to pocket the difference as profit. In the context of Australian banks, institutional investors have built approximately $10.9 billion in short positions against the big four, wagering that share prices will fall from what they view as stretched valuations.

Domestic fund managers cite valuations that are priced for an ideal scenario, leaving little margin for error if earnings disappoint. Key concerns include net interest margin compression, a softer credit growth outlook, regulatory pressures, and Federal Budget policy changes that could weigh on the sector's earnings trajectory.

Commonwealth Bank of Australia (CBA) carries the largest short position, with approximately $5.66 billion in exposure, more than half of the total $10.9 billion across all four banks. Short sellers target CBA specifically because it trades at a material premium to peers, meaning any re-rating carries the largest potential price decline.

Not necessarily. Record short interest is a warning signal from professional investors, not a guaranteed predictor of price falls. During the post-Hayne Royal Commission period, elevated short positions did not result in a sustained share price collapse, and if conditions surprise positively, forced short-covering can actually amplify upside moves.

ASIC requires holders of significant short positions to report daily to the regulator, with aggregate data published publicly, making Australia one of the more transparent markets globally for tracking institutional bearish sentiment. The current regime has been in effect since 1 June 2010, though derivative structures are not fully captured in the disclosed data.