With the RBA cash rate at 4.35% following the May 2026 increase, Australian investors face a pointed question: can dividend-paying shares still compete with term deposits? For many, the answer is yes, and often by a meaningful margin once franking credits enter the calculation. The ASX 200 currently delivers a trailing dividend yield of approximately 4.0-4.3% in cash terms, rising to roughly 5.5% on a grossed-up basis. For income-focused investors, particularly those approaching or in retirement, that comparison deserves more than a passing glance. This guide explains how dividend income from ASX shares works in practice, why franking credits can tip the scales decisively in favour of equities for a wide range of tax positions, which income-focused ETFs and LICs are generating 4-9% yields in 2026, and how to think about constructing a passive income portfolio in the current rate environment.

Why the RBA’s 2026 rate moves are reshaping how Australians think about income

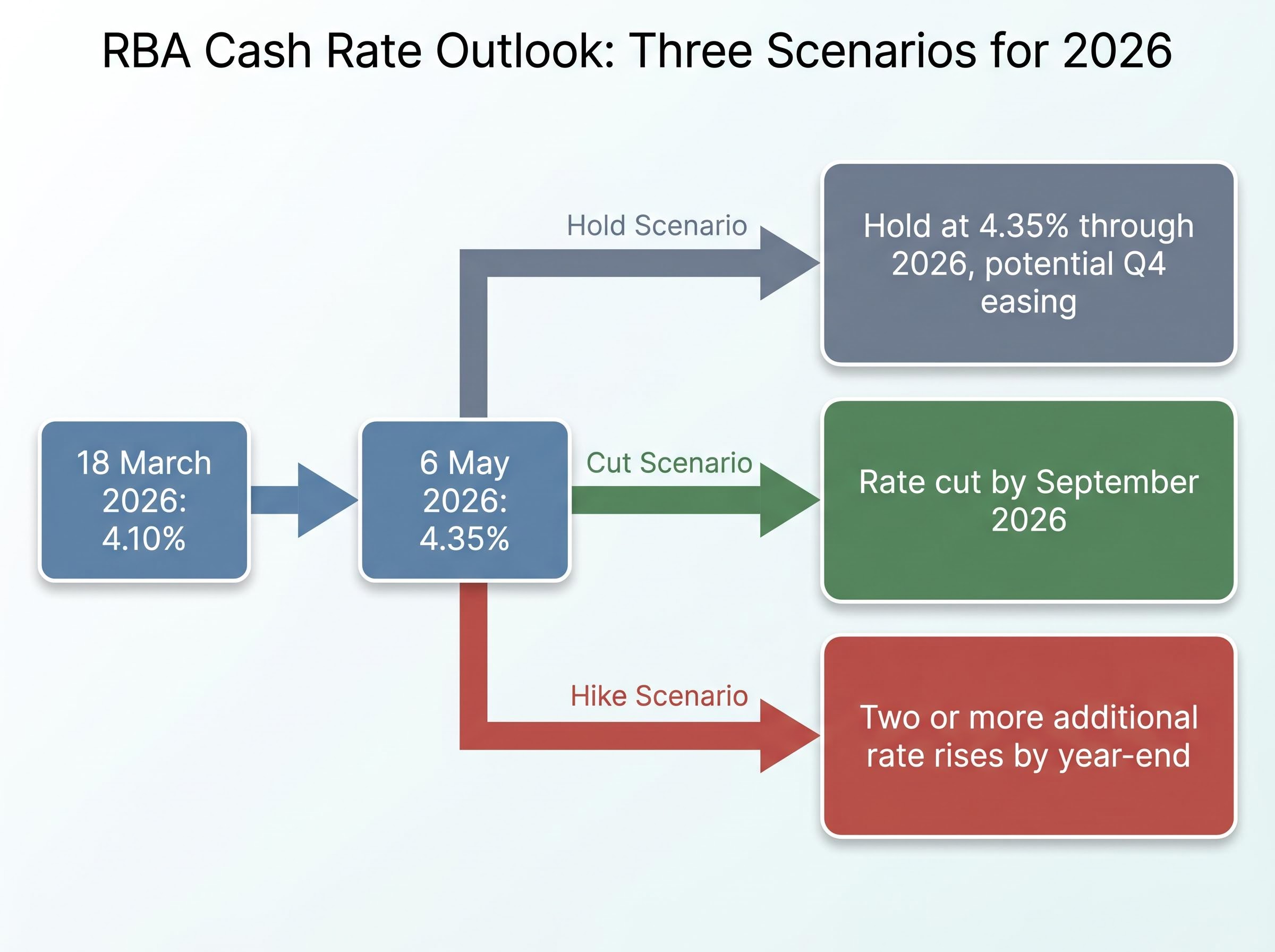

The RBA Board lifted the cash rate target to 4.35% on 6 May 2026, following an earlier increase to 4.10% on 18 March 2026. Both moves reflected persistent concern over sticky services inflation and a labour market that has refused to soften as quickly as the Board projected.

Where rates go from here is the question shaping every income decision made this year. The dominant analyst outlook clusters around three scenarios:

- Hold through 2026: CBA’s base case is for rates to remain at 4.35% for the remainder of the year. Westpac broadly agrees, projecting a hold through most of 2026 with a modest easing cycle beginning around Q4 if core inflation prints allow (as reported 9 May 2026).

- Late-2026 cut: A minority of forecasters, cited by The Australian on 15 May 2026, argue the RBA could cut as early as September 2026 if growth weakens further.

- Further hikes: A Reuters poll of economists from April 2026 found some forecasters expecting two or more additional rate rises by year-end, with the RBA’s 2-3% inflation target band still well above current readings in services categories.

CBA and Westpac base case: The cash rate is expected to remain on hold at 4.35% for the remainder of 2026, with any easing contingent on sustained progress in bringing inflation within the RBA’s 2-3% target band.

Here is the less obvious implication. Rising rates attract capital into term deposits, which can depress ASX share prices. Lower share prices, for companies maintaining or growing dividends, mechanically lift dividend yields. For income investors willing to accept equity risk, this dynamic can create better entry points than a lower-rate environment would offer.

When big ASX news breaks, our subscribers know first

What dividend investing actually means for Australian shareholders

How dividends are paid

Australian companies typically distribute a portion of their after-tax profits to shareholders twice per year, in the form of interim and final dividends. Not all companies pay dividends; those that do are generally mature, profitable businesses with stable cash flows. The payment is a direct transfer of cash (or additional shares, in the case of a dividend reinvestment plan) from the company to its shareholders.

How yield is calculated

Dividend yield is the annual dividend per share expressed as a percentage of the current share price. A simple worked example:

- A company pays a total annual dividend of $1.00 per share (interim plus final).

- Its current share price is $25.00.

- The trailing dividend yield is $1.00 / $25.00 = 4.0%.

This relationship moves in both directions. If the share price falls to $20.00 and the dividend remains unchanged, the yield rises to 5.0%. If the share price climbs to $30.00, the yield compresses to 3.3%. This is how the current rate environment, which has weighed on certain ASX share prices, can create higher yields for new buyers.

As of April-May 2026, the ASX 200 trailing dividend yield sits at approximately 4.0-4.3% on a cash basis, according to data from S&P Dow Jones Indices (Q1 2026: 4.0%), CommSec (4.2%), and Morningstar (4.3%). Individual stocks vary widely: Coles Group (COL) yields approximately 3.19%, while Brambles (BXB) sits around 2.99%.

Those are cash figures. For Australian shareholders, there is a second layer that lifts the effective return: franking credits.

Franking credits: the after-tax advantage that most investors underestimate

Australia’s dividend imputation system is the single most important structural feature distinguishing income investing on the ASX from income investing in almost any other market globally.

The mechanic works as follows. When an Australian company earns a profit, it pays corporate tax at 30%. When it distributes a dividend, it can attach a franking credit representing the tax already paid. The shareholder includes both the cash dividend and the franking credit in their taxable income, then uses the credit as a tax offset. If the credit exceeds the tax owed, the excess is refundable in cash for eligible individuals and SMSFs in pension phase.

The franking credit calculation follows a fixed formula: the cash dividend multiplied by 30 and divided by 70, reflecting the 30% corporate tax rate already paid at the company level, which means a $1,000 fully franked dividend carries an attached credit of $428.57 that eligible investors receive in full as a cash refund from the ATO.

The ATO rules on franking credit refunds for individuals confirm that where a shareholder’s basic tax liability is less than their total franking credits for the year, the excess is refunded in cash, making the imputation system particularly powerful for retirees and SMSF members in pension phase with little or no taxable income.

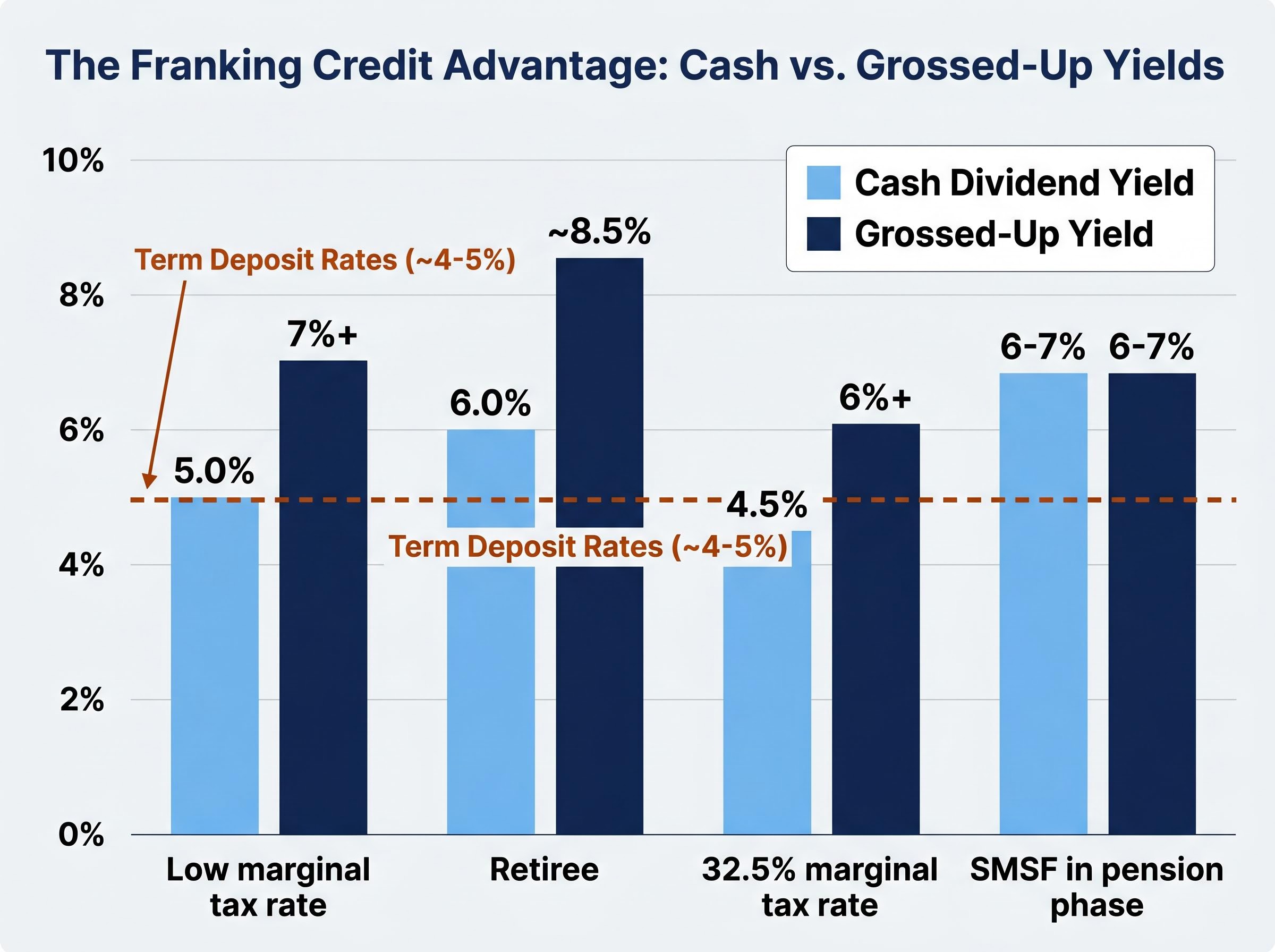

This means a 5% fully franked cash yield is not the full picture. The grossed-up yield, which represents the pre-tax equivalent return, is materially higher.

Peter Gardner of Plato Investment Management, writing in Livewire Markets in March 2025, noted that a 5% fully franked dividend yield can translate into a grossed-up yield above 7% for investors on lower marginal tax rates. For retirees with low taxable income, excess franking credits can be refunded directly, boosting after-tax income well beyond what bank deposits offer.

Dr Don Hamson, Managing Director of Plato Investment Management, stated in the Australian Financial Review in October 2024 that for many retirees, “a 6% fully franked yield equates to closer to 8.5% on a grossed-up basis,” which “comfortably tops the best-available term deposit rates even after accounting for risk.”

The following table illustrates how the advantage scales across different investor profiles:

| Investor Profile | Cash Dividend Yield | Grossed-Up Yield | Notes |

|---|---|---|---|

| Low marginal tax rate (0-19%) | 5.0% fully franked | 7%+ | Excess credits refundable or offset against minimal tax |

| Retiree (typical scenario) | 6.0% fully franked | ~8.5% | Per Plato/Hamson AFR October 2024 commentary |

| SMSF in pension phase (0% tax) | 6-7% portfolio | 6-7% (fully retained) | No tax payable; all credits refunded as cash |

| 32.5% marginal tax rate | 4.5% fully franked | 6%+ | Per Craig Meller, Money Management August 2024 |

Term deposit and savings account rates referenced in these comparisons sit at approximately 4-5%. For investors in the lower tax brackets, the comparison is not close.

On the policy front, no legislation since January 2024 has altered the dividend imputation system, franking credit refundability for individuals, or treatment for SMSFs in pension phase, according to Chartered Accountants Australia and New Zealand commentary on the 2025-26 Budget. A targeted integrity measure passed in late 2023 restricts companies from paying franked special dividends funded by capital raisings, but this is a company-level rule that does not affect ordinary dividend treatment for retail investors.

Income-focused ETFs and LICs generating 4-9% yields on the ASX in 2026

Understanding the theory is one step. Seeing what it looks like in practice is the next.

The following table summarises the key ASX-listed income vehicles discussed in Australian financial media through 2025 and into 2026, with yields as reported by the named sources:

| Ticker | Type | Cash Yield | Grossed-Up Yield | Key Note |

|---|---|---|---|---|

| VHY | ETF | ~5.5% | 7%+ | Broad high-yield Australian equities (Morningstar, April 2026) |

| IHD | ETF | ~6.0% | Not specified | Predominantly franked (Livewire, March 2026) |

| HVST | ETF | ~8-9% | Not specified | High capital volatility flagged (AFR, February 2026) |

| YMAX | ETF | ~7% | Not specified | Covered call strategy; mostly franked (AFR/Betashares, May 2025) |

| SYI | ETF | ~5.2% | Not specified | Select high dividend yield focus (Money magazine, June 2025) |

| PL8 | LIC | ~6.0% | ~7.0-7.5% | Income maximiser mandate (Livewire, November 2025) |

| ARG | LIC | ~4.0% | Not specified | Fully franked; long track record (The Australian, March 2025) |

| AFI | LIC | ~3.7% | Not specified | Fully franked; large-cap LIC (Morningstar, December 2025) |

ETFs for ASX dividend income

Rules-based high-yield ETFs such as VHY, IHD, and SYI screen for companies paying above-average dividends and weight portfolios accordingly. They offer diversified exposure to income-generating ASX stocks without the need to select individual names.

Option-overlay ETFs like YMAX use a covered call strategy, selling call options on underlying holdings to generate additional income. This can boost the distribution yield, but it caps upside participation if the underlying shares rally sharply. HVST targets the highest-yielding segment of the market and has delivered trailing yields of 8-9%, though the Australian Financial Review (February 2026) flagged significant capital value volatility as a trade-off that income investors relying on capital preservation should weigh carefully.

LICs for ASX dividend income

Listed Investment Companies operate differently from ETFs. They are closed-ended listed companies with a board, a mandate, and the ability to retain earnings in reserve. This reserve structure allows LICs to smooth distributions over time, drawing on retained profits in softer years to maintain or grow dividends.

PL8 (Plato Income Maximiser) targets income with a grossed-up yield of approximately 7.0-7.5%. ARG (Argo Investments) and AFI (Australian Foundation Investment Company) offer lower cash yields of 4.0% and 3.7% respectively, but both are fully franked and carry decades-long track records of consistent dividend payments. For income-dependent investors, the reliability of the distribution stream can matter as much as its size.

Building a passive income portfolio from ASX shares: practical starting points

The right mix of income vehicles depends on three factors that vary by investor: tax position, income target, and time horizon. Three broad profiles illustrate how these factors shape different approaches.

- The accumulator (working age, higher marginal tax rate): Franking credits still offset tax but the grossed-up advantage is smaller than for lower-bracket investors. Consider dividend reinvestment plans (DRPs), which automatically reinvest distributions into additional shares, compounding returns before the income draw-down phase begins. A broad ETF like VHY alongside selective blue-chip holdings can build the income base over time.

- The pre-retiree (moderate tax rate, transitioning toward income dependence): The grossed-up benefit strengthens as taxable income falls in retirement. Begin shifting allocation toward income-focused vehicles while maintaining some growth exposure. A combination of VHY or SYI with a LIC like ARG balances income and capital stability.

- The retiree or SMSF in pension phase (low or zero tax): Franking credits are at their most powerful here. Excess credits are refunded as cash. A diversified portfolio yielding 4-5%+ on a cash basis can deliver 6-8%+ on an after-tax, grossed-up basis, comfortably exceeding term deposit rates.

Owen Rask, CIO of Rask, has noted the complementary role of ETFs and LICs in passive income construction, with ETFs offering low-cost market exposure and LICs providing distribution smoothing.

A practical four-step construction sequence:

Payout ratio analysis is the most direct way to distinguish genuinely sustainable dividend streams from yields inflated by falling share prices or one-off special dividends, with a ratio above 100% indicating the company is distributing more than it earns, a pattern that rarely persists beyond one or two reporting cycles.

- Identify the target annual income needed from the portfolio.

- Assess tax position and the specific franking credit benefit at that marginal rate.

- Select a vehicle mix that matches the income target without concentrating in a single sector (banks, resources, and REITs dominate high-yield strategies, creating sector risk if held exclusively).

- Review diversification across individual holdings, sectors, and vehicle types. Stocks like BXB (yielding 2.99%, above its five-year average) and COL (3.19%, below its historical average) illustrate how individual blue-chip yields can signal different relative value at a given point in time.

For investors wanting to translate a target yield into a specific capital figure, our dedicated guide to living off dividends in Australia works through the ASFA comfortable retirement benchmarks and shows how franking credits reduce the portfolio size required, with SMSF pension-phase structures potentially lowering the capital target by several hundred thousand dollars relative to taxable accounts.

Dividend income in a high-rate world: what 2026 and beyond may hold for ASX income investors

The forward rate path creates two distinct scenarios for income investors, and each carries different portfolio implications:

- If rates hold at 4.35%: Term deposit rates remain elevated, narrowing the margin between cash and franked equity income. Franking credits still provide an after-tax advantage for lower-bracket investors and SMSFs, but the gap is tighter. Income investors in this scenario benefit from locking in equity yields at current levels, which reflect somewhat depressed ASX valuations.

- If rates ease from Q4 2026 onward: Term deposit rates compress at renewal. A term deposit maturing in six months may roll over at a lower rate. Dividend income from ASX shares, by contrast, does not expire at a maturity date. Companies maintaining their payout ratios continue distributing income regardless of the RBA’s direction. Westpac’s base case points to a modest easing cycle beginning around the December quarter of 2026, if inflation allows (as reported 9 May 2026).

ANZ Research has flagged a “non-trivial upside risk” of further hikes if labour market conditions fail to soften (as reported 10 May 2026), while the Australian Financial Review reported on 13 May 2026 that risks remain “skewed to rates staying higher for longer” due to sticky services inflation. The honest answer is that no one knows with certainty.

SMSF Adviser reported in September 2024 that several financial planners noted grossed-up franked yields of 6-7% from diversified equity portfolios remained competitive with deposit rates, even at elevated RBA rate levels, particularly for SMSFs in pension phase where tax is 0%.

Rate uncertainty itself carries a portfolio implication. Committing all income capital to term deposits at today’s rates creates reinvestment risk if the easing cycle arrives. A diversified ASX income portfolio does not face the same cliff.

The comparison between dividends versus term deposits sharpens considerably once reinvestment risk enters the analysis, because a term deposit locked in at today’s rates expires at maturity and may roll over at a lower rate if the RBA begins easing, while dividend income from companies maintaining their payout ratios does not carry an expiry date.

The case for ASX dividend income is structural, not cyclical

For most Australian income investors, the combination of 4-6% cash yields, franking credits that lift effective returns to 5.5-8.5% depending on tax position, and the stability of the imputation system makes dividend investing a durable income strategy rather than a rate-cycle trade. The advantage is structural: it exists because of how Australia taxes corporate earnings and distributes the benefit to shareholders, not because of where the RBA sets rates in any given quarter.

This guide did not cover individual stock selection, SMSF establishment, or personalised financial advice. Each of those areas warrants professional guidance tailored to individual circumstances. Owen Rask’s income-focused research, including analysis of 10 preferred income vehicles, offers a practical next step for readers looking to deepen their understanding.

The investors most likely to benefit from dividend income are those who begin building their portfolio with a clear framework, the right vehicle mix for their tax position, and a time horizon measured in years rather than rate cycles.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.