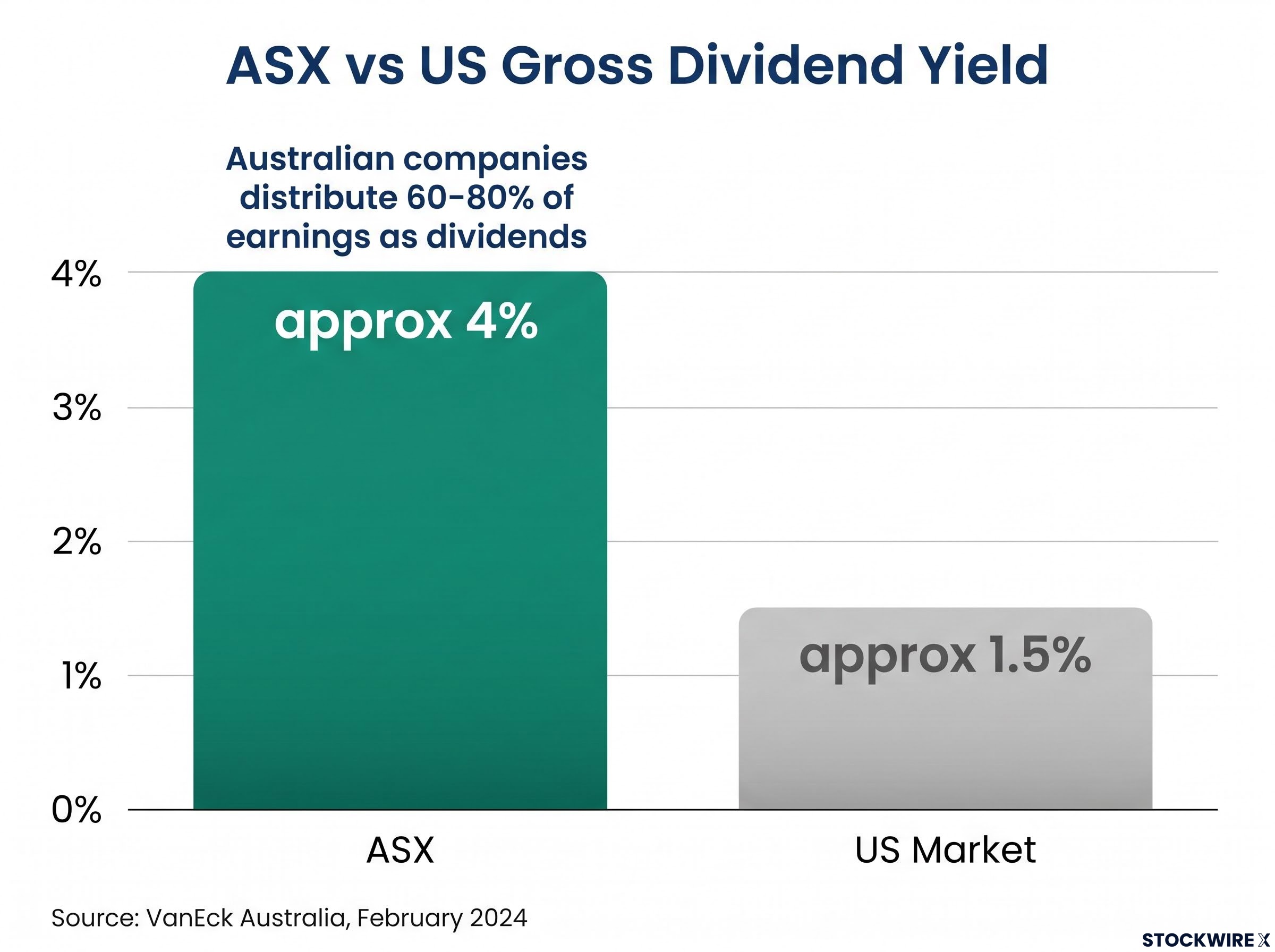

The ASX has historically delivered a gross dividend yield of approximately 4%, roughly double the 1.5% offered by US equities. That gap makes Australia one of the most income-friendly sharemarkets in the world, and it makes passive income investing a particularly compelling strategy for Australian beginners.

Passive income investing is a distinct financial goal from wealth accumulation. The primary objective is generating a reliable stream of cash from investments, whether to supplement current earnings or fund retirement. This guide is designed for beginners who want to understand their options across shares, exchange-traded funds (ETFs), bonds, and cash instruments before committing capital. By the end, the picture should be clear: what each income-generating instrument does, what yields are realistically available on the ASX, what risks accompany each option, and how to combine them into a diversified income portfolio suited to individual goals and timelines.

What passive income investing actually means (and how it differs from growth investing)

The distinction is sharper than most beginners expect. Passive income investing prioritises regular cash flows from a portfolio. The goal is not to maximise the value of the capital base itself but to generate income that arrives in an investor’s account on a predictable schedule, through dividends, interest payments, or fund distributions.

Growth investing works differently. Profits are typically reinvested into the business or compounded within the portfolio. Returns are realised through capital appreciation, usually at the point of sale. A growth investor may hold a company for years without receiving a dollar of income along the way.

Neither approach is inherently superior. What matters is that they serve different purposes, and confusing the two leads to poor decisions. ASIC’s Moneysmart guidance advises investors to consider total return (income plus capital growth) and to match investments to their risk tolerance and timeframe. That advice applies especially to income investors, who sometimes fixate on yield at the expense of capital preservation.

The defining characteristics of each approach help clarify the choice:

- Income investing targets regular cash distributions (dividends, coupons, interest) as the primary return

- Growth investing targets capital appreciation, with returns realised at sale

- Income investors prioritise capital preservation alongside yield, since a shrinking capital base erodes future income

- Reinvestment optionality exists in both: income investors can reinvest distributions to compound their base before switching to drawdown later

Not every company distributes dividends. Growth-oriented businesses frequently redirect profits back into operations, research, or expansion. Selecting a stock purely because it pays a high yield, without understanding whether that yield is sustainable, is the most common beginner mistake in income investing.

When big ASX news breaks, our subscribers know first

The income toolkit: shares, ETFs, bonds, and cash explained for Australian investors

Four main instrument types generate income for ASX investors. Each works differently, carries distinct risks, and suits different investor needs. Before comparing yields or assessing trade-offs, it helps to understand what each tool actually does.

The structural differences between shares, bonds, and ETFs go deeper than how income is generated: each instrument carries a distinct mechanism for generating returns, a different risk profile in falling markets, and a different cost structure that compounds meaningfully over long holding periods.

Dividend-paying shares distribute a portion of company profits to shareholders, typically on a quarterly or semi-annual basis. In Australia, many of these dividends come with franking credits, a tax feature unique to the Australian system. Franking credits represent tax already paid by the company on its profits; eligible investors can use these credits to reduce their own tax liability, making franked dividends particularly valuable on an after-tax basis. Investors can also elect to reinvest dividends automatically through a dividend reinvestment plan (DRP), compounding their portfolio over time.

Income ETFs and managed funds pool capital from many investors and distribute income sourced from dividends on equities held in the portfolio, interest on fixed-income holdings, and capital gains realised within the fund. Index-tracking ETFs follow a benchmark such as the S&P/ASX 200 or the All Ordinaries, passing through the income generated by their underlying holdings. Because minimal active management is involved, index ETFs typically carry lower fees than actively managed alternatives.

Bonds and bond ETFs generate income through periodic coupon payments. An investor buying a bond is effectively lending capital to a government or corporation in exchange for regular interest and the return of principal at maturity. Bond ETFs hold portfolios of bonds but do not have a fixed maturity date. This is an important distinction: unit prices in bond ETFs fluctuate with interest rates, which can surprise beginners who expect term-deposit-like stability.

Cash instruments, including high-interest savings accounts, term deposits, and cash management accounts, offer the most predictable income stream. Returns are typically the lowest of the four categories, but capital risk is minimal.

| Instrument Type | How Income Is Generated | Income Predictability | Typical Access Method |

|---|---|---|---|

| Dividend-paying shares | Profit-sharing payments (dividends), often franked | Medium | ASX via broker |

| Income ETFs / managed funds | Dividends, interest, and capital gains from underlying holdings | Medium | ASX (ETFs) or fund manager (managed funds) |

| Bonds / bond ETFs | Periodic coupon payments; principal returned at maturity (direct bonds only) | Medium-High | ASX (bond ETFs) or OTC market (direct bonds) |

| Cash instruments | Interest on deposits | High | Bank or platform directly |

What Australian income investors are actually earning right now

Abstract instrument definitions only go so far. Concrete yield numbers are what allow beginners to calibrate expectations against reality. The figures below are historical snapshots tied to specific past dates; they are not current live rates and are subject to change.

According to VanEck Australia (February 2024), the S&P/ASX 200 delivered a gross dividend yield of approximately 4%, compared with approximately 1.5% for the US market at the same time. That gap is a structural feature of the Australian market, not an anomaly.

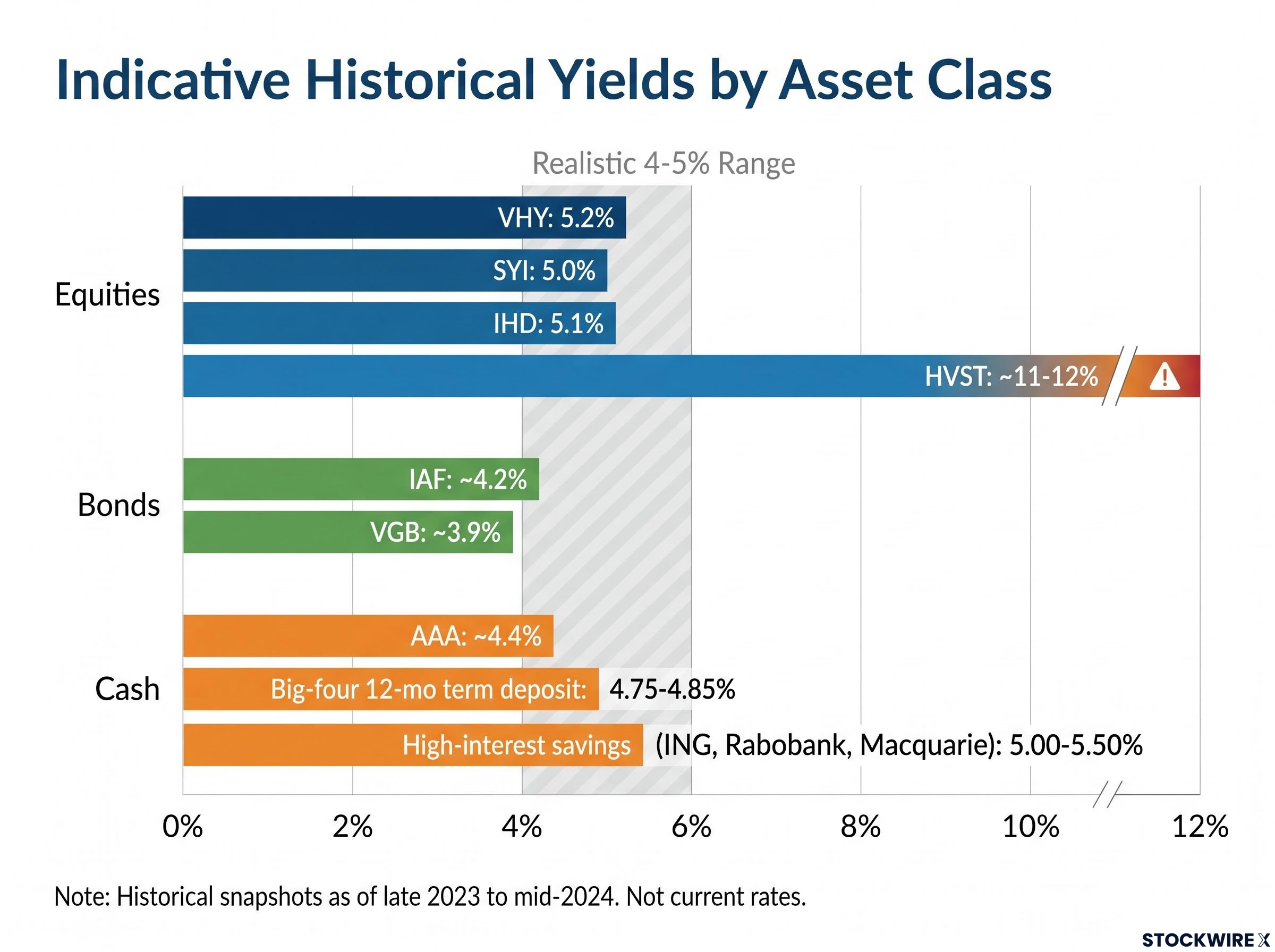

Equity income ETFs offered trailing 12-month distribution yields in the 5.0-5.2% range as at 29 February 2024, according to Morningstar Australia (March 2024). VHY (Vanguard Australian Shares High Yield ETF) yielded 5.2%, SYI (SPDR S&P/ASX 200 Dividend ETF) yielded 5.0%, and IHD (iShares S&P/ASX Dividend Opportunities ETF) yielded 5.1%.

With ASX dividend ETFs compared across index methodology, management cost, franking levels, and five-year total return, the performance gap between top and bottom performers in the same category reached 30 percentage points over the year to March 2026, which illustrates why selecting the lowest-cost option within a category is not the same as selecting the best-performing one.

On the fixed-income side, IAF (iShares Core Composite Bond ETF) carried a running yield of approximately 4.2% as at 31 December 2023, while VGB (Vanguard Australian Government Bond Index ETF) showed a yield to maturity of approximately 3.9% at the same date, according to Morningstar Australia (January 2024). BetaShares‘ AAA cash ETF delivered a 12-month net distribution yield of approximately 4.4% as at April 2024, as reported by the Australian Financial Review (May 2024).

Cash instruments were competitive during this period. High-interest savings accounts from ING, Rabobank, and Macquarie offered headline rates between 5.00% and 5.50% p.a. as at mid-2024, mostly with bonus conditions attached, according to RateCity (June 2024). Big-four bank 12-month term deposits ranged from 4.75% to 4.85% p.a. as at July 2024, per RateCity.

At the other end of the spectrum, the BetaShares Australian Dividend Harvester Fund (HVST) showed a 12-month net distribution yield of approximately 11-12% as at March 2024. That headline figure demands context: HVST uses options overlays and dividend-harvesting strategies that produce significant capital volatility and distribution variability. The Australian Financial Review (April 2024) described it as unsuitable as a core income holding for beginners.

| Instrument / Product | Indicative Yield (as at date noted) | Asset Class | Risk Level |

|---|---|---|---|

| VHY (equity income ETF) | 5.2% (29 Feb 2024) | Australian equities | Medium-High |

| SYI (equity income ETF) | 5.0% (29 Feb 2024) | Australian equities | Medium-High |

| IHD (equity income ETF) | 5.1% (29 Feb 2024) | Australian equities | Medium-High |

| IAF (bond ETF) | ~4.2% (31 Dec 2023) | Australian bonds | Medium |

| VGB (government bond ETF) | ~3.9% (31 Dec 2023) | Government bonds | Low-Medium |

| AAA (cash ETF) | ~4.4% (Apr 2024) | Cash / deposits | Low |

| Big-four 12-month term deposit | 4.75-4.85% (Jul 2024) | Cash | Low |

| High-interest savings (ING, Rabobank, Macquarie) | 5.00-5.50% (mid-2024, conditions apply) | Cash | Low |

| HVST (dividend harvester) | ~11-12% (Mar 2024) | Australian equities (options overlay) | High |

All figures are historical snapshots tied to specific past dates and are not current. Yields change over time; bonus conditions commonly apply to savings accounts.

The takeaway is practical. A diversified income portfolio across equities, bonds, and cash could realistically have generated income in the 4-5% range from Australian instruments during this period, without reaching for high-risk products.

The risks income investors overlook: yield traps, rate sensitivity, and concentration

The highest-yielding option in every income category carries trade-offs that beginners are least equipped to absorb. Understanding these risks before deploying capital is more valuable than any specific product recommendation.

A yield trap occurs when a product’s headline income figure masks capital erosion underneath. HVST is the clearest example: its 11-12% distribution yield as at March 2024 was generated through options overlays and dividend-harvesting strategies that produced large capital drawdowns and unstable distributions over time. The logic extends to any product where income is partially funded by return of capital rather than genuine earnings. Morningstar’s income ETF checklist (June 2024) advises investors to verify that income is not funded by return of capital.

Dividend traps on the ASX are most common among companies where payout ratios already exceed 70-75% of earnings, leaving almost no buffer when revenues soften, and where franking credits subtly encourage investors to hold positions longer than fundamentals support, a dynamic that is particularly acute in banking and resources sectors.

Concentration risk is a subtler problem. High-yield equity ETFs such as VHY, SYI, and IHD carry heavy tilts toward financials and materials. A banking credit event or commodity price collapse would disproportionately affect these portfolios. BHP and Rio Tinto remain among the ASX’s largest dividend payers, but resource company payouts fall sharply when commodity prices soften, making resource income unreliable as a predictable stream.

ASIC’s Moneysmart guidance cautions investors against choosing investments solely because they offer high income; total return and risk-tolerance matching should come first.

Before selecting any income product, assess these five risk categories:

- Yield sustainability: Is the income funded by genuine earnings or by return of capital?

- Capital volatility: How much can the unit price or share price fall while income is being paid?

- Sector concentration: Is the portfolio heavily tilted toward one or two sectors?

- Interest-rate sensitivity: Will rising rates erode the value of the underlying holdings?

- Reinvestment risk: When a term deposit or bond matures, will future rates be lower?

Bond and interest-rate risk

The inverse relationship between interest rates and bond prices catches many beginners off guard. When interest rates rise, existing bonds become less attractive because newly issued bonds offer better coupon rates. The price of existing bonds falls to compensate. For an investor holding a direct bond to maturity, this price movement is largely academic: they still receive their coupons and their principal back at maturity.

Bond ETFs work differently. They do not mature. The fund continuously buys and sells bonds, so there is no fixed date at which an investor automatically receives face value back. Unit price risk persists for as long as the investment is held. The ASX’s investor education guidance (May 2024) notes that longer-duration bond ETFs are more sensitive to rate changes, making them more volatile when rates move quickly. Morningstar (January 2024) warned that investors focused purely on yield may overlook interest-rate risk and credit risk, especially in high-yield bond ETFs.

For cash instruments, the risk runs in the opposite direction. When a term deposit matures, future rates may be lower, reducing forward income even when the original deposit felt secure. This reinvestment risk is easy to ignore when rates are high but becomes apparent over longer timeframes.

Building your income portfolio: mixing assets, managing reinvestment, and setting realistic expectations

Risk awareness converts into practical value only when it shapes portfolio construction. The good news is that a simple, diversified income portfolio does not require expertise. It does require intentional asset mixing.

The principle is straightforward: combining equities, bonds or bond ETFs, and cash instruments reduces reliance on any single sector or instrument. Morningstar (June 2024) recommends a mix of income sources for precisely this reason. A banking downturn that cuts dividend income does not affect term deposit interest. A rate rise that pushes bond ETF unit prices lower simultaneously improves yields on new savings accounts and term deposits.

How to weight the mix depends on the investor’s income timeline. A retiree drawing income today tolerates less capital volatility and may weight more heavily toward cash and short-duration bonds. A younger investor building toward future income can accept more equity exposure and use dividend reinvestment plans (DRPs) to compound the capital base over time before switching to drawdown. The ASX’s investor education resources note that DRPs allow investors to reinvest dividends automatically, building holdings without additional capital outlays.

Fees matter more than beginners expect. A 0.5% annual management fee meaningfully erodes income from a 4-5% yielding portfolio over time. Morningstar’s income ETF checklist (June 2024) advises comparing yields net of fees, checking payout sustainability, reviewing diversification, and assessing sector tilts before selecting any product.

A practical starting framework (without prescribing specific products) might combine a broad Australian dividend ETF, a diversified bond ETF, and a high-interest savings account or term deposit, weighted toward the investor’s risk tolerance and income timeline.

- Define the income goal and timeline: How much income is needed, and when does it need to start?

- Select instruments across at least two asset classes: Equities plus bonds, or equities plus cash, at minimum

- Check yields net of fees: A 5% gross yield with a 0.5% fee is a 4.5% net yield

- Verify income sustainability: Confirm that distributions are funded by genuine earnings, not return of capital

- Review concentration risk in equity holdings: Check sector tilts, particularly toward financials and resources

ASIC advises investors to read the Product Disclosure Statement (PDS) and target market determination carefully before investing in any ETF marketed as “high yield” or “income,” as these products may take more risk through sector concentration or lower-quality bonds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Australian income investing has structural advantages worth using deliberately

Australia offers income investors several features that most global markets do not.

Franking credits are the most distinctive. When an ASX-listed company pays tax on its profits and distributes a franked dividend, eligible investors receive an imputation credit that can reduce or eliminate the tax payable on that dividend income. A gross yield of 4-5% on franked dividends becomes even more valuable on an after-tax basis for many Australian resident investors. The ASX’s investor education resources note that the tax treatment of franking credits varies by investor; those with complex circumstances should seek financial advice.

The ATO guidance on franking credit refunds confirms that eligible Australian resident investors can receive a cash refund for excess imputation credits where the credit amount exceeds their total tax liability, a feature that materially increases the after-tax value of franked dividends for low-to-middle income earners.

The high-payout culture reinforces the yield advantage. According to VanEck Australia (February 2024), many Australian companies distribute 60-80% of earnings as dividends, particularly in banking and resources. This structural preference for shareholder distributions, rather than share buybacks or reinvestment, is one reason the ASX 200’s gross yield of approximately 4% roughly doubles the US market’s 1.5%.

The combination of these features creates a toolkit that allows Australian beginners to construct diversified income portfolios without needing sophisticated instruments:

- High payout culture: Many ASX companies distribute the majority of earnings as dividends

- Franking credits: Tax-effective income for eligible Australian resident investors

- Competitive cash rate environment: Savings accounts and term deposits offered yields above 4.5% through mid-2024

- Accessible ASX-listed income instruments: Diversified dividend ETFs, bond ETFs, and cash ETFs are available through any standard broker account

Individual tax outcomes from franking credits depend on the investor’s marginal tax rate and circumstances. The structural advantage is real, but it is only fully captured with an understanding of how personal tax situations interact with franked income.

The income investor’s edge is patience, diversification, and discipline over yield-chasing

Passive income investing in Australia offers genuine structural advantages. Franking credits, a high-payout corporate culture, competitive cash rates, and accessible ASX-listed instruments create an environment that rewards income-focused strategies more than most global markets do. Those advantages are only accessible, however, to investors who diversify across asset classes, assess risks beyond headline yield, and match their income strategy to their actual timeline and risk tolerance.

For beginners, a practical hierarchy from lowest to highest risk provides a starting point:

- Cash instruments and term deposits: Highest capital security, lowest yield, reinvestment risk acknowledged

- Diversified bond ETFs: Moderate income with interest-rate sensitivity and no fixed maturity

- Broad dividend ETFs: Higher potential income with equity risk, sector concentration, and dividend cyclicality accepted

The next step is not selecting a product. The next step is defining an income goal: how much income, over what timeframe, and with how much capital volatility is acceptable. Match that goal to an instrument mix rather than selecting instruments based on headline yield alone.

Investors who have defined their income goal and timeline and want to work backward to a specific capital target will find our full explainer on living off dividends in Australia useful, covering the ASFA comfortable retirement benchmarks, how franking credits reduce the capital required at different yield assumptions, and the superannuation asset location strategy that maximises after-tax income in retirement.

ASIC’s Moneysmart website and the ASX’s investor education resources are free, regulator-backed starting points for further research before committing capital.