The Smartphone Market Paradox: Volume Falls, Value Climbs

2 hrs ago

On 2 June 2026, a single comment from Nvidia CEO Jensen Huang sent one AI semiconductor stock up nearly 30% while a separate supply announcement pushed memory names in the opposite direction, all within the same trading session. The split was not random volatility. It was a compressed, real-time illustration of a structural divide running through the AI semiconductor sector: custom silicon and networking chips on one side, commodity memory on the other. Understanding what drove each move is increasingly necessary for investors attempting to read AI-driven demand signals without conflating very different business dynamics. This analysis unpacks the mechanics behind both moves, explains the underlying structural divergence between AI-custom and commodity-memory chip markets, and identifies what each signal means for investors tracking the sector.

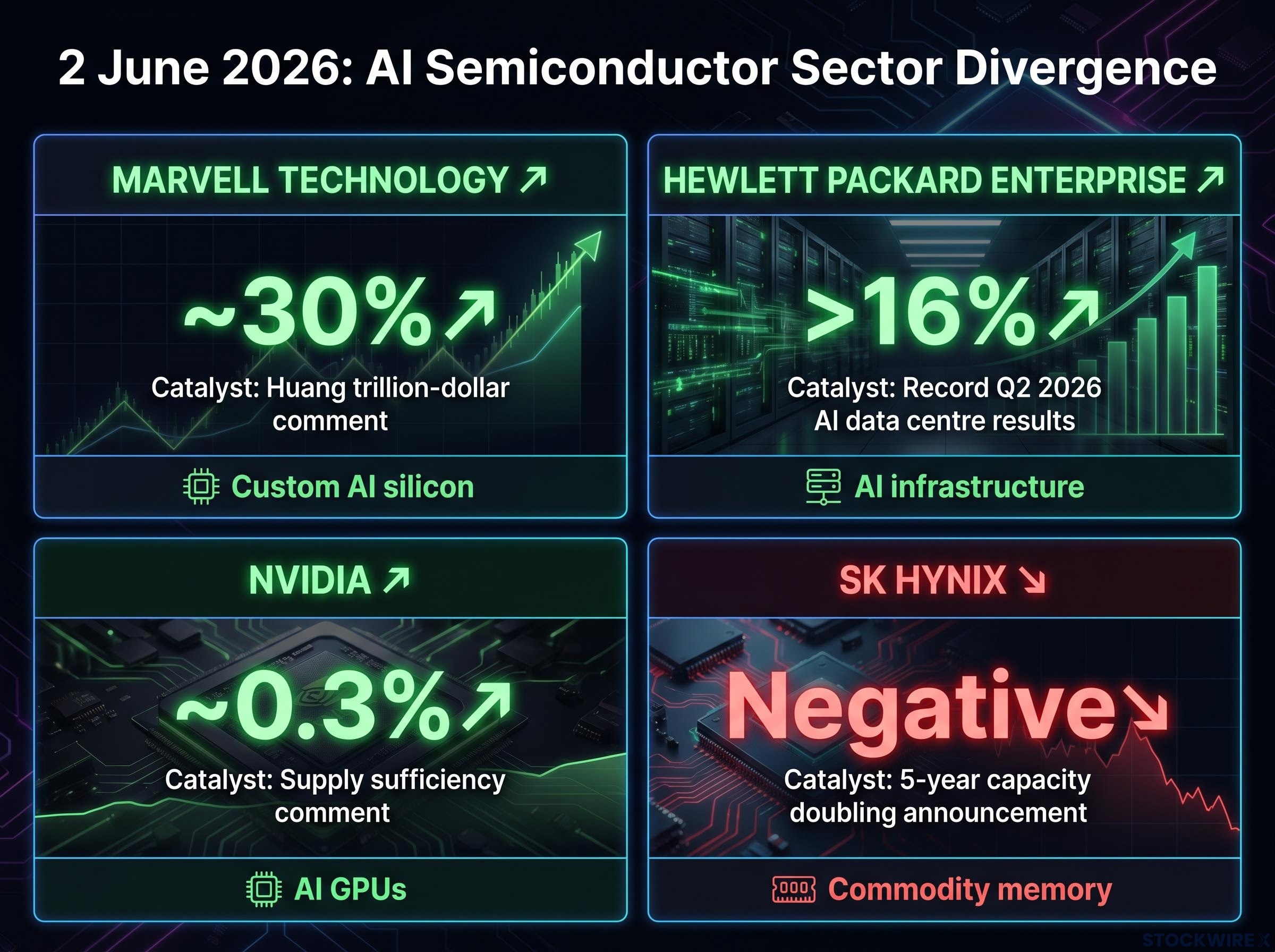

Marvell Technology surged approximately 30% on 2 June 2026, adding tens of billions of dollars to a market capitalisation that stood at just under $192 billion before the session opened. The catalyst was specific: Jensen Huang publicly identified Marvell as a potential future trillion-dollar company. Nvidia itself gained approximately 0.3% on the same day, a muted move that underscores how targeted the Marvell repricing was. This was not a broad sector rally.

On the opposite side of the ledger, SK Hynix disclosed plans to double its memory manufacturing capacity over a five-year horizon. Memory sector equities moved lower as investors weighed the implications of that supply expansion for future pricing.

A third signal reinforced the day’s constructive AI infrastructure narrative. Hewlett Packard Enterprise shares gained more than 16% after the company reported record second-quarter results, with AI data centre demand cited as the primary driver. HPE also accelerated its long-term financial targets by two years.

Three catalysts defined the session:

| Company | Single-Day Move | Catalyst | Sector Sub-Category |

|---|---|---|---|

| Marvell Technology | ~30% | Huang trillion-dollar comment | Custom AI silicon / networking |

| Nvidia | ~0.3% | Supply sufficiency comment | AI GPUs / accelerators |

| SK Hynix | Negative | Capacity doubling announcement | Commodity memory (DRAM/NAND) |

| Hewlett Packard Enterprise | >16% | Record Q2 2026 AI data centre results | AI infrastructure / systems |

Investors who treat “semiconductor stocks” as a monolithic category would have been whipsawed by this session. The divergence between a 30% surge and a negative drift within the same sector, on the same day, is the story.

Huang did not issue a price target or a formal partnership announcement. He identified Marvell as a company with the potential to reach a trillion-dollar valuation. Michael O’Rourke, Chief Market Strategist at Jones Trading, flagged the comment as the direct catalyst for the session’s outsized move, as reported by Investing.com on 2 June 2026.

Jensen Huang characterised Marvell Technology as a potential future trillion-dollar company, according to reporting by Investing.com on 2 June 2026. With Marvell’s pre-surge market capitalisation at just under $192 billion, the implied gap to that valuation represents an approximately 5x move from the prior close.

The comment carries a specific analytical tension. Huang is not a disinterested observer. He runs the company whose GPUs and accelerators sit at the centre of the AI infrastructure build-out, and Marvell designs custom silicon and networking chips that plug into that same ecosystem. His endorsement is simultaneously self-interested (a stronger Marvell ecosystem benefits Nvidia’s platform) and structurally informed (few people have better visibility into the AI supply chain’s trajectory).

Nvidia’s platform valuation, which analysts at Goldman Sachs and Morgan Stanley now decompose across GPU silicon, networking, systems, and software revenue layers, is precisely what gives Huang’s public commentary about ecosystem partners the structural weight it carries; a CEO endorsing a networking chip partner is simultaneously describing the health of his own platform’s interdependencies.

Huang also stated on the same day that Nvidia has sufficient supply to meet rapidly expanding AI CPU and GPU demand. That second comment matters because it signals ecosystem-level confidence, not just a stock tip. If Nvidia’s supply constraints were worsening, Huang’s optimism about a networking chip partner reaching a trillion dollars would carry less weight.

CEO endorsements from ecosystem partners carry a different analytical weight than analyst upgrades. The market’s 30% response reflected that distinction.

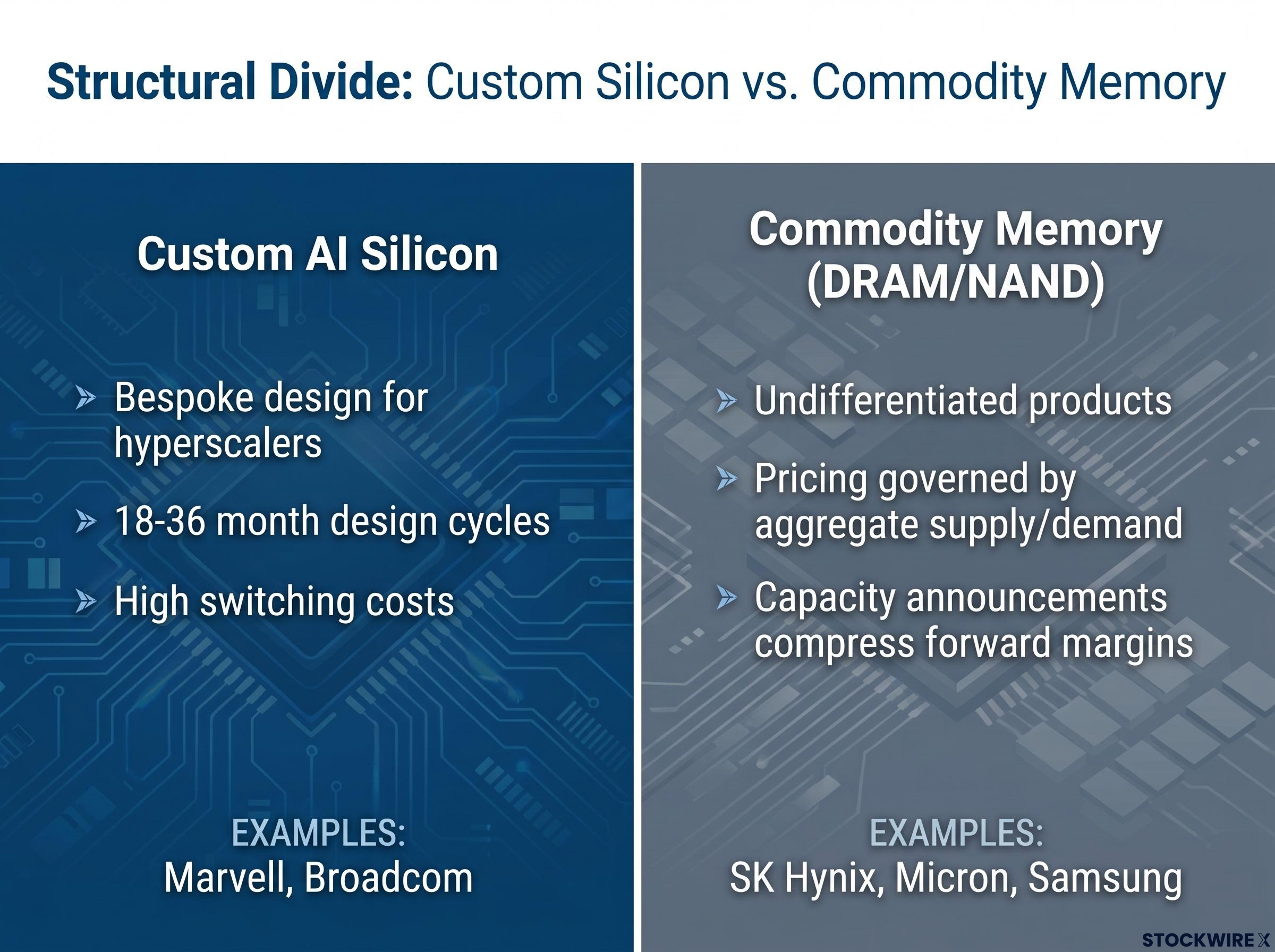

Custom AI silicon refers to application-specific integrated circuits (ASICs) and networking chips designed for a particular customer’s workload, rather than sold as general-purpose products into the open market. Companies like Marvell and Broadcom design bespoke chips in deep collaboration with hyperscale cloud operators. The resulting product is tailored to a specific data centre architecture and cannot be swapped in for a competitor’s design without significant re-engineering.

Commodity memory, by contrast, is undifferentiated. A DRAM module from SK Hynix performs the same function as one from Micron or Samsung. Pricing in commodity memory markets is set by aggregate supply and demand across fungible products, which means any announcement of significant capacity expansion is an immediate forward pricing signal.

Key structural characteristics distinguish the two:

Custom AI silicon:

Commodity memory:

The stickiness of custom silicon demand is structural, not sentimental. A hyperscaler that has co-designed a chip with Marvell cannot switch to a competitor without years of re-engineering work. That integration depth creates a moat that commodity memory producers do not enjoy.

AMD’s Q1 2026 results illustrate the broader demand picture. The company reported revenue of $10.3 billion, with data centre and AI infrastructure cited as the primary growth driver. AMD’s Q2 2026 guidance of approximately $11.2 billion (representing approximately 46% year-over-year growth at the midpoint) reflected conviction that inferencing and agentic AI are driving sustained demand for high-performance CPUs and accelerators.

This is the context in which Huang’s endorsement carries weight: he is signalling confidence in the custom silicon ecosystem’s growth trajectory, not merely recommending a stock.

Investors exploring the long-term competitive dynamics of the custom silicon ecosystem will find our dedicated guide to hyperscaler custom silicon programmes, which examines how Alphabet, Amazon, and Microsoft are funding proprietary AI chip development from the same $700 billion capex wave that fills Nvidia’s order book, and what the absence of publicly quantified workload migration data means for evaluating the credibility of the threat.

SK Hynix’s plan to double memory manufacturing capacity over a five-year horizon, announced on 2 June 2026, landed squarely on a well-understood investor concern. In commodity memory markets, supply expansion at this scale raises the probability of future pricing pressure and margin compression. The negative market reaction was not irrational pessimism; it was a direct application of the supply-cycle logic that has governed memory investing for decades.

The same company supplying AI infrastructure’s most constrained component, high-bandwidth memory, is simultaneously expanding conventional memory capacity at a scale that concerns the market. That tension sits at the centre of any memory investment thesis in the current AI cycle.

The distinction between high-bandwidth memory (HBM) and conventional DRAM and NAND matters here. HBM, the specialised memory stacked directly onto AI accelerator packages, has remained structurally tight through 2025 and into 2026. US coverage has repeatedly characterised HBM scarcity as a constraint on AI server shipments, supporting strong pricing power for producers like SK Hynix and Micron.

HBM production is technically distinct from conventional DRAM manufacturing and is unlikely to represent the primary target of the capacity doubling. The advanced packaging and stacking processes required for HBM limit how quickly capacity can be expanded, and the customer base (primarily Nvidia and AMD) is concentrated.

Conventional DRAM and NAND, however, face traditional supply-cycle dynamics. When a major producer signals a doubling of capacity, the market prices in the forward risk of oversupply, regardless of how strong near-term demand appears.

For investors wanting to understand why this cycle may be structurally resistant to the usual supply-expansion playbook, our full explainer on the memory chip supercycle examines how hyperscaler multi-year supply agreements extending through 2028-2030 and a near-term manufacturing supply vacuum are creating conditions that have historically not coincided with conventional capacity-driven margin compression.

The investor takeaway is that position within memory matters more than sector-level exposure. An allocation to SK Hynix based on its HBM relationship with Nvidia carries a fundamentally different risk profile from broad memory sector exposure that absorbs the conventional DRAM and NAND supply overhang.

Two additional data points from the same period reinforce the breadth of the AI infrastructure demand cycle, reducing the risk that Marvell’s 30% move was purely sentiment-driven.

These are independent data points from different parts of the AI supply chain, a systems vendor and a chip designer, both showing accelerating AI-driven demand within weeks of each other. The convergence provides corroborating evidence that the AI infrastructure spending cycle is broad and durable.

The divergence on 2 June 2026 was not an anomaly. It was a compressed demonstration of a structural split that has been building through 2025 and into 2026: custom AI silicon and networking chips are being re-rated upward on ecosystem endorsement and structural demand, while commodity memory stocks are being judged on supply-cycle logic regardless of near-term AI demand strength.

IDC’s semiconductor market forecast projects the sector will exceed $1 trillion by 2026, with hyperscaler capital expenditure on AI infrastructure identified as the primary structural driver, a macro backdrop that contextualises why custom silicon valuations are being re-rated at the speed the Marvell session illustrated.

The practical implication is that sector-level exposure to AI semiconductor names is insufficient. Sub-sector positioning determines whether an investor captures the custom silicon re-rating or absorbs the memory supply overhang.

Custom AI silicon exposure:

Commodity memory exposure:

Marvell’s 30% single-day move on a CEO comment illustrates how quickly custom silicon names can reprice on narrative. That velocity creates both opportunity and risk. Investors positioned in this sub-sector benefit from the upside repricing but remain exposed to the same dynamic in reverse if ecosystem sentiment shifts.

The memory sector repricing argument gains additional texture from NAND dynamics: SanDisk reported 78.4% non-GAAP gross margins in Q3 2026 as AI data centres absorbed approximately 70% of high-end NAND production under multi-year hyperscaler contracts, a data point that sits in structural tension with the conventional supply-cycle logic that the SK Hynix capacity announcement reactivated.

The events of 2 June 2026 demonstrated in a single session what has been building across the sector for more than a year. Custom silicon and commodity memory are not the same trade, and treating them as interchangeable produces a portfolio that absorbs contradictory forces simultaneously.

As AI infrastructure spending accelerates, the gap between custom-silicon pricing power and commodity memory cycle risk is likely to persist as a defining feature of the sector. The framework for navigating it is not complex: identify where in the AI supply chain a given company sits, understand what supply and demand dynamics govern its specific segment, and evaluate whether an endorsement, earnings report, or capacity announcement is a signal for that segment or noise from an adjacent one.

The session rewarded that distinction. Future sessions are likely to do the same.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Custom AI silicon chips are application-specific integrated circuits designed for a particular hyperscaler customer's workload, featuring high switching costs and long design cycles of 18-36 months. Commodity memory products like DRAM and NAND are undifferentiated, meaning pricing is governed by aggregate supply and demand rather than customer-specific relationships.

Marvell Technology surged approximately 30% after Nvidia CEO Jensen Huang publicly identified Marvell as a potential future trillion-dollar company, a comment reported by Investing.com. With Marvell's pre-surge market capitalisation at just under $192 billion, the implied gap to a trillion-dollar valuation represented roughly a 5x move from the prior close.

In commodity memory markets, capacity expansion announcements directly compress forward margin expectations because the products are undifferentiated and pricing is set by aggregate supply and demand. Investors applied well-established supply-cycle logic, pricing in the forward risk of oversupply regardless of near-term AI demand strength.

High-bandwidth memory (HBM) is a specialised memory type stacked directly onto AI accelerator packages, and it has remained structurally tight through 2025 and into 2026 due to technically demanding production requirements and a concentrated customer base of primarily Nvidia and AMD. HBM carries a fundamentally different risk profile from conventional DRAM and NAND, meaning an investor's position within memory matters more than broad sector-level exposure.

AMD reported Q1 2026 revenue of $10.3 billion with Q2 guidance of approximately $11.2 billion (around 46% year-over-year growth), citing inferencing and agentic AI as primary drivers, while HPE posted record Q2 2026 results driven by AI data centre demand and accelerated its long-term financial targets by two years. These independent data points from different parts of the AI supply chain provide corroborating evidence that AI infrastructure spending is broad and durable.