Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

1 hr ago

Twenty-seven ASX 200 stocks hit fresh 52-week lows in the week ending 22 May 2026, with Brambles alone shedding more than 20% in a single session, one of the company’s worst single-day falls on record. The ASX 200 was already trading 6-8% below its March 2026 all-time high, but the week’s damage was concentrated and qualitatively different. Four sectors recorded zero new highs while accumulating new lows, and the Brambles guidance shock arrived alongside Webjet’s earnings collapse to reinforce a narrative of deteriorating corporate fundamentals rather than mere index-level drift.

What follows maps the specific catalysts behind each pocket of weakness, presents the full breadth data sector by sector, and addresses the question that matters most for investors with exposure to these names: is this concentrated selling a sign of approaching capitulation, or does further downside remain likely across the ASX’s worst-performing sectors?

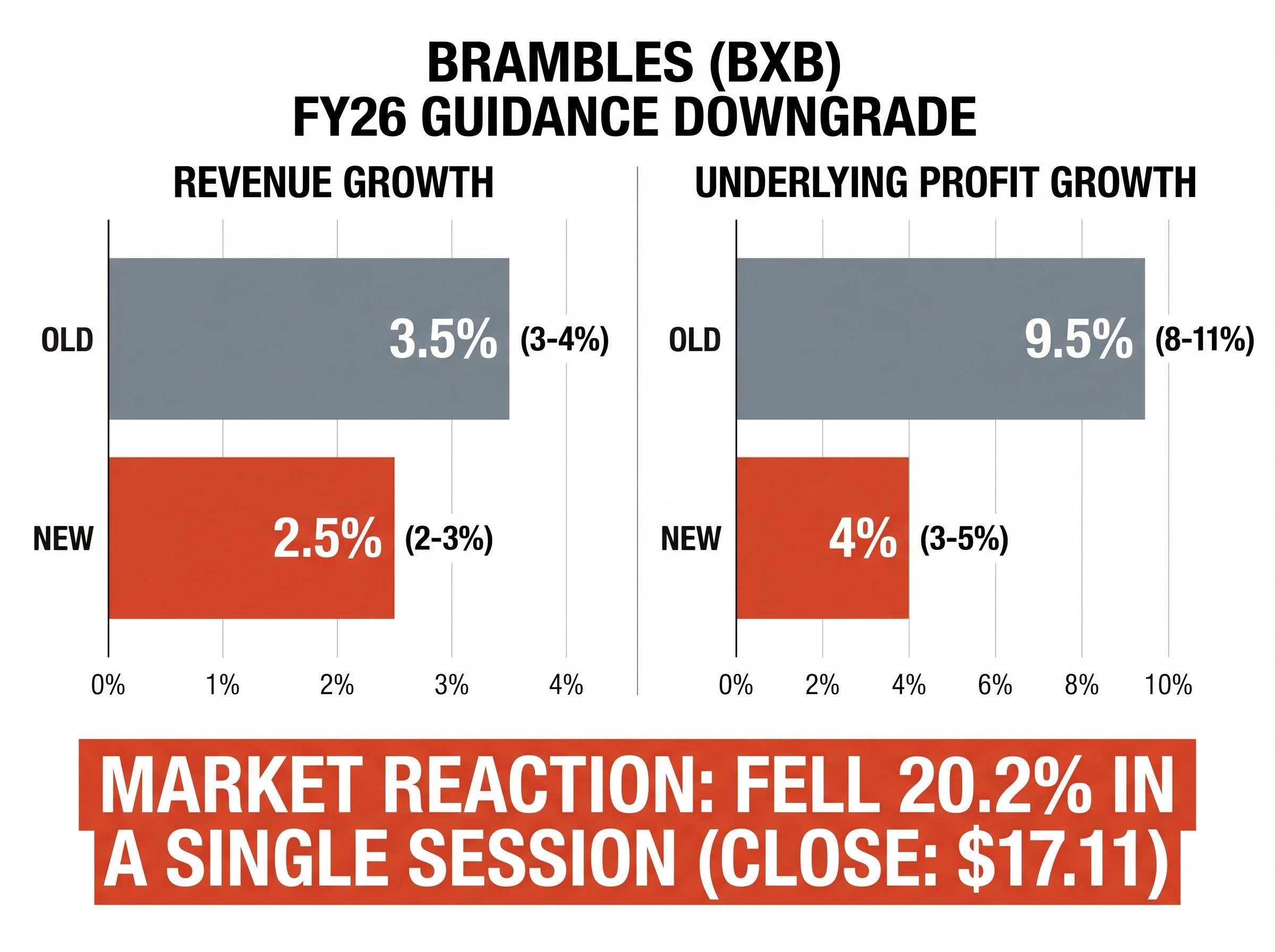

The scale of the move demands attention first. Brambles (BXB) fell 20.2% in a single session, closing the week at $17.11, down 22.6% for the week and 25.0% over the prior twelve months. The stock reached a new 52-week low as of 22 May 2026. A decline of this magnitude in a company of Brambles’ market capitalisation is not a routine downgrade reaction; it ranks among the largest single-day falls in the company’s listed history.

The numbers behind the shock explain why. Management cut its FY26 guidance across both headline metrics:

The downgrade was attributed to repair-capacity constraints that prevented Brambles from meeting demand that had exceeded prior expectations, an operational execution failure rather than a demand problem.

The gap between the old and new profit guidance is not a rounding error. Moving from 8-11% growth to 3-5% represents a fundamental reassessment of near-term earnings power. Broker commentary, including from Macquarie, flagged concerns around earnings quality and cost inflation risk, though specific target price revisions were not publicly confirmed. For investors holding BXB, the question now is whether repair-capacity constraints are temporary or structural.

The Consumer Discretionary sector recorded 8 new 52-week lows and zero new highs in the week ending 22 May 2026. That ratio is not a stock-picking story. It is a breadth failure.

ASX market breadth deterioration was already accelerating before this week’s damage: 22 index constituents hit 52-week lows in the week ending 1 May 2026, double the prior week’s tally, even as the headline ASX 200 fell just 0.65%, a textbook divergence between surface-level index moves and underlying selling pressure.

Webjet (WEB) provided the week’s sharpest individual catalyst, falling 11% in a single session on its FY26 results.

Webjet’s OTA bookings declined 12% year-on-year, while total transaction value (TTV) fell 15% year-on-year, a result that confirmed weakening demand across Australia’s online travel market.

The selling pressure cut across distinct sub-categories: travel (Webjet, Flight Centre, Web Travel Group), retail (Premier Investments, Harvey Norman, Nick Scali), education (IDP Education), and automotive accessories (ARB Corporation). When every sub-category within a sector is simultaneously making new lows, the selling is systemic rather than idiosyncratic.

| Company | Ticker | Weekly Close | Weekly Change (%) | 12-Month Change (%) |

|---|---|---|---|---|

| IDP Education | IEL | $2.67 | New 52-week low | -67.5% |

| Web Travel Group | WEB | $2.32 | -11% (single session) | -50.4% |

| Premier Investments | PMV | $11.71 | New 52-week low | -44.1% |

| ARB Corporation | ARB | $18.05 | New 52-week low | -41.1% |

| Nick Scali | NCK | $13.38 | New 52-week low | -28.5% |

| Flight Centre | FLT | $10.02 | New 52-week low | -24.0% |

| Harvey Norman | HVN | $4.39 | New 52-week low | -17.5% |

| Tabcorp | TAH | $0.68 | New 52-week low | -5.6% |

For investors with any Consumer Discretionary exposure, the breadth data signals that there is currently no safe corner within this sector.

The sector-level damage above is not a valuation anomaly or a sentiment blip. It reflects genuine household financial stress that macroeconomic data has been confirming for months.

The Reserve Bank of Australia held the cash rate at 4.35% at its May 2026 Monetary Policy Decision, keeping monetary policy firmly restrictive. The RBA’s own communications are direct about the consequences.

The RBA’s May 2026 Monetary Policy Statement confirms that consumption growth is being constrained by fuel prices eroding disposable incomes, providing the official macro backdrop against which the sector-wide breadth deterioration in Consumer Discretionary, Staples, and Real Estate must be understood.

According to the RBA’s May 2026 statement, “consumption growth remains subdued,” with high inflation and interest rates “weighing on real incomes and household spending.”

Australian Bureau of Statistics (ABS) retail turnover data corroborates this. Monthly retail growth remained soft through 2025 and into 2026, with consumers reducing discretionary spending, particularly on household goods and apparel, and trading down to private-label alternatives. The Westpac-Melbourne Institute Consumer Sentiment Index rose 3.5% in the prior week, but this recovery came from extremely pessimistic levels, a bounce from a low base rather than a trend reversal.

Four headwinds are operating simultaneously:

This matters because the recovery timeline is set by the rate cycle. Consumer Discretionary, Real Estate, and related sectors cannot durably recover until the RBA pivots, and that threshold has not yet been reached.

The four headwinds listed above are intensified by household stress building beneath the GDP headline: corporate insolvencies set an all-time record in 2025, diesel prices nearly tripled from January to late April following the Strait of Hormuz closure, and per capita GDP growth of roughly 0.4% in Q4 2025 confirmed that aggregate output figures were masking a deterioration in individual living standards that is directly relevant to discretionary spending capacity.

The damage extended well beyond Consumer Discretionary last week. Health Care, Real Estate, Consumer Staples, and Technology each contributed new 52-week lows with zero new highs, establishing that the weakness is cross-market rather than confined to a single sector.

The most severe annual declines carry real weight. Lendlease (LLC) closed at $2.82, down 51.1% over the year. Seek (SEK) closed at $12.71, down 46.6%. Tuas (TUA) fell 62.1% in a single week, though its collapse was driven by a deal-specific catalyst (the termination of the M1 acquisition agreement and suspension of the Singapore regulatory review) that distinguishes it from macro-driven declines.

| Sector | Company | Ticker | Weekly Close | 12-Month Change (%) |

|---|---|---|---|---|

| Health Care | Sonic Healthcare | SHL | $18.68 | -28.8% |

| Health Care | Fisher & Paykel | FPH | $27.65 | -19.0% |

| Health Care | Ansell | ANN | $26.25 | -16.6% |

| Real Estate | Lendlease | LLC | $2.82 | -51.1% |

| Real Estate | Stockland | SGP | $3.97 | -27.4% |

| Consumer Staples | GrainCorp | GNC | $4.76 | -36.1% |

| Consumer Staples | A2 Milk | A2M | $5.66 | -31.0% |

| Consumer Staples | Endeavour Group | EDV | $3.08 | -24.1% |

| Consumer Staples | Elders | ELD | $5.88 | -7.0% (YoY); -18.3% (week) |

| Technology | Seek | SEK | $12.71 | -46.6% |

| Technology | Iress | IRE | $5.73 | -32.4% |

| Technology | Tuas (deal-specific) | TUA | $2.31 | -62.1% (week) |

The spread of new lows into Health Care and Staples, traditionally the market’s defensive anchors, signals that even capital-preservation strategies are being tested. There are few reliable shelters within the domestic equity market at present.

The count of new 52-week lows rose to 27 in the week ending 22 May 2026, up from 22 two weeks earlier. The trend is widening, not contracting. The ASX 200 sits 6-8% below its 2 March 2026 all-time high, and the RBA cash rate remains at 4.35% with no confirmed pivot signal.

The current week’s 27 new lows against zero new highs in four sectors follows a two-to-one ratio of lows to highs that was already visible in the week ending 1 May 2026, when eleven ASX 200 names hit annual highs, all concentrated in lithium and materials, while twenty-two hit annual lows across consumer and health-care names, confirming that the rotation away from domestic consumer exposure toward commodity-linked names has been building across multiple consecutive weeks.

Some oversold indicators are flashing. Market Index and CommSec commentary have noted that parts of the discretionary and real-estate sectors appear oversold on technical measures. The Westpac-Melbourne Institute Consumer Sentiment Index bounced 3.5% in the prior week. Morningstar Australia has flagged certain discretionary and real-estate names as trading at discounts to assessed fair value since mid-to-late 2025, though this assessment is conditional on macro stabilisation.

These signals look like capitulation. They are not, at least not yet.

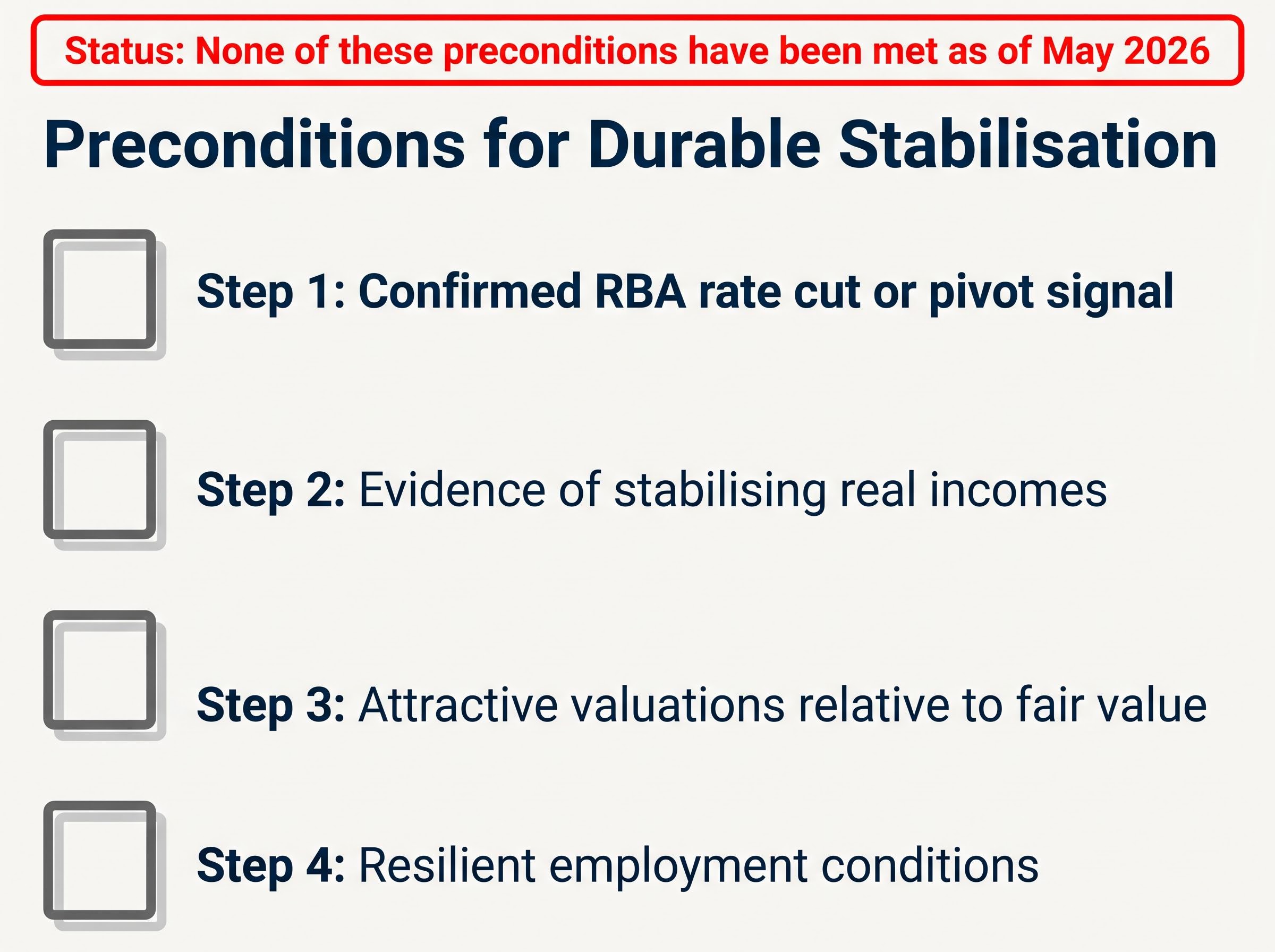

Oversold conditions alone do not constitute a durable bottom. According to analysis from NAB Markets and ANZ Research, a sustained rally requires clearer evidence of RBA easing or pivot, accompanied by improving consumer confidence and retail sales data. The following four preconditions are consistently cited as necessary for durable stabilisation in rate-sensitive ASX sectors:

None of these preconditions have been met as of May 2026. For investors deciding whether to add exposure to beaten-down sectors or maintain defensive positioning, this distinction between “oversold” and “bottomed” is the most actionable takeaway from the current data.

The week’s damage separates into two distinct categories of risk that require different responses.

Idiosyncratic catalysts:

Systemic macro pressure:

Energy and Utilities were the only sectors recording new highs with zero new lows, supported by geopolitical and yield tailwinds that provided a stark contrast to the domestic consumer story.

Energy and Utilities holding positive breadth while Consumer Discretionary, Health Care, and Staples accumulate new lows is precisely the pattern a sector rotation framework would predict at this stage of the cycle: late-cycle positioning typically sees capital move toward energy, commodities, and yield-defensive names as rate pressure compresses consumer and growth-oriented sectors before any official recession declaration arrives.

The distinction matters for positioning. Isolated stock-specific failures may represent opportunities for patient investors willing to assess whether the damage is temporary. Systemic sector-wide pressure requires waiting for macro conditions to shift before re-entering with conviction.

Watchpoints for the weeks ahead:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

A 52-week low means a stock has fallen to its lowest traded price over the past year, often signalling deteriorating fundamentals, negative earnings surprises, or broader sector selling pressure that has overwhelmed buyer demand.

Brambles fell 20.2% in a single session after management cut FY26 guidance, reducing underlying profit growth expectations from 8-11% down to 3-5%, with the downgrade attributed to repair-capacity constraints that prevented the company from meeting customer demand.

According to analysis cited in the article, four conditions are required for durable stabilisation: a confirmed RBA rate cut or pivot signal, evidence of stabilising real incomes, attractive valuations relative to fair value with stable macro conditions, and resilient employment data preventing a broader economic contraction.

Consumer Discretionary recorded 8 new 52-week lows with zero new highs, while Consumer Staples, Health Care, Real Estate, and Technology also contributed new lows, with only Energy and Utilities recording positive breadth during the same period.

An oversold stock has fallen sharply and may appear cheap on technical measures, but a genuine bottom requires the underlying macro or fundamental conditions driving the decline to stabilise or reverse; as the article notes, none of the four key recovery preconditions had been met for rate-sensitive ASX sectors as of May 2026.