Barclays: Iran Deal Could Spark Cross-Asset Rally on Oil Drop

1 hr ago

Goldman Sachs has pinpointed the single variable that has separated winners from losers in the 2026 equity market: upward earnings revisions. Stocks exhibiting the strongest positive estimate revisions have broadly outperformed the wider market year-to-date, and the firm’s analyst Ben Snider is using that signal to build a specific case for AI infrastructure stocks rather than a generic index-level call. The argument is more precise than it appears. Goldman contends that multiple expansion is effectively off the table at 21x forward price-to-earnings, that further S&P 500 gains must therefore be entirely earnings-driven, and that hyperscalers and power infrastructure companies sit at the centre of that earnings growth channel. What follows unpacks both sides of the framework: where Goldman sees the clearest earnings-revision-led opportunity, and which four risk factors the firm explicitly flags as capable of derailing the thesis. Investors will leave with a clearer picture of the logic behind the call and the conditions under which it would break down.

Goldman’s framework follows a three-step logic chain, and each step narrows the investment universe.

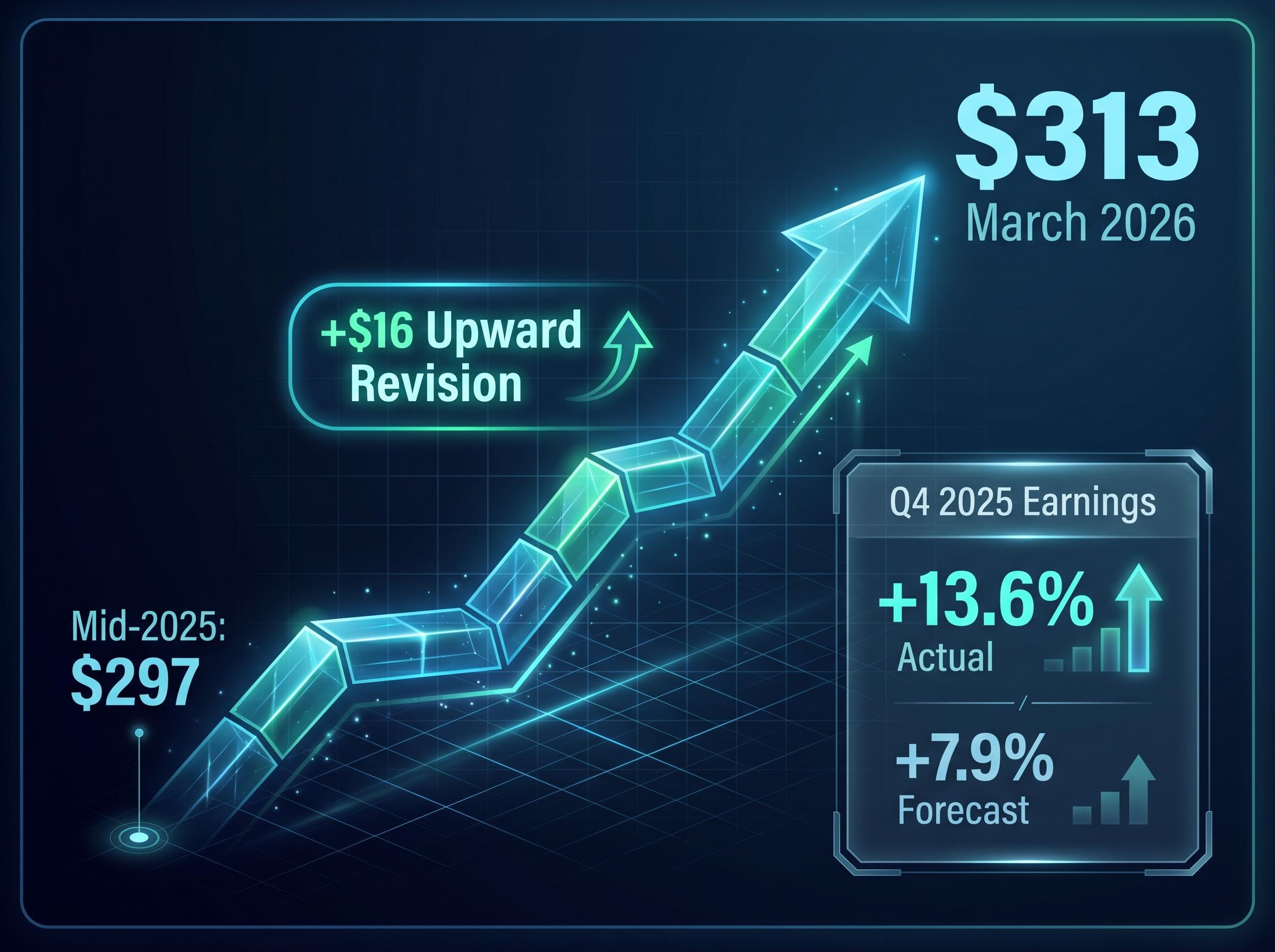

The revision trend has fundamental support behind it. Q4 2025 earnings growth came in at +13.6% year-over-year, well above an initial forecast of +7.9%, according to U.S. Bank data as of 4 March 2026. That beat was not a one-quarter anomaly; it sat within a broader upward trajectory for 2026 S&P 500 earnings per share estimates.

Goldman’s 2026 S&P 500 EPS assumption has climbed from $297 in mid-2025 to $313 by March 2026, a $16 upward revision in roughly eight months.

The revision direction, not just the current estimate level, is what Goldman’s thesis relies on. If estimates continue moving higher, the framework holds. If they stall, the thesis is under stress.

Earnings revision breadth across the S&P 500 accelerated sharply following the March 2026 correction, with 22% of estimates revised upward against only 5% downgraded and the forward EPS growth forecast for the median S&P 1500 stock rising from 8% to 12%, a pattern that corroborates Goldman’s signal that revision momentum, not just absolute estimate levels, is the operative performance differentiator in the current market.

The number that anchors the entire positioning call is $650 billion. That is the projected capital investment by large cloud providers in 2026, up roughly 59% from approximately $410 billion in 2025, according to U.S. Bank. Spending at that scale does not simply benefit the companies making it; it creates a downstream revenue channel wide enough to move aggregate S&P 500 earnings.

The most recent quarterly disclosures place hyperscaler capital expenditure well above the $650 billion full-year figure Goldman cited, with Amazon, Microsoft, Alphabet, and Meta collectively spending $130 billion in Q1 2026 alone and combined full-year guidance now tracking toward $725 billion, a figure that continues to move the revision needle for every company in the AI supply chain.

Goldman’s Ben Snider specifically recommended hyperscalers and power infrastructure companies as the preferred positioning within the AI capex theme. The distinction between these two categories matters for portfolio construction.

| Category | Earnings mechanism | Link to AI capex |

|---|---|---|

| Hyperscalers | Capex is both a cost and a direct signal of future revenue trajectory | Primary spenders on AI compute and data centre infrastructure |

| Power infrastructure | Revenue driven by structural electricity demand from data centres | Indirect but structurally necessary beneficiary of the buildout |

Hyperscalers occupy a dual role in this cycle. They are simultaneously the largest spenders on AI infrastructure and the most direct revenue beneficiaries of that spending. Their capex guidance functions as a forward indicator: when a hyperscaler raises its spending commitment, analysts revise earnings estimates upward for the company itself and for its supply chain. That sensitivity to capex guidance is precisely why earnings revisions for these names have led the broader market.

Power infrastructure companies capture a different slice of the same capex flow. Data centres require enormous amounts of electricity, and that demand is structural rather than cyclical. A hyperscaler may adjust its computing architecture between chip generations, but the power demand underlying those facilities persists. Goldman’s preference for power infrastructure names reflects this longer-duration earnings visibility, which carries less of the performance bar risk attached to headline AI names.

Goldman’s view that the S&P 500 forward price-to-earnings ratio is projected to remain near 21x through the forecast period sounds like a valuation footnote. It is not. It is a constraint that reshapes the entire return equation.

Equity returns come from two sources: earnings growth and multiple expansion. Goldman has effectively removed one of those engines from the equation. At 21x forward earnings, a level already above the S&P 500‘s 5-year and 10-year historical averages according to U.S. Bank, there is no valuation buffer. If earnings disappoint, the multiple provides no cushion.

At 21x forward earnings, Goldman sees no room for multiple expansion; future index gains must come from earnings alone.

U.S. Bank independently arrived at the same conclusion, noting that elevated valuations mean companies cannot afford earnings stumbles. The convergence of two separate institutions on this view adds weight.

Bank of America’s independent analysis of S&P 500 forward valuation arrives at the same constraint Goldman describes, with BofA’s internal model showing the index expensive on 16 of 20 metrics and the 21.4x forward P/E sitting roughly 20% above its 10-year average, a convergence of two separate institutional frameworks on the same ceiling that adds weight to the no-multiple-expansion premise underpinning Goldman’s call.

The practical implications for investors are specific:

Goldman’s thesis rests on a specific economic mechanism, not on enthusiasm about artificial intelligence as a concept. Understanding how hyperscaler capital spending flows through to aggregate earnings is what separates a reasoned position from a thematic bet.

The transmission runs through four stages:

At each stage, a different category of company benefits: compute hardware at stage two, data centre construction and network equipment at stage three, and power utilities throughout, given the structural electricity demand underpinning the entire chain.

The $297-to-$313 upward revision in 2026 S&P 500 EPS estimates is not statistical noise. U.S. Bank explicitly connects the upward revision trend to heavy AI infrastructure investment by large cloud providers. As hyperscaler capex guidance has escalated, analysts have systematically upgraded their assumptions for AI-adjacent companies, producing the aggregate lift visible in the index-level estimate.

The scale of the capex cycle explains why. A 59% year-over-year increase in projected hyperscaler spending, from approximately $410 billion in 2025 to approximately $650 billion in 2026, is not a normal capital investment cycle. The deviation from historical norms is what justifies treating it as a structural earnings growth driver rather than a cyclical bump.

Goldman’s framework relies on the direction of future revisions, not just their current level. If the next round of hyperscaler earnings calls produces capex guidance that meets or exceeds expectations, the revision trend should persist. If guidance disappoints, the entire chain slows.

Goldman’s Ben Snider did not present the constructive outlook without qualification. The firm identified four specific risk channels, each with a distinct mechanism through which it could damage the thesis.

| Risk factor | Mechanism | What to monitor | Why it matters now |

|---|---|---|---|

| Oil price shock | Produces slowing growth plus tighter financial conditions | Crude price spikes, credit spread widening, inflation expectations | This combination has historically preceded the end of prior bull market cycles |

| AI infrastructure earnings bar | Strong prior performance raises the future outperformance threshold | Quarterly earnings beats relative to already-elevated estimates | AI stocks have priced in substantial optimism; sustained delivery is required |

| Midterm election seasonality | Historical flow patterns moderate returns in months preceding midterm elections | Positioning data and fund flow trends as November approaches | 2026 Congressional midterms fall directly within the tactical window |

| Momentum exhaustion | Near-term mean reversion pressure after the strength of recent gains | Breadth deterioration, rotation signals, momentum factor drawdowns | Recent momentum-driven gains have been strong enough to invite reversion |

Goldman identifies an oil price shock as capable of producing the combination of slowing growth and tighter financial conditions that has historically ended prior bull market cycles.

These are not presented as Goldman’s base case. The firm’s primary view remains constructive. They are the conditions under which the constructive case fails, and that distinction matters. An investor who treats the Goldman call as binary, either buy or do not buy, misses the diagnostic value of knowing which signal to watch for deterioration.

U.S. Bank independently corroborates the energy risk channel, flagging inflation driven by rising energy prices as the primary swing factor for valuations at currently elevated P/E multiples.

Investors wanting a second institutional risk framework alongside Goldman’s four factors will find our full explainer on Wolfe Research’s five compounding tail risks, which maps the yen carry trade unwind, AI capex disappointment, private credit stress, persistent inflation, and bond vigilante dynamics as potentially reinforcing rather than independent risks, with specific monitoring thresholds for each.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Goldman’s framework holds together as a logical chain. Earnings revisions lead performance. AI capex drives revisions. Hyperscalers and power infrastructure companies are the most directly positioned beneficiaries. At 21x forward earnings, with both Goldman and U.S. Bank independently concluding that multiple expansion is not a realistic return driver, the entire weight of the equity market’s forward progress falls on earnings delivery.

That coherence is also the source of fragility. The thesis is built on the assumption that the current capex escalation continues and that none of the four identified risks materialises in a way that disrupts the earnings chain. The $313 current 2026 EPS estimate is the baseline; further upward revision sustains the thesis, while stagnation or downward revision is the primary warning signal.

Investors treating this as a passive position would be misreading the framework. Goldman’s call requires active monitoring, and the checkpoints are specific:

The Goldman call is not a set-and-forget position. It is a thesis with identifiable conditions for success and identifiable triggers for reassessment. Investors who hold it actively, with those four checkpoints in view, are positioned to act on the framework rather than simply hope it holds.

AI infrastructure stocks include hyperscalers (large cloud providers like Amazon, Microsoft, Alphabet, and Meta) and power infrastructure companies that supply electricity to data centres. Goldman Sachs is bullish on them in 2026 because projected hyperscaler capital investment of $650 billion is driving upward earnings revisions across the S&P 500 supply chain, which Goldman analyst Ben Snider identifies as the primary performance differentiator in the current market.

At a forward price-to-earnings ratio of approximately 21x, the S&P 500 is already trading above its 5-year and 10-year historical averages, leaving little valuation headroom for the multiple to expand further. This means future index gains must come entirely from earnings growth, not from investors paying a higher price for each dollar of earnings.

When a hyperscaler raises its data centre and computing infrastructure budget, purchase orders flow to semiconductor companies, equipment manufacturers, network providers, and construction firms, many of which are S&P 500 constituents. Analysts then revise earnings estimates upward for each supplier, lifting the aggregate index-level EPS forecast, which is how projected hyperscaler capex of $650 billion in 2026 has contributed to Goldman raising its S&P 500 EPS assumption from $297 to $313.

Goldman identified an oil price shock (which combines slowing growth with tighter financial conditions), a high earnings bar for AI infrastructure stocks (where elevated estimates require sustained delivery to maintain outperformance), midterm election seasonality (historical flow patterns that may moderate returns ahead of November 2026), and momentum exhaustion (near-term mean reversion pressure following strong recent gains).

Goldman's framework points to four active checkpoints: the direction of 2026 S&P 500 EPS revisions (whether estimates continue rising or plateau), hyperscaler capex guidance on upcoming earnings calls (the most direct input into the earnings chain), oil price trends and financial conditions signals, and seasonal positioning data as the November 2026 midterm election calendar approaches.