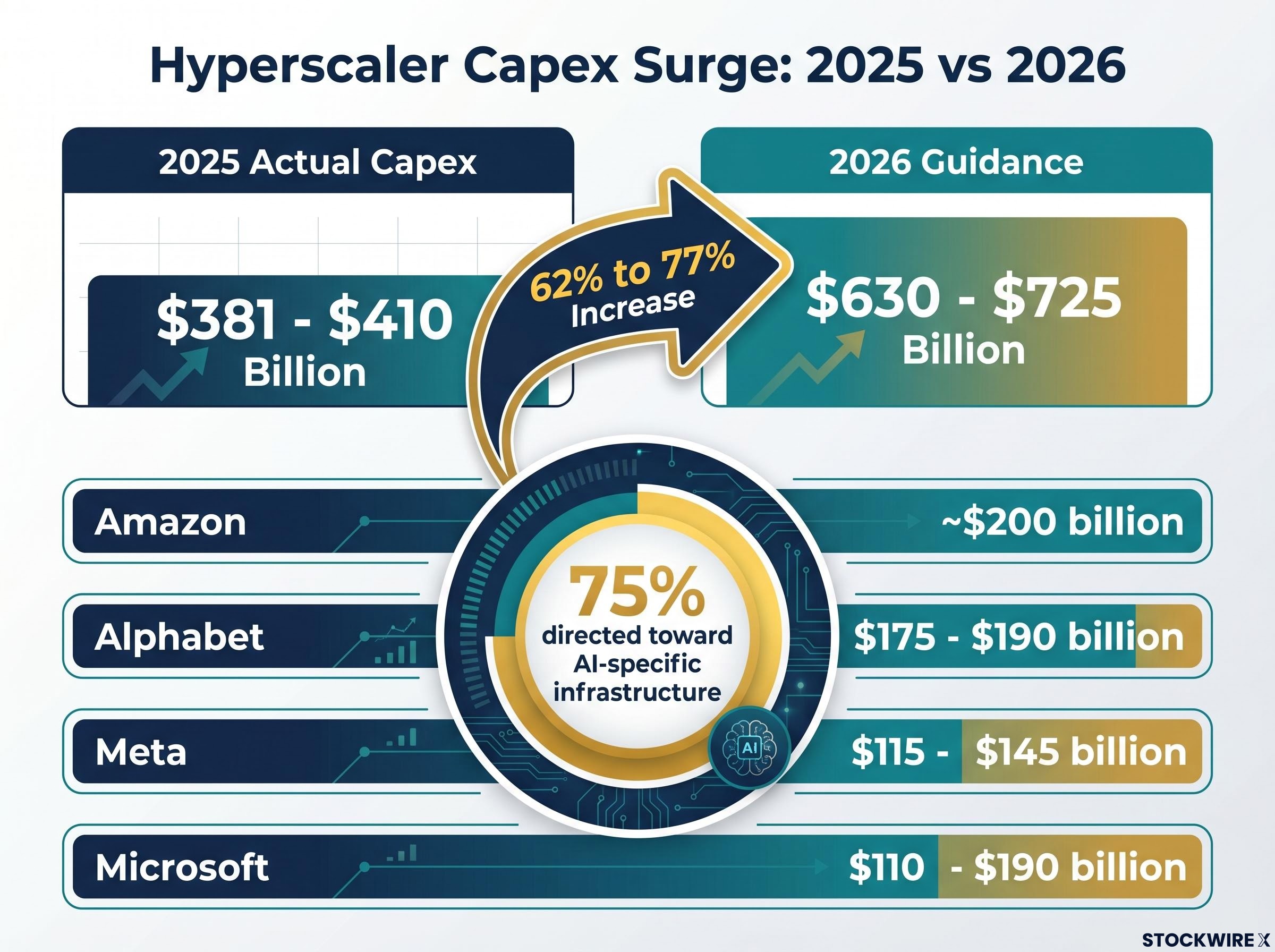

The four largest US hyperscalers are on track to spend a combined $630 to $725 billion on AI infrastructure in 2026 alone, a figure that exceeds the GDP of most countries. The spending is not speculative posturing. It is being pulled by a structural shift in how artificial intelligence is consumed: from simple chatbot exchanges toward always-on autonomous agents that require orders of magnitude more compute per session. For investors evaluating AI supply chain investing opportunities, the question is no longer whether the spend is real, but which parts of the supply chain are capturing the resulting profits. This analysis maps the token consumption escalation to its financial consequences across the AI value chain, identifying where earnings growth is genuinely concentrated and where valuation compression signals risk.

Escalating Token Consumption: The Shift from Conversational to Autonomous AI

A single conversational AI exchange, the kind most users are familiar with, consumes roughly 1,000 tokens. That figure is the baseline. A multi-step agentic workflow, where an AI system plans, executes, and iterates across a complex task, requires approximately 10,000 tokens per task. An always-on autonomous agent operating continuously can consume in the range of 100,000 tokens during sustained operation.

The gap between the first tier and the third is not incremental. It is a 100x multiplier in compute demand per session, according to Cameron Gleason of BetaShares.

The architectural shift driving this demand curve is already visible in procurement data: agentic AI workloads favour CPU architecture over GPUs for sequential reasoning and agent orchestration tasks, with industry estimates placing 35-45% of inference workloads as CPU-bound, a distribution that was not anticipated in earlier AI infrastructure planning cycles.

| Workflow Tier | Token Consumption (Approx.) | Relative Compute Demand |

|---|---|---|

| Conversational AI exchange | ~1,000 tokens | 1x (baseline) |

| Multi-step agentic workflow | ~10,000 tokens per task | 10x |

| Always-on autonomous agent | ~100,000 tokens (continuous) | 100x |

Why constrained supply at this moment matters

Compute capacity expansion operates on multi-year build cycles. New data centres take years to plan, permit, and commission. Demand escalation across the token tiers is happening now, with enterprises already deploying multi-step agentic workflows at scale and autonomous agent architectures entering production environments. The mismatch between rapidly compounding demand and physically constrained supply is the structural condition underpinning current hardware pricing power, and it is unlikely to resolve within a single capital expenditure cycle.

When big ASX news breaks, our subscribers know first

What $630 billion in annual capex actually buys

The combined 2026 capital expenditure guidance from Amazon, Alphabet, Meta, and Microsoft sits at $630 to $725 billion. That range represents a 62 to 77% increase over the approximately $381 to $410 billion the four companies spent in 2025, which was itself a record year.

In the first quarter of 2026 alone, the four hyperscalers spent a combined $130.65 billion on capital expenditure, a single-quarter record.

Roughly 75% of this spending is directed toward AI-specific infrastructure: GPUs, AI-optimised servers, networking equipment, and purpose-built data centres. The remaining quarter covers broader cloud and enterprise infrastructure that increasingly serves AI workloads indirectly.

| Hyperscaler | 2025 Actual Capex (Approx.) | 2026 Guidance | YoY Change |

|---|---|---|---|

| Amazon | ~$125 billion | ~$200 billion | +60% |

| Alphabet | Raised multiple times | $175-$190 billion | Significant increase |

| Meta | Prior cycle figure | $115-$145 billion | Significant increase |

| Microsoft | $37.5B in single recent quarter | $110-$190 billion | Significant increase |

These figures translate directly into revenue for the semiconductor, networking, and data centre companies sitting upstream. Understanding the composition of this spend, and the fact that three-quarters flows to AI-specific hardware, clarifies which vendor categories benefit most in the near term.

Tracking Capital Flow: Identifying Key Beneficiaries in the AI Value Chain

The AI supply chain is not a single layer. It is a sequence of value capture points, and the distribution of profits across those points is uneven.

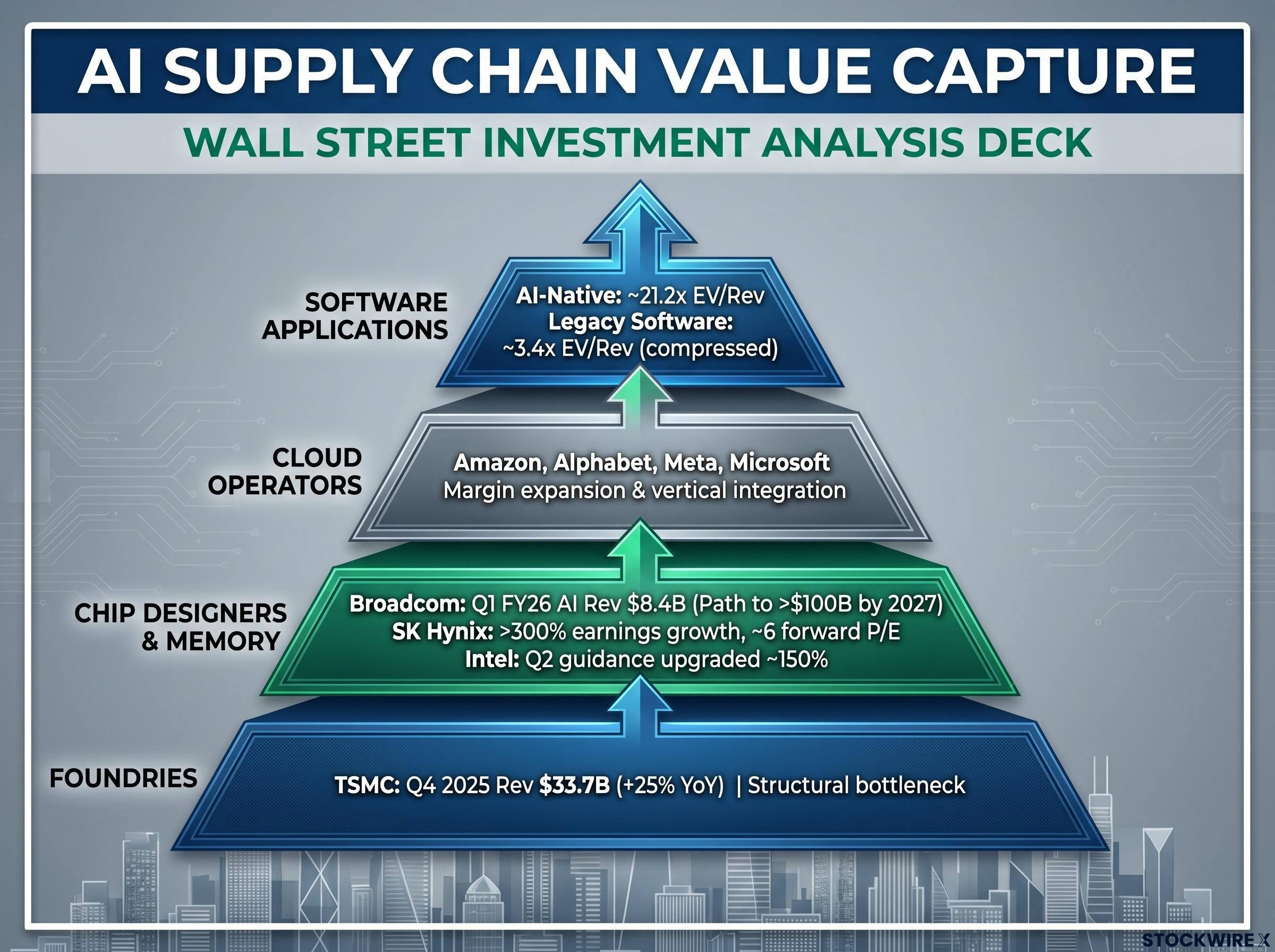

At the top of the chain sit foundries and chip fabricators. TSMC reported Q4 2025 revenue of $33.7 billion, up 25% year on year, driven by AI chip production ramps. Below the foundries, chip designers and memory producers capture the most concentrated earnings growth. SK Hynix, a leading producer of high-bandwidth memory (HBM) used in AI accelerators, has reported earnings growth exceeding 300% for the current year.

SK Hynix has posted earnings growth exceeding 300% this year, yet the company trades at a forward price-to-earnings ratio of approximately 6, a gap between earnings momentum and market valuation that stands out across the semiconductor layer.

Broadcom illustrates the same dynamic at the chip design level. In Q1 FY2026, the company posted total revenue of $19.3 billion (up 29% year on year), with AI semiconductor revenue reaching $8.4 billion, a 106% year-on-year increase. Guidance for Q2 FY2026 came in at approximately $22.0 billion (up 47% year on year), and management has indicated a path toward more than $100 billion in annual AI semiconductor run rate by 2027. Intel upgraded its Q2 earnings guidance by approximately 150% during the current year.

The profit concentration pattern, mapped across the value chain, follows a consistent hierarchy:

- Foundries (TSMC): Retain structural pricing power through fabrication concentration; revenue grows in step with total chip volume

- Chip designers and memory (Broadcom, SK Hynix, Intel): Capture the most concentrated earnings growth from direct AI demand

- Cloud operators (Amazon Web Services, Google Cloud, Azure): Monetise AI through higher-margin workloads and vertical integration via proprietary silicon

- Software applications: Selective strength for AI-native tools, but broader multiple compression for legacy platforms (covered in detail below)

Cloud operators as infrastructure enablers and value capturers

Hyperscalers benefit from AI workload margin expansion while simultaneously pursuing vertical integration through proprietary chip development, which shifts their cost structure over time. Amazon Web Services holds the largest global cloud market share, which contextualises why AWS infrastructure decisions carry outsized weight for upstream suppliers. Each dollar a hyperscaler spends on proprietary silicon still flows through the foundry and memory ecosystem, meaning the semiconductor layer captures revenue regardless of which company designs the chip.

The proprietary chip arms race and what it means for the supply chain

All four hyperscalers are now serious participants in custom silicon development, each with multi-generational roadmaps and production-scale deployments:

- Amazon: Trainium2 deployed at scale (hundreds of thousands of chips); Trainium3 announced with competitive performance claims

- Alphabet (Google): TPU progression through v5p, Trillium (v6), and Ironwood (v7, announced November 2025), with expanded cloud availability

- Microsoft: Maia 200 unveiled in early 2026, claiming up to 3x performance on certain workloads over prior custom accelerators, built on TSMC 3nm with substantial HBM capacity (these performance claims have not been independently verified)

- Meta: Multiple new MTIA generations focused on inference workloads (deployment details not independently confirmed)

The apparent paradox is that these custom chips are designed to reduce reliance on third-party GPUs, yet they depend on the same foundry and memory ecosystem. Every custom ASIC still requires TSMC fabrication. Every AI accelerator, whether designed by Alphabet or Amazon, requires HBM from producers like SK Hynix. Broadcom provides ecosystem components across multiple custom chip programmes.

Anthropic offers a useful illustration. The company maintains partnerships spanning both Amazon Trainium and Google TPU deployments, distributing compute relationships across custom and general-purpose silicon simultaneously. Even the most GPU-intensive AI developers are hedging their infrastructure dependencies.

Each hyperscaler’s custom silicon programmes share a structural paradox: the same capital flowing into Alphabet TPUs and Amazon Trainium is simultaneously sustaining Nvidia’s order book, because no custom ASIC programme has yet disclosed the workload migration metrics that would allow investors to quantify how much third-party GPU demand is actually being displaced.

Why foundry dependency preserves the semiconductor layer’s leverage

Regardless of who designs the chip, fabrication concentration at TSMC means the foundry layer retains structural pricing power. HBM memory integration requirements for both custom and general-purpose AI chips reinforce the position of memory producers. The custom silicon arms race creates selective differentiation among hyperscalers without dismantling the upstream ecosystem they all depend on.

Software’s Mixed Signals: Explaining Valuation Discrepancies

The AI investment narrative has created a sharp divide within software. Legacy horizontal application software, the SaaS platforms that dominated the prior cycle, has experienced significant multiple contraction. According to available market data, application software EV/NTM revenue multiples may have compressed approximately 41% over the trailing twelve months, falling from around 5.8x to 3.4x, compared with a pre-pandemic average of approximately 7.8x (these figures have not been independently verified).

Application software valuation multiples may have compressed by approximately 41% over the trailing twelve months, a contraction that reflects market judgment about where near-term earnings growth is concentrated.

AI-native companies tell a different story. According to available VC round data, AI-native firms may trade at a median 21.2x EV/revenue, compared with approximately 5.5x for legacy SaaS (these figures have not been independently verified). Since late 2022, AI-focused companies have reportedly delivered returns of approximately +513%, while horizontal software has declined (figures not independently verified).

| Category | EV/Revenue Multiple | Earnings Trend | Primary Risk Factor |

|---|---|---|---|

| Legacy horizontal software | ~3.4x (compressed) | Near-term resilience, forward uncertainty | Multiple compression; AI displacement risk |

| AI-native software | ~21.2x (VC rounds) | Rapid growth from low base | Premium sustainability; execution risk |

The compression dynamic is a market judgment about where near-term earnings growth is concentrated, not necessarily a verdict on long-run software value. Legacy software near-term earnings have not yet materially deteriorated, even as multiples contract. For investors holding or evaluating software positions, the ability to separate AI-native platforms from legacy horizontal applications is a material input into positioning decisions.

Strategic Positions: Navigating Profit Concentration for Long-Term Value

The supply chain map, the capex trajectory, and the valuation divergence converge on a pattern. Profit concentration in the AI infrastructure cycle follows the direction of capital flow, and the largest share of that flow reaches the semiconductor and foundry layer before it reaches anyone else.

Three observations, ordered from most upstream to most downstream, orient the current landscape:

- Foundries and memory producers (TSMC, SK Hynix) sit at the structural bottleneck of the supply chain, retaining pricing power regardless of whether hyperscalers design their own chips or purchase third-party accelerators. SK Hynix’s earnings growth exceeding 300% against a forward P/E of approximately 6 highlights the gap between earnings momentum and market valuation in this layer.

- Chip designers and interconnect providers (Broadcom, Intel) capture direct revenue from both general-purpose and custom AI accelerator programmes. Broadcom’s guided path toward more than $100 billion in annual AI semiconductor run rate by 2027 provides a forward earnings signal grounded in committed hyperscaler spend.

- Cloud operators and software platforms capture value further downstream, with cloud margins expanding on AI workloads while legacy software faces multiple compression that may persist until AI monetisation matures.

The combined $630 to $725 billion in 2026 hyperscaler capex guidance represents a demand floor for semiconductor suppliers through at least the medium term. These are committed figures, not aspirational targets.

The forward demand signal investors may be underweighting

Always-on autonomous AI agents represent a demand tier that is early in deployment but already observable in hyperscaler compute planning. The 100,000-token consumption profile per continuous session suggests the current capex cycle is a leading indicator of a demand wave that extends well beyond the 2026 guidance horizon. Infrastructure company valuations may not yet fully reflect this trajectory.

Beyond Current Capex: The Sustained Trajectory of AI Infrastructure

The token consumption escalation from conversational AI to always-on agents is structural and compounding. Each tier multiplies compute demand, and enterprise adoption of agentic workflows is accelerating rather than plateauing. The infrastructure layer’s earnings tailwind is tied to this adoption trajectory, not a one-time upgrade cycle.

Risks remain visible. Hyperscaler proprietary chips could gradually erode portions of third-party semiconductor revenue over multiple generations. Software valuations may recover as AI monetisation pathways mature and legacy platforms integrate agentic capabilities. Neither outcome is assured, and both operate on longer timeframes than the current earnings cycle.

The capex-to-revenue lag running at 18-24 months across the semiconductor stack is the central counterweight to the earnings momentum case: Morningstar analyst Dennis Li has identified this lag as the primary structural risk, and Gartner estimates that only 20% of current AI agent pilots are scalable to production by 2027, meaning the demand floor implied by committed hyperscaler spend is not the same as guaranteed revenue realisation for every supplier in the chain.

The current evidence points to profit concentration in the semiconductor and foundry layer, with the custom silicon arms race creating selective differentiation rather than wholesale disruption to the upstream ecosystem. For investors mapping the AI supply chain, the infrastructure buildout is where earnings growth is verifiable today.

For investors wanting to translate the supply chain profit map into concrete portfolio construction decisions, our dedicated guide to building an AI investment framework walks through the three-tier structure of hardware, cloud platform, and pure-play software positions, including the specific risk profiles, position sizing logic, and institutional consensus from J.P. Morgan, BlackRock, and Goldman Sachs on where each tier belongs in a portfolio.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—