Why Harvest’s MicroStrategy ETF Is Down 90% but Still Running

27 mins ago

Global corporate AI investment reached $581.7 billion in 2025, according to the Stanford AI Index, yet most retail investors still cannot articulate why they would own NVIDIA instead of Microsoft, or Palantir instead of either. The AI investment universe has expanded so rapidly that naming individual stocks has outpaced any framework for understanding what each stock actually represents. Three structurally distinct tiers have emerged within the AI value chain: hardware, cloud platforms, and pure-play software. Each carries a different revenue driver, volatility profile, and portfolio role. This guide builds the framework for evaluating AI investment strategy across all three layers, covering which names represent each tier, how each behaves under market stress, and how to match the right tier to the right part of a portfolio. By the end, the reader will have a concrete mental model for evaluating any AI stock, not just the five covered here.

Most investors approach AI with a list of tickers and no structure. NVIDIA, Broadcom, Microsoft, Alphabet, Palantir: all labelled “AI stocks,” all behaving very differently under the same market conditions. The confusion is understandable, but it is also solvable.

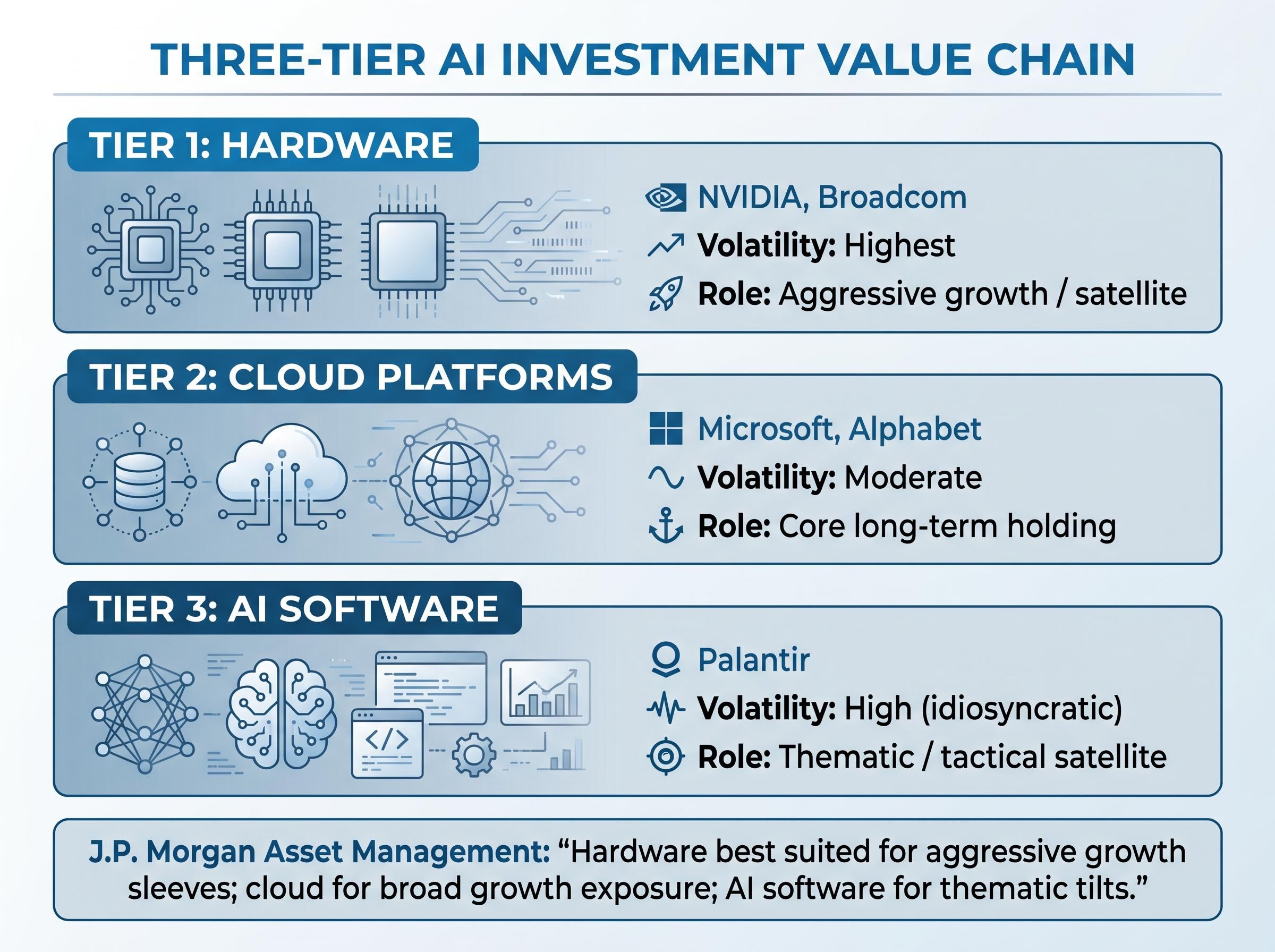

AI investment is not a monolithic category. It is a supply chain with upstream, midstream, and downstream participants, each capturing value at a different point and with a different rhythm. The three tiers break down as follows:

This is not a proprietary framework. Morgan Stanley’s “Three Layers of AI Exposure,” Goldman Sachs’ “AI Stack” categorisation, and research from BlackRock and J.P. Morgan Asset Management all independently converge on the same three-tier structure, with remarkably similar characterisations of each layer’s risk and return profile.

J.P. Morgan Asset Management’s allocation guidance is direct: “Hardware best suited for aggressive growth sleeves; cloud for broad growth exposure; AI software for thematic tilts.”

Without this structural map, investors risk conflating very different risk profiles under a single “AI trade.” The rest of this guide builds on this architecture, tier by tier.

The numbers make the case before any analyst commentary does. NVIDIA reported full-year fiscal 2026 total revenue of $215.9 billion, up 65% year-over-year, with data centre revenue accounting for $193.7 billion of that total. In Q1 fiscal 2027 (quarter ended April 2026), data centre revenue reached $75.2 billion, a 92% year-over-year increase.

The NVIDIA fiscal 2026 earnings release confirmed full-year revenue of $215.9 billion, up 65% year-over-year, with data centre revenue of $193.7 billion representing the clearest single-company illustration of how directly hardware names convert AI capital expenditure into recognised revenue.

That trajectory has made NVIDIA the primary beneficiary of the AI infrastructure build-out. Goldman Sachs characterises the company as carrying the “highest operating leverage to AI spending,” with returns strongest during the 2024-2026 build-out phase but expected to normalise as supply catches demand. Morgan Stanley has flagged the same opportunity while noting structural risks: competition from AMD, custom application-specific integrated circuit (ASIC) development by hyperscalers, and revenue concentration among a small number of large cloud buyers.

Broadcom offers a different entry point to the same tier. In Q1 fiscal 2026, AI semiconductor revenue reached $8.4 billion, up 106% year-over-year. Q2 fiscal 2026 guidance of $10.7 billion in AI semiconductor revenue signals sustained momentum.

The structural difference is visibility. Broadcom’s revenue is anchored in longer-term custom ASIC and data centre networking contracts with hyperscalers, providing more forward revenue certainty than spot GPU sales. That contract structure makes Broadcom a somewhat lower-volatility hardware alternative, though it remains firmly within the highest-beta tier.

| Company | Most Recent AI/Data Centre Revenue | YoY Growth | Key Risk Factor |

|---|---|---|---|

| NVIDIA | $75.2B (Q1 FY2027 data centre) | 92% | AMD competition, custom ASICs, hyperscaler customer concentration |

| Broadcom | $8.4B (Q1 FY2026 AI semiconductor) | 106% | Dependence on hyperscaler contract renewals |

Hardware is where the largest absolute dollar gains in AI have been generated, but also where drawdown risk is highest. Investors allocating here are buying into the capex cycle, not a recurring-revenue business. That distinction matters when the cycle turns.

A common misconception runs through retail AI investing: if AI spending goes up, all AI stocks go up. The reality is more specific, and the specificity is what determines returns.

Each tier captures a different slice of AI spending at a different speed. The concept institutional analysts call “operating leverage to AI spending” works in plain terms like this:

This sequencing explains why headline spending figures can mislead. Gartner forecasts worldwide AI spending at $2.52 trillion in 2026, up 44% year-over-year. IDC projects global AI systems spending at approximately $301 billion in 2026, up from $223 billion in 2025. These figures represent different scopes, and neither maps directly onto any single stock’s revenue. Understanding which slice of spending each tier captures is the prerequisite for interpreting any AI spending data as it is released.

A record 133-percentage-point performance gap across the technology sector had opened between the top and bottom deciles of technology stock returns as of May 2026, the largest dispersion in Morningstar’s dataset, with storage and semiconductor hardware firms dominating the top performers list while software names clustered at the bottom.

BlackRock Investment Institute draws the distinction sharply, framing infrastructure semiconductors as “core AI infrastructure holdings” and software as “AI satellites” with more speculative characteristics.

At the software layer, outcomes depend less on aggregate spending levels and more on individual contract wins, enterprise adoption rates, and competitive differentiation. This idiosyncratic risk is what separates Tier 3 from the others and why position sizing matters more there than anywhere else in the AI value chain.

UBS coined the most useful shorthand for this tier: hyperscalers are “AI toll roads,” collecting recurring revenue from AI workloads, in contrast to hardware “arms suppliers” whose revenues are more cyclical and tied to capex cycles. The metaphor holds up under scrutiny, but the toll road requires serious upfront construction.

Microsoft has committed $190 billion in capital expenditures for calendar 2026, driven primarily by AI infrastructure. Azure growth is guided in the high-30s percent range, with AI services contributing 7 percentage points to Azure’s 31% growth as recently as Q3 FY2024. Goldman Sachs characterises Microsoft as a “core AI infrastructure and applications beneficiary” with lower risk than pure hardware, thanks to diversified revenue streams.

Alphabet presents a similar profile through Google Cloud, which reported revenue of $9.6 billion in Q1 2024, up 28% year-over-year. Capex reached $11 billion in Q4 2023 alone, with management confirming ongoing increases into 2025-2026 with AI as the primary driver. Alphabet does not disaggregate an explicit “AI revenue” line, but AI underpins Search, YouTube, Ads, and Cloud products.

| Company | AI Revenue Signal | 2026 Capex Commitment | Analyst Characterisation |

|---|---|---|---|

| Microsoft | AI contributed 7pp to Azure growth | $190 billion | “Core AI infrastructure and applications beneficiary” (Goldman Sachs) |

| Alphabet | AI embedded across Search, YouTube, Ads, Cloud | Ongoing increases confirmed | “Lower-volatility AI exposure” (Bernstein) |

The diversification argument is what distinguishes this tier from both hardware above and software below. Non-AI revenue buffers against capex volatility:

For investors seeking meaningful AI exposure without accepting hardware-level drawdown risk, cloud platforms represent the most practical core-portfolio vehicle. The capex commitments are real and substantial, but the recurring revenue and business diversification provide a structural buffer that pure-play names in either direction cannot match.

Palantir occupies a structurally different position from every other name in this guide. It is asset-light and contract-based. Revenue is driven by government and enterprise deployments of the Palantir Artificial Intelligence Platform (AIP), not by capex cycles or cloud workload billings.

In Q1 2024, Palantir reported total revenue of $634 million, up 21% year-over-year. U.S. commercial revenue reached $175 million, up 40% year-over-year, and the company posted GAAP net income of $106 million, its sixth consecutive profitable quarter. For full-year 2023, total revenue was $2.23 billion, with U.S. commercial revenue of $808 million (up 36%) and customer count growing 35%.

The government anchor remains substantial. The U.S. Army TITAN contract, valued at up to $250 million over several years, provides AI-driven sensor fusion capability and illustrates the kind of large-scale deployments that drive this tier’s revenue.

CEO Alex Karp has described Palantir as “the default operating system for AI in the enterprise and in defence.”

The valuation tension arrives naturally from these numbers. RBC Capital Markets acknowledges strong AI positioning but warns that “valuation embeds very high expectations relative to current revenue scale.” ARK Invest frames the trade-off directly: Palantir offers “higher upside but greater execution risk, particularly around commercial scaling.” Morningstar notes that Palantir trades at higher price-to-sales and price-to-earnings multiples with wider valuation dispersion than hardware or cloud peers.

Enterprise AI adoption rates remain far below what Palantir’s current multiple implies: an estimated 70-80% of enterprise AI pilots fail or stall, only 12-20% of enterprises achieve meaningful operational AI embedding, and agentic AI deployment sits at just 17% as of April 2026, a gap that explains why Goldman Sachs projects ROI from AI enterprise deployments will not emerge meaningfully until 2027-2028.

The contrast against the other tiers clarifies what an investor is buying:

Position sizing becomes the critical variable. The upside is real, but it is priced into the multiple, and the earnings story depends on a smaller, more concentrated set of outcomes than either Tier 1 or Tier 2.

Understanding the three tiers intellectually is the first step. Placing them into an actual allocation context is where the framework becomes useful.

Institutional consensus converges on clear role assignments. BlackRock Investment Institute recommends infrastructure semiconductors as a smaller percentage of overall equity allocation for risk-averse investors, hyperscalers as more suitable core AI holdings, and AI software as tactical or thematic. Morningstar research confirms the pattern: semiconductor stocks showed higher beta and greater earnings volatility versus cloud platforms, which had lower beta and more stable earnings revisions. J.P. Morgan Asset Management assigns hardware to aggressive growth sleeves, cloud to broad growth exposure, and AI software to thematic tilts.

The BlackRock Investment Institute AI framework organises AI equity exposure across three phases, buildout, adoption, and transformation, with foundational infrastructure including chips and cloud systems treated as the earliest and most directly exposed layer, a structure that maps closely onto the hardware-cloud-software tiers used throughout this guide.

The practical sequencing question matters as much as the role assignment:

| Tier | Representative Names | Volatility Profile | Portfolio Role | Best Suited For |

|---|---|---|---|---|

| Tier 1: Hardware | NVIDIA, Broadcom | Highest | Aggressive growth / satellite | Investors with high risk tolerance seeking maximum AI beta |

| Tier 2: Cloud Platforms | Microsoft, Alphabet | Moderate | Core long-term holding | Broad growth exposure with diversified revenue buffer |

| Tier 3: AI Software | Palantir | High (idiosyncratic) | Thematic / tactical satellite | Investors comfortable with contract-concentration risk and elevated multiples |

These roles are not permanent. As the AI build-out cycle matures through the mid-2020s, hardware growth rates may normalise further, cloud platforms may begin converting heavy capex into free cash flow recovery, and the software layer may see consolidation that changes its risk profile. The framework adapts; the structural distinctions endure.

Investors wanting to stress-test their AI allocation against broader market structure will find our full explainer on AI stock valuation concentration risk useful: it examines how low index-level volatility is masking single-stock distributional divergence, why passive investors may be carrying more AI-specific risk than they realise, and how Goldman Sachs’ May 2026 assessment frames the monetisation timeline investors should be monitoring.

The three-tier framework is durable beyond the 2026 cycle. As AI spending evolves, the same structural distinctions, capex-driven hardware, recurring-revenue cloud, and contract-driven software, will continue to define how value flows through the chain. The tiers may add new entrants (AI agents, inference-specific hardware, autonomous systems platforms), but the underlying logic of where capital enters and how revenue accrues at each layer will persist.

Near-term dynamics are specific and worth tracking. Hardware growth is decelerating from peak triple-digit rates but remains substantial, with NVIDIA’s most recent quarter still showing 92% year-over-year data centre revenue growth. Cloud platforms are in a heavy investment phase where capex temporarily weighs on free cash flow, with Microsoft’s $190 billion commitment the most visible example. Software is in a commercial scaling phase where execution against individual contracts matters more than aggregate AI spending figures.

Investors who built this framework now are better positioned to evaluate every new AI name, emerging tier, or spending forecast that arrives. The stocks will change. The structure will not.

For investors ready to translate the three-tier model into a specific weighting structure, our dedicated guide to AI infrastructure stock allocation walks through the 50/40/10 hardware-cloud-software split recommended by US financial advisors for growth portfolios, with current data on NVIDIA’s GPU market share, Broadcom’s forward P/E, and Google Cloud’s Q1 2026 growth rate applied to each allocation layer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An AI investment strategy framework organises AI stocks into three structural tiers: hardware and infrastructure (such as NVIDIA and Broadcom), cloud platforms (such as Microsoft and Alphabet), and pure-play AI software (such as Palantir), each capturing value at a different point in the AI supply chain with distinct volatility profiles and portfolio roles.

NVIDIA is a Tier 1 hardware name whose revenue is driven directly by AI capital expenditure cycles, making it the highest-beta option, while Microsoft is a Tier 2 cloud platform that collects recurring revenue from AI workloads across a diversified business, making it more suitable as a core long-term holding with moderate volatility.

Institutional consensus, including guidance from BlackRock, J.P. Morgan Asset Management, and Morningstar, recommends establishing cloud platforms like Microsoft and Alphabet as the core position first, adding hardware names like NVIDIA and Broadcom as growth satellites, and sizing pure-play software like Palantir as a smaller thematic or tactical allocation only after the core and growth sleeves are set.

Each tier captures spending at a different speed: hardware names like NVIDIA recognise revenue almost immediately when capex orders are placed, cloud platforms bill workloads over months through consumption-based pricing, and software companies like Palantir only capture value when multi-year enterprise contracts are signed and expanded.

Pure-play AI software names carry high idiosyncratic risk because earnings depend on a concentrated set of individual contract wins rather than aggregate AI spending levels; analysts at RBC Capital Markets and ARK Invest highlight that Palantir's valuation already embeds very high expectations relative to its current revenue scale, and enterprise AI adoption rates remain far below what the current multiple implies.