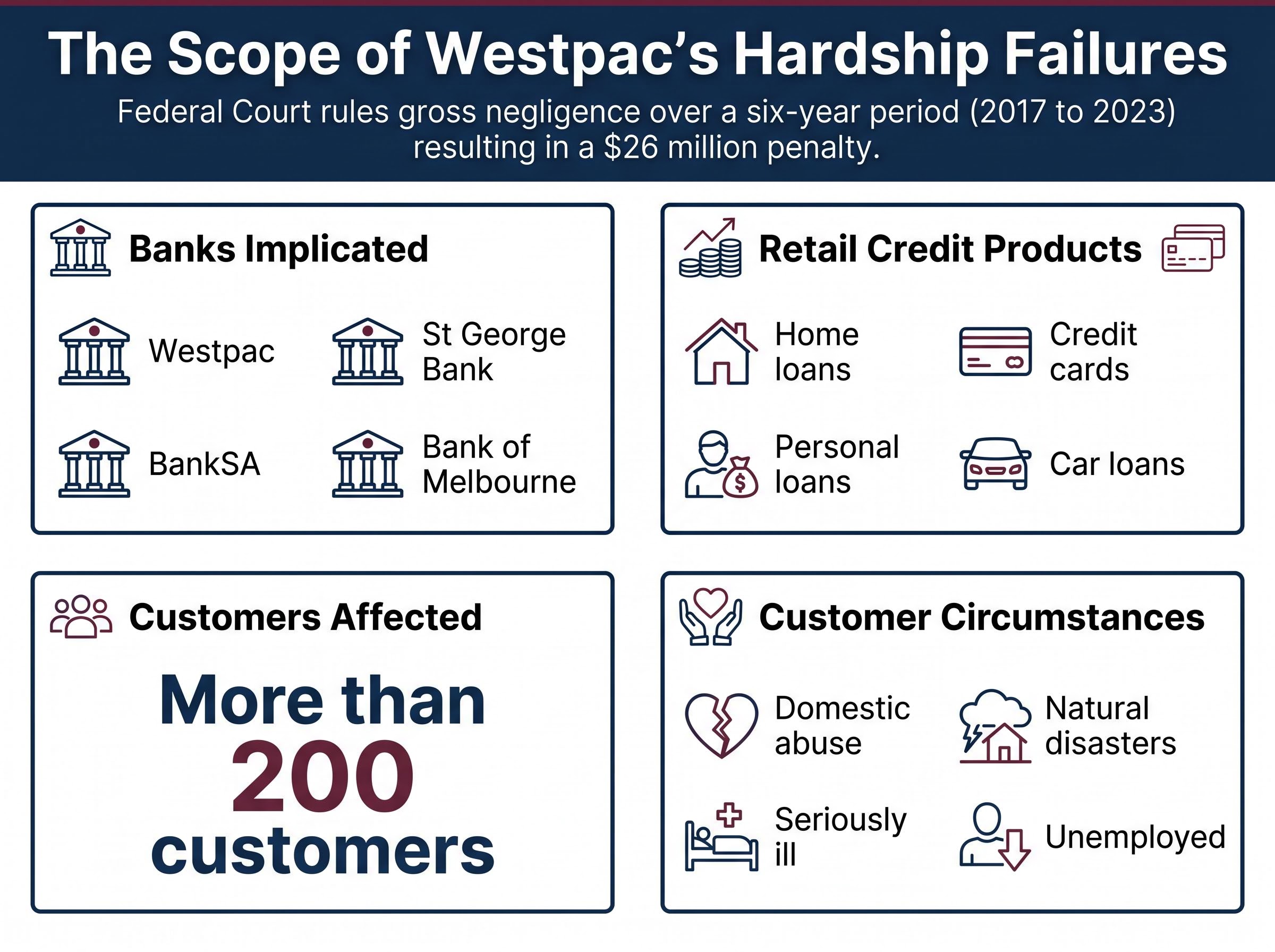

More than 200 Australians facing domestic abuse, serious illness, job loss, and natural disasters reached out to their bank for help. Westpac did not respond in time. A Federal Court has now ruled that failure was not just an oversight but gross negligence.

The ruling, handed down on 27 May 2026 by Federal Court Justice Timothy McEvoy, imposes a $26 million penalty on Westpac and extends across the bank’s three subsidiary brands. It covers nearly six years of systemic hardship processing failures, from 2017 to 2023. ASIC brought the case as part of its enforcement mandate around credit providers and vulnerable customer obligations.

What follows is a breakdown of what the court found, which customers were affected, how Australian credit law frames the bank’s obligations, how Westpac has responded, and what the ruling signals for banking accountability across the sector.

Federal Court finds Westpac grossly negligent in hardship failures spanning six years

The core findings of the Federal Court ruling are significant in both scale and classification:

- Penalty: $26 million imposed on Westpac

- Scope: More than 200 online hardship applications went unanswered within the legally required timeframe

- Duration: Failures spanned approximately six years, from 2017 to 2023

- Judicial classification: Conduct found to be grossly negligent, not merely negligent or inadvertent

Justice McEvoy’s classification matters. Gross negligence is not a finding that a system occasionally failed or that individual staff members made errors. It is a determination that the bank’s conduct fell so far below the standard required by law that it constituted a serious and sustained dereliction of its obligations under the National Credit Act.

Judicial classification: Federal Court Justice Timothy McEvoy found Westpac’s conduct was not intentional but was grossly negligent, a finding that places the failures well beyond isolated administrative error and into the territory of systemic institutional failure.

The case was brought by the Australian Securities and Investments Commission (ASIC), which pursued the matter as part of its broader enforcement focus on how credit providers handle hardship applications. At the centre of the breach was a specific failure: online hardship applications submitted by customers in genuine financial difficulty were not responded to within the timeframes required by Australian credit law. These were not ambiguous cases. The customers had identified themselves as being in hardship, and the bank’s systems did not process their requests in time.

When big ASX news breaks, our subscribers know first

Customers affected included domestic abuse victims, the seriously ill, and disaster survivors

Behind the legal classification sit the people the system failed. The more than 200 customers whose hardship applications went unanswered were not a homogeneous group. They included individuals in some of the most difficult circumstances a person can face:

- Domestic abuse survivors seeking financial separation from abusive partners

- Natural disaster victims dealing with the financial aftermath of catastrophic events

- Seriously ill customers managing treatment costs and income disruption

- Unemployed individuals who had lost their primary source of income

Each of these categories carries its own urgency. A domestic abuse survivor requesting hardship assistance may be attempting to secure financial independence as part of leaving a dangerous situation. A delay of weeks or months is not an inconvenience; it is a material failure at the point of greatest vulnerability.

Failures spanned Westpac’s entire retail banking group

The failures were not confined to Westpac’s primary brand. Three subsidiary banks were also implicated: St George Bank, BankSA, and Bank of Melbourne. Across the group, the affected products included home loans, credit cards, personal loans, and car loans, meaning the failures cut across the full spectrum of retail credit products rather than sitting within a single portfolio.

What Australian credit law requires from banks when customers ask for help

The legal obligations that Westpac breached are not discretionary. They are codified in the National Credit Act, which sets out specific requirements for how credit providers must handle hardship applications from customers in financial difficulty.

A compliant hardship response follows a defined sequence:

- Receipt and acknowledgment: The lender must acknowledge receipt of a hardship application within a specified timeframe.

- Assessment: The lender must assess the customer’s circumstances and determine what hardship arrangements may be appropriate.

- Outcome communication: The lender must inform the customer of the outcome, whether the application is approved, modified, or declined, within the legally prescribed period.

These steps are not suggestions. They are legal obligations, and failure to meet them constitutes a breach of the credit provider’s licence conditions.

Regulatory priority: ASIC’s Corporate Plan 2024-28 explicitly lists “credit providers’ compliance with hardship and vulnerable customer obligations” as an enforcement priority, signalling that the regulator views this area as an active and continuing focus for surveillance and enforcement action.

ASIC Report 781, published in September 2023 and titled “Hardship practices of lenders,” documented systemic failures across bank hardship processes well before this ruling. That report foreshadowed further enforcement action and placed the banking sector on notice that hardship processing was under active regulatory scrutiny.

The Money3 case illustrates the same enforcement logic: ASIC pursued responsible lending breaches through the Federal Court, secured a penalty explicitly designed to deliver general deterrence across all Australian credit licensees, and identified vulnerable and First Nations consumers as the population most exposed to the underlying conduct.

ASIC Report 783 on lender hardship practices, published in May 2024 following a review of large home loan lenders, documented systemic shortfalls in how banks identify, assess, and respond to customers seeking hardship assistance, providing the evidentiary foundation that preceded the Westpac enforcement action.

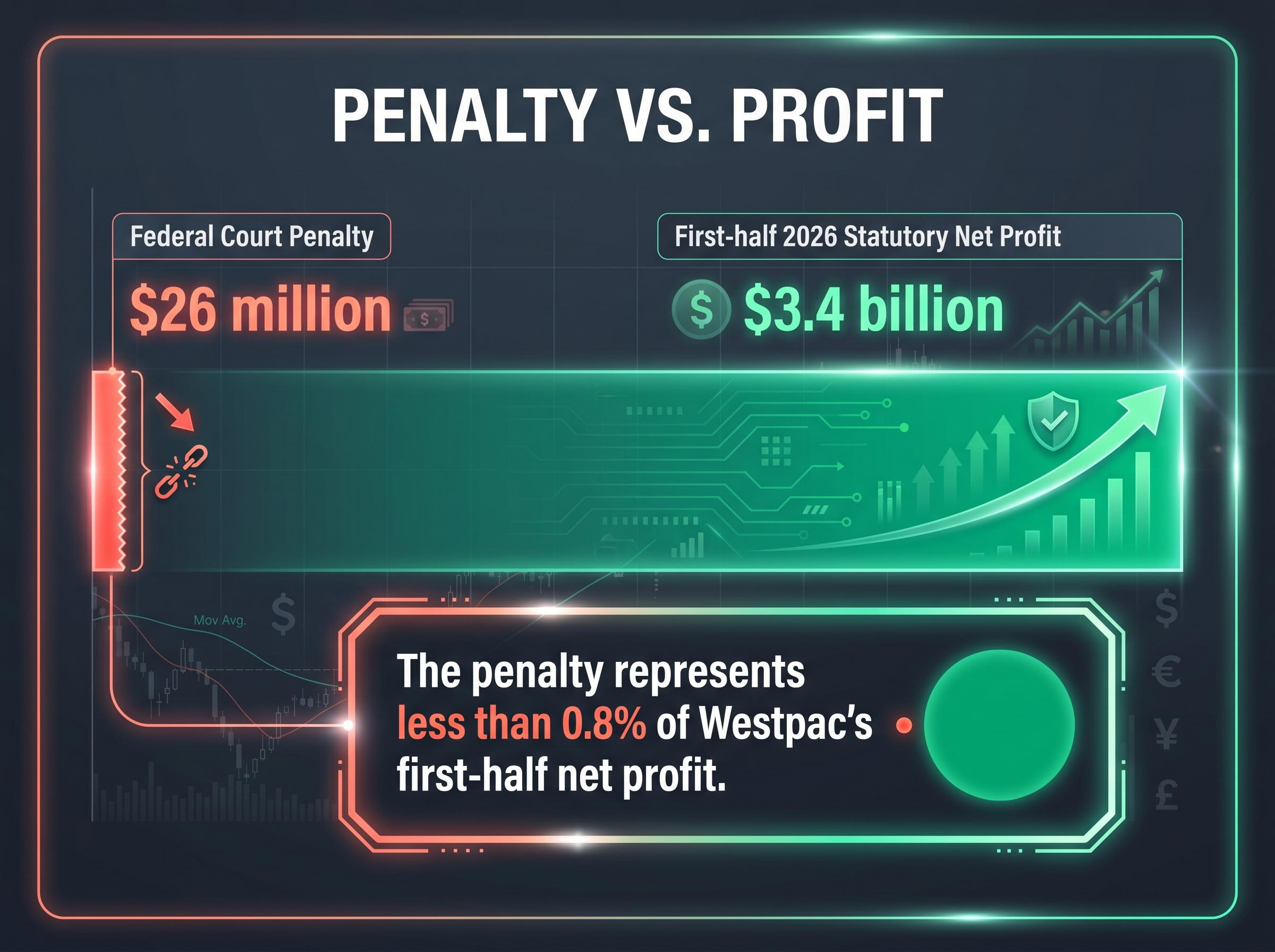

A $26 million penalty in the context of a $3.4 billion profit

The $26 million penalty is the largest figure in the ruling. It is not the largest figure in Westpac’s financial statements.

| Metric | Figure |

|---|---|

| First-half 2026 statutory net profit | $3.4 billion (up 3% on prior year) |

| Federal Court penalty | $26 million |

| Share price (27 May 2026) | $35.96 (down approximately 1.78%) |

| Year-to-date share performance (2026) | Down approximately 7% |

| 12-month share performance | Up approximately 13% |

| Interim dividend | 77 cents per share, fully franked, payable 26 June 2026 |

The $26 million penalty represents less than 0.8% of Westpac’s first-half net profit of $3.4 billion. Whether a penalty at this scale changes institutional behaviour is a question the numbers leave open.

Westpac shares declined approximately 1.78% to $35.96 on 27 May 2026. The stock is down roughly 7% year-to-date but remains approximately 13% higher over the prior 12 months. The bank declared an interim dividend of 77 cents per share, fully franked, payable on 26 June 2026, as part of its first-half results announced on 5 May 2026.

Australian bank shares were already under pressure before the Westpac ruling arrived, with the four major banks collectively allocating approximately $800 million in additional loan loss provisions during the most recent reporting season as RBA rate movements and an energy price shock compressed earnings from multiple directions.

The market’s reaction was measured. For investors assessing whether this penalty constitutes a financial deterrent or a manageable line item, the ratio between the sanction and the profit speaks plainly.

Westpac’s apology and the steps it says it has already taken

Westpac has expressed deep regret for the failures identified by the court, apologising to the customers whose hardship applications were not handled within the required timeframes.

The bank has described a remediation programme that it states is now complete, covering three categories of action:

- Fee refunds for charges applied during the period when hardship applications should have been under assessment

- Debt waivers for affected customers where outstanding balances were linked to the processing failures

- Compensation payments to customers impacted by the delays

System upgrades and process changes following the failures

Beyond direct customer remediation, Westpac states it has made changes to the systems and processes that allowed the failures to occur. The bank has described enhancements to its internal hardship processing workflows and upgrades to its online hardship support infrastructure.

These changes were implemented during the remediation period, prior to the court ruling itself. Whether completed remediation and system upgrades alter the accountability calculus is a judgment the ruling leaves to the reader. The court’s finding of gross negligence stands alongside the bank’s assertion that the failures have been addressed.

The next major ASX story will hit our subscribers first

A ruling that puts every major bank’s hardship processes under the spotlight

This ruling carries implications well beyond Westpac.

ASIC pursued this case against one of Australia’s four largest banks, secured a gross negligence finding, and obtained a $26 million penalty. The enforcement action covered all four major retail credit product categories: home loans, credit cards, personal loans, and car loans. The signal to other credit providers is direct.

ASIC Corporate Plan 2024-28: The regulator has listed “credit providers’ compliance with hardship and vulnerable customer obligations” as an enforcement priority, indicating that surveillance and enforcement action in this area will continue.

ASIC Report 781, published in September 2023, had already documented systemic failures across bank hardship processes more broadly. The Westpac ruling now provides a concrete enforcement outcome that demonstrates the regulator’s willingness to pursue these failures through the courts.

ASIC’s November 2025 preliminary findings from its motor vehicle finance review identified hardship communication failures as one of four systemic failure patterns across the sector, placing inadequate hardship processes alongside unaffordable loans and excessive fees as the regulator’s primary concerns well before the Westpac ruling landed.

ASIC’s proceedings against NAB for hardship failures, filed in November 2024, confirm that the regulator’s enforcement focus extends across the major bank sector rather than targeting a single institution, reinforcing the view that the Westpac ruling is a sector-wide signal rather than an isolated outcome.

The implications for the sector can be summarised in three points:

- Regulator intent is clear. ASIC has demonstrated it will pursue hardship failures to Federal Court penalties, not just surveillance letters.

- Product scope is broad. The case covered home loans, credit cards, personal loans, and car loans, meaning no retail credit product line sits outside the enforcement perimeter.

- The gross negligence standard is now set. Systemic, multi-year failures to respond to hardship applications can attract a gross negligence classification, not just a finding of administrative non-compliance.

Gross negligence, $26 million, and what Australian banks owe their most vulnerable customers

More than 200 customers asked for help. They were facing domestic abuse, serious illness, unemployment, and natural disasters. For nearly six years, Westpac’s systems did not respond in time, and a Federal Court has classified that failure as gross negligence.

The $26 million penalty is paid. The remediation programme is described as complete. The question that remains is whether the regulatory and reputational consequence is sufficient to change how Australia’s largest banks resource and design their hardship systems. ASIC’s Corporate Plan makes clear that enforcement in this area is not finished.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.