SK Hynix Hits $1 Trillion as AI Memory Bet Lifts KOSPI to a Record

1 hr ago

The Reserve Bank of New Zealand held its Official Cash Rate (OCR) at 2.25% on Wednesday, 27 May 2026, but the accompanying statement carried a message that markets cannot afford to treat as routine. The RBNZ flagged that rate hikes will need to arrive sooner and hit with greater magnitude than the bank had previously anticipated, a shift in forward guidance that reframes the hold as a launching pad rather than a resting point.

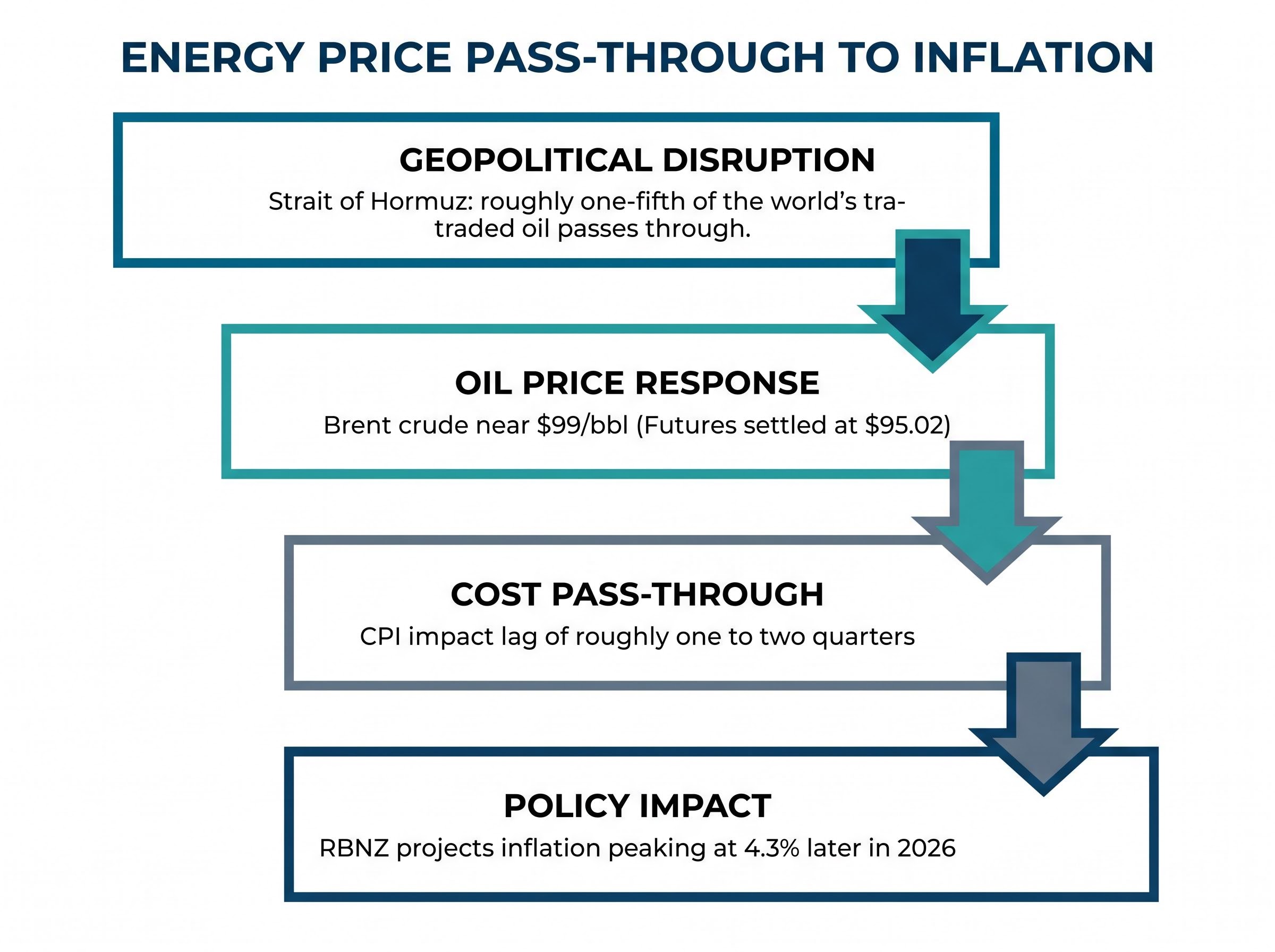

With Brent crude trading near $99 per barrel on supply disruption fears tied to the Strait of Hormuz, Asia-Pacific central banks are confronting an energy-price shock they cannot control but cannot ignore. The RBNZ’s decision puts the region’s monetary policy dilemma in sharp relief, and Australian inflation data released the same day added a second confirming signal. What follows covers what the RBNZ decided, why the inflation forecast shifted, how energy markets are driving the pressure, and what the parallel Australian consumer price index (CPI) data suggests about where regional rates are headed.

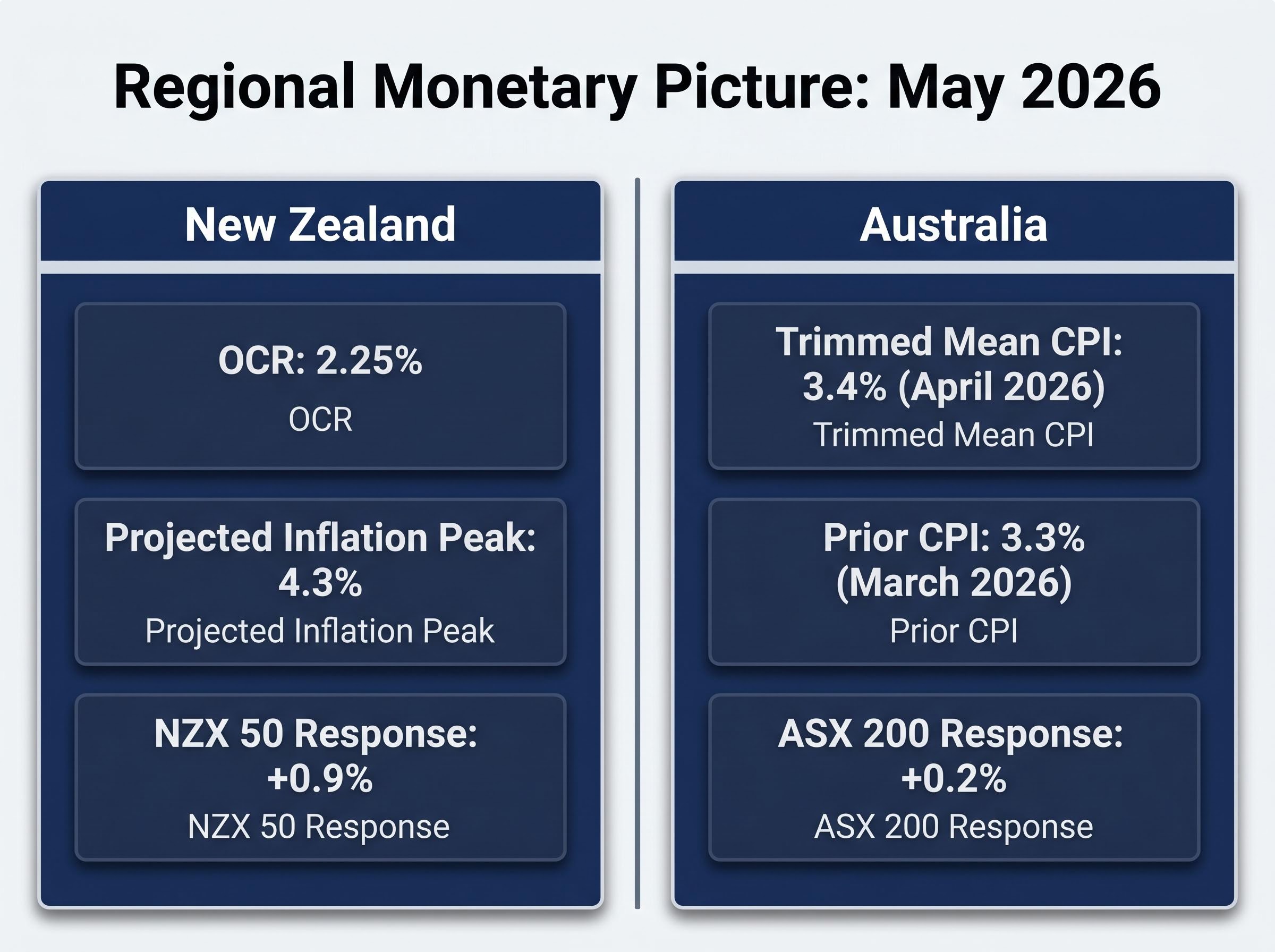

On the surface, the decision was steady. The OCR remained at 2.25%, unchanged from the prior meeting, and the NZX 50 responded with an approximate 0.9% gain on the session, suggesting equity markets read the hold as the dominant near-term signal.

The statement told a different story.

The RBNZ indicated that rate hikes would need to come sooner and at greater magnitude than previously anticipated, citing persistent upside inflation risks driven by energy costs and imported price pressures.

That language represents a material shift in the bank’s reaction function. A hold with hawkish forward guidance is a tightening signal in all but name; it tells markets that the pause is temporary and conditional, not an expression of comfort. For holders of New Zealand fixed income and rate-sensitive equities, the rate itself is not the story. The projected path is.

The gap between what the RBNZ did and what it said is where the real positioning information sits. The bank chose to hold now while explicitly pre-committing to a steeper tightening trajectory, a deliberate communication strategy that gives markets time to price the shift before it arrives in the OCR itself.

The link between a geopolitical event in the Middle East and a rate decision in Wellington is not immediately obvious. It becomes clearer when traced step by step.

The RBNZ now projects inflation peaking at 4.3% later in 2026, a level it attributes in part to higher fuel and petrochemical prices stemming from the Middle East conflict.

The bank’s concern is not confined to current energy prices. It extends to the persistence of those pressures through late 2026 and into 2027, particularly if the Strait of Hormuz situation remains unresolved. That persistence risk is what separates a one-off supply shock from a structural shift in the inflation outlook.

The Hormuz oil risk premium is not expected to decompress quickly even under a best-case diplomatic resolution: war-risk insurance markets have effectively closed the strait to standard commercial traffic, VLCC daily hire rates are tracking around $110,000 per day, and the IEA projects a two-year supply chain recovery timeline, meaning the persistence risk the RBNZ cited is anchored in physical market structures rather than spot price sentiment alone.

A 4.3% inflation peak is not an abstract macroeconomic projection. It is the number that will govern fixed-rate mortgage decisions, wage negotiation benchmarks, and retail consumption patterns in New Zealand through the second half of 2026.

The RBNZ acknowledged that inflation may peak even as economic growth shows signs of softening, a combination that carries stagflationary risk. Households face a two-sided squeeze: purchasing power erodes as prices rise, while borrowing costs increase as the central bank moves to contain those very price pressures.

For context, New Zealand’s December 2023 quarter CPI ran at 4.7%, and household living-cost inflation reached 6.2% at its prior peak, according to Statistics New Zealand data. Those figures provide a baseline for how elevated inflation has felt in practice for New Zealand consumers. The projected 4.3% peak sits below those prior readings but arrives in an environment where the next move in rates is up rather than down, meaning mortgage repricing pressure is additive rather than offsetting.

| Metric | Current / Projected | Prior Comparison | RBNZ Implication |

|---|---|---|---|

| Official Cash Rate | 2.25% (held May 2026) | 5.50% (May 2024 peak) | Hikes expected sooner and larger than prior guidance |

| Inflation peak projection | 4.3% (late 2026) | 4.7% CPI (Dec 2023 quarter) | Energy-driven upside risk binding on policy outlook |

| Growth outlook | Signs of softening | N/A | Stagflationary risk acknowledged; rate path conditional |

The timing of any rate hike will depend on how quickly energy-price pressures feed through to core CPI measures, but the direction of travel is now explicit.

The RBNZ’s hawkish shift might look like an outlier if not for what arrived the same day from across the Tasman.

Australia’s April 2026 trimmed mean CPI printed at 3.4% year-on-year, up from 3.3% in March 2026. Trimmed mean is the Reserve Bank of Australia’s (RBA) preferred inflation gauge; it strips out the most volatile price movements at both ends of the distribution to reveal the underlying trend. The month-on-month acceleration, while modest, pointed in the wrong direction for those anticipating near-term rate relief.

Australia’s trimmed mean CPI accelerated to 3.4% year-on-year in April 2026, up from 3.3% the prior month, reinforcing the RBA’s position that rate cuts remain premature.

The same energy-price transmission dynamic described in the RBNZ context applies to Australia. Both economies are net energy importers, both face pass-through from elevated crude prices into transport and manufacturing costs, and both central banks have explicitly identified Middle East geopolitical uncertainty as an upside inflation risk. The RBA flagged as much in its May 2024 communications, when it noted that “global uncertainties, including in the Middle East” posed upside risks to the inflation outlook.

Two central banks in the same region, on the same day, signalling the same direction. For investors tracking Asia-Pacific fixed income and currency positioning, the convergence carries more weight than either signal alone.

The RBNZ’s hawkish pivot sits within a broader regional pattern: the Asia-Pacific inflation outlook heading into late May 2026 was already under pressure from structurally different but directionally aligned inflation engines in Australia, New Zealand, and Japan, all pointing toward a higher-for-longer rate environment across the region.

The RBNZ has handed markets a conditional roadmap. The hold is temporary; the hike is coming. The question is when, and how large. The following data points will determine the answer:

The U.S. inflation data due Thursday, 29 May 2026 matters for the RBNZ not only as a global macro signal but because analyst pass-through estimates suggest 40-60% of an oil price increase feeds into core CPI over 3-6 months, meaning the April U.S. print and subsequent June and July readings will indicate how far the cost-push wave has travelled through the world’s largest economy and, by extension, how durable the commodity price pressure bearing on New Zealand import costs is likely to be.

The NZX 50’s 0.9% gain on decision day reflects a market reading of the hold as benign in the short term. The guidance language, however, creates a more complex medium-term picture for rate-sensitive sectors, including real estate investment trusts, utilities, and leveraged consumer names.

The RBNZ held at 2.25% on 27 May 2026, projected inflation peaking at 4.3% later in the year, and told markets to prepare for hikes that arrive sooner and hit harder than previously signalled. On the same day, Australia’s trimmed mean CPI accelerated to 3.4%, and Brent crude traded near $99 per barrel.

The hold is conditional, not comfortable. It only makes sense if energy prices plateau. If they do not, the RBNZ’s own forecast logic demands action, and the bank has now said as much explicitly. The shift from neutral observation of energy risks to forward guidance pre-committing to tightening is the material change.

The RBNZ signalled that rate hikes would need to come sooner and at greater magnitude than previously anticipated, making the energy price trajectory the single most consequential variable for the bank’s next move.

For investors positioned across New Zealand and Australian rate-sensitive assets, the Strait of Hormuz is now a monetary policy input, not just a geopolitical headline. The energy price trajectory will determine whether the RBNZ’s conditional language becomes a confirmed hike timeline or a contingency that never fires.

For investors wanting to model the upper and lower bounds of the RBNZ’s inflation scenario, our deep-dive into the global oil supply crisis examines why emergency SPR and IEA releases totalling approximately 280 million barrels have failed to halt inventory drawdowns, why OPEC spare capacity of roughly 0.5 million barrels per day is negligible at current disruption scale, and why the IEA sees no supply-demand rebalancing scenario before October 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors, and past performance does not guarantee future results.

The Reserve Bank of New Zealand held its Official Cash Rate at 2.25% on 27 May 2026, keeping it unchanged from the prior meeting while signalling that rate hikes will need to come sooner and at greater magnitude than previously anticipated.

The RBNZ shifted to hawkish forward guidance because persistent upside inflation risks, driven by elevated energy costs and imported price pressures linked to Strait of Hormuz supply disruptions, shifted the bank's inflation outlook materially to the upside.

The RBNZ projects New Zealand inflation peaking at 4.3% later in 2026, attributing the elevated forecast in part to higher fuel and petrochemical prices stemming from the Middle East conflict.

New Zealand is a net energy importer, so supply disruptions near the Strait of Hormuz push up crude prices, which flow through to domestic fuel and manufacturing costs within one to two quarters, lifting headline CPI and forcing the RBNZ to consider tighter monetary policy.

Australia's April 2026 trimmed mean CPI accelerated to 3.4% year-on-year from 3.3% the prior month, reinforcing a regional pattern of hawkish central bank positioning and confirming that both the RBA and RBNZ face energy-driven inflation pressures pointing in the same direction.