Negative Gearing, CGT and Trust Tax: the 2026 Budget Reforms

19 mins ago

A proposed change to how capital gains are taxed in Australia has the potential to affect the retirement plans of millions of property investors, trust beneficiaries, and ordinary shareholders. The measure, flagged in the federal budget context, would introduce a minimum 30% effective tax rate on capital gains, functioning as a floor that overrides the standard 50% CGT discount long-term investors currently rely on. If legislated, it would reach into some of the most common investment and estate planning structures in the country, from testamentary trusts to properties held under the six-year main-residence rule. Yet the proposal’s legislative status remains genuinely unclear, and the political environment surrounding it adds a second layer of uncertainty. Acting prematurely on Australian capital gains tax changes could prove as costly as ignoring them entirely. What follows explains what is currently known about the proposal, how it would interact with existing CGT rules, which planning strategies face the greatest disruption, and why the period of uncertainty itself demands careful consideration.

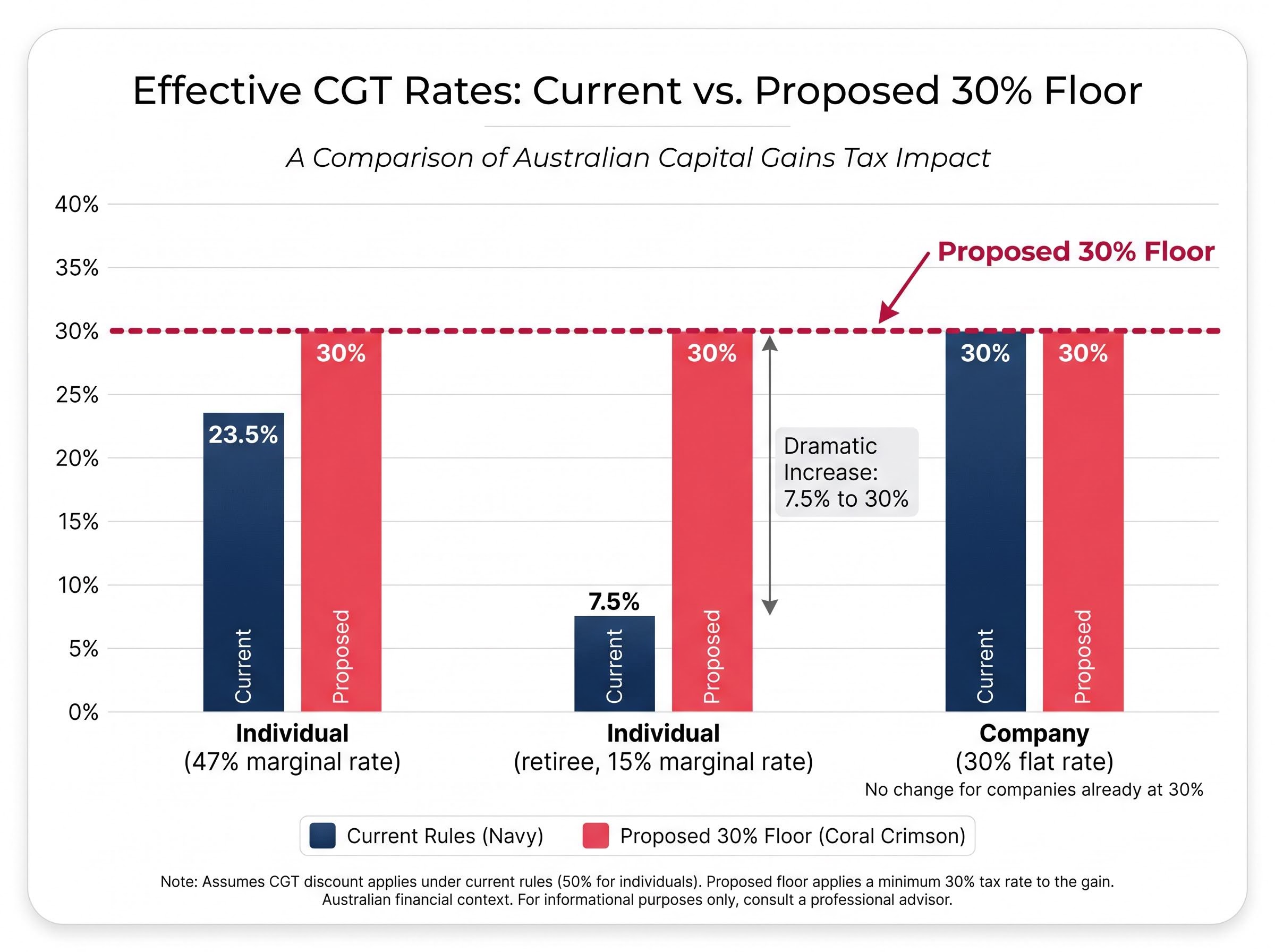

The existing CGT framework gives individuals a 50% discount on capital gains for assets held longer than 12 months. In practice, this means the gain is halved before being added to the taxpayer’s assessable income and taxed at their marginal rate. An individual on the top marginal rate of 47% (including the Medicare levy) therefore pays an effective CGT rate of approximately 23.5% on a long-term capital gain.

The ATO’s CGT discount rules confirm that individuals who are Australian tax residents and have held an asset for at least 12 months are entitled to reduce their capital gain by 50% before it is included in assessable income, a concession that sits at the centre of most long-term investment strategies.

The retirement-timing strategy builds on this foundation. By deferring the sale of a property or share portfolio until a year when taxable income is lower, typically the first year of retirement, investors can push their marginal rate well below 47%, compressing the effective CGT rate further. A retiree on a 15% marginal rate, for instance, pays just 7.5% effective CGT under current rules.

Companies, by contrast, receive no CGT discount and pay a flat 30% rate on capital gains. This distinction matters: it is the gap between companies at 30% and individuals who can achieve rates below 30% that the proposed change is designed to close.

The 30% floor discussed here is only part of the structural change confirmed in the 12 May 2026 federal budget; the CGT rules from 1 July 2027 also replace the 50% discount with CPI-based cost base indexation, a separate mechanism that will affect how taxable gains are calculated on every asset disposal after the transition date, and superannuation funds are explicitly excluded from the new framework.

| Taxpayer type | Effective CGT rate (current rules) | Effective CGT rate (proposed 30% floor) |

|---|---|---|

| Individual (47% marginal rate) | 23.5% | 30% |

| Individual (retiree, 15% marginal rate) | 7.5% | 30% |

| Company (30% flat rate, no discount) | 30% | 30% (no change) |

Discretionary and testamentary trusts pass income and capital gains through to beneficiaries, who are then taxed at their own marginal rates. This creates the planning opportunity the proposed change targets: by distributing gains to beneficiaries on low or zero incomes, including minor beneficiaries of testamentary trusts who are taxed at adult marginal rates rather than penalty children’s rates, families can shelter significant income. Two minor beneficiaries can collectively receive up to $36,000 annually tax-free (up to $18,200 each at the tax-free threshold).

Companies, already taxed at 30% with no CGT discount, sit precisely at the proposed floor. The change therefore has no effect on corporate structures.

The proposal functions as a floor, not a replacement rate. It would not alter an investor’s marginal tax rate or the mechanics of the 50% discount. Instead, it would prevent the effective rate on capital gains from falling below 30%, regardless of the taxpayer’s income in the year of sale.

The distinction matters most for retirement-timing strategies. Under current rules, an investor who holds a property for 25 years and sells in their first year of retirement, when taxable income may be minimal, can achieve an effective CGT rate in the single digits. The proposed floor would set 30% as the minimum, eliminating the tax benefit of timing the sale to coincide with a low-income year. A retiree on a 15% effective marginal rate could no longer reduce CGT liability below 30%.

The measure is reported to raise approximately $5-6 billion in its first year of implementation, a figure that signals how broadly the government expects it to reach across individual and trust-based investment structures.

Three categories of taxpayer face the most direct exposure:

The $250 payment to working Australians is cited as one of the expenditure items the measure is designed to fund, placing the CGT floor within a broader fiscal rebalancing argument.

Trusts already in existence at budget night are reportedly exempt from the 30% minimum. At first glance, this looks like relief for families with existing estate planning structures.

The limitation becomes clear on closer examination. Testamentary trusts can only be created upon someone’s death, which means the exemption cannot be locked in by any living person today. A testamentary trust that does not yet exist because the Will-maker is still alive receives no guaranteed protection under the reported grandfathering provision.

Under current rules, testamentary trusts allow minor beneficiaries to be taxed at adult marginal rates rather than the penalty rates that normally apply to children’s unearned income. This means a family with two minor beneficiaries can shelter up to $36,000 annually (up to $18,200 per child at the tax-free threshold). The proposed floor would compress or eliminate this advantage for trusts established after the budget night reference point.

Anyone with a current Will or estate plan built around the expectation that a future testamentary trust will access the CGT discount at rates below 30% faces a planning gap. The trust does not yet exist, so it cannot be grandfathered. The exemption for pre-existing trusts offers no protection.

Professional legal and tax advice is warranted before restructuring, however. Redesigning a Will or trust structure in anticipation of legislation that has not yet passed carries its own cost, particularly if the legislation is later amended or abandoned. The timing question explored in the legislative uncertainty section below applies here with particular force.

The six-year rule allows a property to retain its main residence CGT exemption for up to six years while being rented out. This is one of the most practically important CGT strategies for ordinary property owners, particularly those who relocate for work or choose to rent where they live while holding a former home as an investment.

The conditions required to access the rule are specific:

The ATO guidance on the main residence six-year rule confirms that owners can continue to treat a former home as their main residence for up to six years when it is used to produce income, provided no other property is nominated as the main residence during that period.

Properties already owned at the time of the budget announcement are reportedly exempt from the proposed changes, even if subsequently converted to investment properties. This grandfathering provision would, if confirmed, protect existing “rentvestors” and relocating homeowners.

The reported exemption for properties already owned at budget night has not been confirmed in final legislation. Property owners should not rely on this provision without obtaining professional advice, as the boundaries of the grandfathering remain undefined pending legislative passage.

The broader investor behaviour question is whether the 30% effective CGT floor changes the hold-or-sell calculus for long-held investment properties. For investors close to retirement who had planned to sell during a low-income year, the removal of timing-based tax advantages may bring forward sale decisions, or at least prompt a reassessment of the after-tax return on continued holding.

City-level variation in CGT outcomes under the new indexation model is substantial: PropTrack analysis found roughly a quarter of property investors who generated a gain over the past decade would have paid less tax under indexation than under the existing 50% discount, with Melbourne investors more likely to benefit and Brisbane investors more likely to face a larger bill.

The proposed 30% CGT floor has not been legislated. As of May 2025, no final legislation has passed, and the measures remain at the proposal stage. This distinction carries practical weight for any investor considering structural changes to their portfolio or estate plan.

Opposition figures, including Angus Taylor, have signalled intent to repeal the measures if elected. While the specifics of any formal repeal commitment remain subject to political developments, the signal itself creates a genuine possibility that the 30% floor may not survive a change of government.

Tax legislation changes are reversible. Physical asset disposals are not. An investor who sells a property to avoid a proposed tax change, only for that change to be repealed or substantially amended, cannot undo the sale. The asymmetry between the reversibility of legislation and the irreversibility of asset transactions deserves weight in any planning decision made during this period.

Separating tax policy noise from genuine legislative signal is a skill that has material dollar value in 2026: research across three concurrent tax events in South Korea, the Netherlands, and Australia found that markets historically over-discount tax policy risk at announcement and partially re-rate as legislative uncertainty resolves, meaning investors who move on a proposal rather than a law often sell into a trough they did not need to enter.

The dividend preference shift offers a useful illustration of premature action. If investors rotate toward high-dividend equities and away from capital-growth assets to reduce future CGT exposure, they are already making allocation decisions based on a law that does not yet exist. Australia’s investment return profile already skews toward income: historically, at least 50% of returns have been derived from income rather than capital growth, compared to international markets where capital growth accounts for roughly 80%. A further tilt toward dividends, driven by a proposal rather than legislation, could produce portfolio concentration at precisely the wrong moment.

Three considerations for investors weighing whether to act before legislation is finalised:

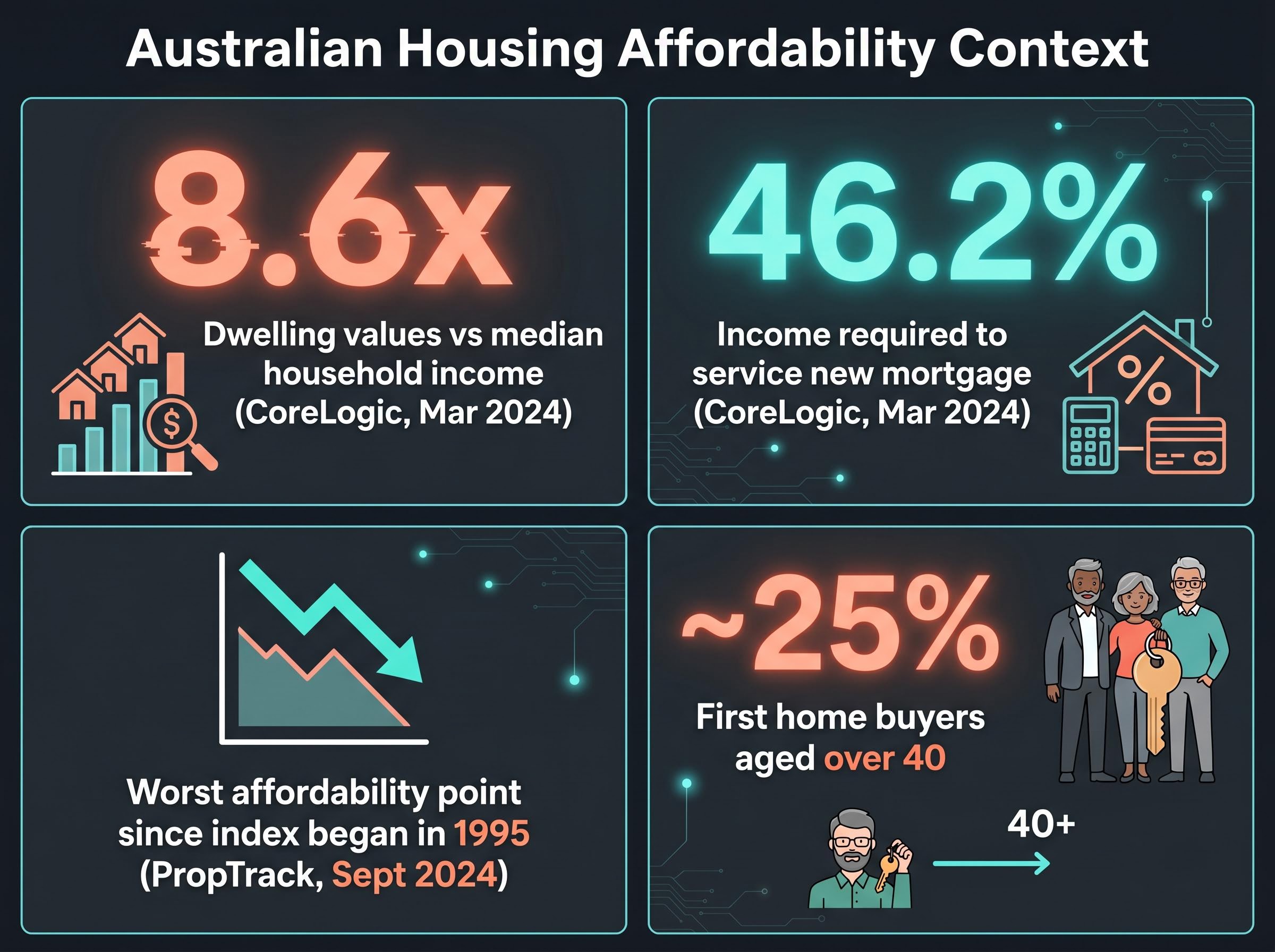

The CGT debate sits within a broader housing affordability picture that has deteriorated markedly. According to CoreLogic’s June 2024 Housing Affordability Report, national dwelling values averaged 8.6 times median household income as at the March quarter 2024. The portion of household income required to service a new mortgage reached approximately 46.2% over the same period.

According to CoreLogic, approximately 46.2% of household income was required to service a new mortgage as at March 2024, a figure that reflects affordability pressure at or near record levels.

PropTrack’s Housing Affordability Index, published in September 2024, assessed affordability as at its worst point since the index began in 1995. Commentary across multiple sources suggests the average first home buyer is now approaching their late 30s, with some indicative data pointing to roughly 25% of first home buyers being aged over 40, though these figures have not been confirmed by ABS releases and should be treated as directional rather than definitive.

The policy tension is genuine. CGT discounts and negative gearing are widely understood to have contributed to investor demand for established housing, but limiting or removing these concessions may not automatically translate into affordability improvements if supply constraints remain the binding factor.

First home buyers who purchase an investment property first, the rentvesting strategy, forfeit access to several government incentives:

This creates a structural tension: the rentvesting approach, which the CGT discount currently supports, sits outside the government support framework designed to help first home buyers enter the market.

The proposed 30% minimum CGT floor is a structurally significant measure if legislated, capable of altering the after-tax returns on strategies that millions of Australians have relied on for decades. Its path to law, however, remains uncertain, and the planning decisions it prompts deserve careful rather than reactive consideration.

Three categories of reader face the most immediate exposure: investors in long-held property planning to sell near retirement, families with testamentary trust structures embedded in existing Wills, and younger investors at the rentvesting or first-home stage navigating conflicting incentives between investment flexibility and government support.

The most important step for affected investors is to seek qualified tax and legal advice before making structural changes to portfolios, property holdings, or estate plans. Revisiting those decisions once the legislation is either passed or definitively abandoned will be far less costly than restructuring around a proposal that may never take its current form.

For investors who want to understand why the government’s chosen mechanism may still distort long-term investment decisions even after the floor is applied, our deep-dive into the CGT reform design flaws models how the indexation-plus-floor approach produces a tax bill more than $100,000 higher than a tapered alternative on a $100,000 portfolio over 20 years, and examines why the 12-month cliff that rewards threshold-crossing over genuine patience is left untouched.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The legislative proposals discussed remain subject to change, and specific tax outcomes depend on individual circumstances.

The proposed 30% minimum CGT floor is a measure that would set a minimum effective tax rate of 30% on capital gains, preventing investors from using the existing 50% CGT discount to reduce their effective rate below that level regardless of their marginal tax rate or income in the year of sale.

Under current rules, retirees can time the sale of long-held assets to coincide with low-income years, potentially reducing their effective CGT rate to single digits. The proposed 30% floor would eliminate this advantage by setting a minimum rate that applies regardless of the investor's taxable income in the year of sale.

Properties reportedly owned at the time of the budget announcement may be grandfathered and exempt from the proposed changes, but this provision has not been confirmed in final legislation and the boundaries of any grandfathering remain undefined pending legislative passage.

Trusts already in existence at budget night are reportedly exempt, but testamentary trusts can only be created upon death, meaning anyone whose Will-maker is still alive cannot lock in that exemption today and faces a genuine planning gap under the proposed rules.

As of May 2025, the proposed 30% minimum CGT floor has not been legislated and remains at the proposal stage. Opposition figures have signalled intent to repeal the measures if elected, meaning the law may not survive in its current form.