ASX 200 Chart at a Supply Zone Test as NFP Week Looms

2 hrs ago

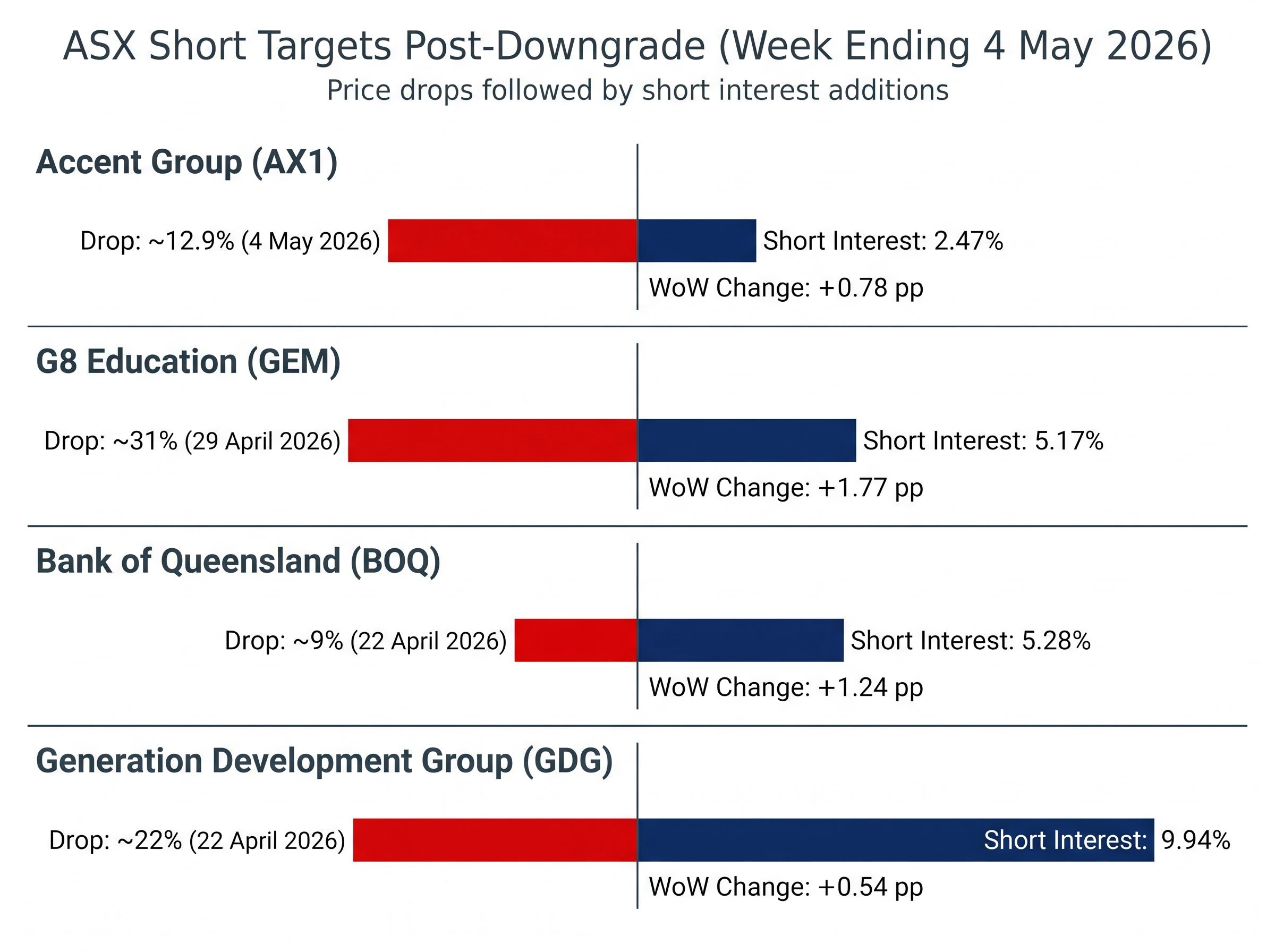

Four ASX-listed companies fell between 9% and 31% in a single trading session after earnings downgrades in late April and early May 2026. Within days, short sellers were adding to positions in all four.

The latest ASIC short position data, covering the week ending 4 May 2026, shows short interest climbing in Accent Group, G8 Education, Bank of Queensland, and Generation Development Group immediately after each stock had already been punished by the market. This is not a random pattern. It reflects a deliberate short-seller strategy: the belief that the first drop is rarely the last.

What follows unpacks what that behaviour signals, why post-downgrade stocks attract short sellers rather than bargain hunters, and what the short-interest data means for ASX investors trying to read market sentiment during earnings season.

The ASIC short position table for the week ending 4 May 2026 covers a broad cross-section of bearish institutional positioning. Energy, uranium, lithium, gold, and funds management names all saw short interest additions. But a specific cluster stands out: four stocks where short sellers added positions within days of a sharp earnings-downgrade selloff.

The timeline is precise.

| Stock (ASX Code) | Selloff Date | Single-Day Decline | Short Interest (4 May) | Week-on-Week Change |

|---|---|---|---|---|

| Accent Group (AX1) | 4 May 2026 | ~12.9% | 2.47% | +0.78 pp |

| G8 Education (GEM) | 29 April 2026 | ~31% | 5.17% | +1.77 pp |

| Bank of Queensland (BOQ) | 22 April 2026 | ~9% | 5.28% | +1.24 pp |

| Generation Development Group (GDG) | 22 April 2026 | ~22% | 9.94% | +0.54 pp |

GDG’s monthly increase of 3.96 percentage points to 9.94% is particularly telling. Short sellers were building that position well before the single-week snapshot captured the full picture.

Important caveat: ASIC short position data carries a four-day reporting lag. Disclosure is not required until three business days after trade execution, and the public table reflects positions as of the prior Thursday. The figures above already incorporate positions taken in the days immediately following each selloff, but retail investors reading the table on publication day are working with data that is at minimum four days old.

The instinct for most retail investors is to treat a 20% single-day drop as evidence that the bad news is priced in. Short sellers read the same event differently. An initial selloff signals that the market has begun to agree with the bearish thesis, not that it has finished agreeing.

This is the momentum confirmation logic. The first drop is not the end of the trade; it is the entry signal. Short sellers view the post-downgrade period as the window where three specific conditions tend to persist:

Earnings quality deterioration beneath headline results is one reason short sellers are not waiting for a second miss before adding to positions: when a company beats consensus on the top line but reports a 45.6% surge in credit impairment charges, as NAB did in H1 FY26, the beat itself becomes a warning about the forward period rather than reassurance that the bad news is priced.

Broker data suggests a median further decline of approximately 10-12% for ASX small-caps over three months following an initial downgrade selloff. When companies record a second major miss, historical patterns point to 20-30% further declines before support forms, according to analysis of the Flight Centre case published by The Bull.

Not every downgrade triggers a sustained short position. Stocks where the selloff resolves the problem, through a clean guidance reset, intact balance sheet, and no multi-quarter structural issues, tend to stabilise and offer less attractive short targets.

The indicators that short sellers watch for further downside include repeated misses, deteriorating cash flow, and management turnover. In the Week 20 case studies, none of the four stocks exhibited a clean, single-event resolution. Each carried unresolved questions about whether the reported weakness was a one-off or the beginning of a longer cycle. That distinction is what separates a dip from a deterioration, and it is why shorts added rather than covered.

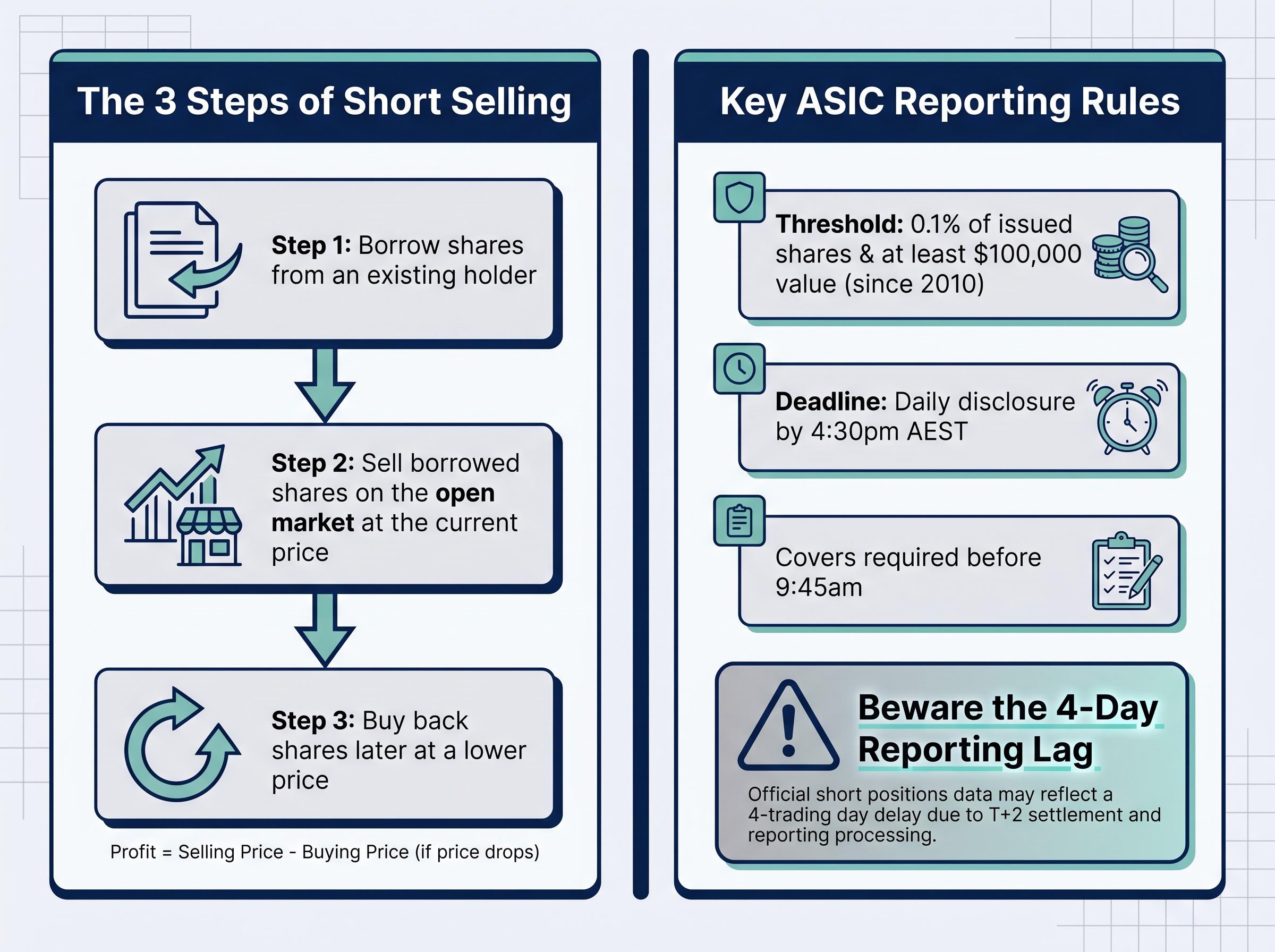

A short position is a bet that a stock’s price will fall. The mechanics involve three steps:

If the price rises instead, the short seller faces a loss, and there is no cap on how high a stock can go. That asymmetry is why short selling carries more risk than buying, and why the positions reflected in ASIC data represent high-conviction bets rather than casual speculation.

ASIC’s reporting framework governs what becomes visible to the public:

The ASIC short selling rules that govern what becomes visible to investors were stress-tested in March 2026 when the NSW Supreme Court imposed a $35 million penalty on Macquarie Securities Australia Limited for misreporting short sale data across more than 1.5 billion transactions spanning 15 years, a ruling that exposed how systematically degraded public short interest dashboards can become when compliance breaks down.

Ashurst’s analysis of ASIC derivative disclosure rules details how the Treasury Laws Amendment (Strengthening Financial System and Other Measures) Act 2025 introduced the “deemed economic interest” concept, which extended transparency obligations to derivative positions that previously fell outside the reporting framework.

The public table reflects positions as of the prior Thursday. A short position opened the day after a downgrade may not appear until the following week’s publication. For the Week 20 data, this means the figures for AX1, GEM, BOQ, and GDG already incorporate positions taken in the immediate aftermath of each selloff, but retail investors reading the table on 11 May 2026 are observing a snapshot that is at least four days old.

This lag does not make the data useless. It does mean the signal is confirmatory rather than predictive. The ASIC table tells investors what short sellers did; it does not tell them what short sellers are doing right now.

The four stocks share a pattern (post-downgrade short interest build) but tell different stories across different sectors. Each represents a distinct bearish thesis.

Pre-downgrade short positioning in Generation Development Group is particularly instructive: institutional short sellers were lifting their stake from approximately 4% to over 9% in the weeks preceding the 22 April selloff, treating a quarterly FUM update the company classified as non-price-sensitive as a growth warning the market had not yet fully absorbed.

Source for all short position data: Market Index Short Seller Series, Week 20, authored by Kerry Sun, published 11 May 2026.

Approximately 55% of surveyed retail investors now view rising short interest as a meaningful sentiment gauge, up from 2025 levels, according to financial media polling. Thread analysis of r/AusFinance from April and May 2026 found roughly 60% of participants treating short buildups in post-downgrade names as red flags for further downside. The shift is real: retail investors are reading ASIC data with increasing pragmatism.

The signal, however, is not mechanically reliable. Four caveats apply:

Calibrating expectations: The sustained success rate of approximately 50-60% for post-earnings short strategies sits well below the 70% headline figure sometimes cited in financial media. Accounting for forced covers during mid-cycle rallies, as occurred in mid-2025, is what separates the real hit rate from the advertised one.

The short-interest data is most useful when combined with other signals: management commentary, balance sheet trends, and the direction of analyst revisions. It is a sentiment layer, not a standalone trade signal.

The Week 20 data captures a snapshot from a single week in a reporting season that is still producing results. The pattern of short interest building after selloffs is likely to continue as remaining ASX companies report.

The ASX earnings downgrade wave sweeping retail, healthcare, and industrials in 2026 is not a cluster of isolated company-specific events; overlapping macro pressures including a 4.6% CPI print, renewed RBA rate hikes, and elevated input costs have pushed the ASX 200 into negative territory for the calendar year, creating conditions where short sellers can position against sector-wide deterioration rather than single-stock thesis calls.

The broader rising shorts table reinforces this. Beyond the four earnings-downgrade names, short sellers added positions across energy, uranium, lithium, gold, and funds management stocks during the same week. The bearish institutional posture extends well beyond the case studies examined here.

Two other names illustrate how the playbook operates across longer timeframes. Domino’s Pizza (DMP) carried 15.86% short interest as of 4 May 2026, reflecting sustained bearish positioning in a consumer-facing name with ongoing margin compression concerns. Flight Centre (FLT) sat at 10.70% short interest, down 0.98 percentage points for the week but still deeply shorted after a year-to-date decline of approximately 32%, a position that has persisted across multiple quarters following repeated downgrades. Lotus Resources (LOT) offered a variant of the same pattern: short interest surged to 15.11% after a 34% single-day collapse on 30 April 2026 following a data retraction rather than an earnings miss.

For investors who want a structured approach to interpreting this data during the rest of the reporting season, the framework is straightforward:

The direction of that movement, up or stable, is the market’s first collective assessment of whether the worst has passed. It is not infallible. But it is one of the few signals available to retail investors that reflects what institutional participants are actually doing with their capital, not what they are saying.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

As of the week ending 4 May 2026, Generation Development Group (GDG) carried the highest short interest among the post-downgrade names at 9.94%, while Domino's Pizza (DMP) led the broader ASX short table at 15.86% and Lotus Resources (LOT) surged to 15.11% after a 34% single-day collapse.

Short sellers view the initial post-downgrade selloff as a momentum confirmation signal, not a resolution. They add positions because management credibility is damaged, margin compression is often multi-quarter, and analyst earnings revisions typically arrive in multiple rounds rather than a single cut.

Under ASIC rules in place since 2010, any short position representing at least 0.1% of issued shares and a minimum value of $100,000 must be disclosed by 4:30pm AEST daily, with public tables published weekly; however, a four-day reporting lag means the published data reflects positions as of the prior Thursday, not the current day.

Rising short interest indicates that institutional participants are increasing bearish bets on a stock, suggesting they expect further price declines. However, it is not a one-way signal, as heavily shorted stocks are also vulnerable to short squeezes if positive news triggers forced covering.

According to a December 2025 Livewire Markets review, post-earnings short strategies on the ASX have seen sustained success rates of approximately 50-60% when accounting for forced covers during mid-cycle rallies, which is notably below the 70% headline figure sometimes cited in financial media.