RBNZ Holds at 2.25% but Signals Larger Hikes Ahead

22 mins ago

On 27 May 2026, a single analyst upgrade in New York triggered a chain reaction that ended with a South Korean chipmaker joining the trillion-dollar club and the KOSPI hitting a record high it had never reached before. The move was not random. It reflects a deepening structural thesis: that the artificial intelligence infrastructure build-out will require extraordinary volumes of advanced memory, and that SK Hynix and Samsung Electronics sit at the centre of that supply chain. The day’s price action crystallised months of accumulating conviction into a single explosive session. What follows maps the full catalyst chain, from Micron Technology’s 19.29% surge on Wall Street through to the KOSPI’s 5% leap, explains what the $1 trillion milestone means for South Korean semiconductor stocks, and identifies the macro forces that could either sustain or undercut the rally.

The transmission mechanism from a Wall Street brokerage note to a record-breaking session in Seoul followed a precise three-step sequence:

Micron Technology surged 19.29% to $895.88 on 26 May 2026, the single-session move that set the catalyst chain in motion.

The UBS thesis mattered because it was rooted in AI capital expenditure conviction, not company-specific operational improvement. That distinction is why the signal radiated outward to all memory chipmakers rather than remaining contained to Micron alone. By the time South Korean markets opened on 27 May, the combination of a sector-wide AI demand upgrade and fresh Wall Street record closes had already priced the direction of travel.

For investors monitoring geographically diversified portfolios, the sequence illustrates a structural shift. South Korean semiconductor stocks are no longer moving primarily on domestic fundamentals. They are now directly wired to U.S. analyst sentiment on AI infrastructure spending, and the transmission speed from a New York brokerage desk to a Seoul trading floor is measured in hours, not weeks.

SK Hynix (KS: 000660) gained approximately 13.60-14% on 27 May 2026, pushing its market capitalisation above $1 trillion for the first time. Samsung Electronics (KS: 005930) advanced approximately 6.69-8% in the same session.

The milestone places SK Hynix alongside Samsung Electronics and Micron Technology in a valuation group defined almost entirely by AI memory demand.

| Company | Single-Day Move | Market Cap Status | Primary AI Exposure |

|---|---|---|---|

| SK Hynix | +13.60% | Above $1 trillion (first time) | HBM (High Bandwidth Memory) |

| Samsung Electronics | +6.69% | Existing trillion-dollar member | DRAM / NAND |

| Micron Technology | +19.29% (prior session) | Trillion-dollar context | HBM / DRAM |

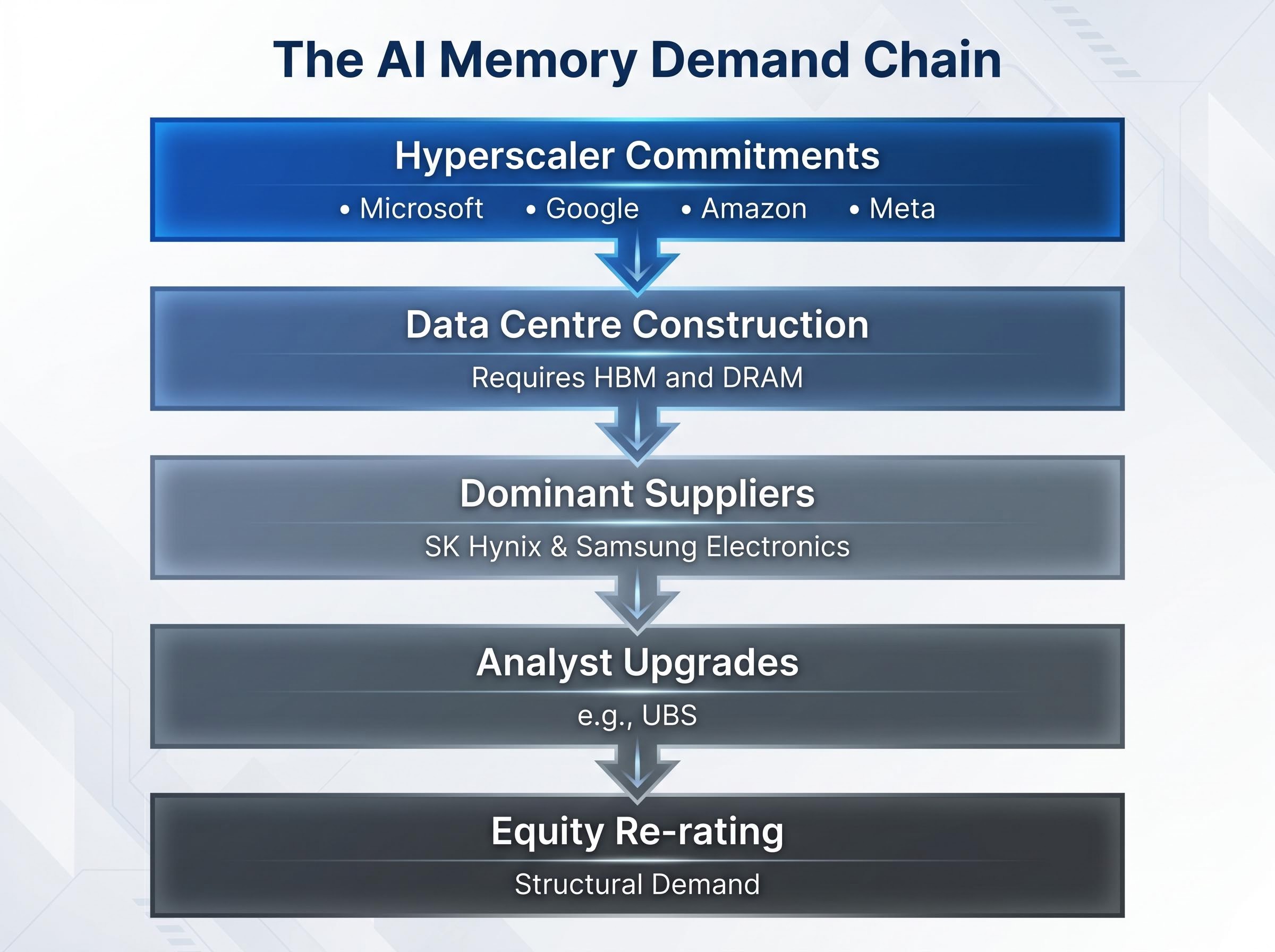

High Bandwidth Memory (HBM) is a specialised type of memory chip stacked in layers to deliver the data throughput that AI accelerators, including those produced by NVIDIA, require. Conventional DRAM cannot match HBM’s speed or capacity per unit area, and SK Hynix is the dominant global supplier of these chips.

PatSnap’s HBM market analysis places SK Hynix at approximately 57% to 62% of global HBM supply in 2025, with Samsung Electronics at 17% and Micron at 21%, a concentration that gives the two South Korean producers combined control over roughly three-quarters of the memory chips underpinning AI accelerator deployments worldwide.

The $1 trillion valuation reflects a market judgment that HBM supply constraints will persist well into 2027, sustaining pricing power that conventional memory cycles would not support. Institutional capital is now pricing SK Hynix as a structural beneficiary of the AI build-out on the same scale as the largest technology companies in the world, with direct implications for index weightings, fund flows, and how the stock will be benchmarked going forward.

With HBM capacity sold out across SK Hynix and Micron through 2026-2027, a condition driven by manufacturing complexity rather than capital investment cycles, pricing power is structurally insulated from the demand softness that has historically ended memory upcycles.

The UBS upgrade, the KOSPI record, and the SK Hynix milestone are all expressions of the same underlying thesis: data centre spending by the world’s largest technology companies is creating a structural demand floor for advanced memory that did not exist three years ago.

The demand chain operates in a specific sequence:

Hyperscaler AI capital expenditure reached $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, with full-year 2026 combined guidance sitting at approximately $725 billion and a $1 trillion annual run rate projected for 2027, numbers that reframe the entire demand chain described above as a multi-year commitment rather than a single-year spending spike.

The KOSPI surged approximately 5% to a record 8,457.9 on 27 May 2026, the macro-level expression of the AI memory demand thesis applied at index scale.

The broader technology sector uplift across Asia on 27 May reinforced the pattern. This was not a one-stock event; it was a sector-wide repricing driven by a single upstream variable: the scale and durability of AI infrastructure spending.

For investors assessing whether these stocks have moved too far too fast, the structural demand case is the determining input. If AI capex commitments prove durable across a multi-year cycle, the valuation re-rating may have further to run. If they are front-loaded or discretionary, the risk profile shifts considerably.

Samsung Electronics reached a wage and bonus agreement with its workforce on or around 27 May 2026, resolving a contested labour dispute that had presented operational and reputational overhang for the stock.

The resolution matters, but it matters as risk removal rather than as a new positive catalyst. A threatened strike that did not materialise reduced downside exposure; it did not create fresh upside momentum.

The differential between the two moves illustrates the distinction. SK Hynix’s rally was pure conviction in AI memory demand. Samsung’s rally was that same conviction, discounted by the fact that the market had already been pricing in some probability of production disruption.

Samsung’s production continuity is a systemic variable for the global memory market. A strike at the world’s largest memory chip producer would have tightened supply and introduced pricing complexity that extended well beyond the company itself. The deal’s resolution simplifies the investment thesis for both Samsung and the broader sector.

The KOSPI’s record session did not extend uniformly across Asia. On 27 May, China’s Shanghai Composite fell 1.1%, the CSI 300 retreated 0.7%, and Hong Kong’s Hang Seng declined approximately 0.8%. Japan’s Nikkei 225 advanced as much as 2.2% to a record 66,428.81, reflecting its own semiconductor exposure. The rally was sector-specific, not a broad regional risk-on move.

| Index | Direction | Move | Semiconductor Exposure |

|---|---|---|---|

| KOSPI | Up | +5% | High |

| Nikkei 225 | Up | +2.2% | Moderate |

| Hang Seng | Down | -0.8% | Moderate |

| Shanghai Composite | Down | -1.1% | Lower |

| CSI 300 | Down | -0.7% | Lower |

U.S.-Iran tensions and the risk of military action threatening Strait of Hormuz supply routes kept Brent crude near $99 per barrel, with Brent futures at $95.02 (down approximately 1.71% in the session). Energy cost concerns and geopolitical escalation risk limited how far broader risk appetite could extend beyond the semiconductor pocket of strength.

The Reserve Bank of New Zealand held its official cash rate at 2.25% on the same day, warning that inflation could peak at 4.3% later in 2026, driven partly by energy costs. The rate environment for rate-sensitive assets remains complicated even as AI-exposed equities surge.

U.S. inflation data expected on 29 May represents the most immediate near-term variable. A hotter-than-expected print would reinforce the case for prolonged elevated rates, which could compress valuations for high-multiple technology stocks and test whether the AI capex thesis can sustain current pricing under tighter financial conditions. For investors holding positions in South Korean semiconductor stocks after the 27 May surge, that data release is the next point of vulnerability.

A Wall Street upgrade, a trillion-dollar milestone, a labour resolution, and a record index close all occurred within 48 hours. They were not coincidental. Each was an expression of the same structural conviction: that AI memory demand is repricing the South Korean semiconductor sector on a scale that institutional capital is now treating as durable rather than cyclical.

The risks identified in the macro picture do not invalidate that thesis, but they qualify it. The rally’s concentration in a single sector, combined with geopolitical uncertainty and an unresolved inflation backdrop, means the trade is more exposed to a single macro shock than a broad-based equity advance would be.

Semiconductor supercycle durability is the central question dividing institutional analysts: the PHLX Semiconductor Index added approximately $3.8 trillion in market value over six weeks with gains backed by record earnings, yet concentration risk and US-China export control escalation represent the same category of single-variable shock that could test whether this repricing is structural or speculative.

The forward variable that will most directly test the thesis is whether hyperscaler AI capital expenditure commitments, when next disclosed in earnings, confirm or soften the demand picture that drove the 27 May moves.

For investors assessing position sizing in South Korean equities following the 27 May surge, our deep-dive into KOSPI risk management after a record rally examines Citigroup’s decision to close half its long position, the record retail margin debt reading of 35.7 trillion won that amplifies forced-selling risk, and how JPMorgan and Goldman Sachs are calibrating their 9,000 targets against near-term overbought signals.

KOSPI closed at a record 8,457.9. SK Hynix crossed $1 trillion. The question now is whether the next round of hyperscaler earnings validates the spending commitments that produced these numbers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High Bandwidth Memory (HBM) is a specialised chip that stacks memory layers to deliver the data throughput required by AI accelerators like those made by NVIDIA. SK Hynix controls approximately 57% to 62% of global HBM supply, making it and Samsung Electronics the dominant suppliers underpinning AI infrastructure worldwide.

SK Hynix crossed $1 trillion in market capitalisation on 27 May 2026 after gaining approximately 13.60% in a single session, driven by a UBS upgrade of Micron Technology and broad institutional conviction that AI memory demand will remain structurally elevated through at least 2027.

A UBS upgrade of Micron Technology on 26 May 2026 triggered a 19.29% surge in Micron's share price, which radiated overnight to South Korean markets because the upgrade was rooted in AI capital expenditure demand applicable to all advanced memory chipmakers, not just Micron specifically.

The key near-term risks include a hotter-than-expected U.S. inflation print that could compress high-multiple valuations, geopolitical tensions keeping Brent crude near $99 per barrel, and the possibility that hyperscaler AI capital expenditure commitments soften when next disclosed in earnings.

Amazon, Microsoft, Alphabet, and Meta combined for $130 billion in AI capital expenditure in Q1 2026 alone, with full-year 2026 combined guidance at approximately $725 billion and a $1 trillion annual run rate projected for 2027.